A-level economics - Price determination in a competitive market

1/64

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

65 Terms

market

where buyers and sellers meet to exchange goods and services

why prices rise (demand and supply)

if there is an increase in demand or a fall in supply of a particular good or service, the prices rise

why prices fall (demand and supply)

if there is an decrease in demand or a rise in supply of a particular good or service, the prices fall

demand

the amount of a specific good or service that consumers are willing to buy at a specific price over a specific period of time

supply

the amount of a specific good or servce that suppliers are willing to supply to consumers at a specific price over a specific period of time

factors that will influence supply

- The amount produced at any given time

- The amount that it costs to produce a product

- Productivity of the work force

- taxes and subsides

- Conflict of interest/ what to produce

- New competition

- price

-productivity of workers

- compettion

- seasons

- conflicts

- cost of production

- technology

Factors that will influence demand

- The amount that a consumer is willing to pay for a product

- The cost of alternatives

- The quality of the product

- The time of year

- Rising or falling costs

- Prices of competitors product products/ derived demand

- quality

- price of complements

- derived demand

- tastes and preferences

- income levels

- price of substitutes

- price of the product

- normal goods

- inferior goods

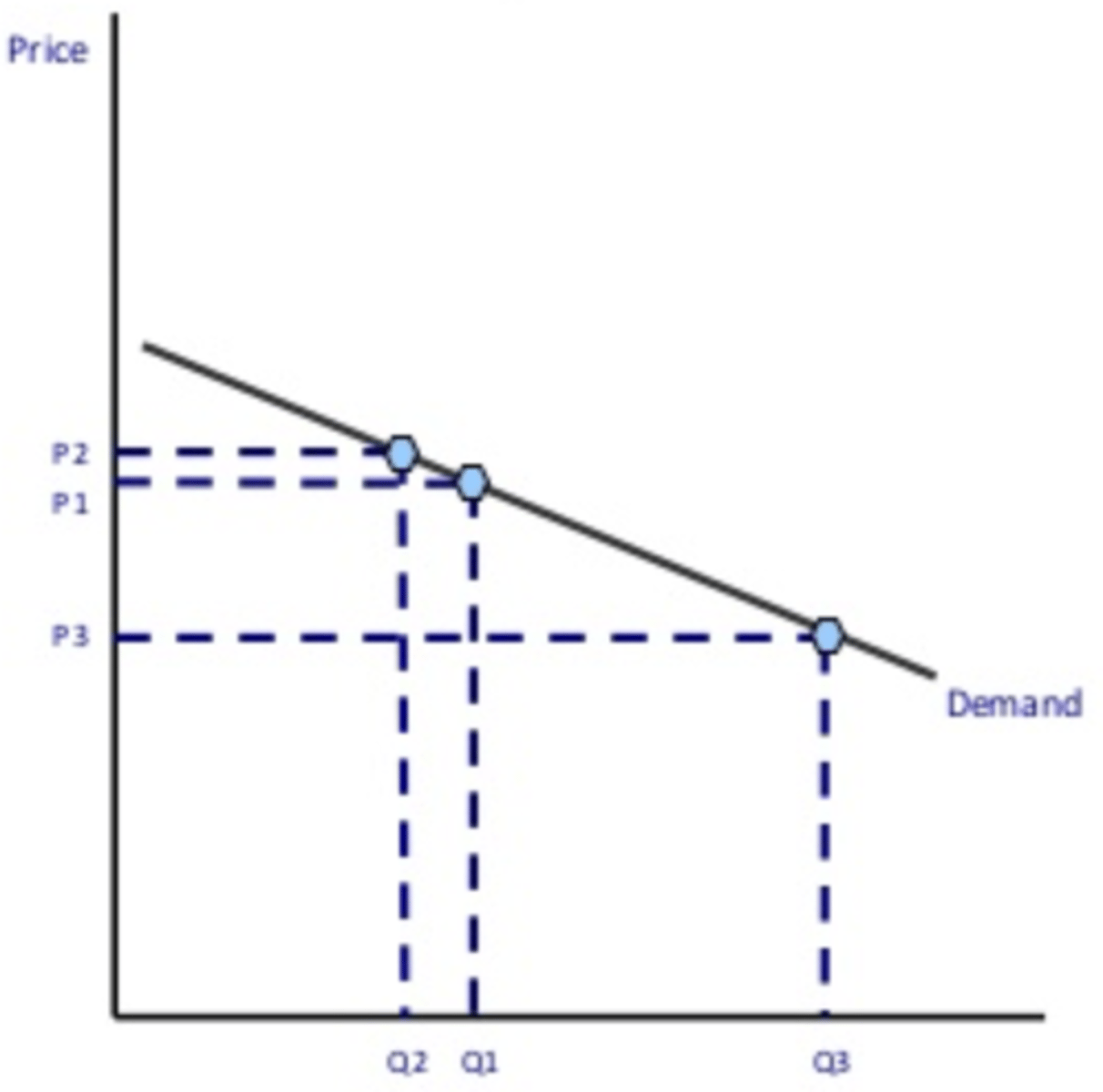

demand curve

shows the relationship between the price and quanitiy of demand. as price falls, demand rises, moving the curve to the left. effected by income and substitutions

substitution effects/ income effect

the economic understanding that as prices rise — or income decreases — consumers will replace more expensive items with less costly alternatives.

