Micro

1/132

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

133 Terms

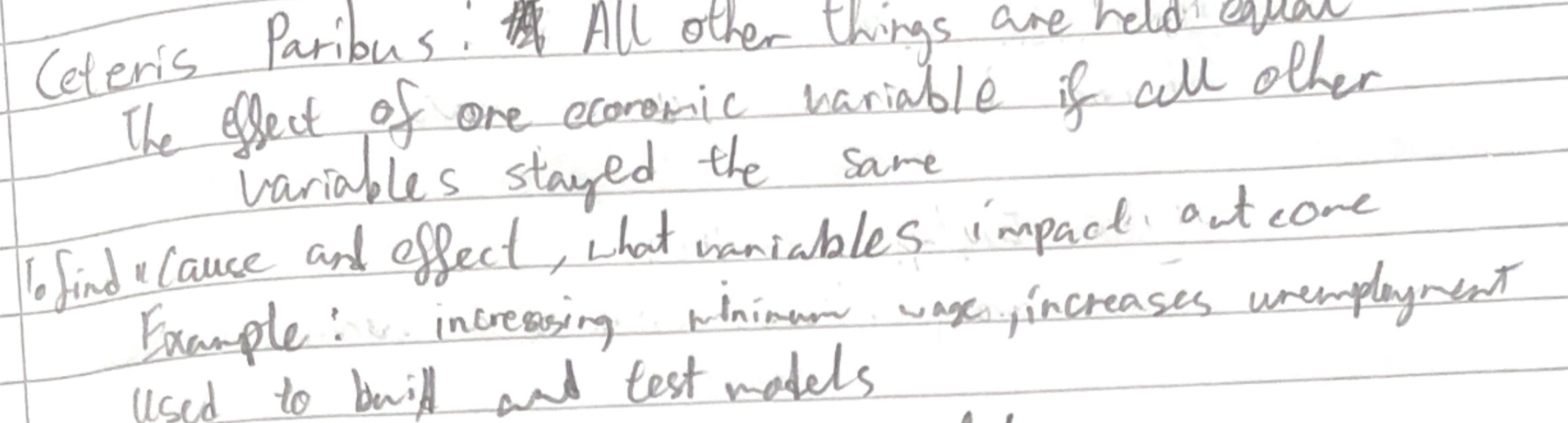

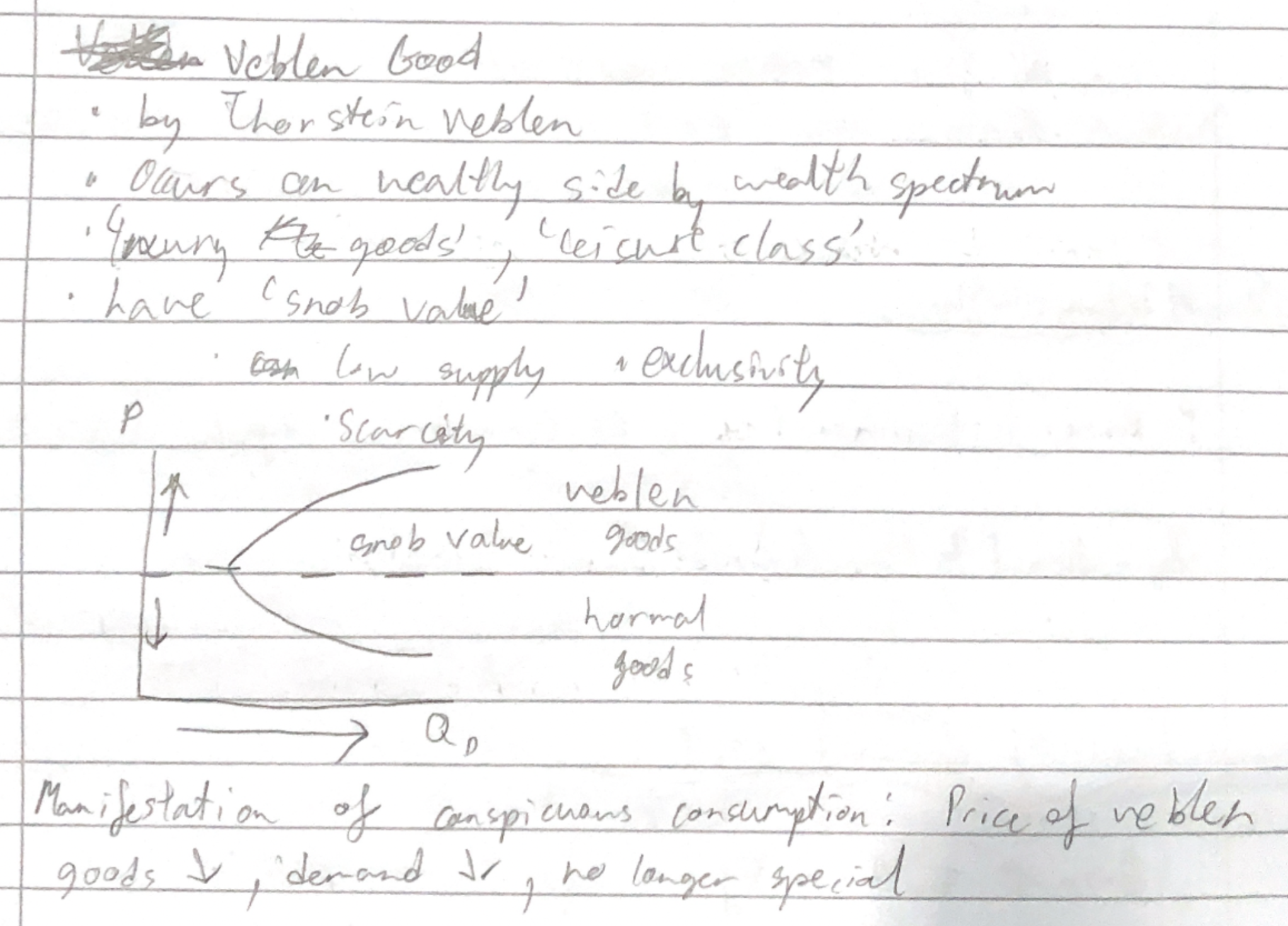

Ceteris paribus

* Natural resources

* Labor

* all human effort

* Capital

* tangible facilities

* Entrepreneurship

* Risk taker, management

* Manages the FOP

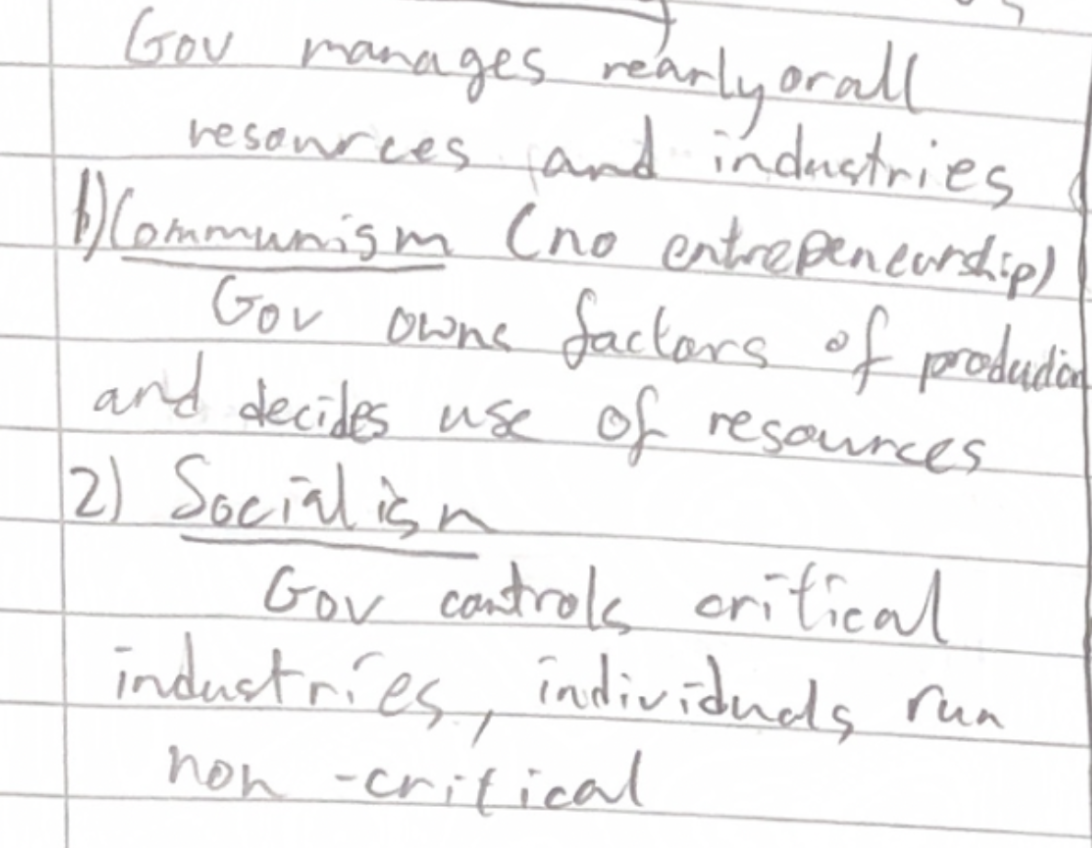

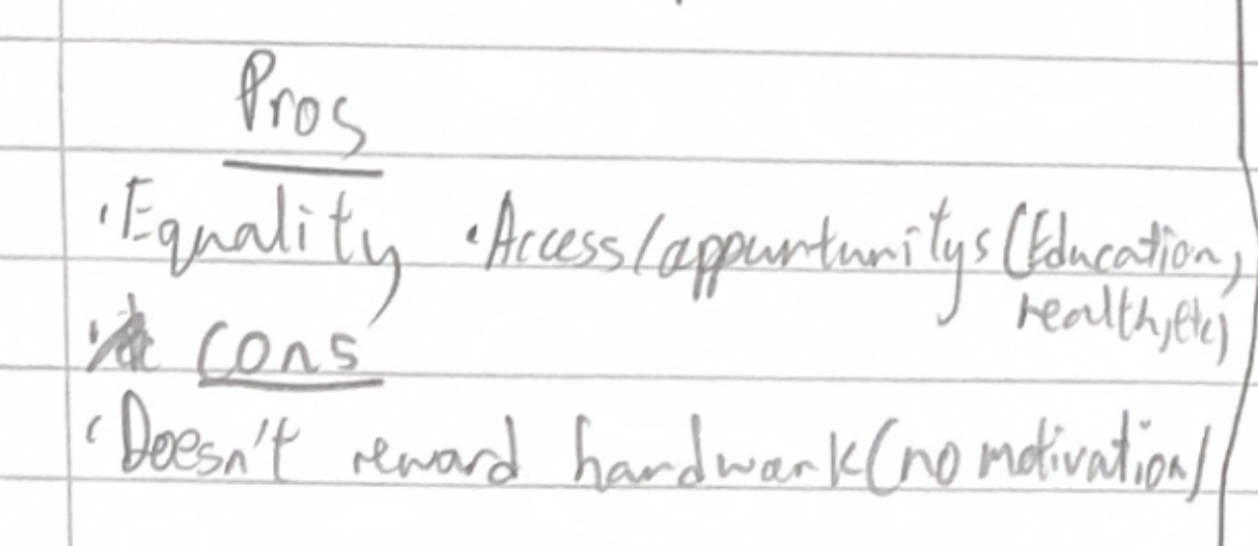

Command economies

Pros, cons of command economies

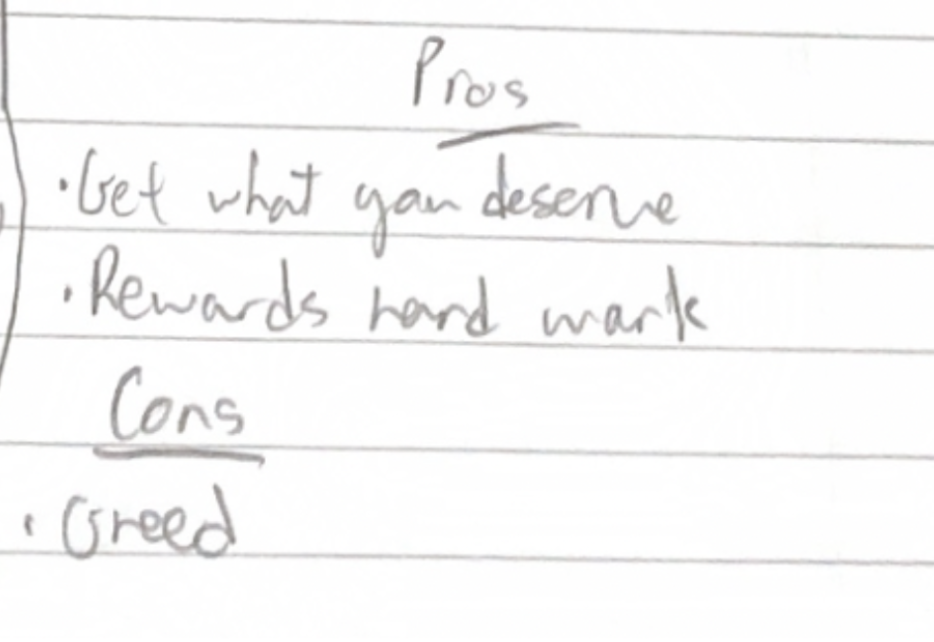

pros, cons of market economies

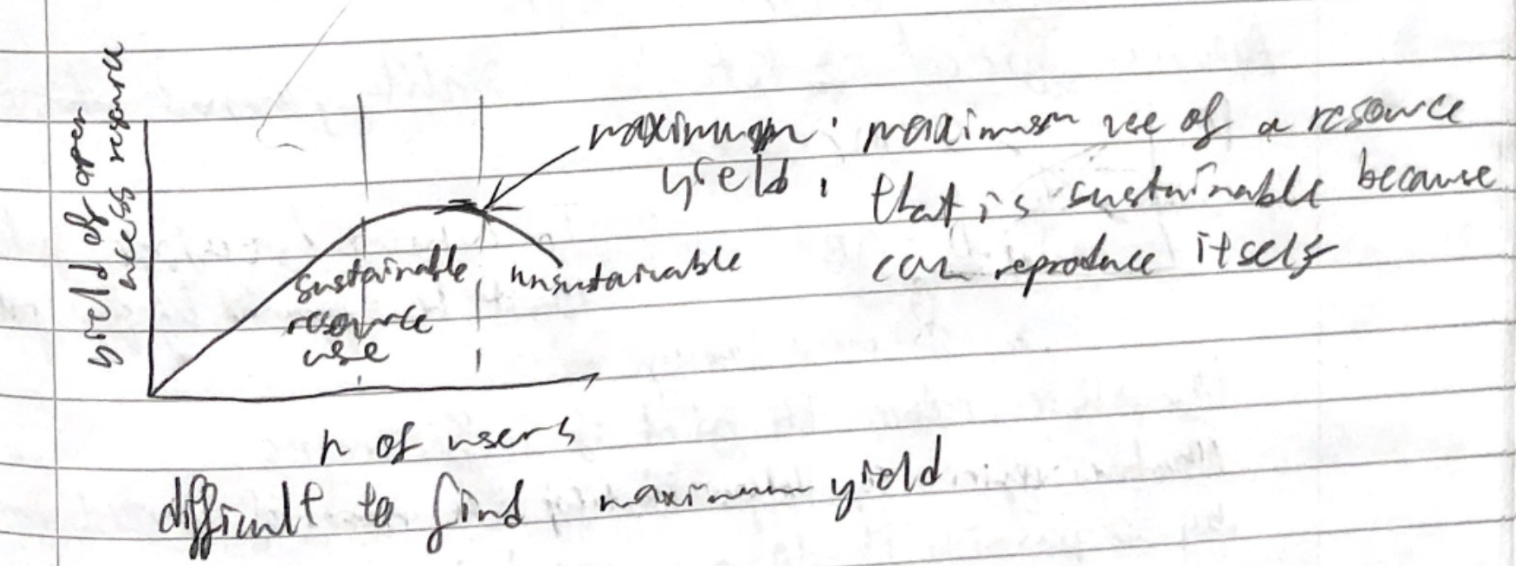

Economic vs free goods

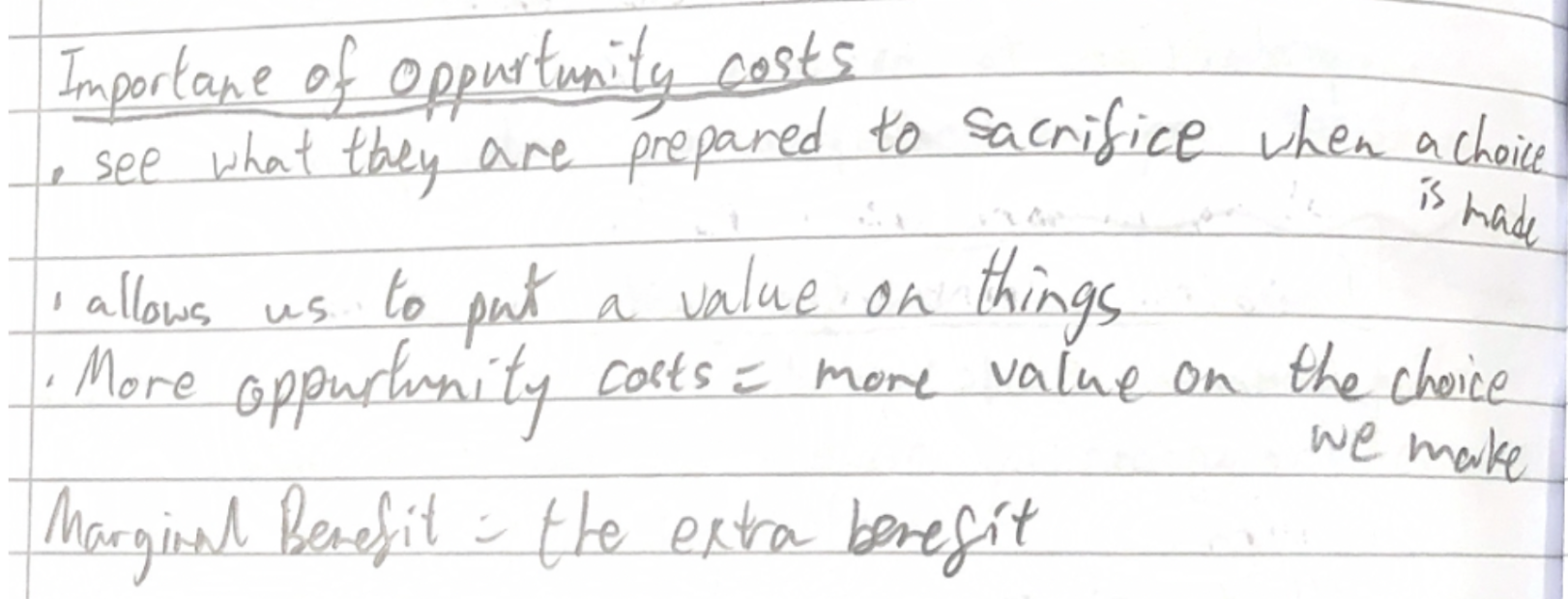

Opportunity costs, and importance

the value of the next-best alternative when a decision is made

