Econ practice set ch.1, 2, 3 & 5

1/75

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

76 Terms

constant unitary elasticity

when a given percent price change in price leads to an equal percentage change in quantity demanded or supplied

elastic demand

when the elasticity of demand is greater than one, indicating a high responsiveness of quantity demanded or supplied to changes in price

elastic supply

when the elasticity of either supply is greater than one, indicating a high responsiveness of quantity demanded or supplied to changes in price

elasticity

an economics concept that measures responsiveness of one variable to changes in another variable

inelastic demand

when the elasticity of demand is less than one, indicating that a 1 percent increase in price paid by the consumer leads to less than a 1 percent change in purchases (and vice versa); this

indicates a low responsiveness by consumers to price changes

inelastic supply

when the elasticity of supply is less than one, indicating that a 1 percent increase in price paid to the firm will result in a less than 1 percent increase in production by the firm; this indicates a low responsiveness of the firm to price increases (and vice versa if prices drop)

infinite elasticity

the extremely elastic situation of demand or supply where quantity changes by an infinite amount in response to any change in price; horizontal in appearance

AKA perfect elasticity

price elasticity

the relationship between the percent change in price resulting in a corresponding percentage

change in the quantity demanded or supplied

price elasticity of demand

percentage change in the quantity demanded of a good or service divided the percentage change in price

price elasticity of supply

percentage change in the quantity supplied divided by the percentage change in price

zero inelasticity

the highly inelastic case of demand or supply in which a percentage change in price, no matter how large, results in zero change in the quantity; vertical in appearance