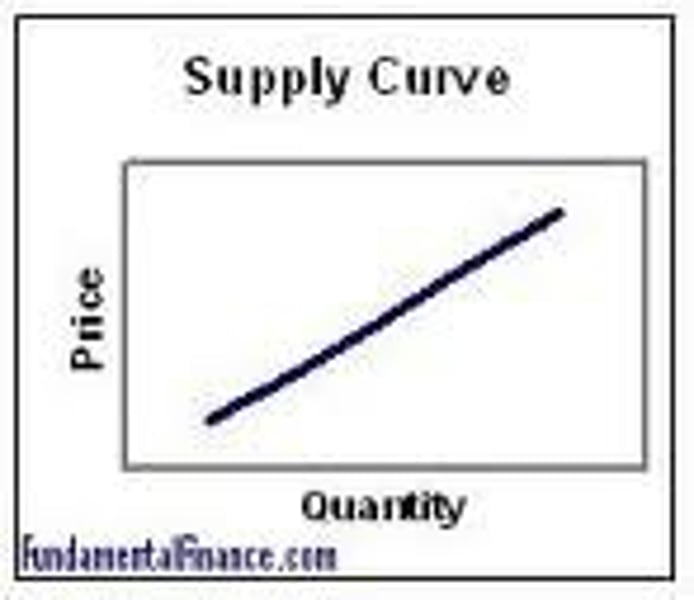

supply curve

why the supply curve moves upwards

-direct / positive relationship between price and supply

- profit revenue to sell stuff at a higher price

equilibrium

a point at which there is a balance or rest and at which there is a tendency for change

- demand = supply

ceteris paribus

the commonly used Latin phrase meaning 'all other things remaining constant'. so basically, most things are constant

Movement along a demand curve

when the price of the good changes and the quantity demanded changes in accordance to the original demand relationship.

complements (joint demand)

the relationship between two or more commodities or services when they are demanded together. There is joint demand for cars and petrol, pens and ink, tea and sugar, etc. These goods also have a negative cross elasticity of demand, in contrast to a substitute good. This means a good's demand is increased when the price of another good is decreased. When two goods are complements, they experience joint demand.

factors in a Shift right in demand

- Decrease in price of a substitute.

- Increase in price of a complement.

- Decrease in income if good is normal good.

substitutes (competitive demand)

A substitute product is a product from another industry that offers similar benefits to the consumer as the product produced by the firms within the industry. These goods have a positive cross elasticity of demand. This means a good's demand is increased when the price of another good is increased; both in the same direction.

composite demand

when goods or services have more than one use so that an increase in the demand for one product leads to a fall in supply of the other. E.g. milk which can be used for cheese, yoghurts, cream, butter and other products.

joint supply

a product or process that can yield two or more outputs. Common examples occur within the livestock industry: cows can be utilized for milk, beef and hide; sheep can be utilized for meat, milk products, wool and sheepskin.

derived demand

demand that comes from (is derived) from the demand for something else. Thus, the demand for machinery is derived from the demand for consumer goods that the machinery can make. If there is low demand for consumer goods, there is low demand for the machinery that can make them. Demand for bricks is derived from spending on new construction projects.

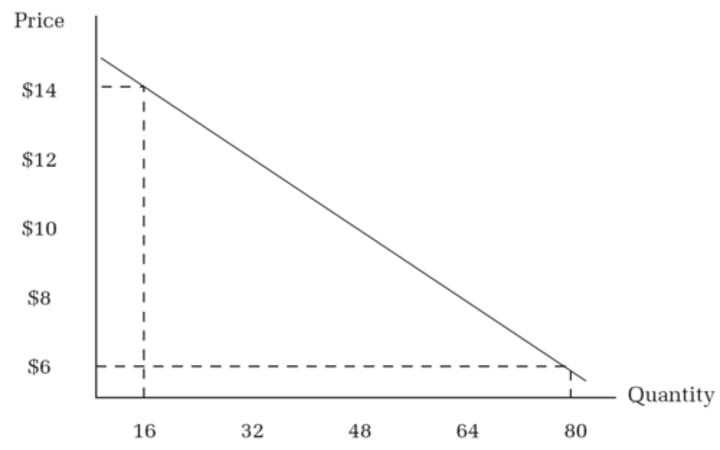

price elasticity of demand (PED)

the responsiveness of demand after a change in a product's own price. PED usually has a negative for there being a change in price and as the price increses, the quantity increses

