Chapter 2

1/25

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

26 Terms

6 steps in measuring external transactions (a)

Use source documents to identify accounts affected by an external transaction

Analyze the impact of the transaction on the accounting equation

Assess whether the transaction results in a debit or credit to account balances

6 steps in measuring external transactions (b)

Record the transaction in a journal using debts and credits

Post the transaction to the general ledger

Prepare a trial balance

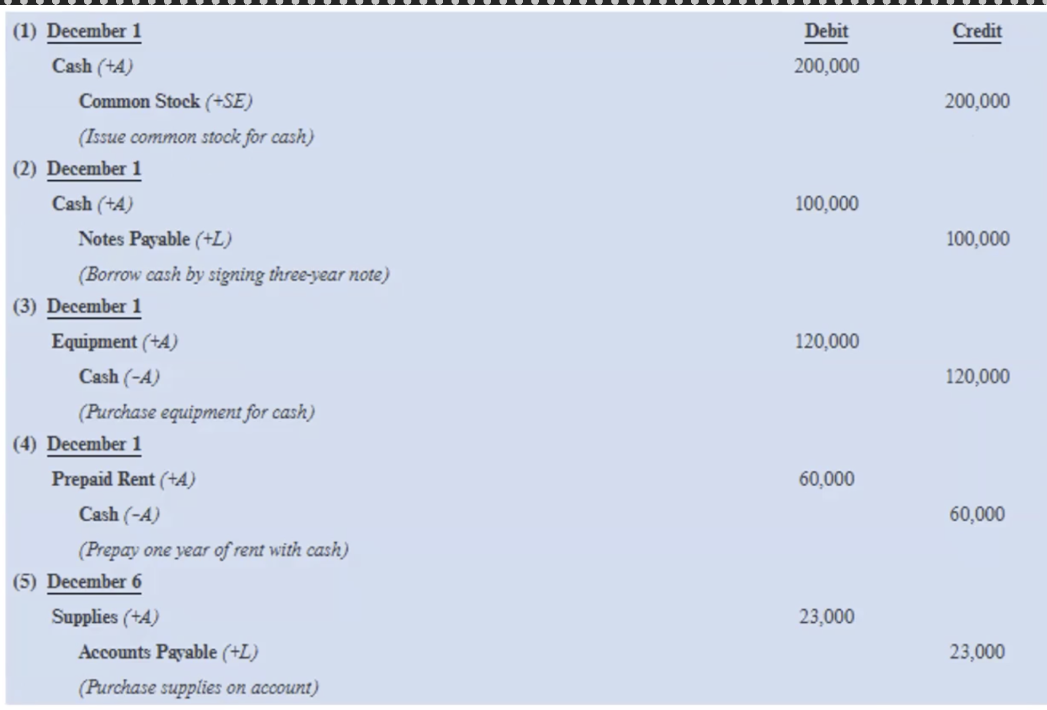

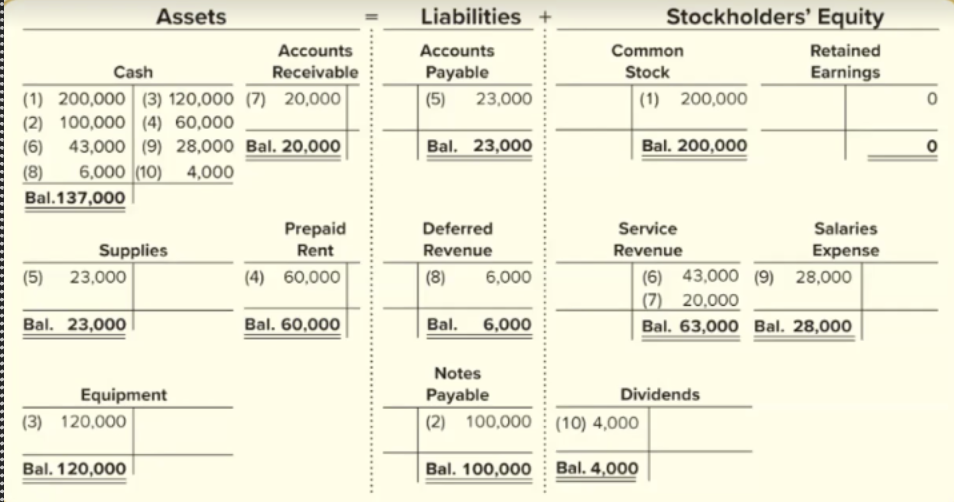

Transaction #1 Issue Common Stock

Company receives 200k cash from investors who in turn become owners of company receiving shares of common stock