allocative effciency

the channeling of resources to their most productive and desired uses

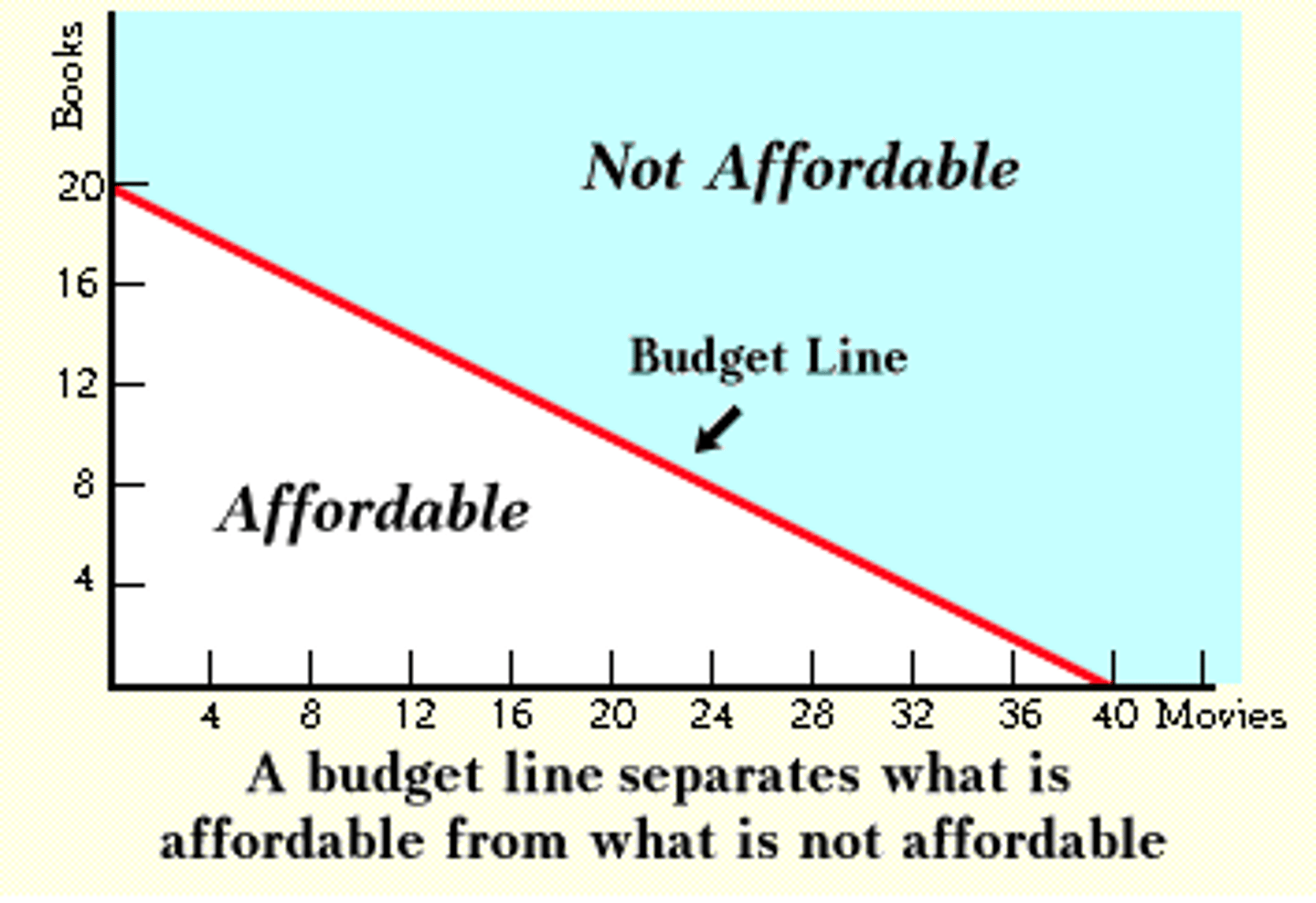

budget constraint

all possible consumption combinations of goods that someone can afford, given the prices of goods, when all income is spent; the boundary of the opportunity set

comparative advantage

when a country can produce a good with a lower opportunity cost than another country

invisible hand

Adam Smith's term for the natural self-regulation of a market economy driven by self-interest and efficiency

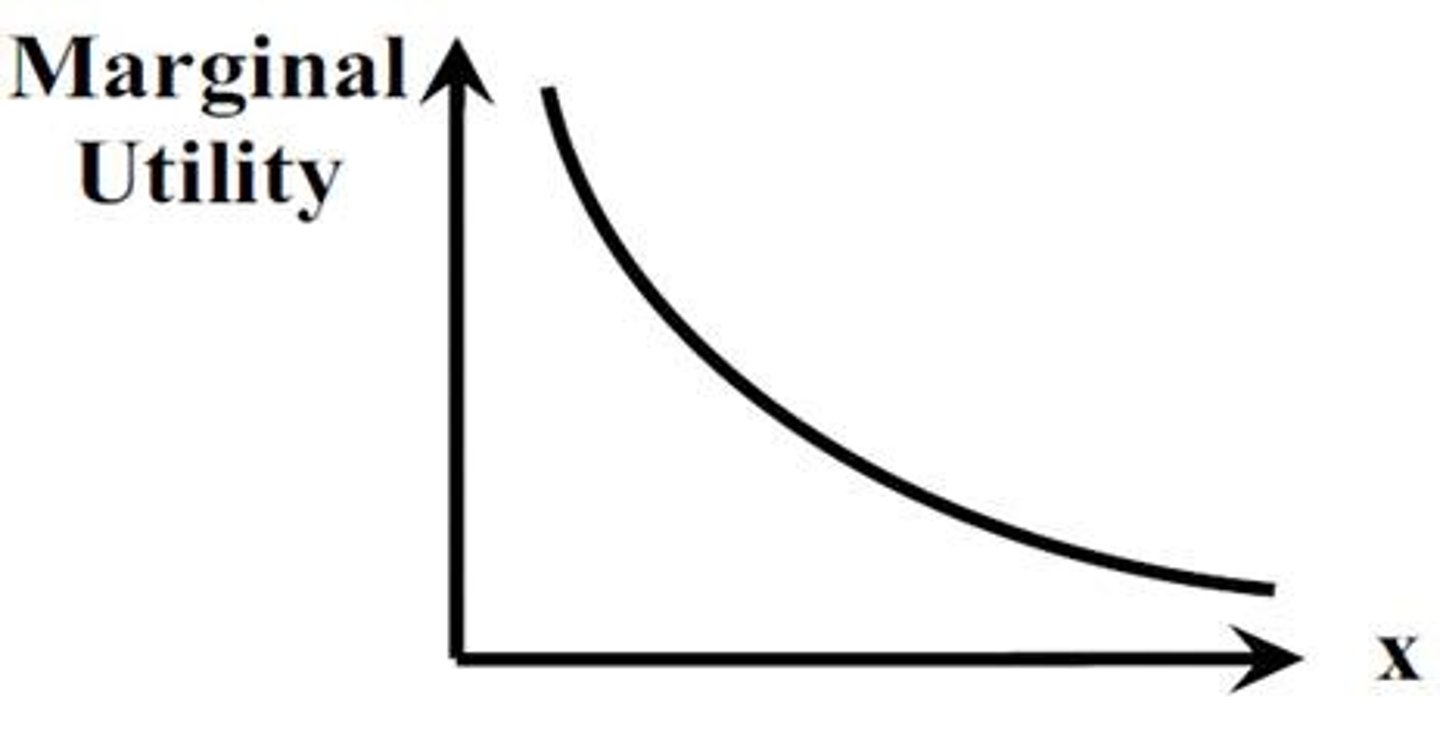

law of diminishing marginal utility

as we consume more of a good or service, the utility we get from additional units of the good or service tend to become smaller than what we received from earlier units

law of diminishing returns

as additional increments of resources are added to producing a good or service, the marginal benefit from those additional increments will decline