price elasticity of demand calculations

% change of the quantiy demanded/ % change in price = PED

-Change price first

values for price elasticity of demand

- PED = 0

- PED < 1

- PED = 1

- PED > 1

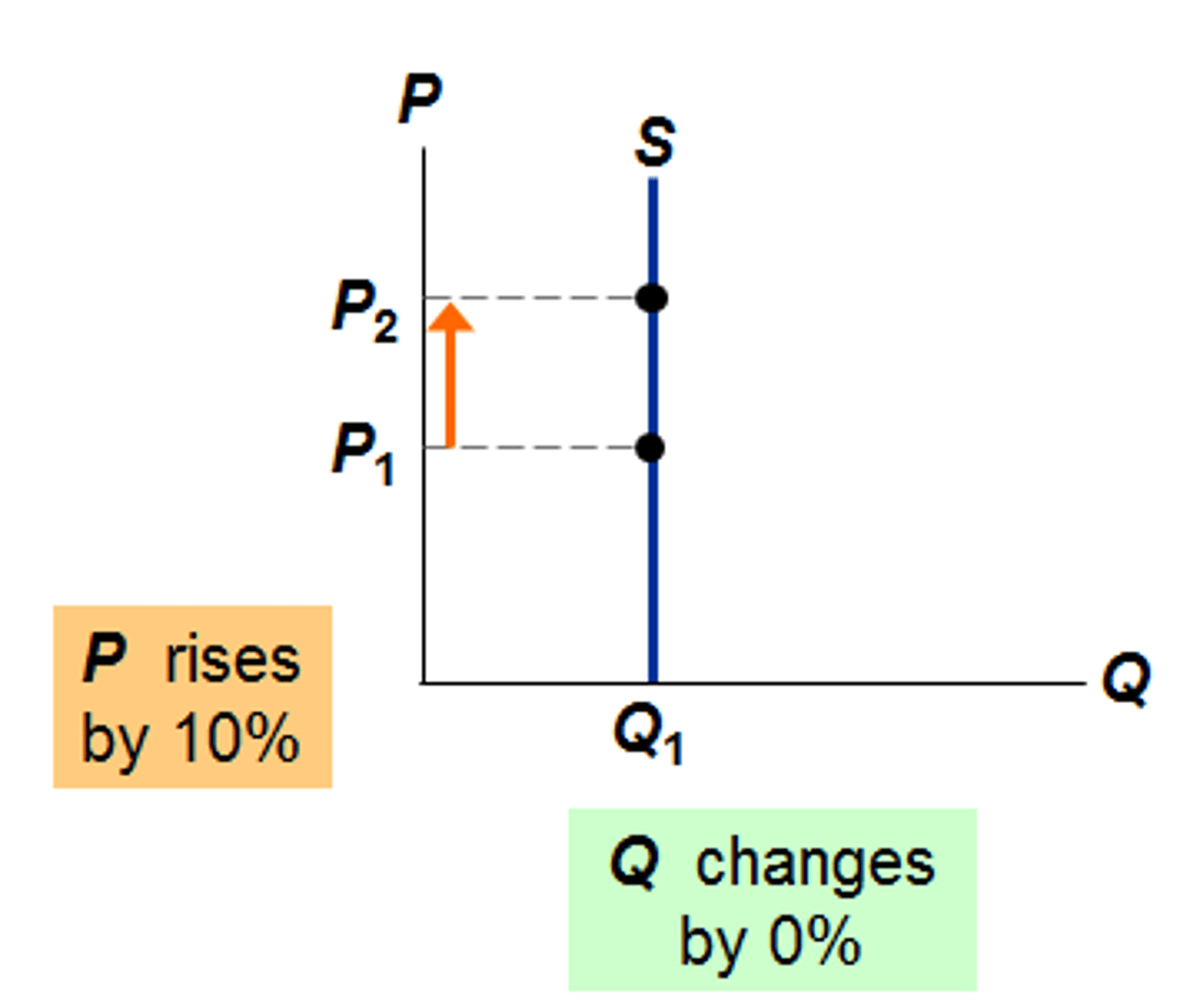

values for price elasticity of demand - PED = 0