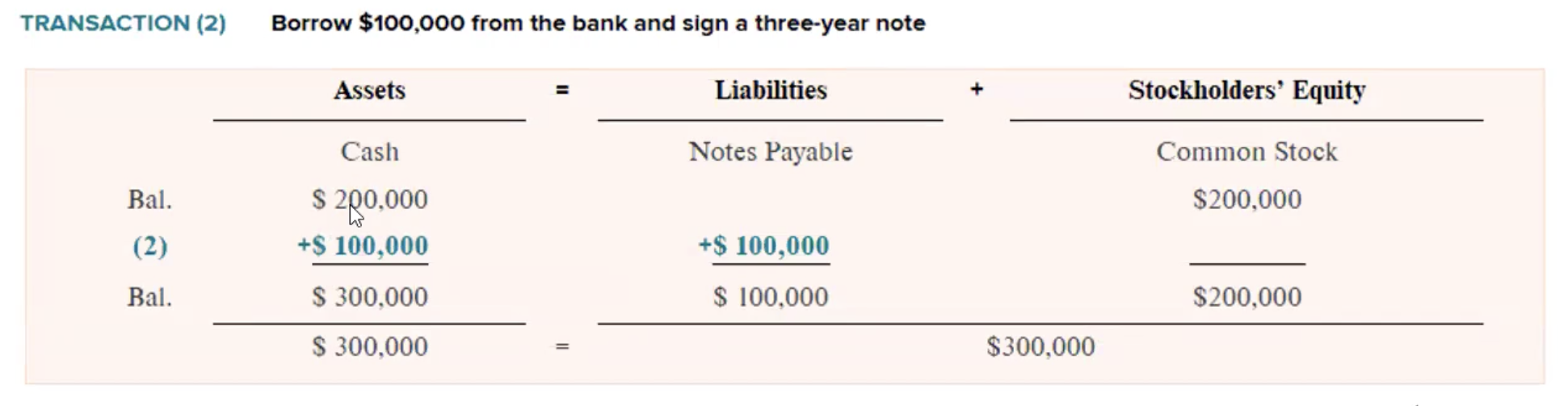

Transaction #2 Borrow cash from the bank

Eagle borrows 100k from bank

Signs a note to repay the loan amount in 3 years

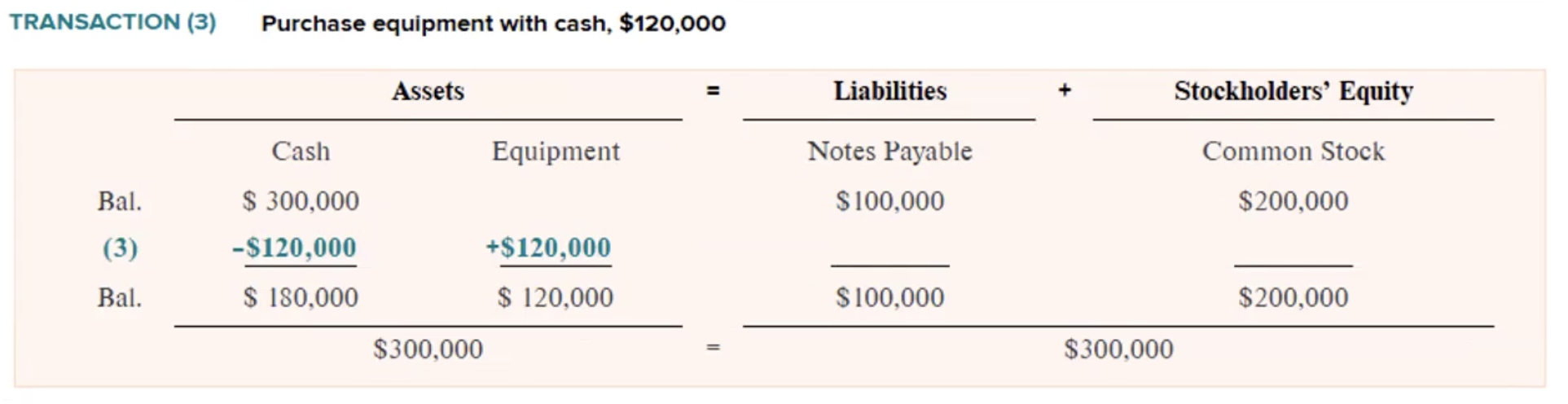

Transaction #3 Purchase Equipment

Eagle purchases 120k in equipment

