macro chapter 1

1/11

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

12 Terms

what is macroeconomics

the study of the forces that affect the economy as a whole

the science of macroeconomic processes

looks into prosperity variation, value of money, inflation rates, recessions, etc

macroeconomic variables

real GDP (gross domestic product): reflects the price-adjusted total income of all economic actors in an economy

nominal GDP: not price adjusted (measured at current prices)

inflation rate: describes how quickly prices are rising

unemployment rate: tells you what portion of labour force in an economy is out of work

measures: investments, inequality, satisfaction

what does an increased GDP mean

economy grew

income has risen, more trade, more products produced

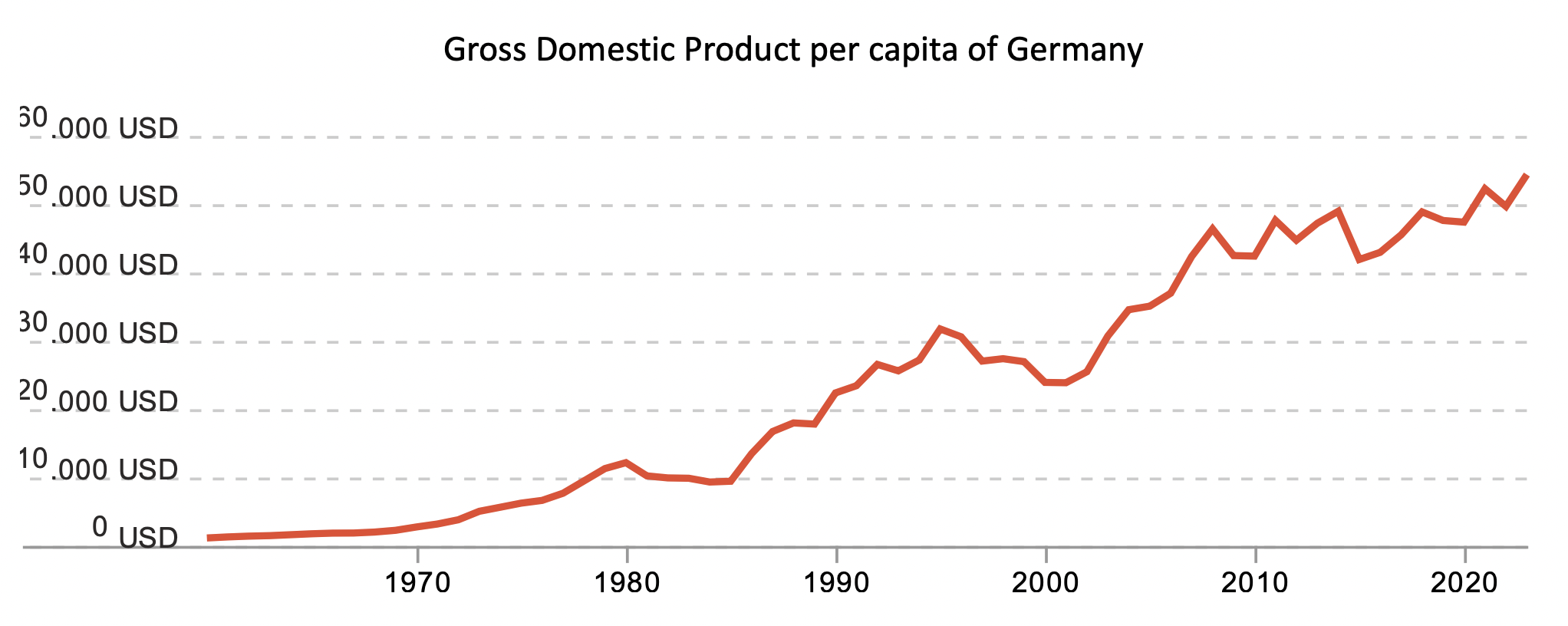

GDP per capita (per person)