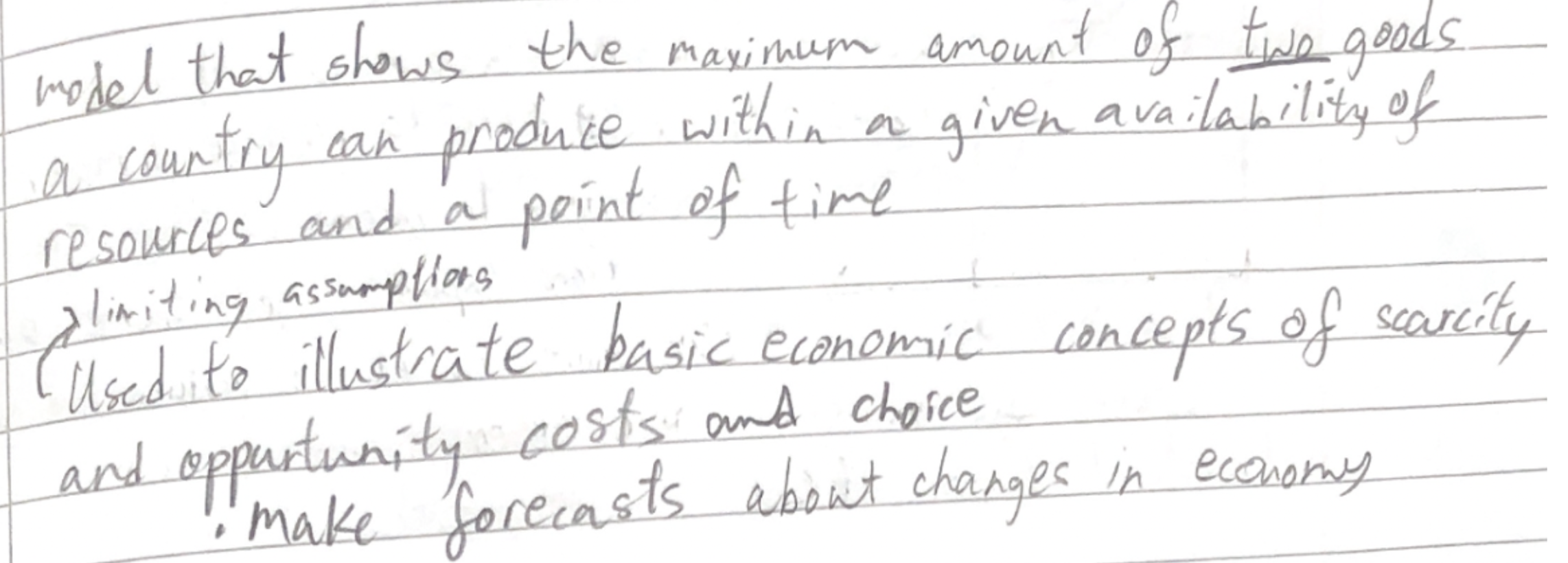

PPC looka at capacity to produce not price

PPC

points on curve is potential output

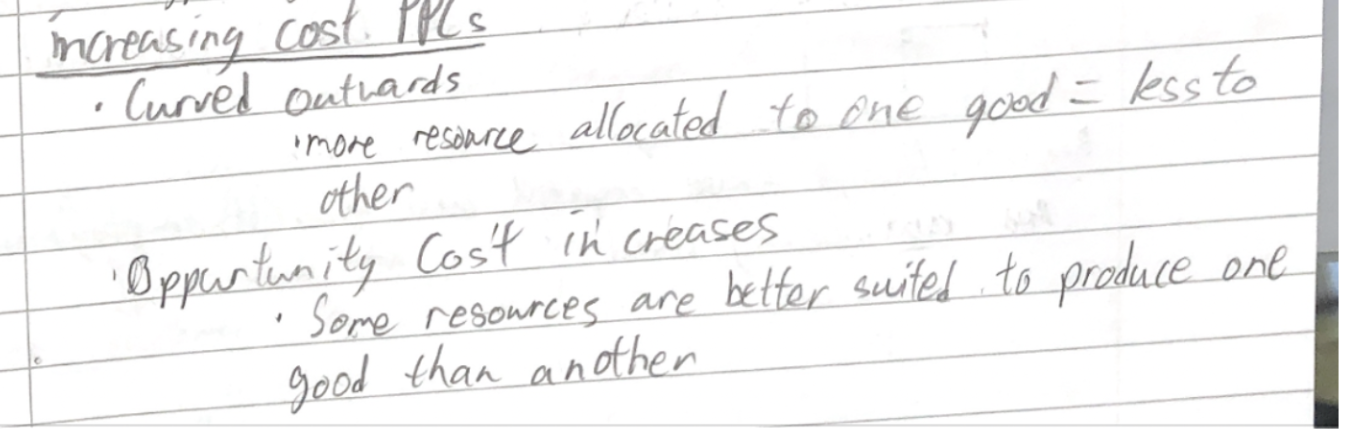

Increasing cost PPC

Opportunity cost increases

PPC curve increases

increases in Q or Quality of FOP

Potential output increase

Reallocation

Moving resources of one to another production

* High price

* signals to consumers to consumer less

* To producers to produce more-higher profits

* Rationing

* More scarce

* demand exceeds supply

* Higher price, conserved

* Incentive

* Prices incentive certain behaviors

* high wage = work

* High price = join market, produce

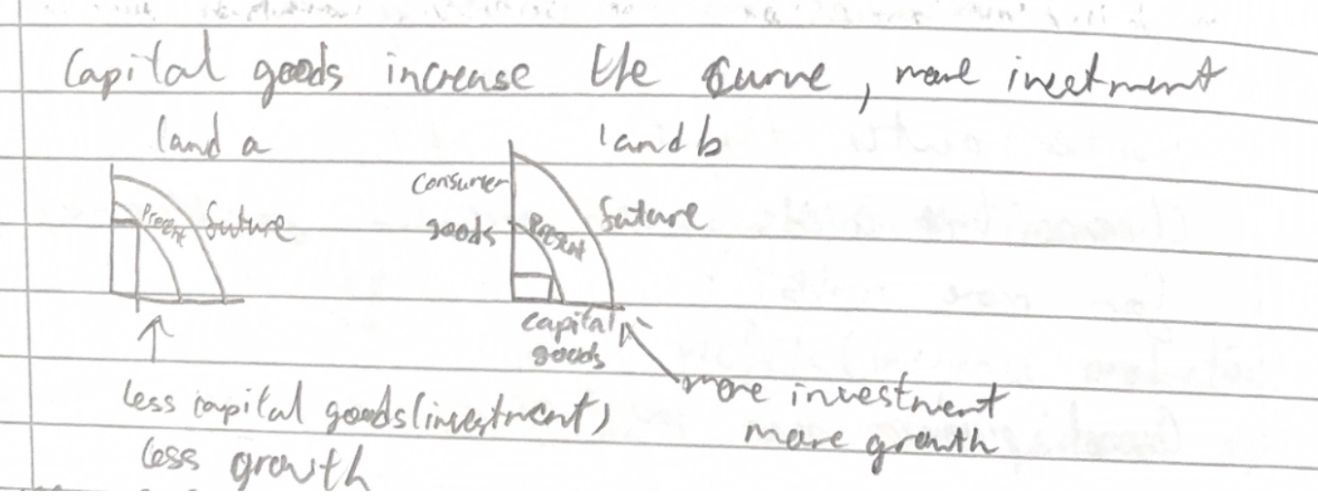

PPC - effect of Capital goods (investment)