Causes one asset (equipment) to increase and another asset (cash) to decrease

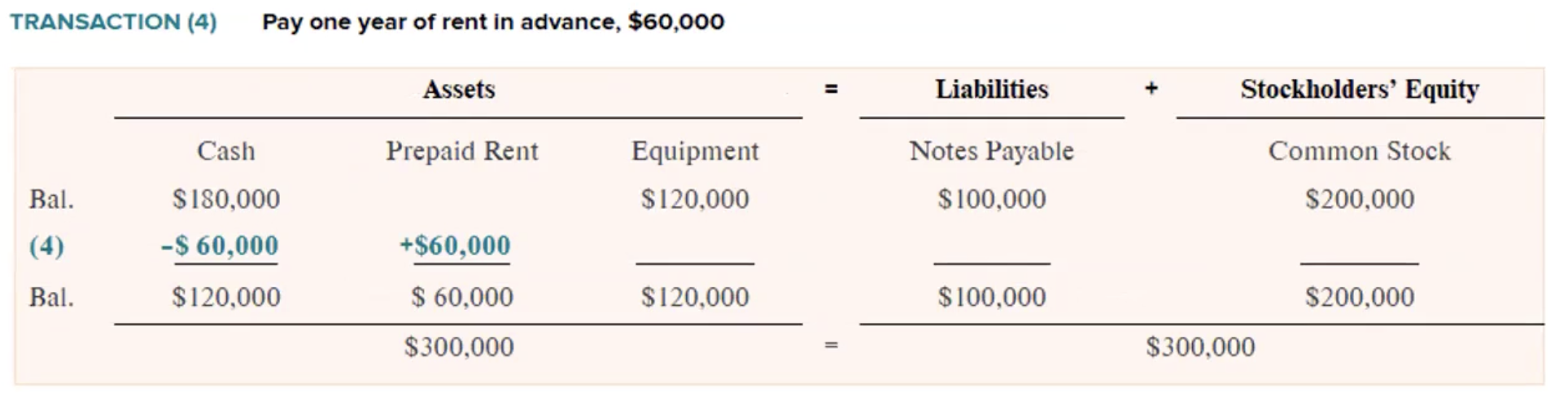

Transaction #4 Pay for rent in advance

Eagle pays 1 year of rent in advance, 60k (5k/month)

Bc rent paid is occupying space in future its listed as a resource (prepaid rent)