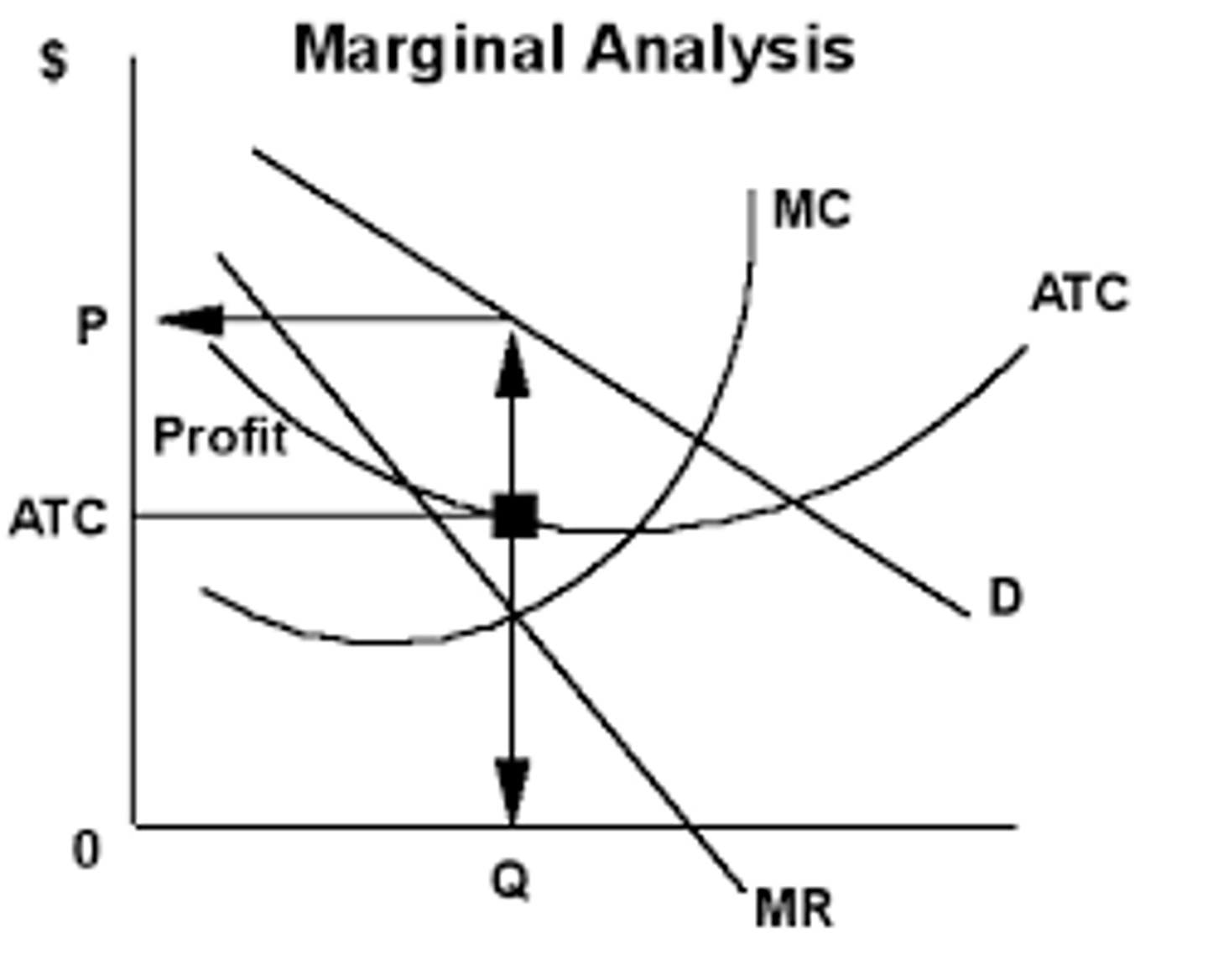

marginal analysis

examination of decisions on the margin, meaning a little more or a little less from the status quo

