CFA Potential Questions

1/15

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

16 Terms

ENVIRONMENTAL, SOCIAL & GOVERNANCE (ESG)

ENVIRONMENTAL, SOCIAL & GOVERNANCE (ESG)

What are some areas where Invesco could improve in ESG?

Invesco’s biggest ESG improvement opportunities are in environmental and social disclosure practices. The firm’s Greenwashing fine of 17.5M in 2024 was due to incorrectly listing a higher percentage of their products as ESG integrated between 2020 and 2022 than they actually were, creating misleading information. Governance is a relative strength, but the company has high audit risk due to PricewaterhouseCoopers LLP ("PwC") serving as the Firm's long-standing external auditor since 2013, potentially creating independence issues due to the long tenure.

What are their environmental goals and targets? (Water, waste, emissions)

IVZ's emission reduction goal, in partnership with the Science Based Targets Initiative (SBTi), is to reduce its corporate Scope 1, 2, and 3 greenhouse gas (GHG) emissions by 4.2% year-over-year. Following this trend will lead to a 46% reduction by 2030 and achieve net zero by 2050 or sooner

Recent energy efficiency initiatives at IVZ's offices have resulted in the Firm reducing its use of fuel for heating and generators, decreasing its Scope 1 and 2 (location-based) emissions by 49% since its baseline FY 2019

You talked about better measurable outcomes / disclosure practices for their social score. Give some examples

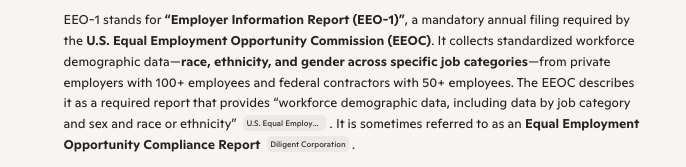

Invesco does not publish their EEO-1 workforce diversity report, which is a major gap because EEO‑1 disclosure is now considered baseline transparency for providing “workforce demographic data, including data by job category and sex and race or ethnicity”

How could MassMutual’s large stake (with common shares and preferred) impact Invesco?

A single investor holding nearly one‑fifth of the common shares gives MassMutual outsized voting power relative to other shareholders. This can tilt governance outcomes, reduce the influence of minority investors, and create the perception that IVZ is not fully independent in major strategic decisions. Despite these risks, MassMutual’s continued investment is also a strong positive signal, as it reflects long‑term confidence in Invesco’s strategy, balance‑sheet improvements, and earnings trajectory

INVESTMENT RISKS

INVESTMENT RISKS

Impact of recession on revenue and profit?

A recession would pressure Invesco primarily through declining AUM. When markets fall, asset values drop and clients typically pull back risk exposure. Because management fees are tied to AUM, revenue falls quickly. At the same time, performance fees shrink and operating leverage works against them, since costs don’t fall as fast as revenue. The result is margin compression and weaker profitability

What is the biggest long-term risk for the company?

The biggest long‑term risk for Invesco is structural fee compression driven by passive competition. Firms like BlackRock and Vanguard continue taking share with ultra‑low‑cost products, which limits Invesco’s pricing power. As clients shift toward passive and model portfolios, Invesco’s ability to maintain margins becomes increasingly challenged

Analyze recent economic and political events and their impact on financial performance (in 2025, the event was tariffs).

Tariffs in 2025 increased global uncertainty, which typically reduces investor risk appetite. That can slow inflows into equities and international strategies, both important revenue drivers for Invesco. Tariffs also contributed to market volatility and weaker global performance, which directly reduces AUM and therefore fee revenue. Institutional clients may also delay allocations during periods of geopolitical tension (use economic policy chart dr astrid is creating or Appendix O - share price evolution)

What does the preferred stock repurchase signal for the future? (1.5 billion from massmutual making it go from 4B to 2.5B)

The repurchase of $1.5B of preferred stock—reducing MassMutual’s holdings from $4B to $2.5B—signals that Invesco is entering a phase of balance‑sheet strengthening and long‑term value creation. Preferred shares carried a 5.9% fixed dividend, so retiring them immediately reduces annual preferred dividends

INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING

INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING

Why has their stock been outperformed by the industry average?

Invesco’s stock has lagged the broader asset‑management industry because the firm has faced structural headwinds that its largest competitors have been better positioned to absorb, including weaker net inflows, fee pressure, and slower revenue growth.

As a mid‑cap manager without the scale advantages of BlackRock or Vanguard, Invesco has been more exposed to fee compression, market volatility, and consolidation pressures, which has contributed to its stock underperforming the industry average over time.

IVZ competes with BlackRock and Vanguard ETF’s. Where does IVZ gain its advantage and win vs competitors?

(Go to competitive advantages slide) IVZ wins against BlackRock and Vanguard not by beating them on broad‑market, low‑cost ETFs—a battle those giants dominate—but by owning specific ETF niches where scale, liquidity, and first‑mover advantages create moats.

How big a threat do you view ultra-low fee ETFs to Invesco’s business model?

Ultra‑low‑fee ETFs create intense fee compression in broad‑market index categories where BlackRock’s scale allows them to push expenses toward zero, pressuring IVZ’s margins and limiting its ability to compete on price. But the threat is far smaller in IVZ’s core ETF franchises—QQQ, RSP, smart beta, and thematic ETFs—where the firm benefits from first‑mover advantages, monopoly/duopoly positions, and liquidity moats that low‑fee competitors cannot easily replicate. In these niches, investors choose IVZ products for exposure, liquidity, and brand strength, not for being the cheapest option, which helps insulate the company from the full force of the ultra‑low‑fee race.

Market share and how it is compared to competitors. Break down by segments.

(Go to industry appendix —- AUM vs peers)

Invesco’s market share sits in the middle of a highly consolidated industry, with 11% of total AUM among major public asset managers, compared with BlackRock at 68%, T. Rowe Price at 9%, Franklin Templeton at 8%, and Federated Hermes at 4%. This positioning shows that while IVZ is far smaller than BlackRock, it remains one of the few firms with meaningful scale. Overall, IVZ’s market share is modest at the firm level but significantly stronger within specific ETF categories where it holds durable competitive moats.

What is their position in the competitive landscape?

Invesco sits as a mid‑sized but strategically differentiated competitor in a highly consolidated asset‑management landscape. What makes IVZ competitive despite its smaller scale is the composition of its AUM: nearly 49% comes from ETFs and QQQ, a segment where it holds category‑leading positions and benefits from first‑mover advantages, strong liquidity, and brand strength.