Macroeconomics Ch. 1,3,7,8,9

1/129

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

130 Terms

Economics

The social science concerned with how individuals, institutions, and society make optimal choices under conditions of scarcity.

Economic Perspective

Individuals and institutions make rational decisions by comparing the marginal costs and marginal benefits associated with their actions.

Scarcity

Limits placed on the amounts and types of goods and services available for consumption as the result of limited economic resources. Creates opportunity costs and requires marginal analysis to make optimal choices,

Opportunity Cost

The amount of products that must be forgone or sacrificed to produce a unit of a given product.

Utility

The satisfaction or pleasure a consumer obtains from the consumption of a good or service.

Economic Principles

Generalizations, assume other things equal, and can be expressed graphically

Microeconomics

Economics concerned with the decisions of individual units (household, firm, industry) & individual markets (specific goods and services)

Macroeconomics

Economics concerned with the economy as a whole. Economic growth, the business cycle, interest rates, inflation, and the behavior of major aggregates.

Aggregate

A collection of specific economic units treated as one unit.

Positive Economics

The analysis of facts or data to establish scientific generalizations about economic behavior. What is.

Normative Economics

The part of economics involving value judgments about what the economy should be like; focused on which economic goals and policies should be implemented; policy economics. What ought to be.

Individual’s Economizing Problem

The need to make choices because wants are unlimited but resources are limited.

Budget Line

A line that shows different combinations of two products a consumer can purchase, given the income and the prices of the products.

Budget Constraint

Budget Line

Economic Resources

Factors of Production

Factors of Production

Land, Labor, Capital, and Entrepreneurial Ability

Land

All natural resources used in the production process. Forests, wind, sunshine, water, arable land.

Labor

Physical actions and mental activities that people contribute to the production process.

Capital

All human-produced physical objects and intangible ideas used to produce consumer goods and services. Physical objects or capital goods include factory storage, transportation, and distribution facilities. Intangible ideas or intellectual property include inventions, recipes, designs, and software.

Investment

Spending that increases the volume of physical capital and intangible ideas that help to produce goods and services. Aka economic investment.

Entrepreneurial Ability

Combines the other factors of production to innovate or produce new products. Entrepreneurs set strategy, take risks, and advance innovation.

Full Employment

The economy is using all of its available resources.

Production Possibilities Curve

Curve showing different combinations that can be produced with full employment, fixed technology, two goods, and fixed resources.

Fixed Resources

The quantity and quality of the factors of production are fixed.

Fixed Technology

The state of technology is constant.

Two goods

The economy is producing only two goods.

Law of Increasing Opportunity Costs

As the production of a good increases, the opportunity cost of producing an additional unit increases.

Optimal Output

Marginal cost equals marginal benefit.

Demand

A schedule or curve that shows the various amounts of a product that consumers are willing and able to purchase at each of a series of possible prices over a specified period of time.

Law of Demand

Other things equal, an increase in price will decrease the quantity demanded, and conversely.

Diminishing Marginal Utility

As a consumer increases the consumption of a good or service, the marginal utility decreases.

Income effect

A change in quantity demanded results from the change in real income caused by a change in the product’s price. Real income is also known as purchasing power.

Determinants of Demand

Consumers’ tastes and preferences, the # of buyers in the market, consumers’ incomes, the prices of related goods, and consumer expectations.

Normal goods

A good or service whose consumption increases when income increases and falls when income decreases, other things equal.

Inferior Goods

A good or service whose consumption declines as income rises, other things equal.

Network effect

The value of a product increases as more people use it. e.g. social media

Congestion effect

The value of a product decreases as more people use it. e.g. highways

Substitute Good

One can be used in the place of another good. When two products are substitutes, an increase in the price of one will increase the demand for another.

Complementary Good

One that is used together with another good. If the price of a complement goes up, the demand for the related good will decline.

A Change in Demand

A shift of the demand curve

A change in quantity demanded

Going from one point to another in a fixed demand curve.