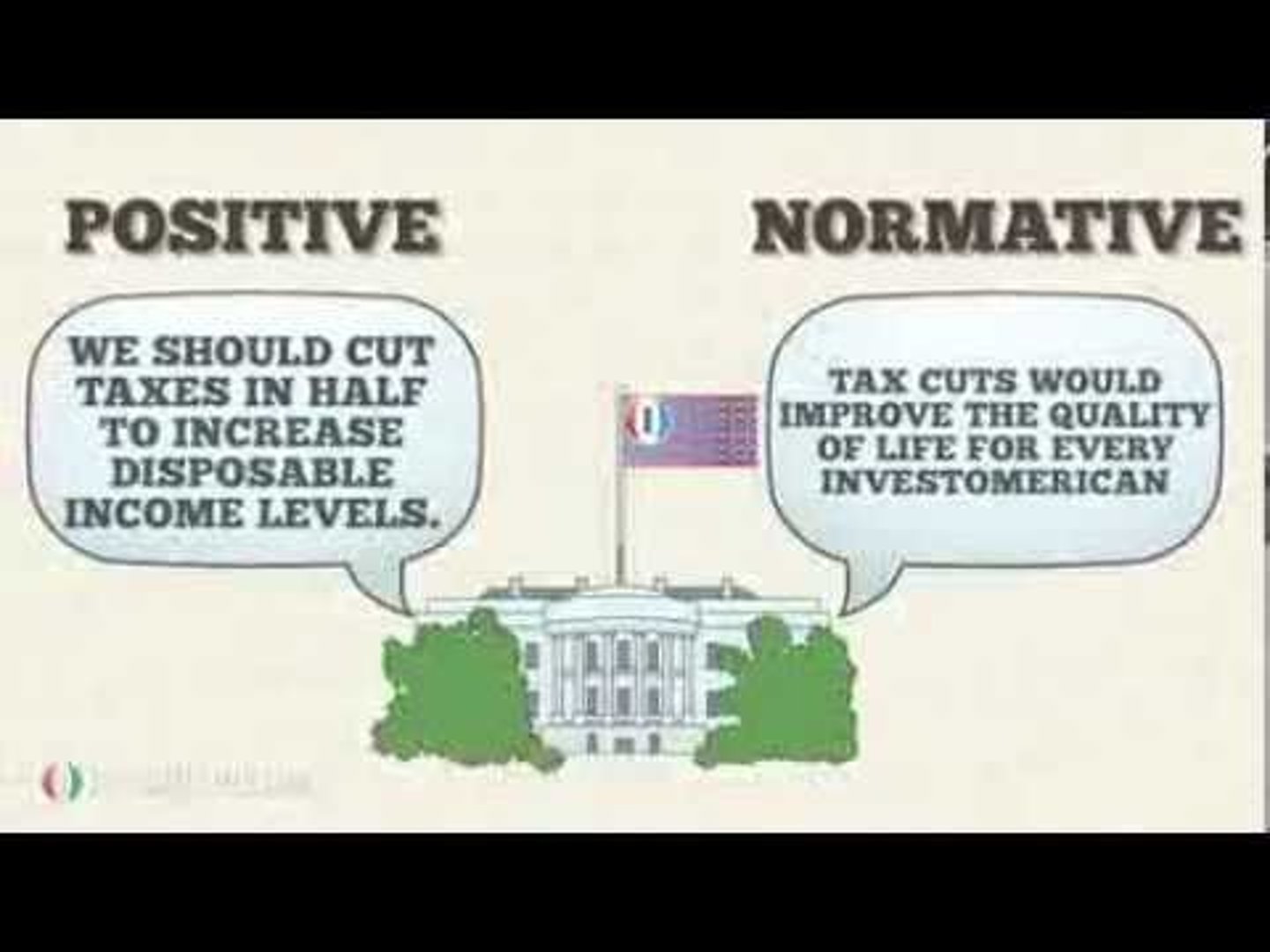

normative statement

statement which describes how the world should be

opportunity cost

Cost of the next best alternative use of money, time, or resources when one choice is made rather than another

opportunity set

all possible combinations of consumption that someone can afford given the prices of goods and the individual's income