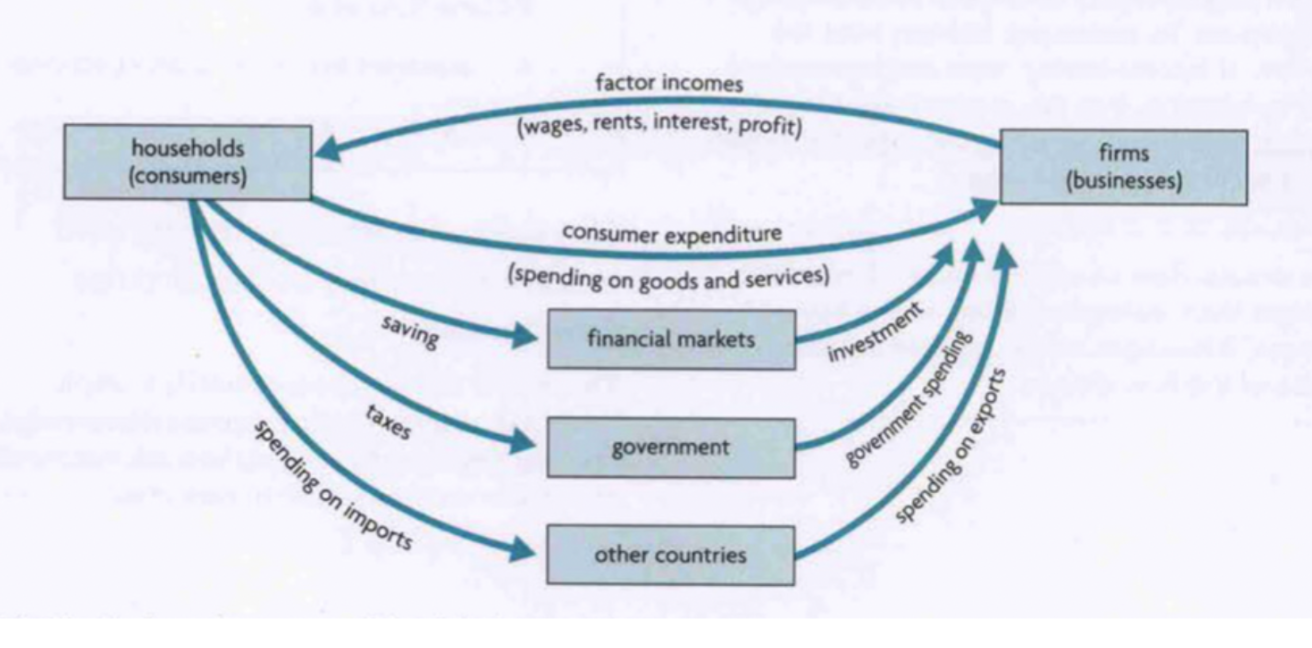

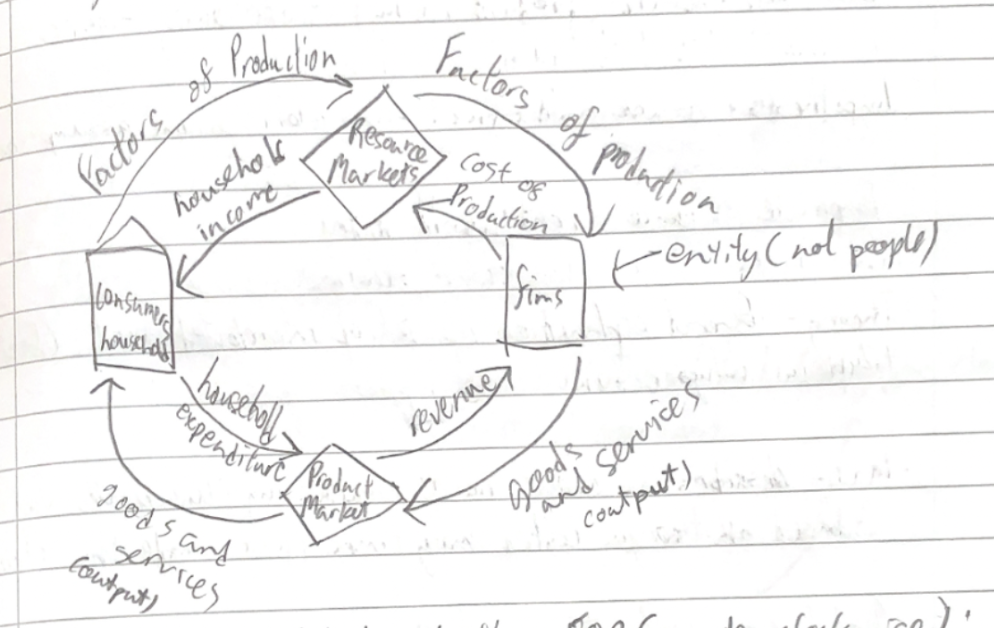

Circular flow of income model

mixed economy more gov intervention

Planned economy, no private sector -gov controls resource and product sector

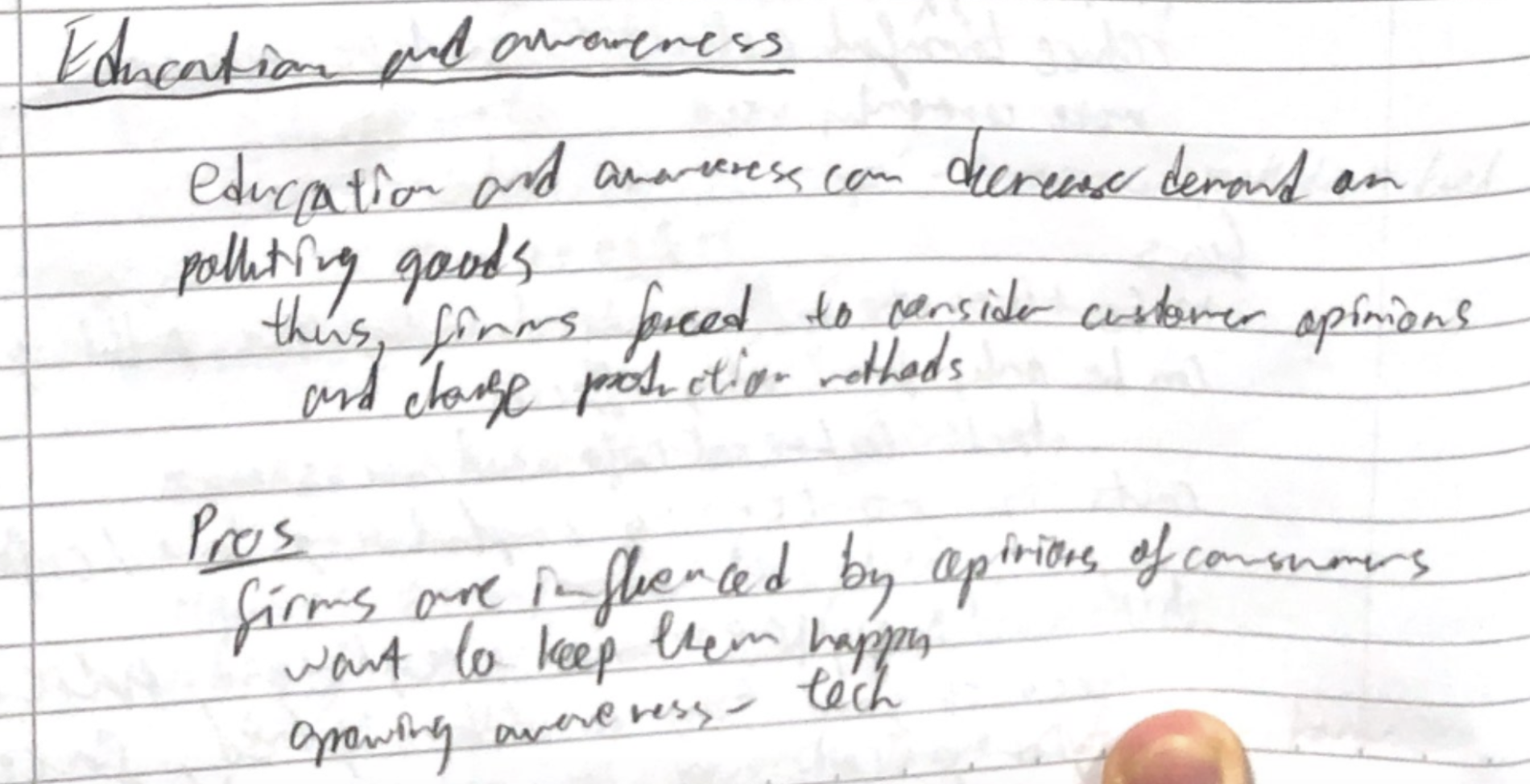

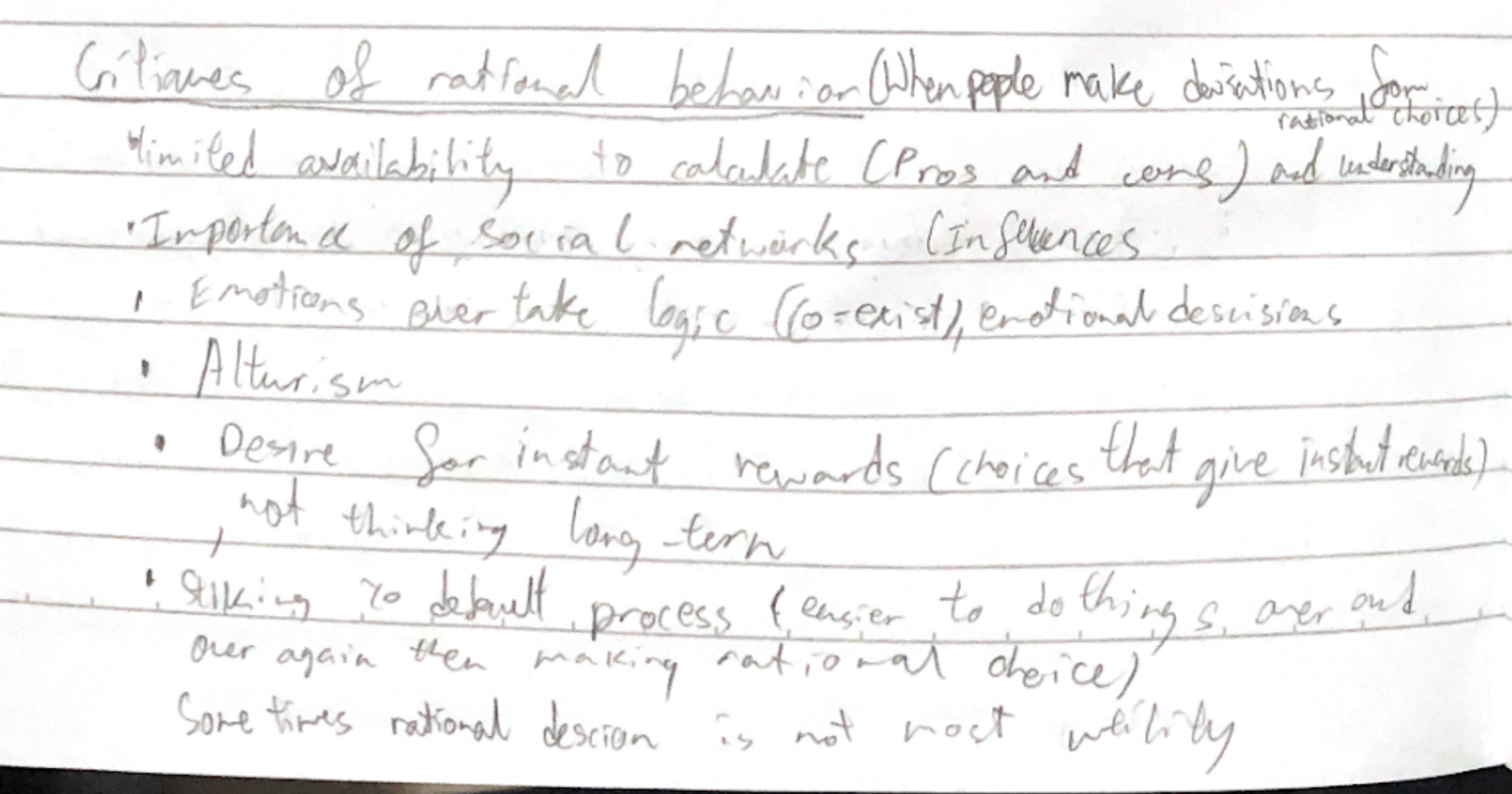

Behavioral econ ctritizes this

Cognitive biases

systematic influences in thinking

Limits to rationality

Bounded rationality - Limits in ability to process all information, thus consumers seek a satisfactory outcome instead of the best