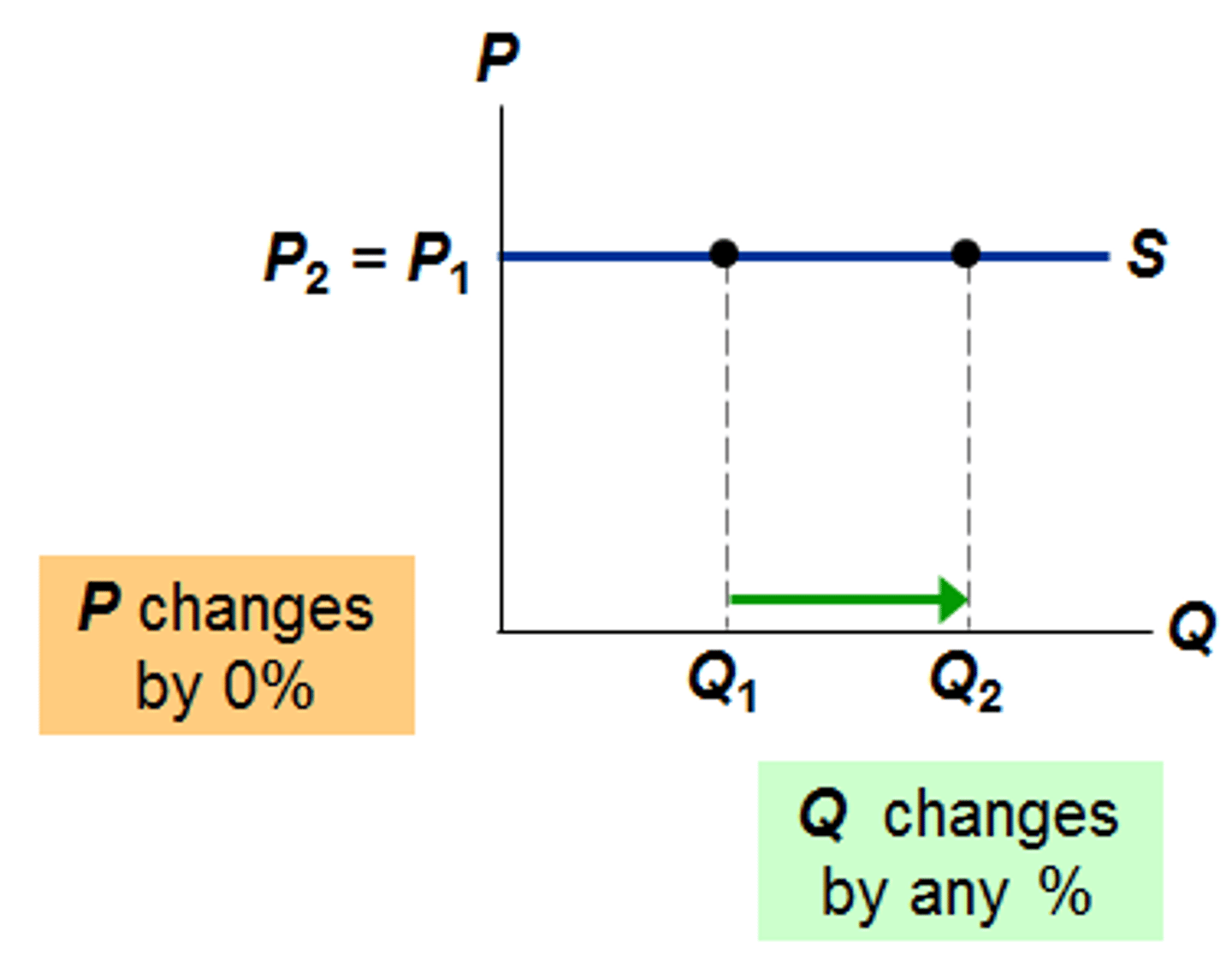

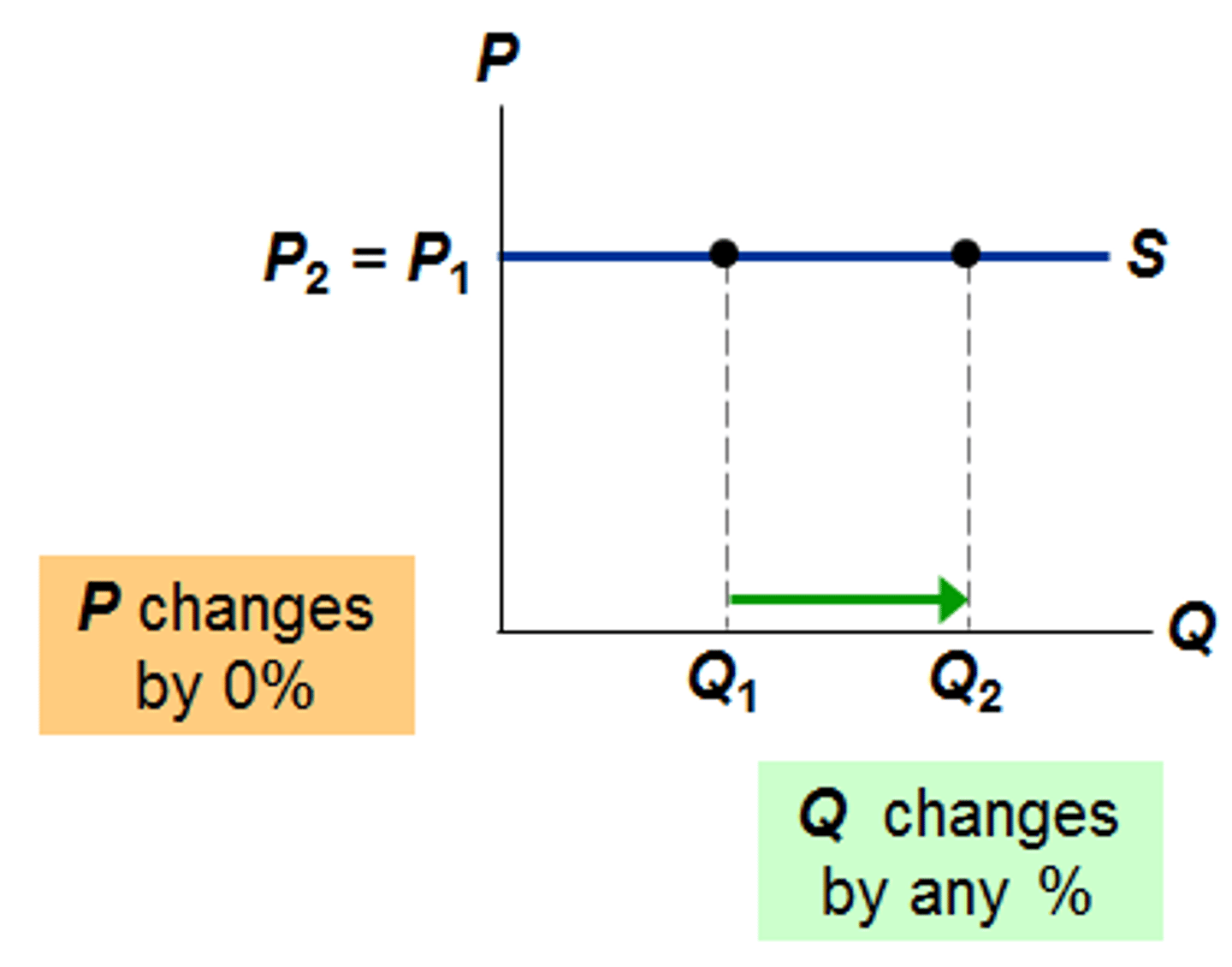

demand is perfectly inelastic - demand does not change at all when the price changes - the demand curve will be vertical.

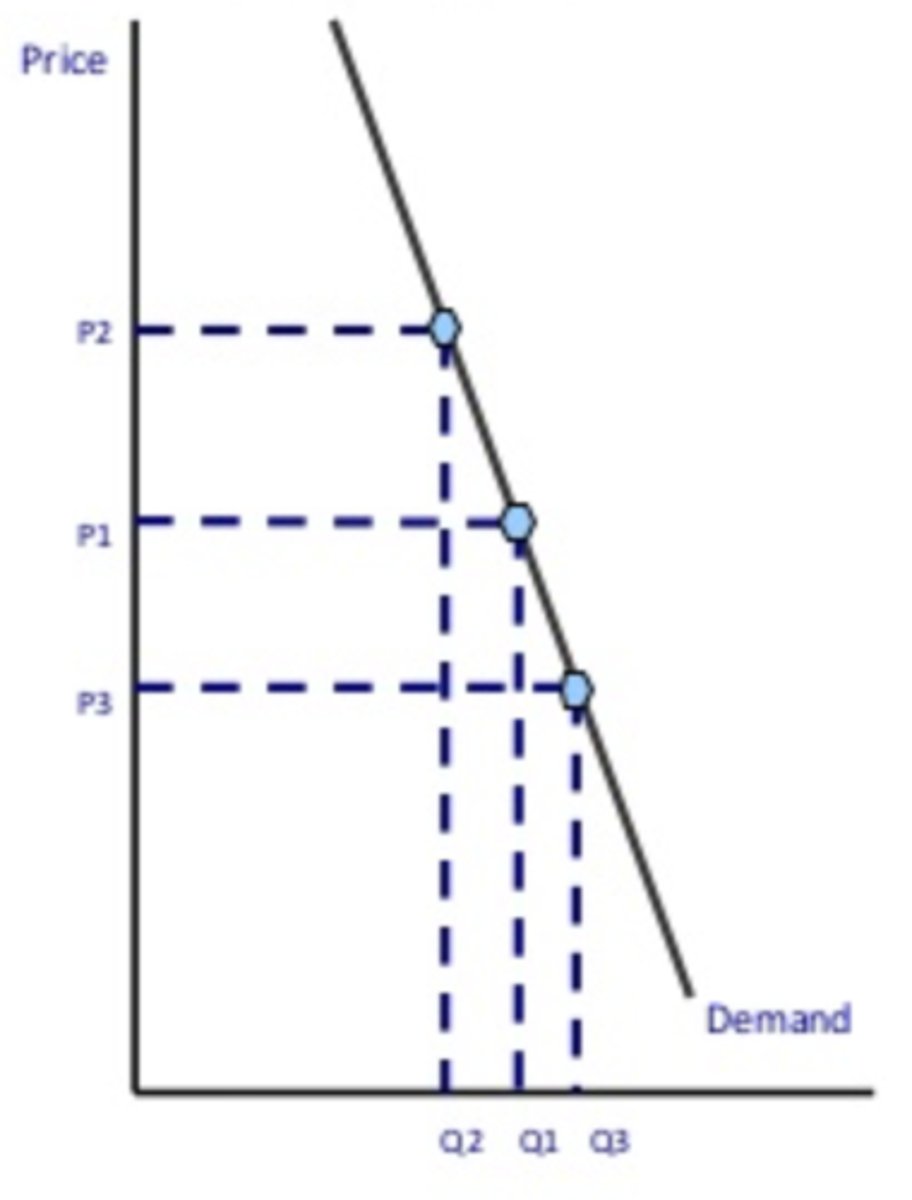

values for price elasticity of demand - PED < 1

then demand is inelastic.