positive statement

statement which describes the world as it is

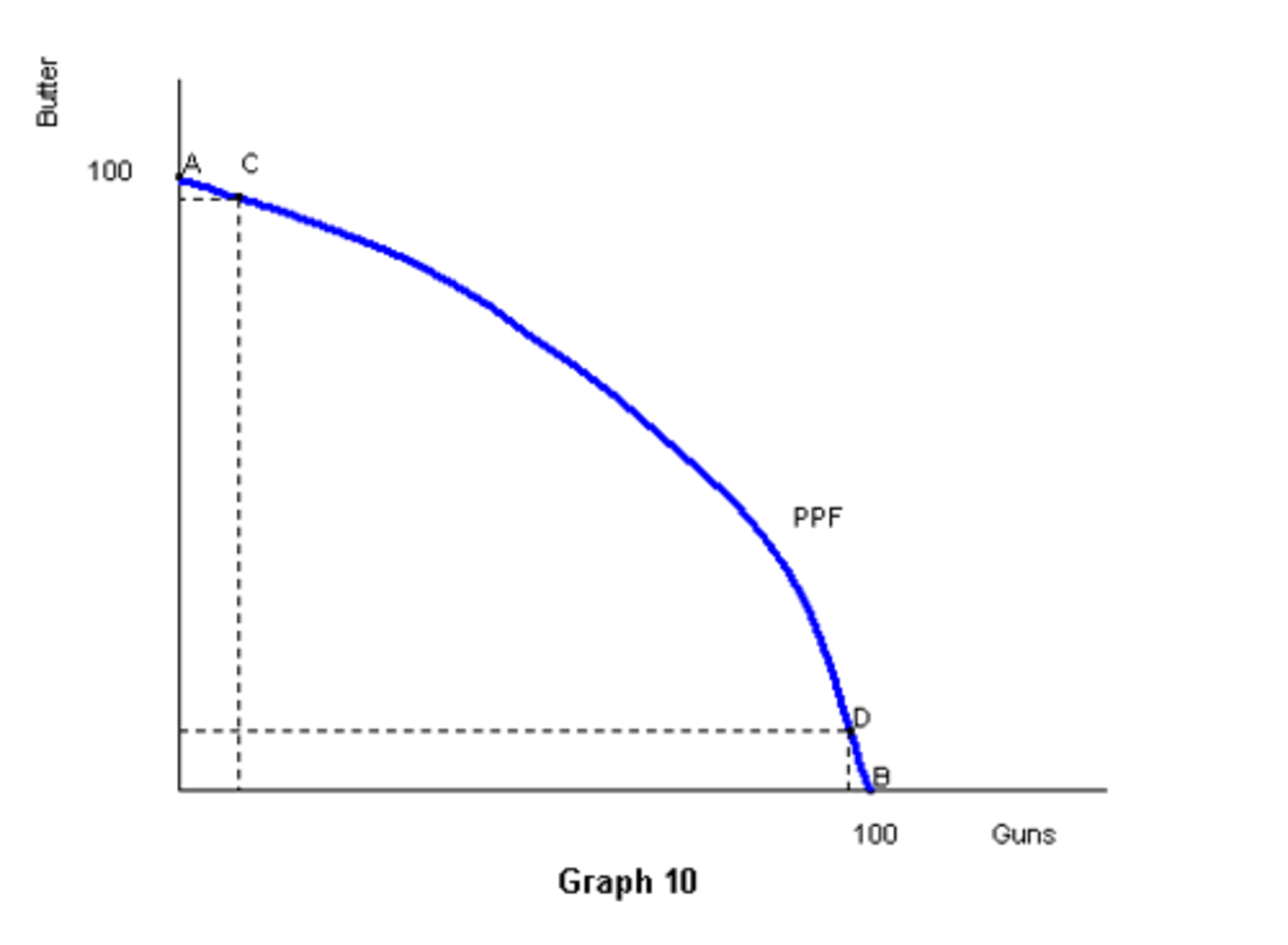