Bounded self-control: People are self contorled only within limits

Bounded selfishness: selfish within limits

Imperfect information

Nudges

when have limited finances do

Choice architecture

framing to influence choice

Illusion of free choice

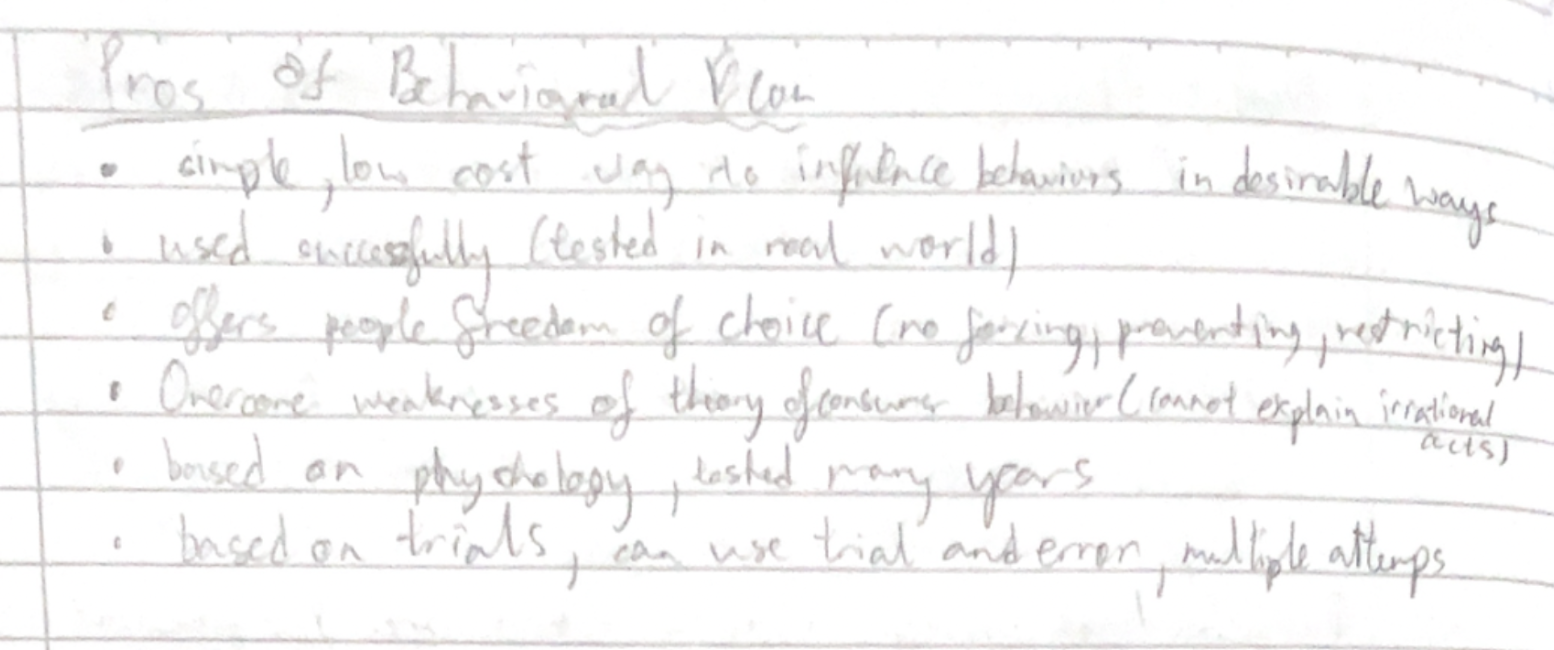

Pros of behavioral econ

Create more socially responsible outcomes

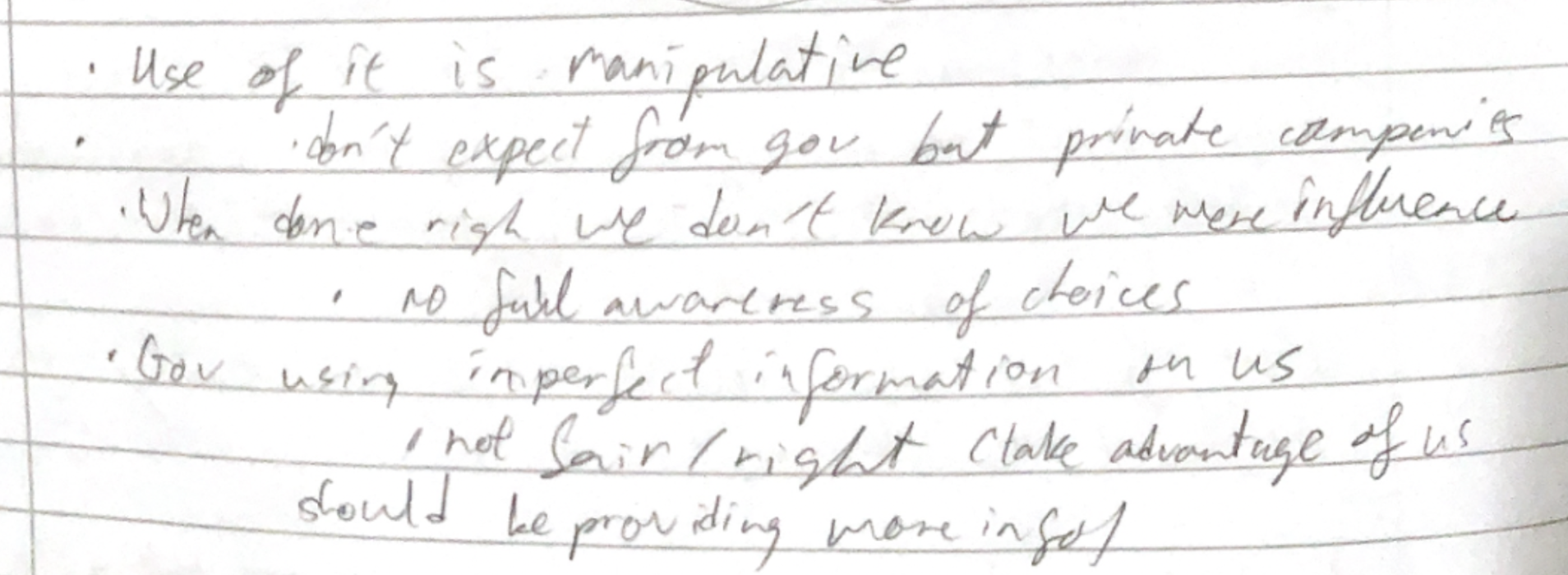

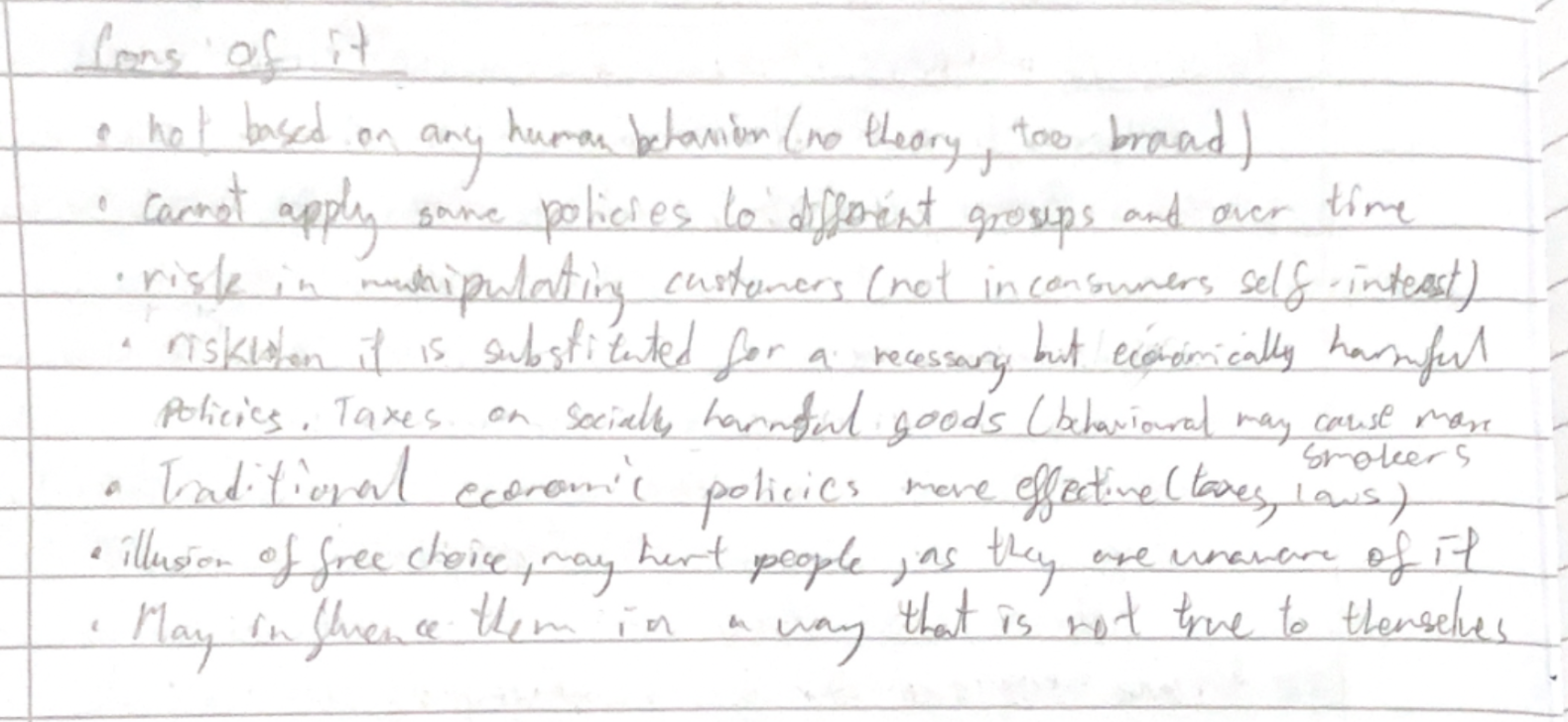

Cons of behavioral econ

Like a gov regulation but disguised as choice

Unexpected outcomes Electricity neighbours comparison People who spent lower, will spend more