measures economic activity/income per person

can tell you if the size of the economy per individual is larger than before

graph is not price adjusted

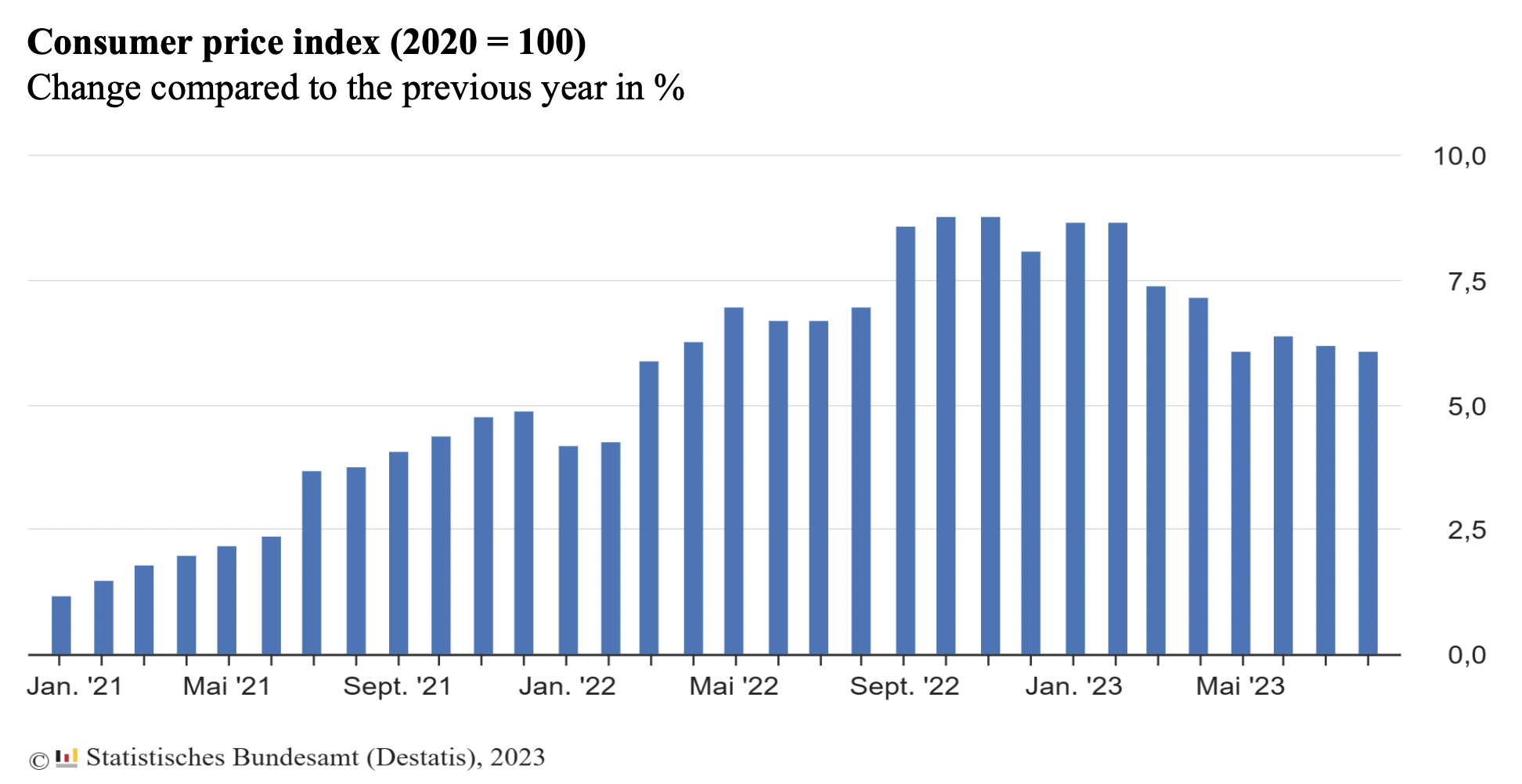

what is inflation

a monthly statistic

a sustained increase in the general price level of goods/services in an economy over a period of time, which reduces the purchasing power of currency

measured as change compared to previous year in %

Macroeconomic instruments

Simplified representations of reality in models

We concentrate on the central variables (try to abstract irrelevant details)

Models are constructed using very restrictive assumptions.