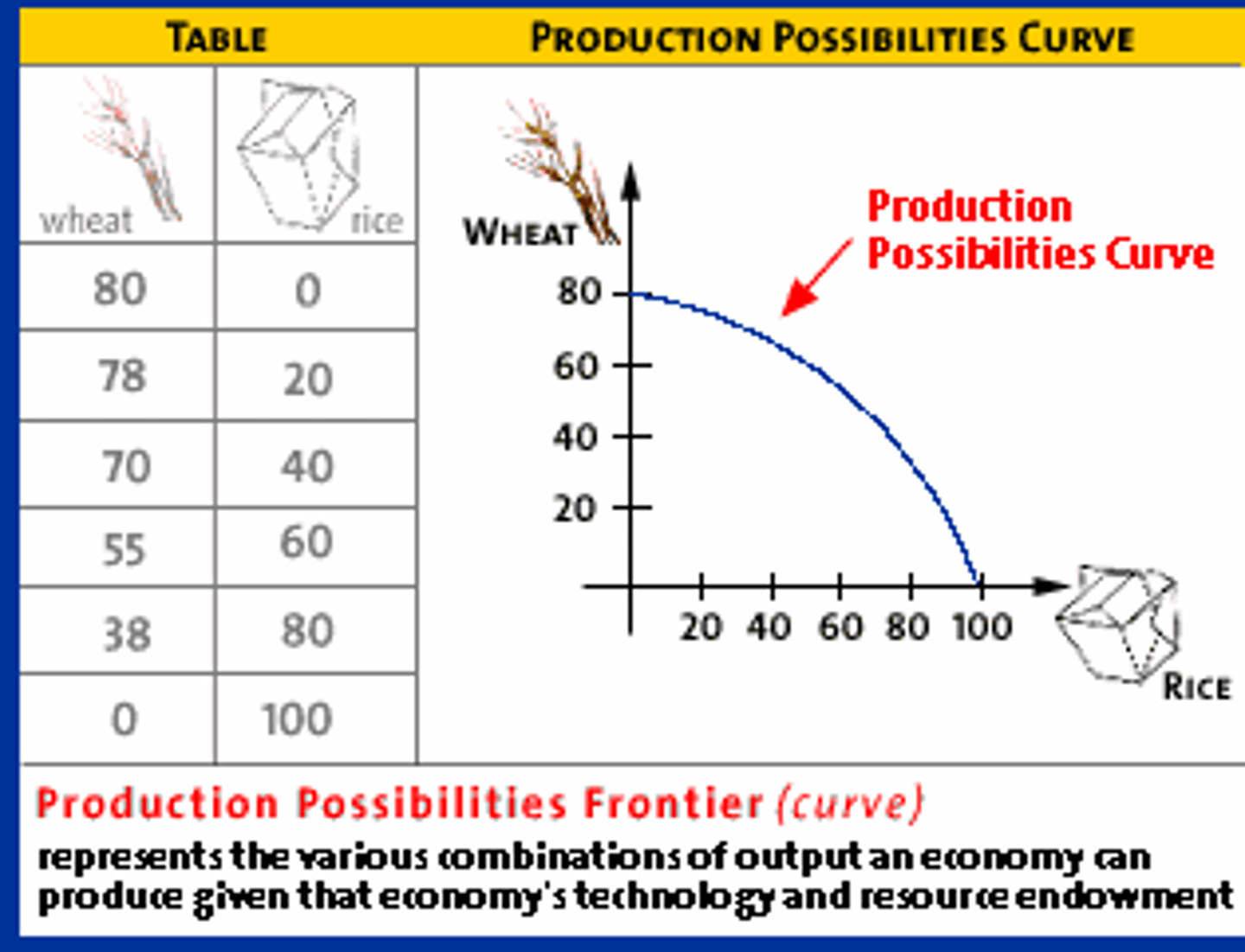

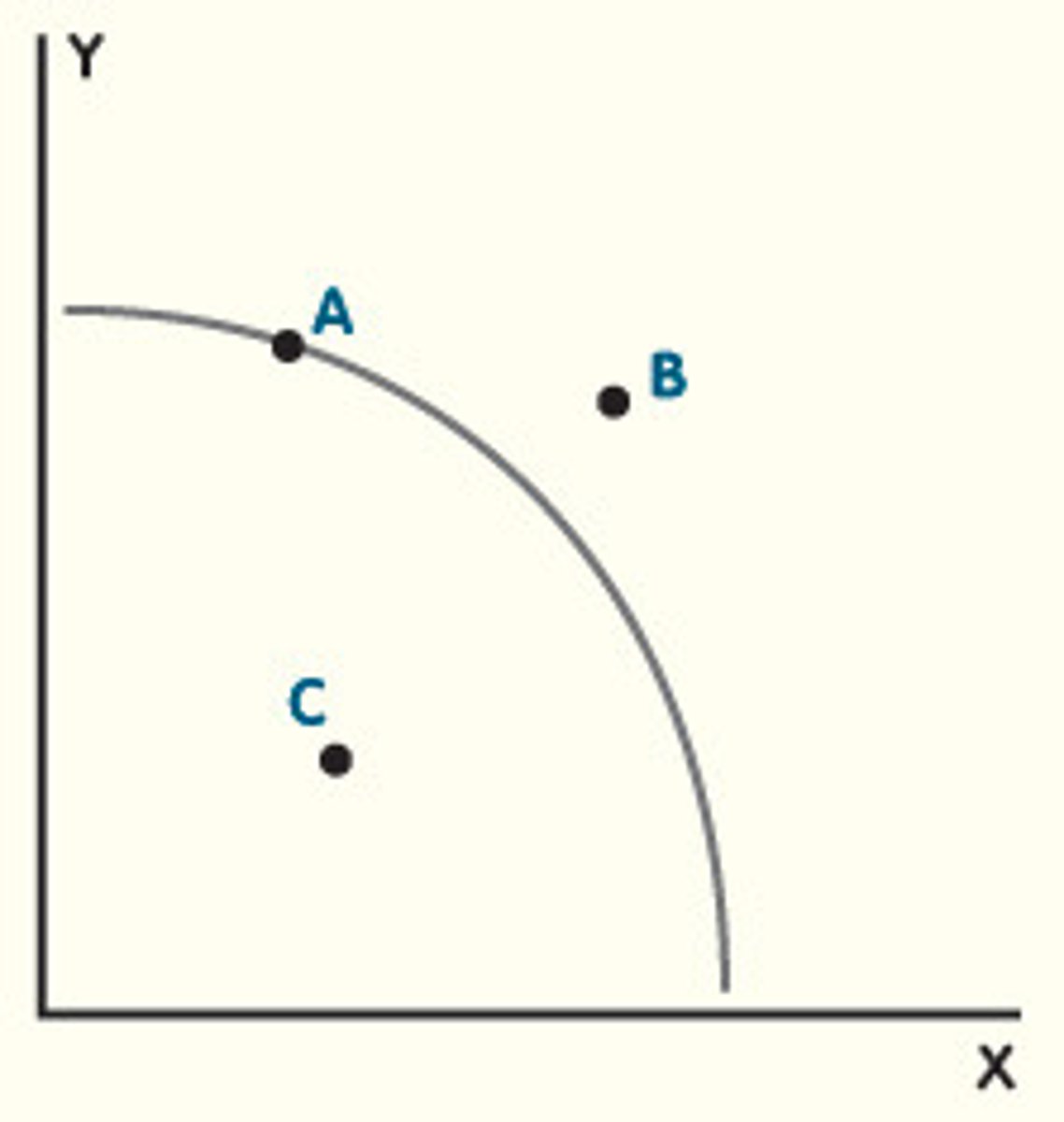

Production Possibilities Frontier (PPF)