Asset cash decreases and asset prepaid rent increases

Types of prepaid things

prepaid insurance, prepaid advertising, prepaid rent and other prepaid services

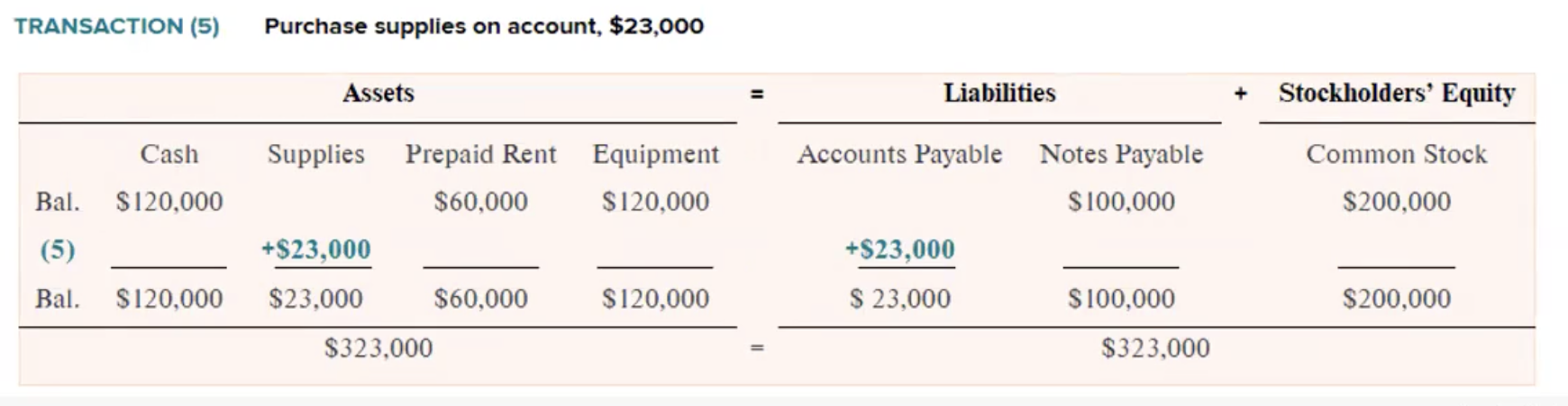

Transaction #5 Purchase supplies on account

Company purchases 23k of supplies on account

Supplies are an asset and the liability is accounts payable

On account

means that company does not pay cash immediately but promises to pay cash in the future

keeps record of companies u will may in future

is like paying w a credit card

Accounts payable vs Notes payable

accounts is paid in 30 days

notes payable may take more than 12 months to pay

Basic accounting equation and expanded accounting equation

If revenue goes up so does net income, then retained earnings, this makes SE go up