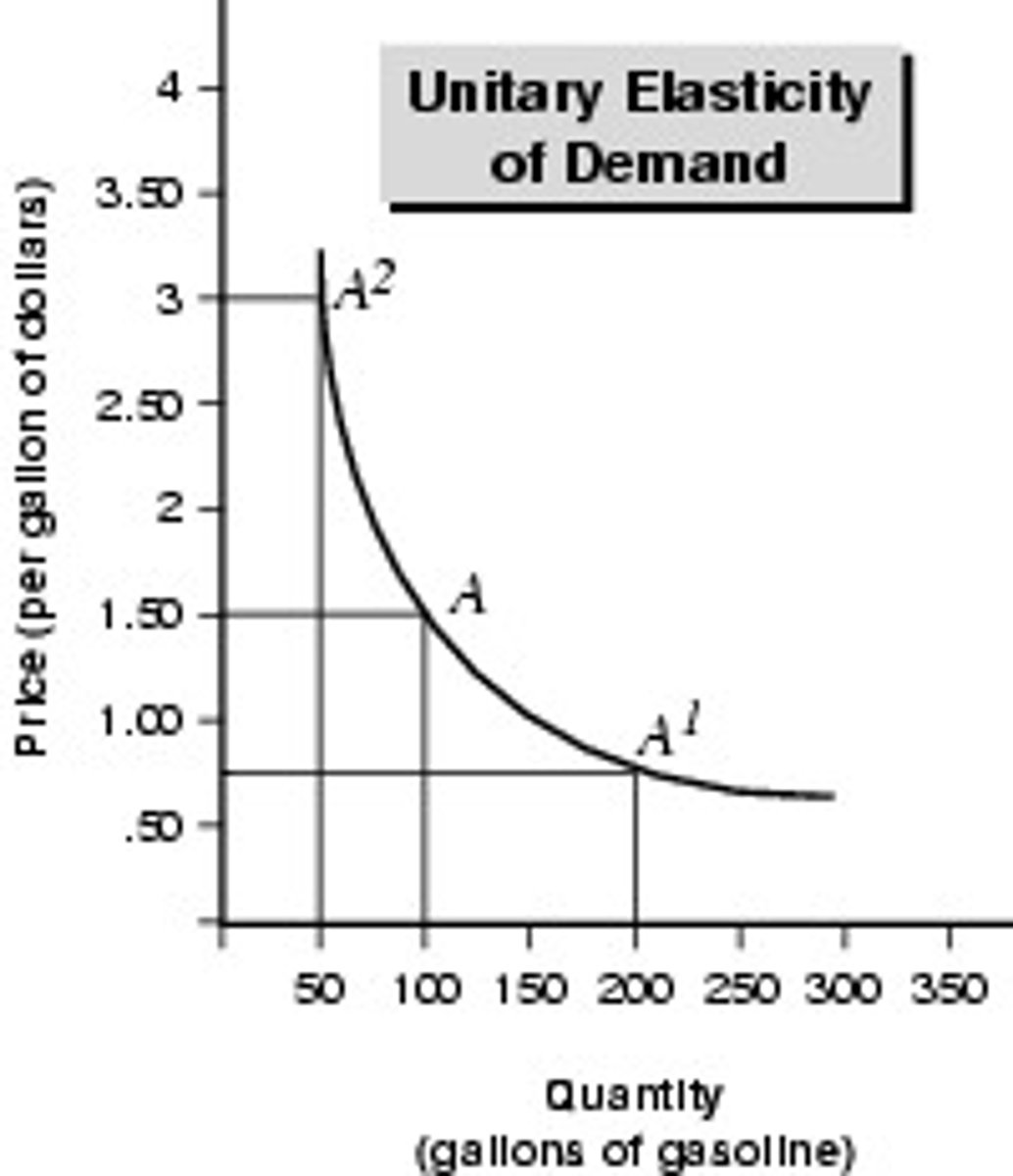

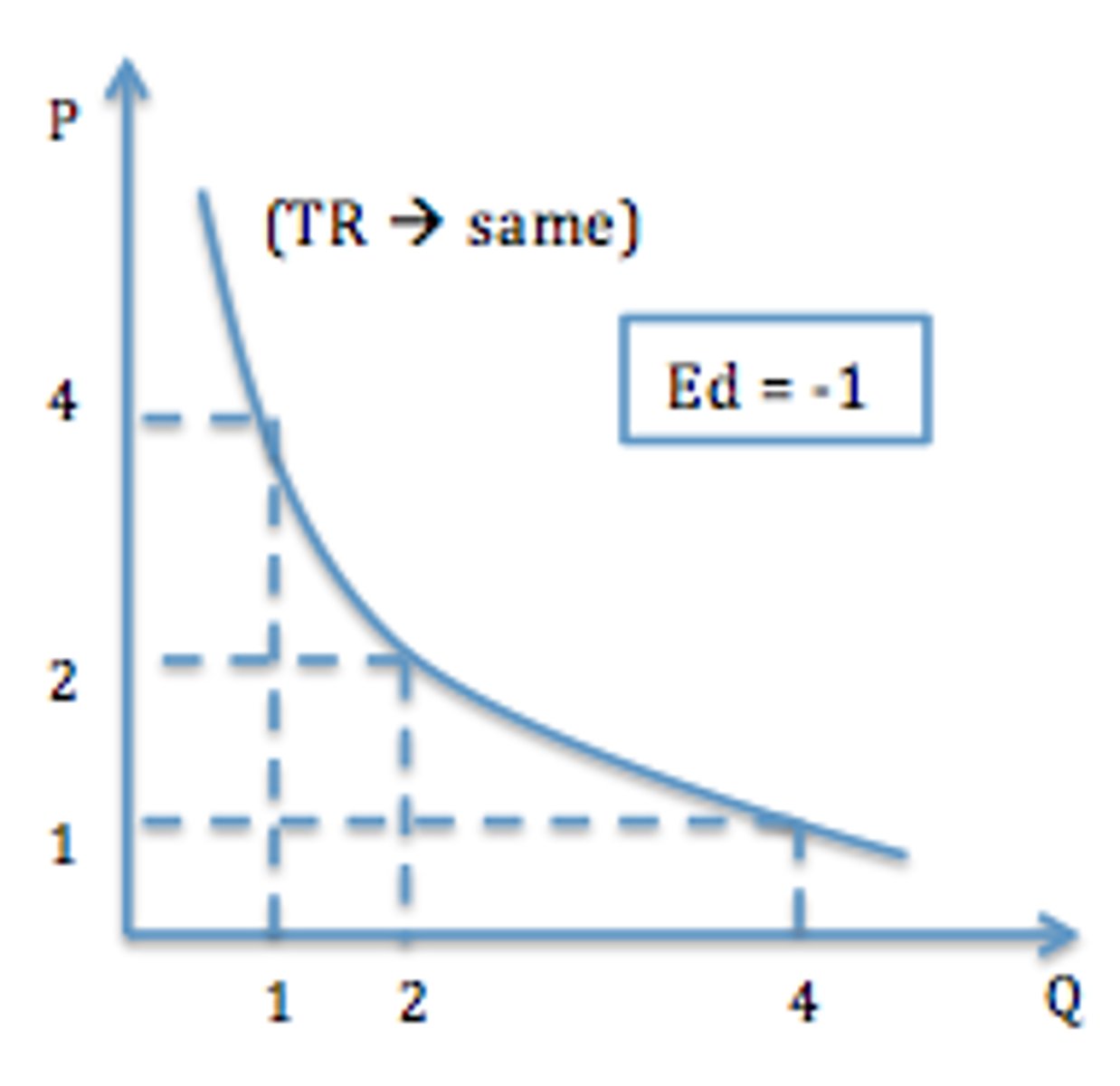

values for price elasticity of demand - PED = 1

then demand is unit elastic. A 15% rise in price would lead to a 15% contraction in demand leaving total spending the same at each price level.

values for price elasticity of demand - PED > 1

then demand responds more than proportionately to a change in price i.e. demand is elastic.

factors effecting the elasticity of demand

- substitutes

- long term or short term (the time period)

- percentage of consumer income

- brand loyalty

- peak/ off peak times

- whether a good is a luxury or a necessity

perfectly elastic

relatively elastic

unitary elastic

relatively inelastic

completely inelastic

income elasticity of demand (YED)

a measures of the responsiveness of the quantity demanded for a good or service to a change in the income of the people demanding the good. It is calculated as the ratio of the percentage change in quantity demanded to the percentage change in income.

normal goods

any good for which demand increases when income increases, i.e. with a positive income elasticity of demand.

necessities

a type of normal good. Like any other normal good, when income rises, demand rises. But the increase for a necessity good is less than proportional to the rise in income, so the proportion of expenditure on these goods falls as income rises.

normal good

a good for which demand increases more than proportionally as income rises, and is a contrast to a "necessity good", for which demand increases proportionally less than income. Luxury goods are often synonymous with superior goods and Veblen goods.

inferior goods

a good whose demand decreases when consumer income rises (or demand rises when consumer income decreases), unlike normal goods, for which the opposite is observed. Normal goods are those for which demand rises as consumer income rises.