a curve showing the maximum attainable combinations of two products that may be produced with available resources and current technology

productive efficiency

a situation in which a good or service is produced at the lowest possible cost

sunk costs

costs that have already been incurred and cannot be recovered

Utility

Ability or capacity of a good or service to be useful and give satisfaction to someone.

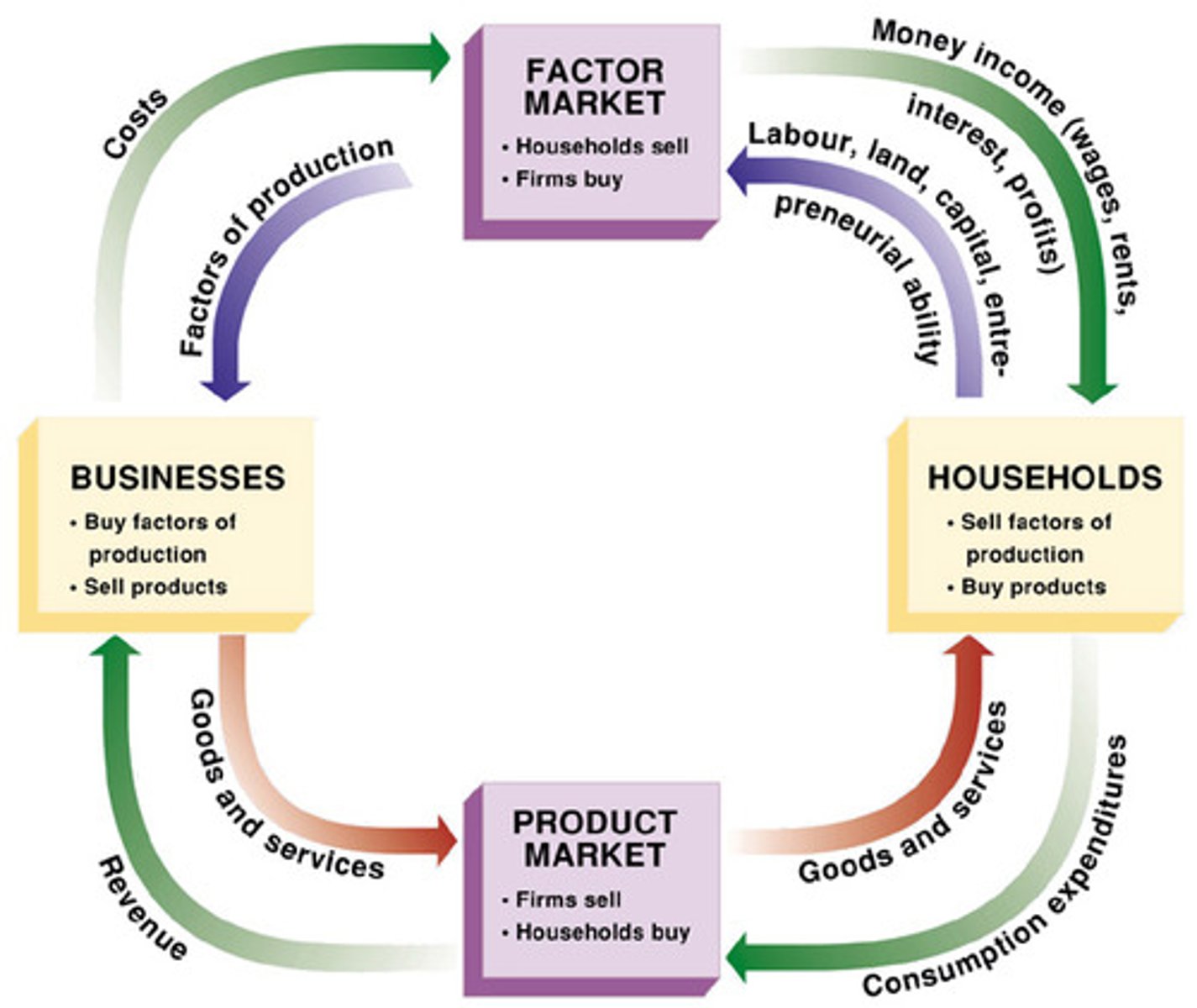

Circular Flow Diagram

a diagram that views the economy as consisting of households and firms interacting in a goods and services market and a labor market