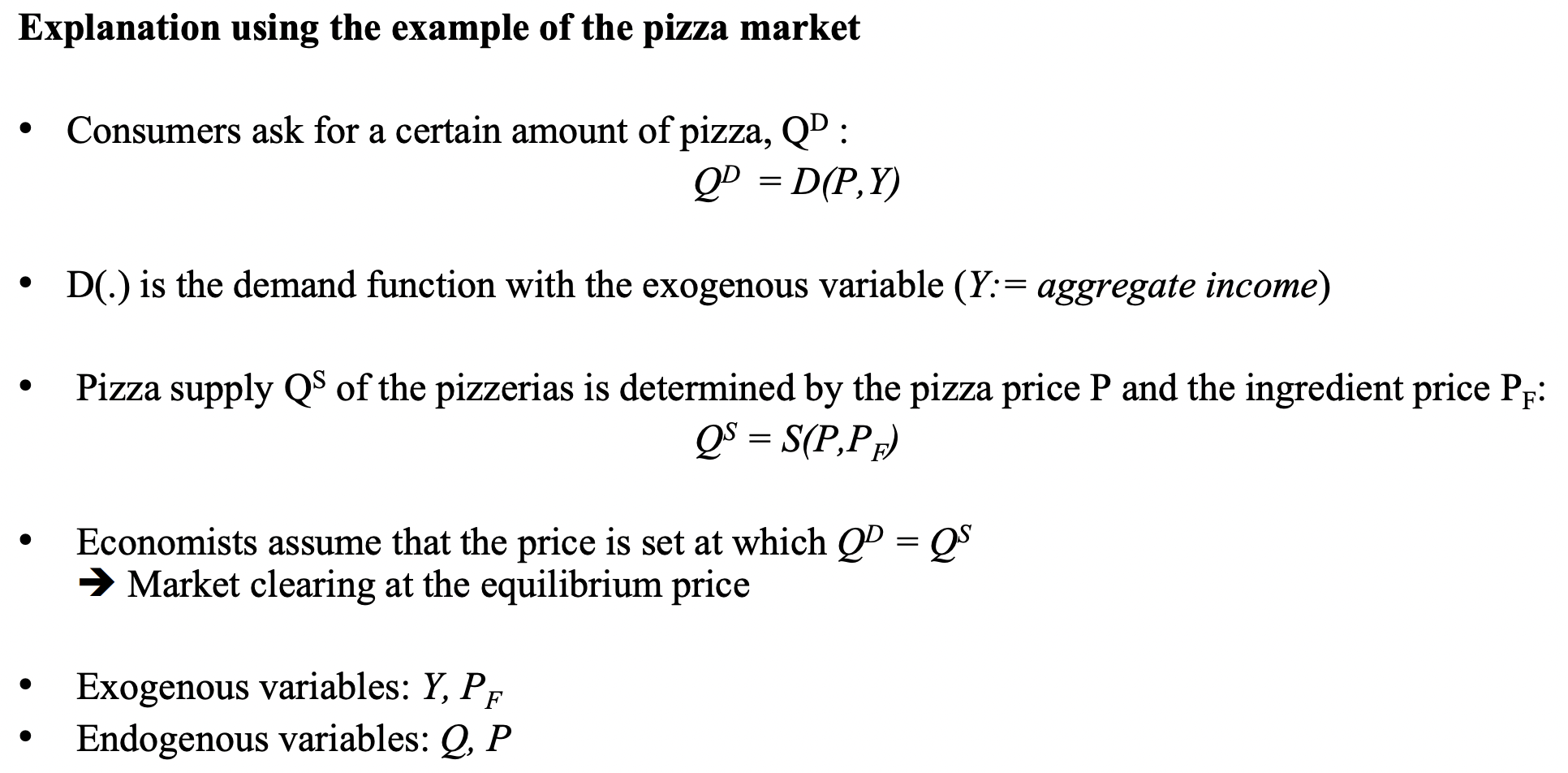

exogenous vs endogenous variables

Exogenous variables are determined outside the model. They are introduced into the model or are fixed

Endogenous variables are determined within the model itself.

how economic models work

simplified theories and show the essential relationships between economic variables

exogenous variables are variables that are determined outside the model

endogenous variables are explained by the model

model shows how a change in an exogenous variable affects all endogenous variables

supply and demand model

problems of simplifying assumptions

not all varieties of the same product are sold at the same price

not all place selling similar products are located in the same place (some may be easier/harder to get to)

flexible vs fixed prices

economists assume that price of goods adjusts quickly → market clearing

at this price, consumers can demand desired quantity, which is offered by producers at this price

flexible: adapt to changes in supply and demand without delay → suitable for describing the long-term (fully adjusted) equilibrium

wage + price rigidity justify a slow/delayed adjustment to changes in supply or demand

Short-term (cyclical) fluctuations are often associated with fixed prices

what is market clearing?

economic process where quantity of a good or service supplied exactly matches the quantity demanded, establishing an equilibrium price

no shortages or surpluses