income elasticity of demand (YED) calculation

% change in quantity demanded ÷ % in real income = YED

values for income elasticity of demand

- YED < +1

- YED > + 1

- YED < 0

income elasticity of demand - YED < +1

- normal goods

- e.g. 0.1 = an increse by 1%

income elasticity of demand - YED < 0

- Luxury goods and services

- e.g. 2 = an increase by 20%

income elasticity of demand -YED > + 1

- inferior goods

- e.g. -0.5 = a decrease of 12.5%

- e.g .-2 = a decrease of 40%

YED goods (positive/ negative/ ect...)

+ = normal goods (elastic)

- = inferior (inelastic)

+>1 = luxury (elastic)

close to 0 = necessity

cross elasticity of demand

measures the responsiveness of the quantity demanded for a good to a change in the price of another good, ceteris paribus.

uses of cross elasticity of demand

allows forms to create strategies to reduce its exposure to the risks that associates with a change in price

goods used in cross elasticity of demand

- complements (negative)

- substitutes (positive)

cross elasticity of demand - complements

- negative

- the price increase for one good causes a decrease in the quantity demeaned for another

- XED < 1 inelastic

cross elasticity of demand - substitutes

- positive

- the increased price of one good will lead to the increased demanded for another on

- XED > 1 elastic

values for cross elasticity of demand

- XED > 1

- XED < 1

cross elasticity of demand (XED) calculation

% change in the quantity demanded of good 1 ÷ % change in the price of good 2 = XED

price elasticity of supply (PES)

a measure used in economics to show the responsiveness, or elasticity, of the quantity supplied of a good or service to a change in its price