If expense goes up, net income, retained earnings, and SE go down

If dividends go up, retained earnings and SE goes down

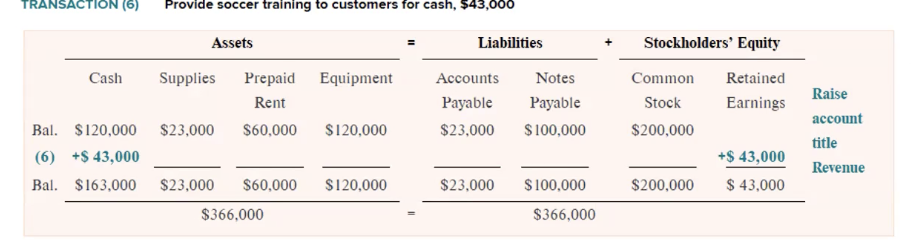

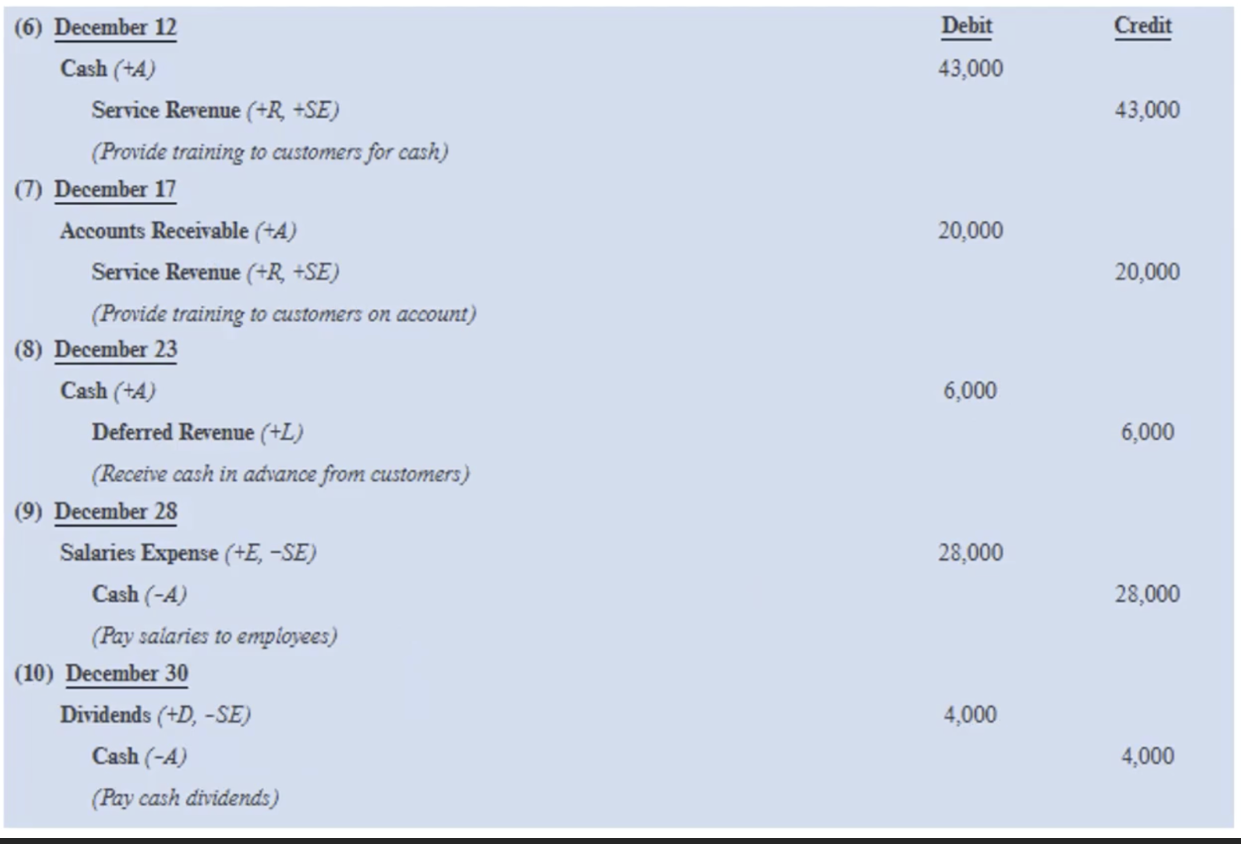

Transaction #6 Provide Services for Cash

Eagle provides 43k of services

Cash asset increases 43k and stockholders' equity increases 43k through 43k increase in retained earnings

Revenue recognition principle

companies recognize revenue at the time they provide goods and services to customers

Amount of revenue to recognize equals the amount of the company is entitled to receive from customers

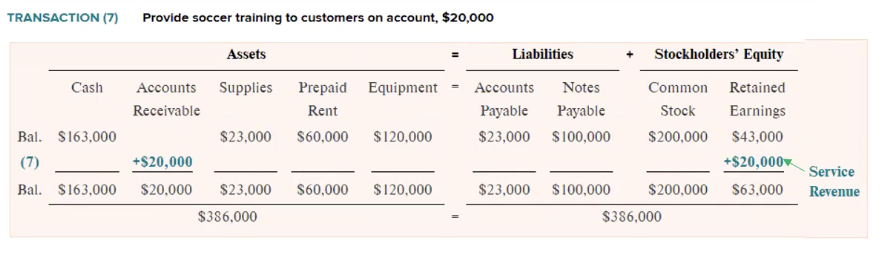

Transaction #7 Provide Services on Account

Customers receive services but don’t pay at time of service, instead pay 20k cash at some other point in time

20k increase in accounts receivable (assets) and 20k increase in stockholders' equity (retained earnings – listed as service revenue)

Transaction #8 Receive Cash In Advance From Customers

Receive 6k of cash from customers in advance for soccer training to be provided later

Receiving cash in advance causes asset (cash) and liability (referred revenue) to increase

Deferred revenue

eventually will be revenue but until service is provided it’s a liability

Transaction #9 Pay Salaries to Employees

Salary expense during current month is 28k

Asset (cash) decreases and stockholders' equity decreases (salary expense in retained earnings decreases)

Transaction #10 Paying Cash Dividends

Payment of 4k cash dividend to stockholders

4k cash is lost in assets and 4k is lost in stockholders' equity (retained earnings through dividends)

Effects of credit and debit on account balances (DEALOR)