Not in individuals benefit

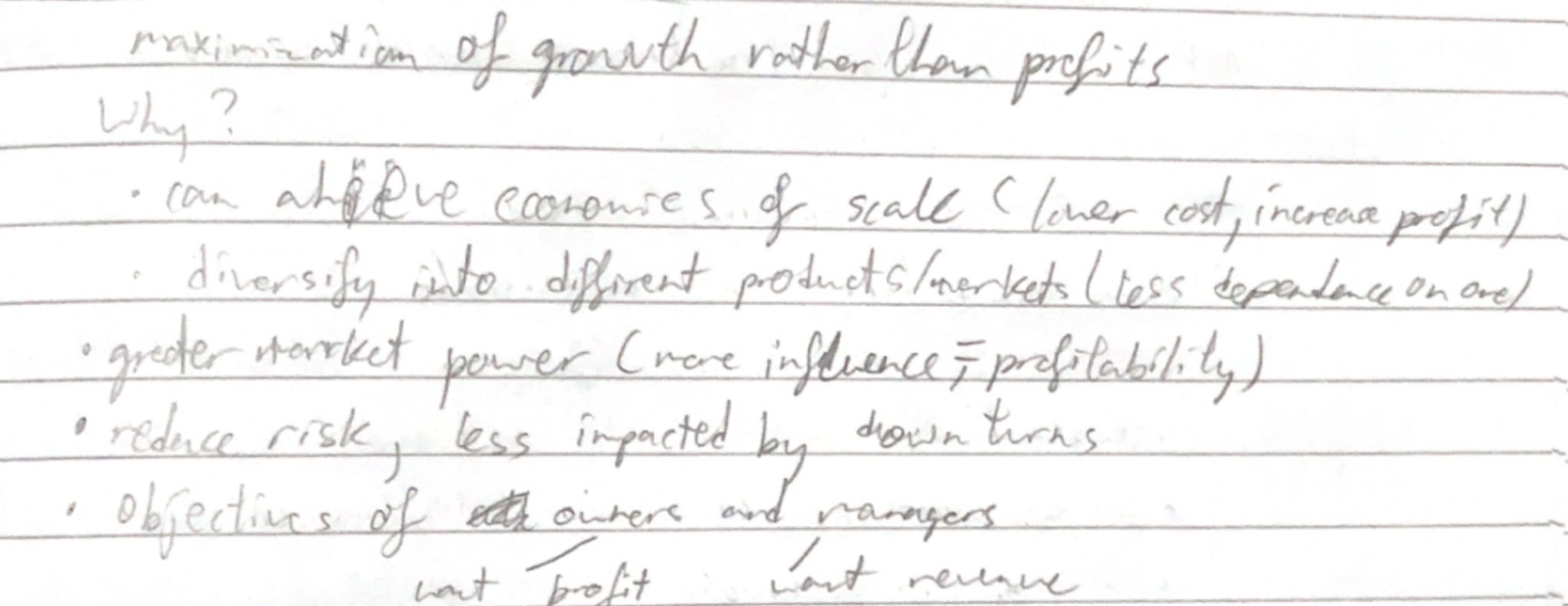

Growth maximiztion for firms why?

satisficing

A decision-making strategy where one chooses the first option that meets the minimum requirements, rather than seeking the optimal solution.

For firm: Instead of maximizing one objective achieve satisfactory result from multiple

Critiques of rational behavior

Demand

Law of diminishing marginal utility

the principle that consumers experience diminishing additional satisfaction as they consume more of a good or service during a given period of time