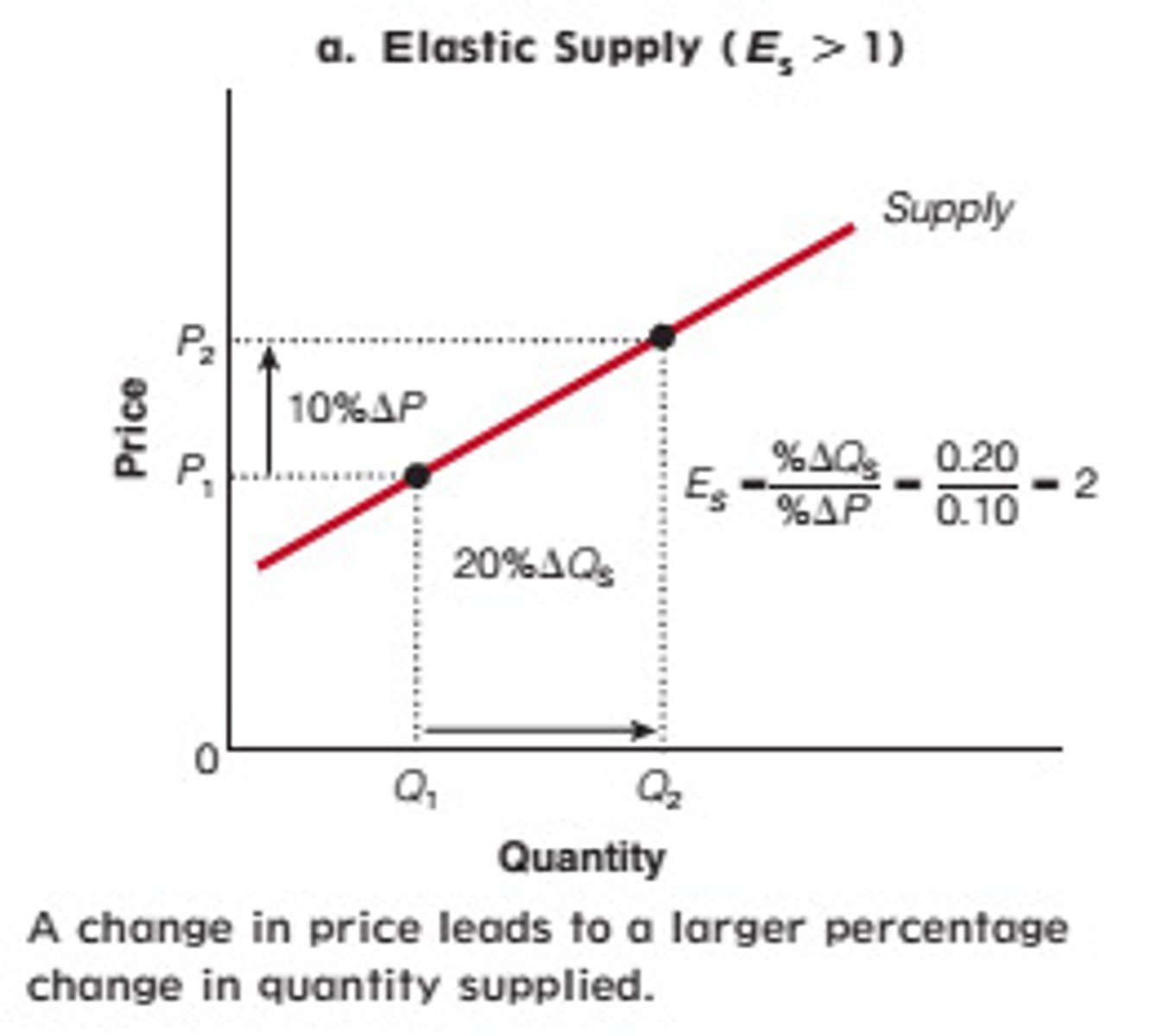

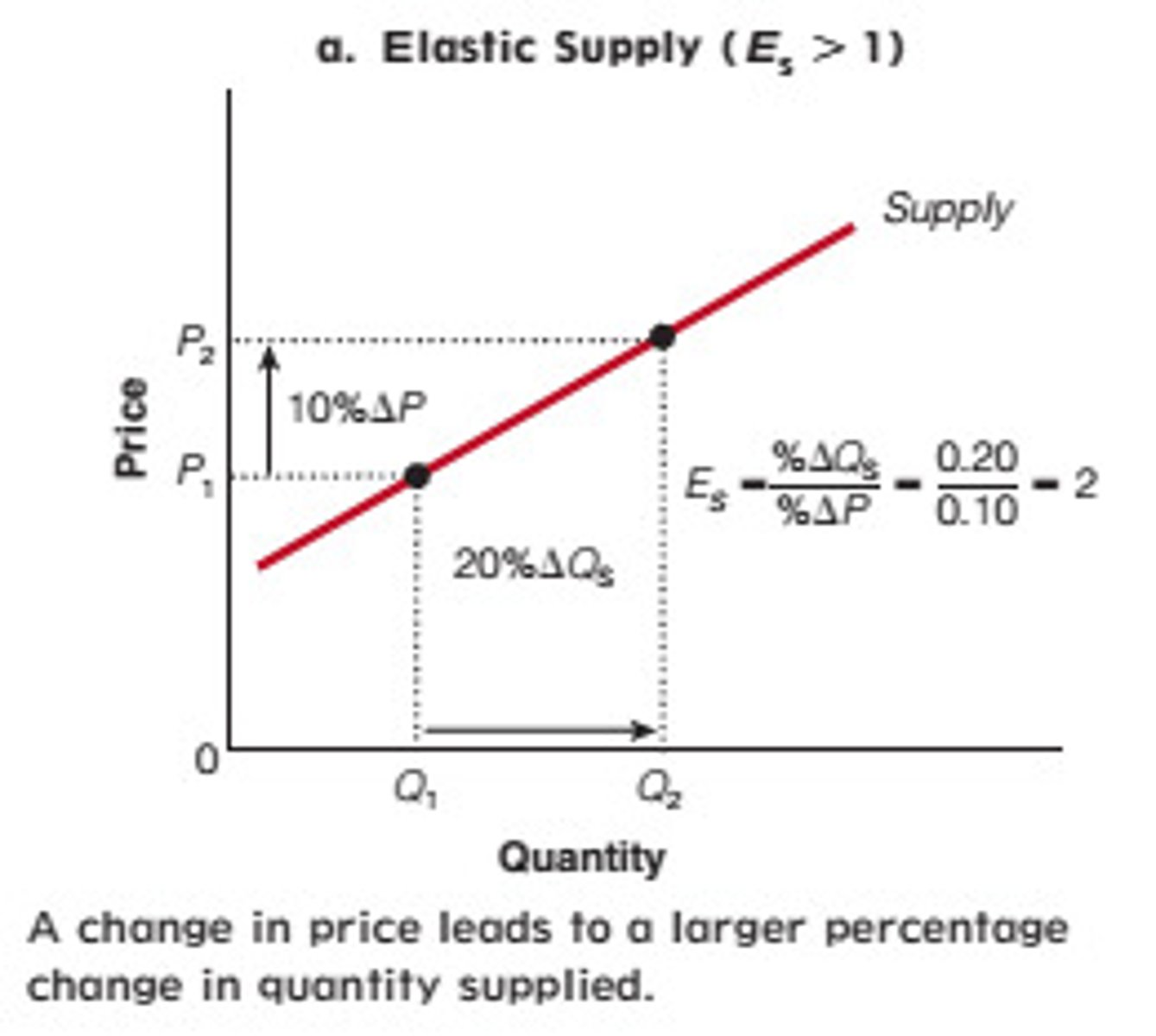

price elasticity of supply (PES) calculation

% change in quantity supplied ÷ % change in price = PES

factors that effect price elasticity of supply (PES)