Command Economy

an economy where economic decisions are passed down from government authority and where the government owns the resources

Division of Labor

the way in which different workers divide required tasks to produce a good or service

Economics

the study of how humans make choices under conditions of scarcity

Economies of Scale

when the average cost of producing each individual unit declines as total output increases

Exports

products (goods and services) made domestically and sold abroad

Fiscal Policy

economic policies that involve government spending and taxes

Globalization

the trend in which buying and selling in markets have increasingly crossed national borders

Goods and Service Market

a market in which firms are sellers of what they produce and households are buyers

Gross Domestic Product (GDP)

measure of the size of total production in an economy

Imports

products (goods and services) made abroad and then sold domestically

Labor Market

the market in which households sell their labor as workers to business firms or other employers

Macroeconomics

the branch of economics that focuses on broad issues such as growth, unemployment, inflation, and trade balance

Market

interaction between potential buyers and sellers; a combination of demand and supply

Market Economy

an economy where economic decisions are decentralized, private individuals own resources, and businesses supply goods and services based on demand

Mircroeconomics

the branch of economics that focuses on actions of particular agents within the economy, like households, workers, and business firms

Monetary Policy

policy that involves altering the level of interest rates, the availability of credit in the economy, and the extent of borrowing

Private Enterprise

system where private individuals or groups of private individuals own and operate the means of production (resources and businesses)

Scarcity

when human wants for goods and services exceed the available supply

Specialization

when workers or firms focus on particular tasks for which they are well-suited within the overall production process

Theory

a representation of an object or situation that is simplified while including enough of the key features to help us understand the object or situation

Traditional Economy

typically an agricultural economy where things are done the same as they have always been done

Underground Economy

a market where the buyers and sellers make transactions in violation of one or more government regulations

Model

A more applied or empirical representation and used to test theories

Ceteris Paribus

Other things being equal. "Any given demand or supply curve is based on the ceteris paribus assumption that all else is held equal".

Demand Curve

A graphic representation of the relationship between price and quantity demanded of a certain good or service, with quantity on the horizontal axis and the price on the vertical axis.

Demand Schedule

A table that shows a range of prices for a certain good or service and the quantity demanded at each price.

Demand

Refers to the amount of some good or service consumers are willing and able to

purchase at each price.

Quantity Demanded

The total number of units of a good or service consumers are willing to purchase at a given price.

Shift in Demand

When a change in some economic factor (other than price) causes a different quantity to be demanded at every price (ex: drought is predicted and people stock up on water).

Law of Demand

The common relationship that a higher price leads to a lower quantity demanded of a certain good or service and a lower price leads to a higher quantity demanded, while all other variables are held constant. It's an inverse relationship between price and quantity demanded.

Normal Good

A good in which the quantity demanded rises as income rises, and in which quantity demanded falls as income falls.

Complements

Goods that are often used together so that consumption of one good tends to enhance consumption of the other.

Substitutes

A good that can replace another to some extent, so that greater consumption of one good can mean less of the other.

Supply

The relationship between price and the quantity supplied of a certain good or service

Supply Curve

A line that shows the relationship between price and quantity supplied on a graph, with quantity supplied on the horizontal axis and price on the vertical axis.

Supply Schedule

A table that shows a range of prices for a good or service and the quantity supplied at each price.

Quantity Supplied

The total number of units of a good or service producers are willing to sell at a given price.

Shift in Supply

When a change in some economic factor (other than price) causes a different quantity to be supplied at every price.

Law of Supply

The common relationship that a higher price leads to a greater quantity supplied and a lower price leads to a lower quantity supplied, while all other variables are held constant.

Inputs/factors of production

The combination of labor, materials, and machinery that is used to produce goods and services; also called "factors of production".

Equilibrium

The situation where quantity demanded is equal to the quantity supplied; the point where the supply curve (S) and the demand curve (D) cross.

Equilibrium Price

The price where quantity demanded is equal to quantity supplied.

Equilibrium Quantity

The quantity at which quantity demanded and quantity supplied are equal for a certain price level.

Excess Demand/Shortage

At the existing price, the quantity demanded exceeds the quantity supplied; also called a "shortage".

Excess Supply/Surplus

At the existing price, quantity supplied exceeds the quantity demanded; also called a surplus.

Price Ceiling

A legal maximum price. Keeps a price from rising above a certain level (the "ceiling").

Price Control

Government laws to regulate prices instead of letting market forces determine prices.

Price Floor

A legal minimum price. Keeps a price from falling below a certain level (the "floor").

Minimum Wage

A price floor that makes it illegal for an employer to pay employees less than a certain hourly rate