Supply

A schedule or curve showing the various amounts of a product that producers are willing and able to make available for sale at each of a series of possible prices over a period of time, other things equal.

Law of Supply

An increase in the price of a product will increase the quantity of it supplied. Suppliers will offer more of a product for sale as its price rises and less of a product as its price decreases.

Determinants of Supply

Resource prices, technology, prices of other goods, taxes and subsidies, producer expectations, and the number of sellers on the market.

Equilibrium Price

The price where quantity demanded and quantity supplied are equal. Also known as the market-clearing price.

Productive efficiency

The production of any particular good in the least costly way.

Allocative Efficiency

The particular mix of goods and services mostly valued by society.

Price Ceiling

A legally established maximum price for a good or service. Create shortages

Price Floor

A minimum price of a good or service fixed by the government. Create surpluses

National Income Accounting

Measures the economy’s overall performance. Helps policymakers make decisions and assess the economy’s health.

Gross Domestic Product (GDP)

The total market value of all final goods and services produced yearly within a nation.

Final goods and services

Products that have been purchased for final use rather than resale or further manufacturing.

Intermediate goods and services

Products that are purchased for resale or further manufacture.

Value Added

The value of a product sold by a firm less than the value of the materials purchased and used for making the product.

Gross Output

The dollar value of the economic activity taking place at every stage of production and distribution.

Public Transfer Payments

Social security, welfare payments, veterans’ payments. The government makes payments directly to houses. Not included in GDP calculations

Private Transfer Payments

Allowance money, cash gifts given during the holidays. Just funds transferred from one person to another. Not counted in GDP calculations.

Financial Asset Transactions

Buying and selling stocks, bonds, etc. Only a transfer of ownership from one person to another. Not counted in GDP calculations.

Secondhand Sales

Contribute nothing new to the economy. Excluded from GDP calculations.

Expenditures Approach

Adds all expenditures made for final goods and services to measure GDP. Consumption expenditures by households (C)+Gross private domestic investment (Ig)+ Government Expenditures (G)+ expenditures by foreigners (Net exports)

Personal Consumption Expenditures

The expenditures of households for both durable and nondurable consumer goods.

Gross Private Domestic Investment

The expenditures that increase the nation’s stock of capital.

Net Exports

Exports-imports

Government Purchases

Expenditures by government for goods and services.

Income Approach

Adds all the income generated by the production of final goods and services to measure GDP. Compensation to employees+ rent + interest + proprietors’ income + corporate profits + taxes on production and imports - net foreign factor income + consumption of fixed capital +statistical discrepancy

Net Domestic Product

GDP minus Consumption of fixed capital.

Personal Income

The earned and unearned income available to resource suppliers and others before the payment of personal taxes.

Disposable Income

Personal income less personal taxes; income available for personal consumption expenditures and personal saving. Disposable income= consumption+saving

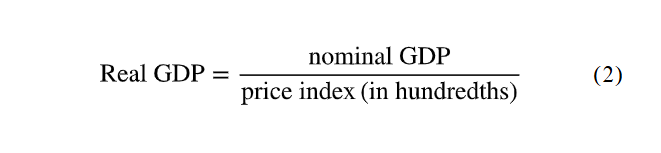

Nominal GDP

GDP measured in terms of the price level at the time of measurement; GDP not adjusted for inflation.

National Income

All income earned through the use of American-owned resources, whether located at home or abroad. Also includes taxes on production and imports.

Price index

An index number that shows how the weighted-average price of a “market basket” of goods changes over time relative to its price in a specific base year.

Base Year

The year with which other years are compared when an index is constructed; for example, the base year for a price index.

Price Index Formula

Real GDP Formula

Shortcomings of GDP

Fails to account for illegal transactions, changes in leisure and product quality, the composition and distribution of output, the environmental effects of pollution, and economic activity at earlier stages of production and distribution.