What can be listed as Assets

Cash

Accounts Receivable

Supplies

Prepaid Rent

Equipment

What can be listed as Liabilities

Accounts Payable

Deferred Revenue

Notes Payable

Format for recording transactions in a Journal

First 5 transactions in the Journal

Last 5 transactions in the Journal

Posting to the General Ledger

One side is credit side and Debits on one side

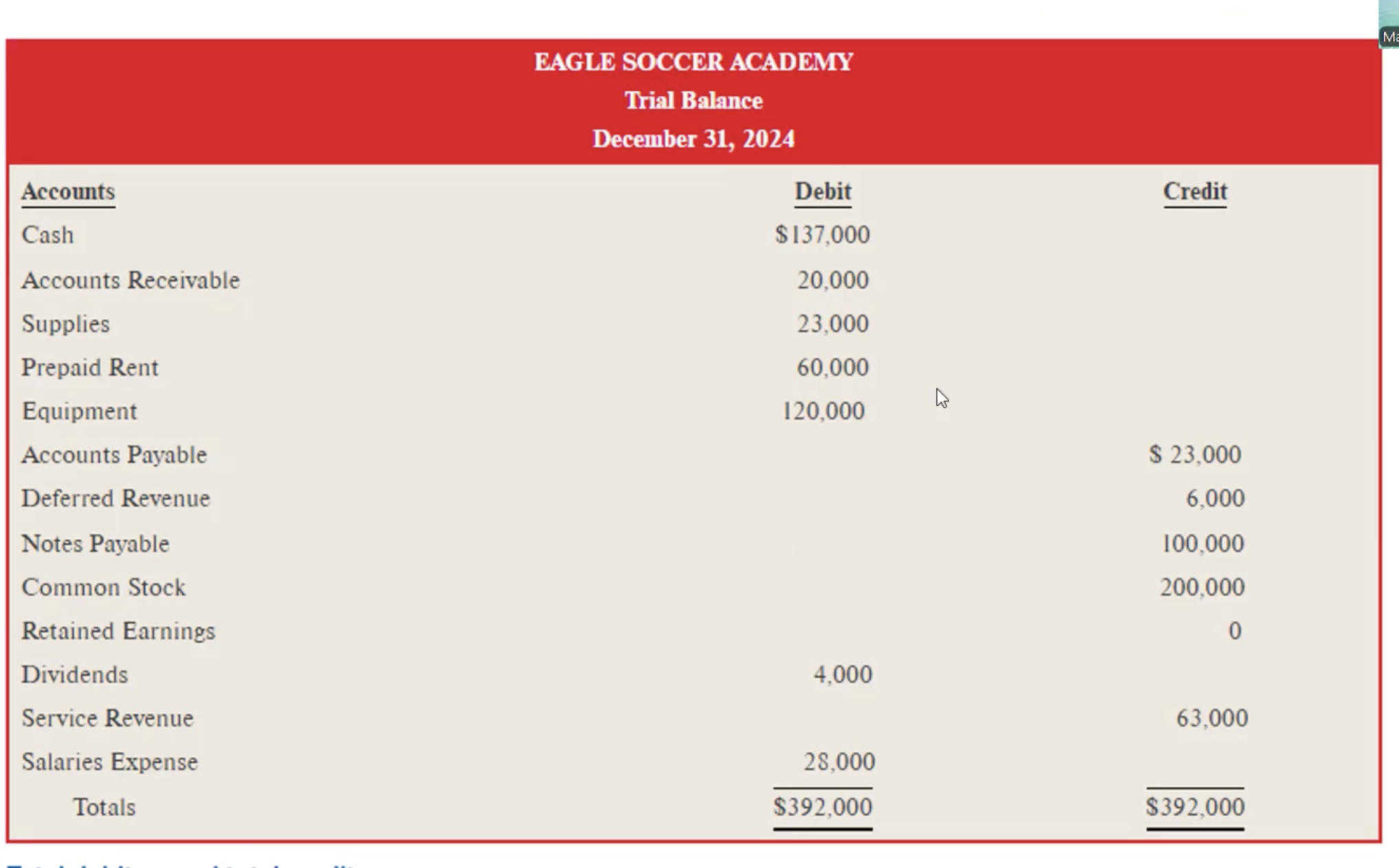

Trial balance

Splits up Debits and Credits