Shifts of demand

Income

Preference

Substitute goods

Complementary goods

Number of consumers

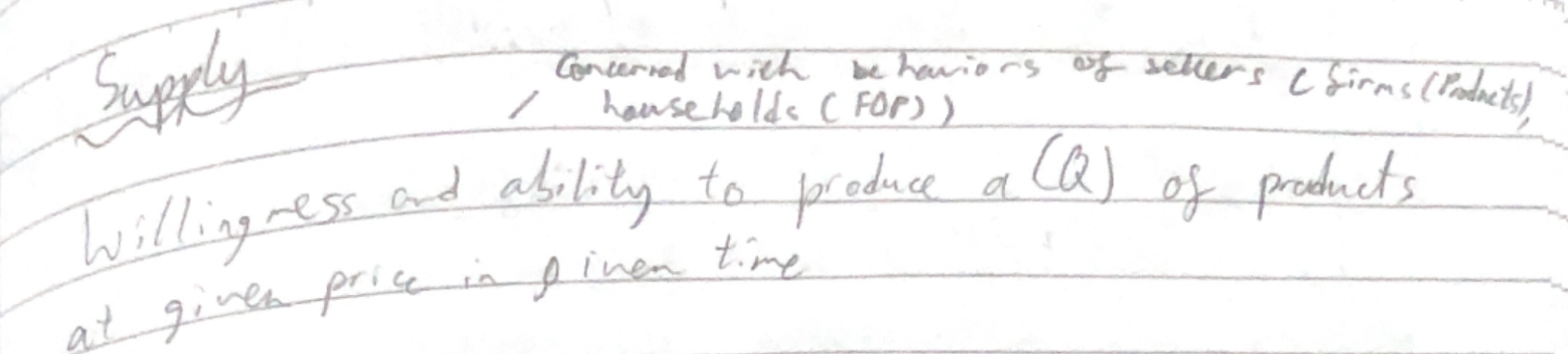

Supply

* Quality/efficiency of FOP

* Tech advancements

* Price of goods

* competing for same resources

* Joint supply - products that result from use of other resources

* Producer price expectations

* Rising prices, may withhold supply from market

* Number of firms

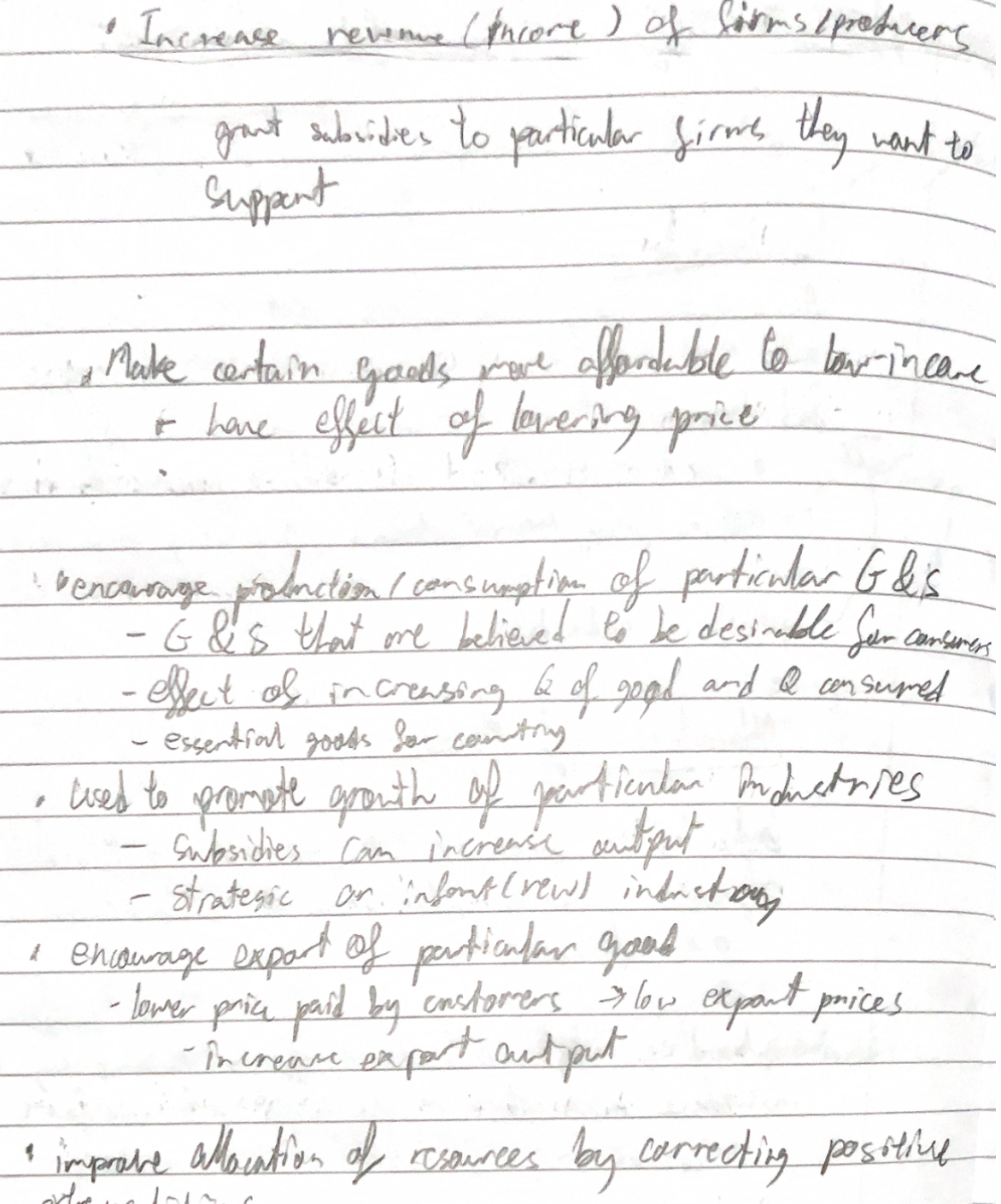

* Government intervention

* Subsidies

* encourage production

* Indirect taxation

* decrease supply

* Taxes paid of G&S

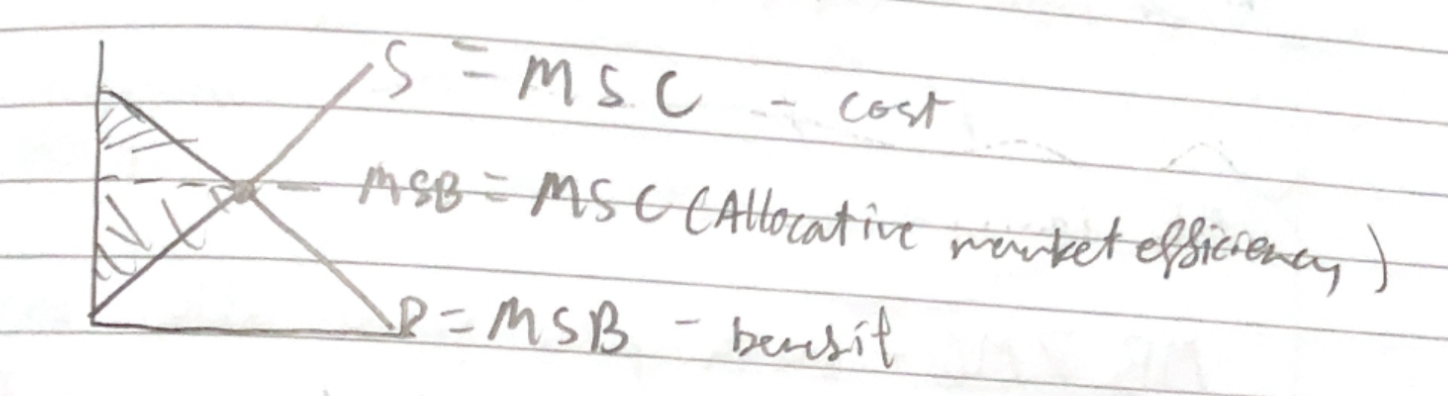

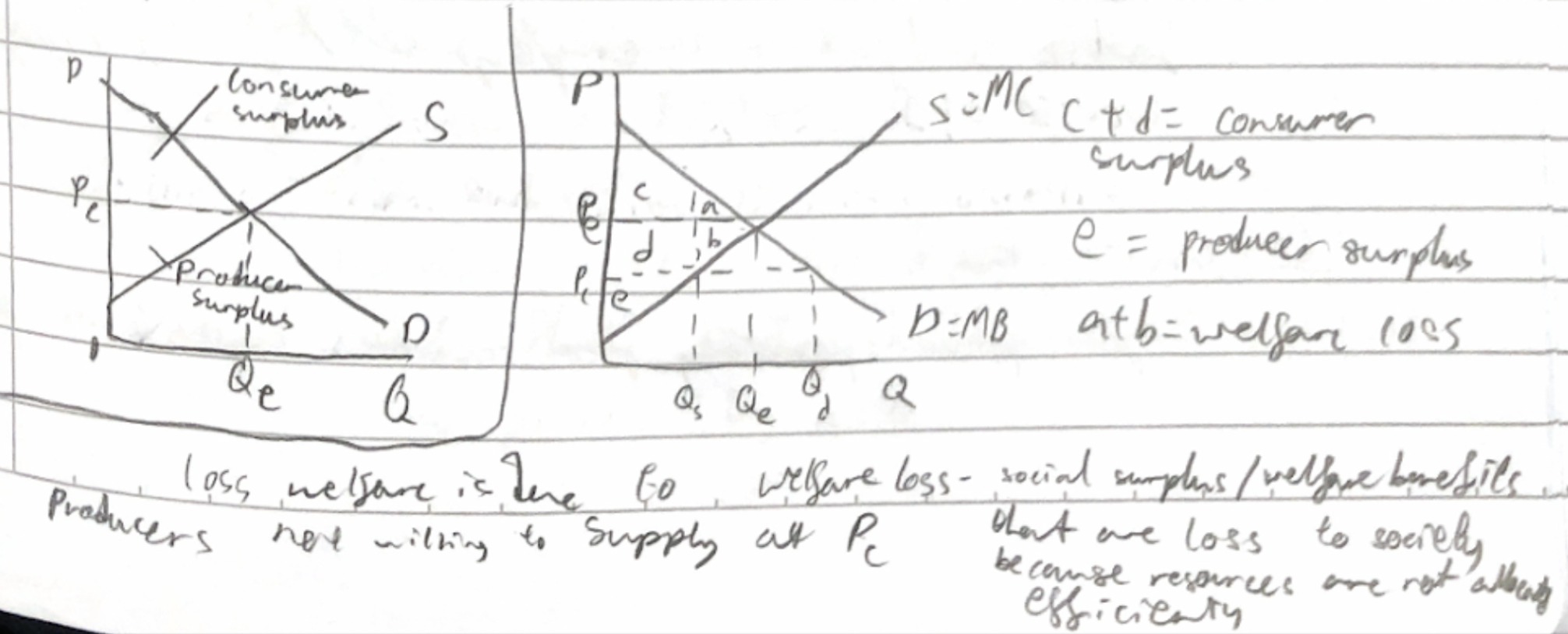

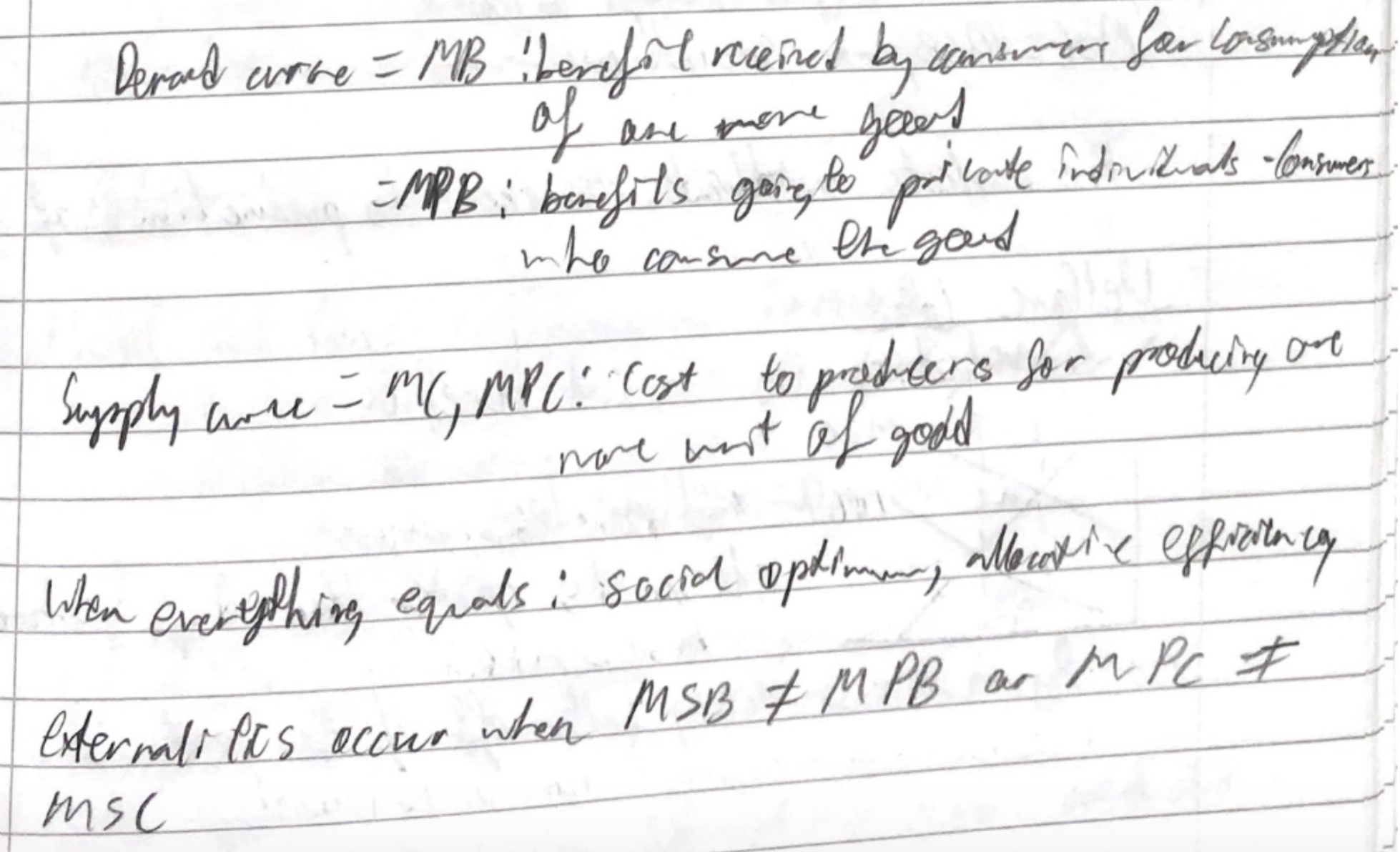

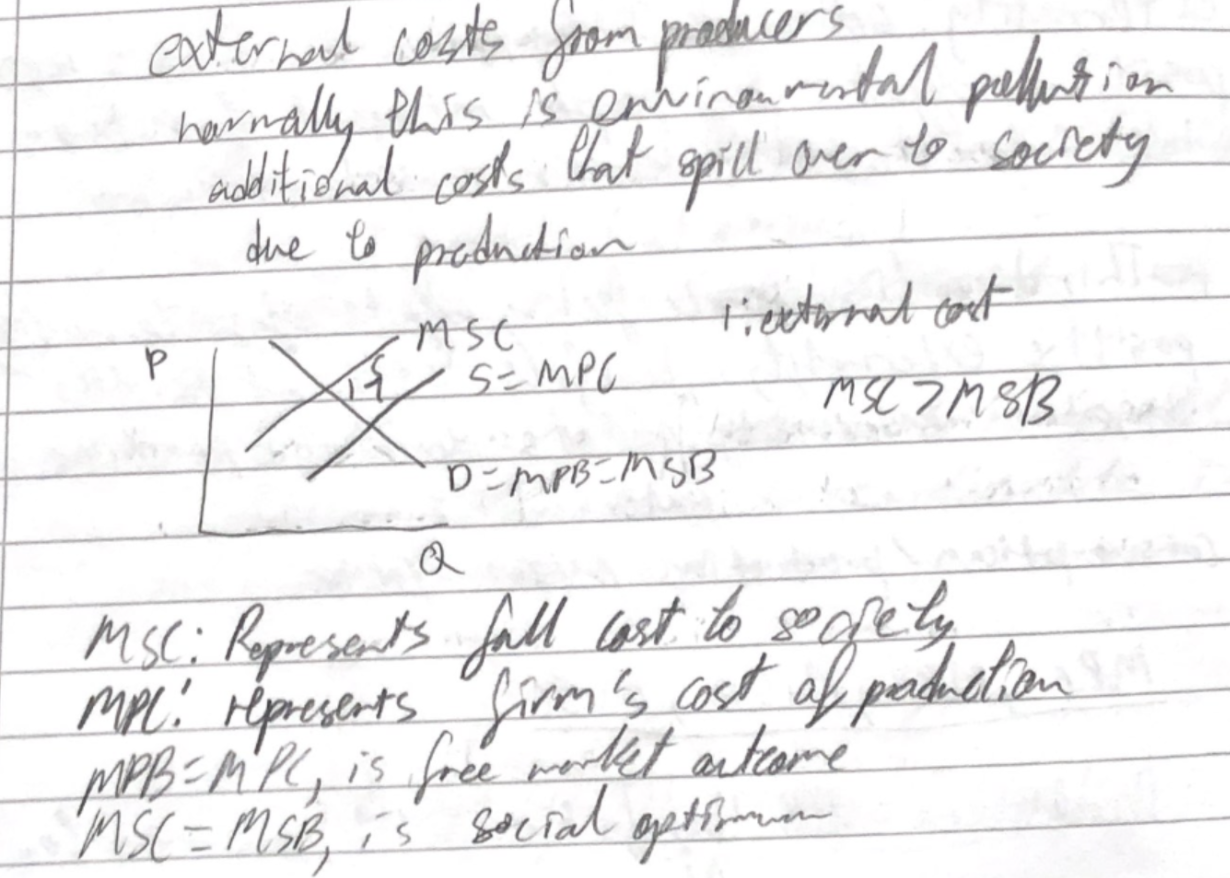

Allocative Efficiency

Consumer and producer surplus

When consumers pay price below willing and able to pay

When producers sell at price above willing and able

* Demand is MB because as each extra unit consumed, benefit decreases. So the curve shows how customers only willing to pay if price falls.