Economic Growth

(1) An outward shift in the production possibilities curve that results from an increase in resource supplies or quality or an improvement in technology; (2) an increase of real output (gross domestic product) or real output per capita.

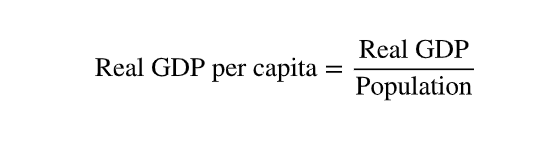

Real GDP Per capita

Real output per person in a country.

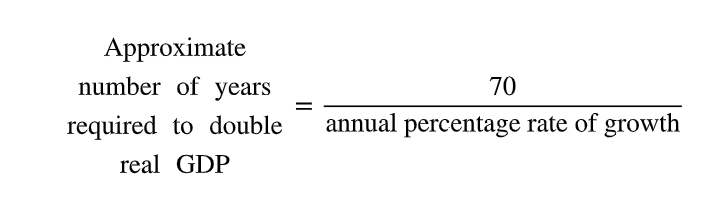

Rule of 70

Real GDP in the U.S.

Real GDP in the U.S. has grown by about 3.0 percent annually since 1950, while Real GDP per capita has grown by roughly 1.9 percent annually over the same period.

Leader Countries

As it relates to economic growth, countries that develop and use the most advanced technologies, which then become available to follower countries.

Follower Countries

As it relates to economic growth, countries that adopt advanced technologies that previously were developed and used by leader countries.

Supply Factors in Growth

The four determinants of an economy’s physical ability to achieve economic growth by increasing potential output and shifting out the production possibilities curve. The four determinants are improvements in technology plus increases in the quantity and quality of natural resources, human resources, and the stock of capital goods.

Demand Factor

The requirement that aggregate demand increase as fast as potential output if economic growth is to proceed as quickly as possible.

Efficiency Factor

The capacity of an economy to achieve allocative and productive efficiency and thereby fulfill the potential for growth that the supply factors (of growth) make possible; the capacity of an economy to achieve economic efficiency and thereby reach the optimal point on its production possibilities curve.

Labor Productivity

Total output (GDP) divided by the quantity of labor (hours of work) employed to produce it; the average product of labor, or output per hour of work.

Real GDP Calculation

Labor Force Participation Rate

The percentage of the working-age population that is actually in the labor force.

Growth accounting

The bookkeeping of the supply-side elements such as productivity and labor inputs that contribute to changes in real GDP over some specific time period.

Infrastructure

The interconnected network of large-scale capital goods (such as roads, sewers, electrical grids, railways, ports, and the Internet) needed to operate a technologically advanced economy.

Human Capital

The knowledge and skills that make a person productive.

Economies of Scale

The situation when a firm’s average total cost of producing a product decreases in the long run as the firm increases the size of its plant (and, hence, its output).

Information Technology

New and more efficient methods of delivering and receiving information through the use of computers, wi-fi networks, wireless phones, and the Internet.

Startup Firms

A new firm focused on creating and introducing a particular new product or employing a specific new production or distribution method.

Increasing returns

An increase in a firm’s output by a larger percentage than the percentage increase in its inputs.

Learning by doing

Achieving greater productivity and lower average total cost through gains in knowledge and skill that accompany repetition of a task; a source of economies of scale.

Business Cycle

Recurring increases and decreases in the level of economic activity over periods of years; consists of peak, recession, trough, and expansion phases.

Peak

The point in a business cycle at which business activity has reached a temporary maximum; the point at which an expansion ends and a recession begins. At the peak, the economy is near or at full employment and the level of real output is at or very close to the economy’s capacity.

Recession

A period of declining real GDP, accompanied by lower real income and higher unemployment.

Trough

The point in a business cycle at which business activity has reached a temporary minimum; the point at which a recession ends and an expansion (recovery) begins. At the trough, the economy experiences substantial unemployment and real GDP is less than potential output.

Expansion

The phase of the business cycle in which real GDP, income, and employment rise.