- availability of resources

- levels of stock

- the ease and cost of factor substitution/mobility

- capacity of utilisation

- Time period and production speed

factors that effect price elasticity of supply - availability of resources

depending on how difficult it is to access the resources, demand may vary elasticity

factors that effect price elasticity of supply - levels of stock

If stocks of raw materials and finished products are at a high level then a firm is able to respond to a change in demand - supply will be elastic. Conversely when stocks are low, dwindling supplies force prices higher because of scarcity

factors that effect price elasticity of supply - capacity of utilisation

higher capacity utilisation means supply is more inelastic

factors that effect price elasticity of supply - the ease and cost of factor substitution/mobility

both capital and labour are occupationally mobile then the elasticity of supply for a product is higher than if capital and labour cannot easily be switched. E.g. a printing press which can switch easily between printing magazines and greetings cards. Or falling prices of cocoa encourage farmers to switch into rubber production

factors that effect price elasticity of supply - Time period and production speed

Supply is more price elastic the longer the time period that a firm is allowed to adjust its production levels. In some agricultural markets the momentary supply is fixed and is determined mainly by planting decisions made months before, and also climatic conditions, which affect the production yield. In contrast the supply of milk is price elastic because of a short time span from cows producing milk and products reaching the market place.

values of price elasticity of supply (PES)

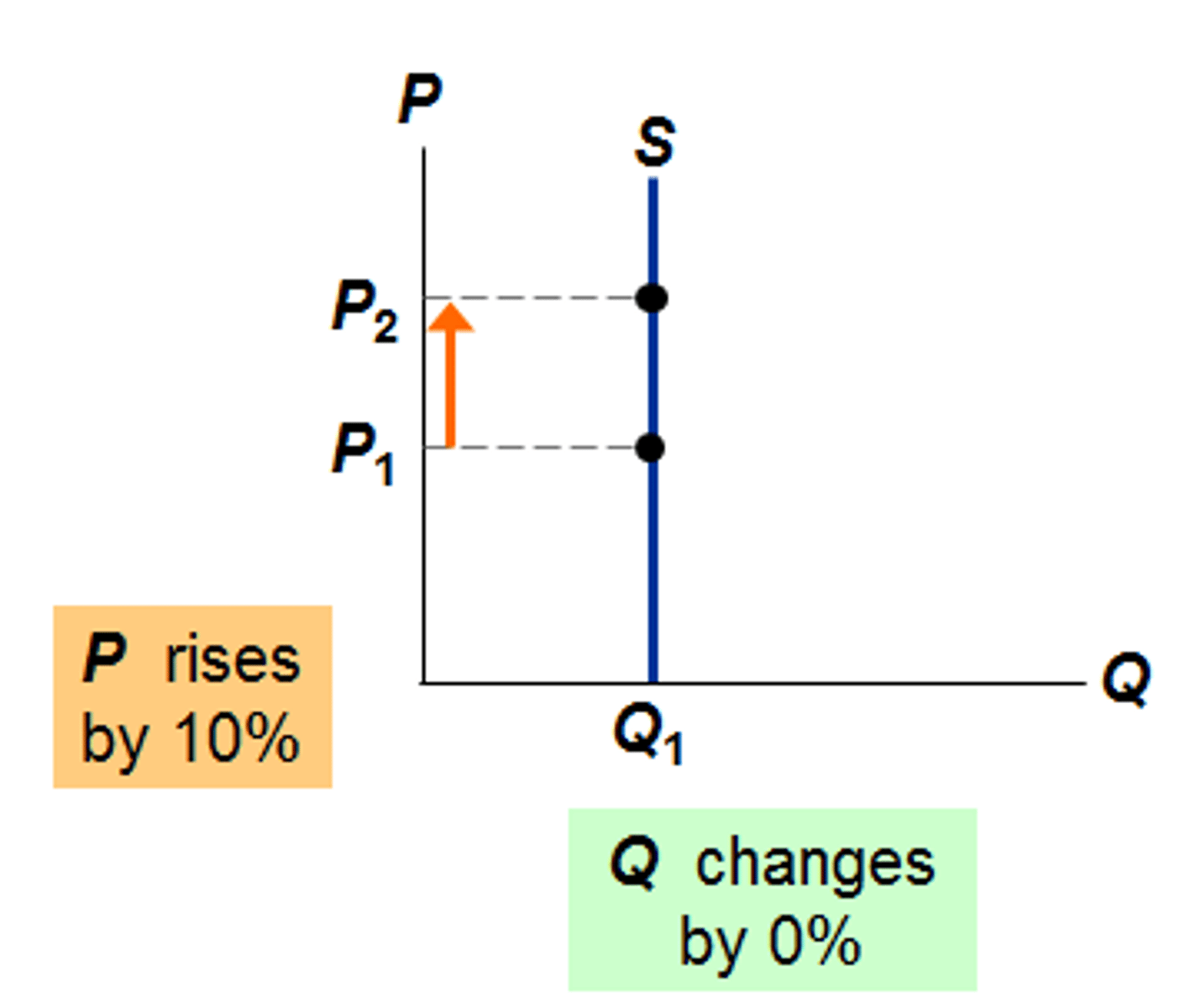

- PES = 0

- PES < 1

- PES = 1

- PES > 1

- PES = INFINITY

values of price elasticity of supply

completely inelastic

values of price elasticity of supply - PES < 1

relatively inelastic

values of price elasticity of supply - PES = 1

unitary

values of price elasticity of supply - PES > 1

relatively elastic

values of price elasticity of supply - PES = INFINITY

perfectly elastic