* Supply is MC because extra unit produced, cost increases. So price must increase to cover the costs (curve shows price willing to accept to produce additional unit)

\

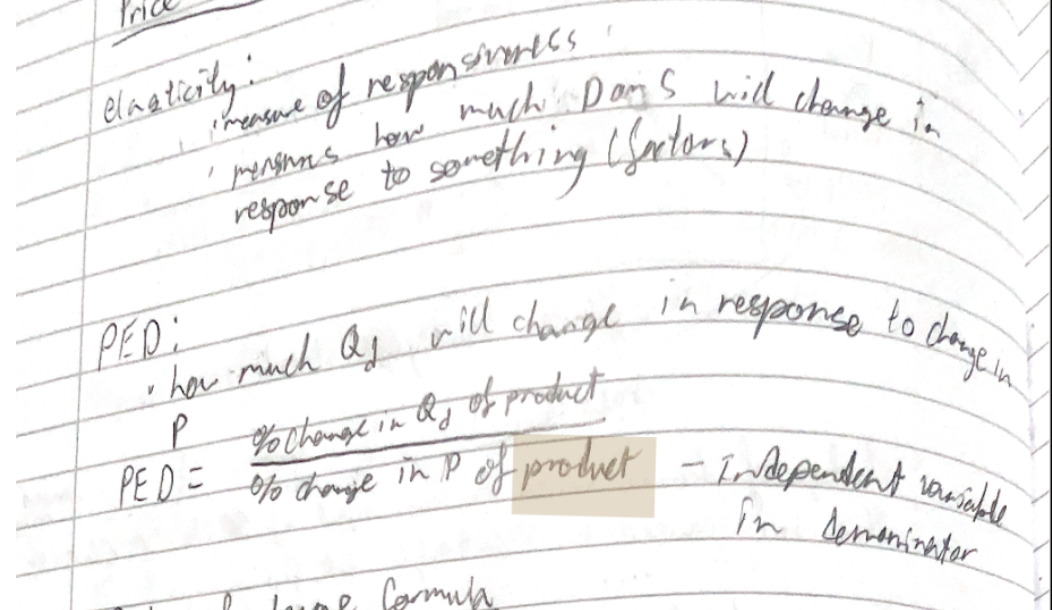

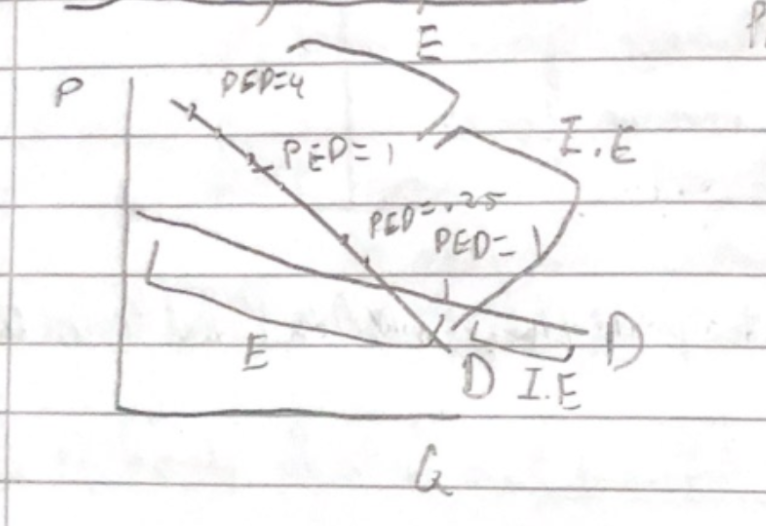

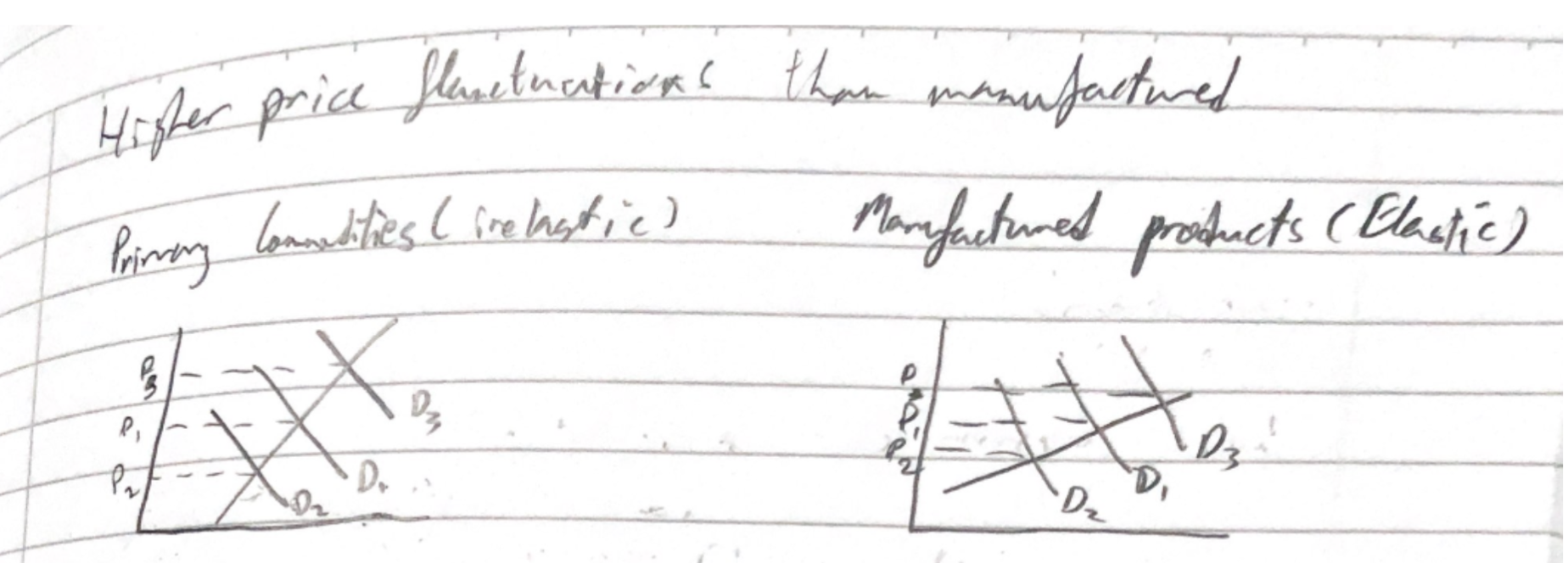

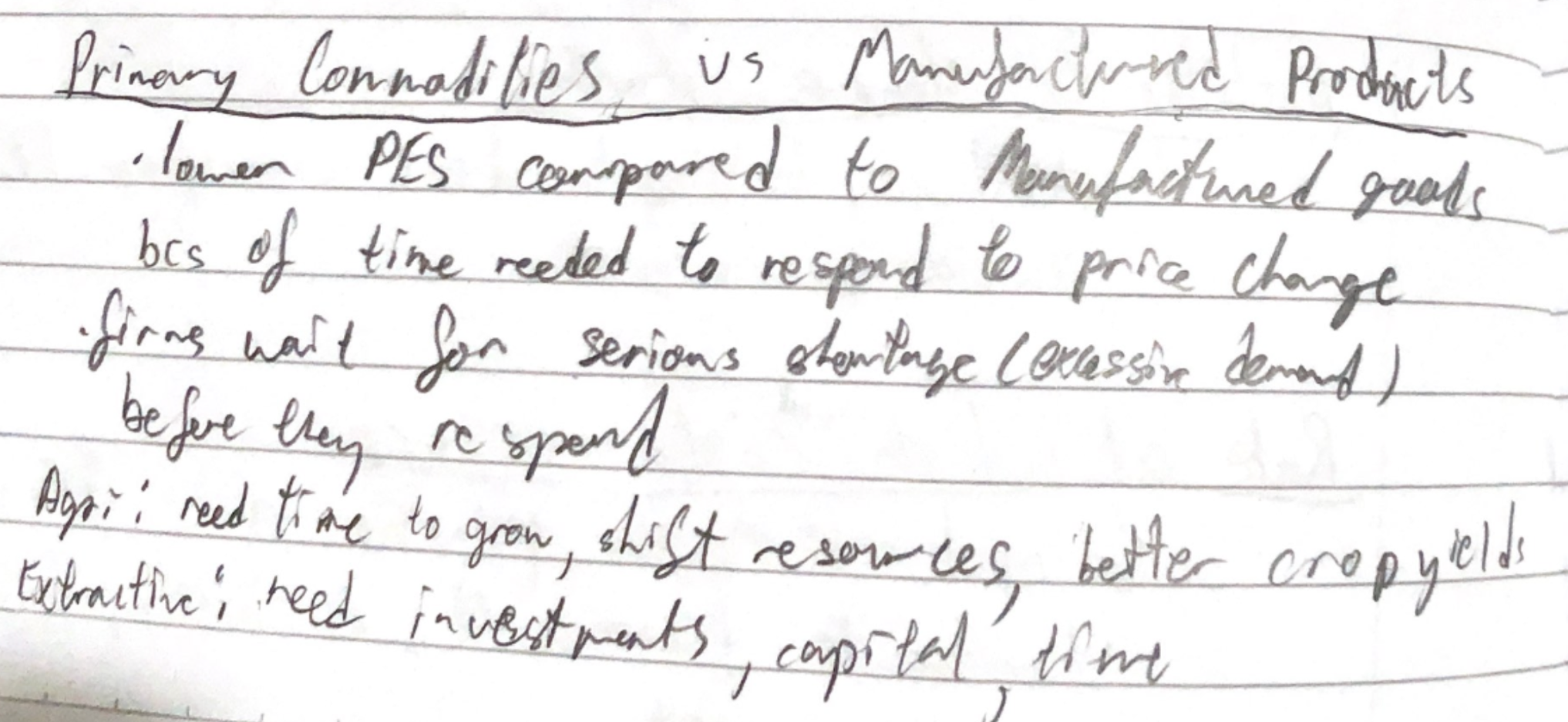

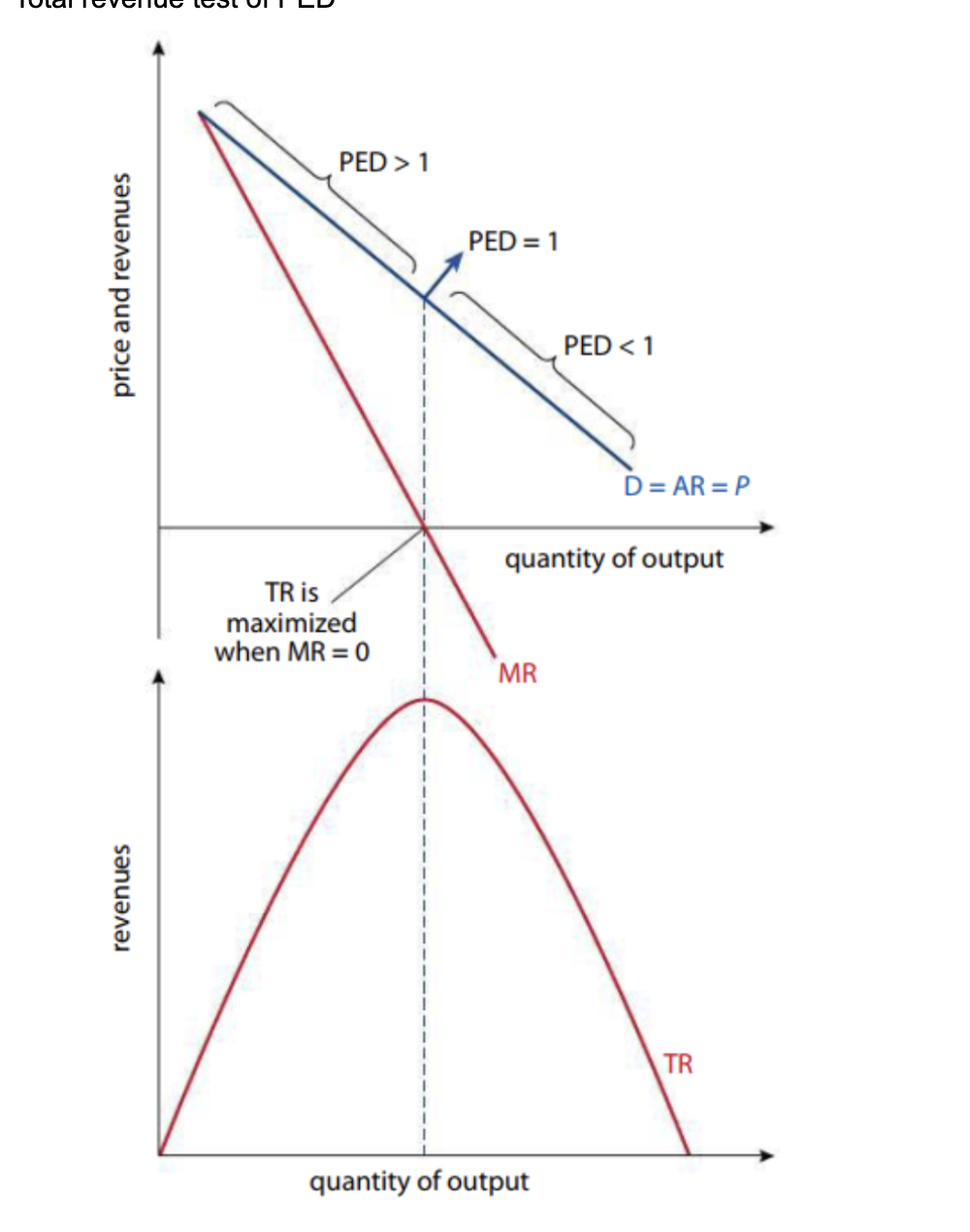

PED

elastic vs inelastic

More responsive to price changes

Less responsive

Lower price, less elastic - price so low no one cares

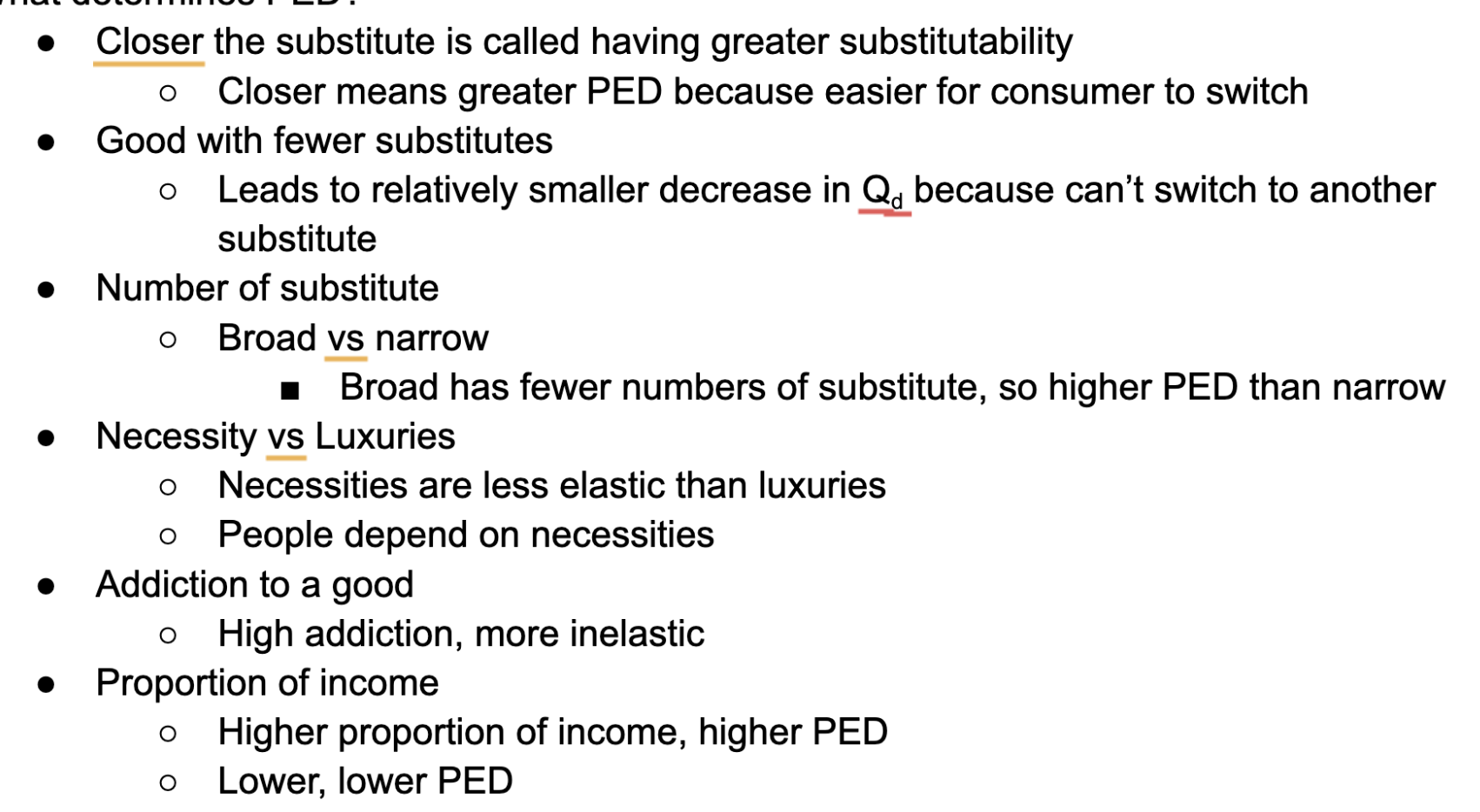

* More time = more elastic

* Have more time to respond

* SPLAT

* sub

* proportion

* Luxury

* Addiction

* Time

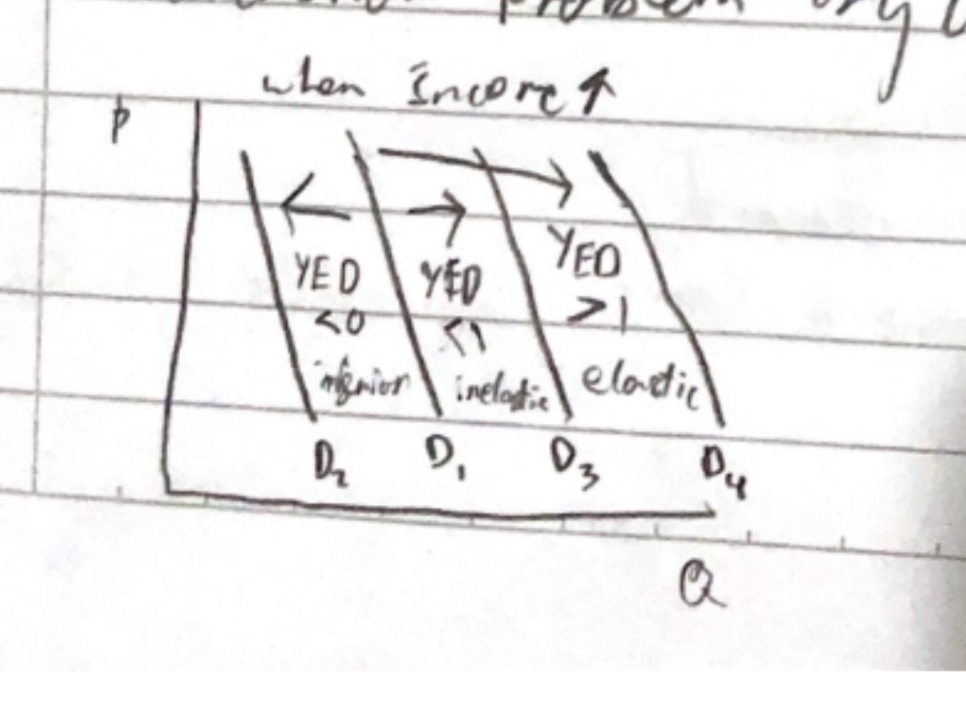

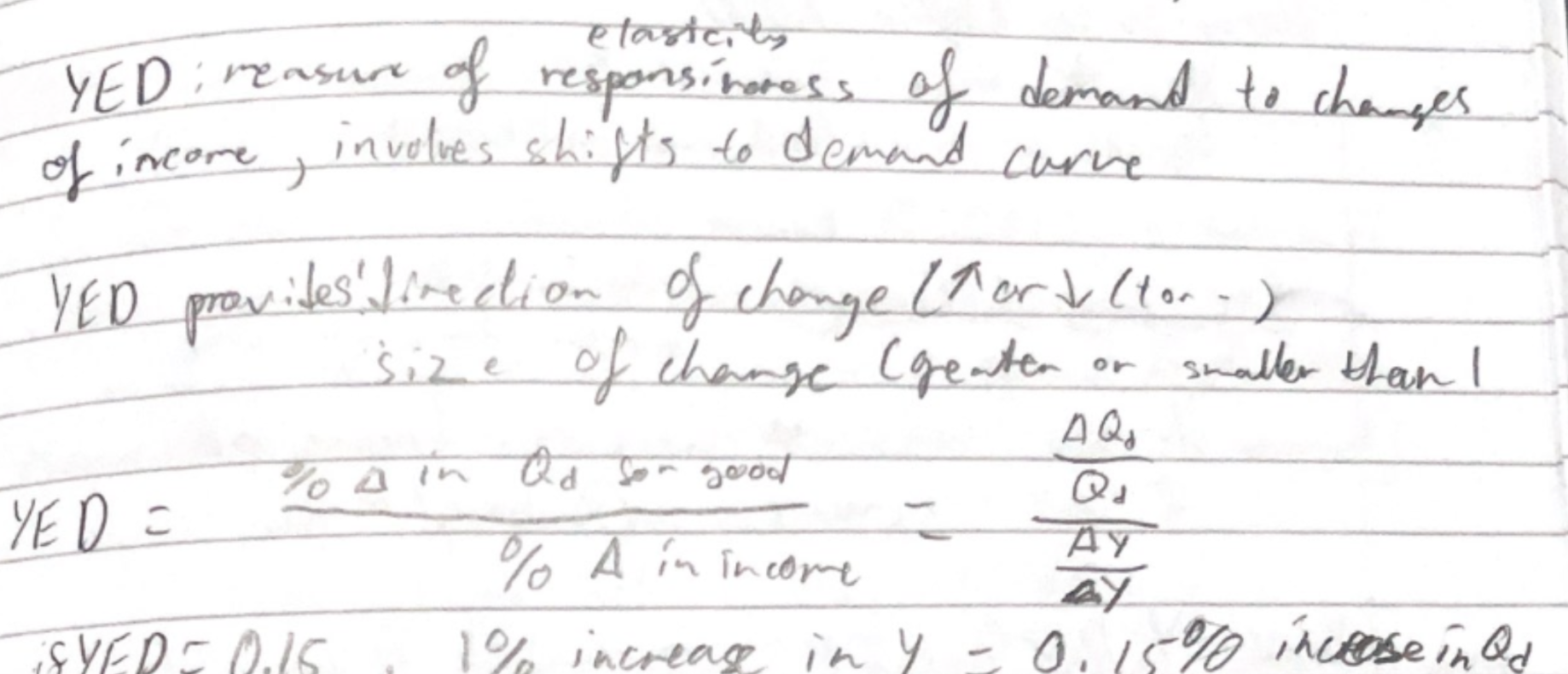

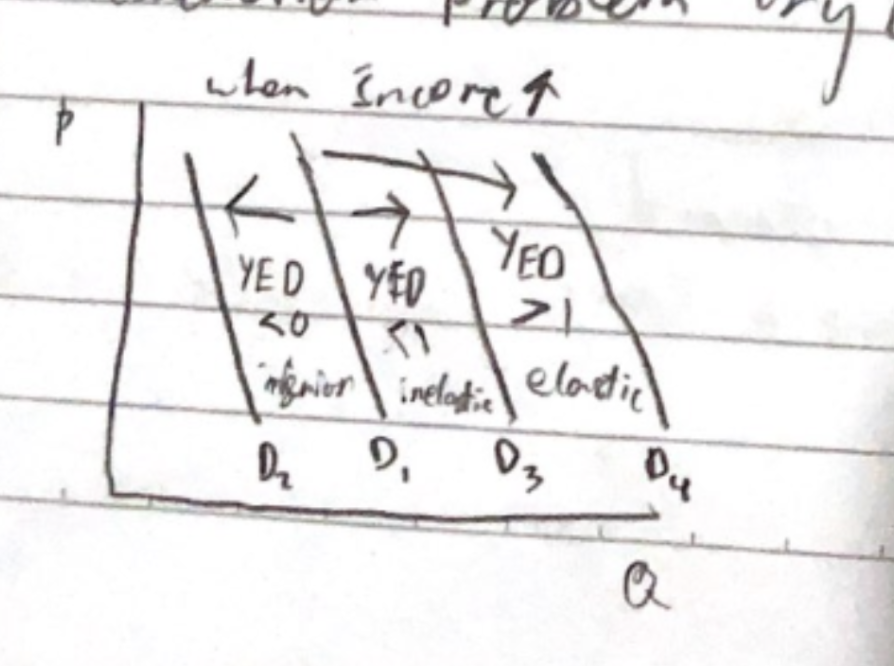

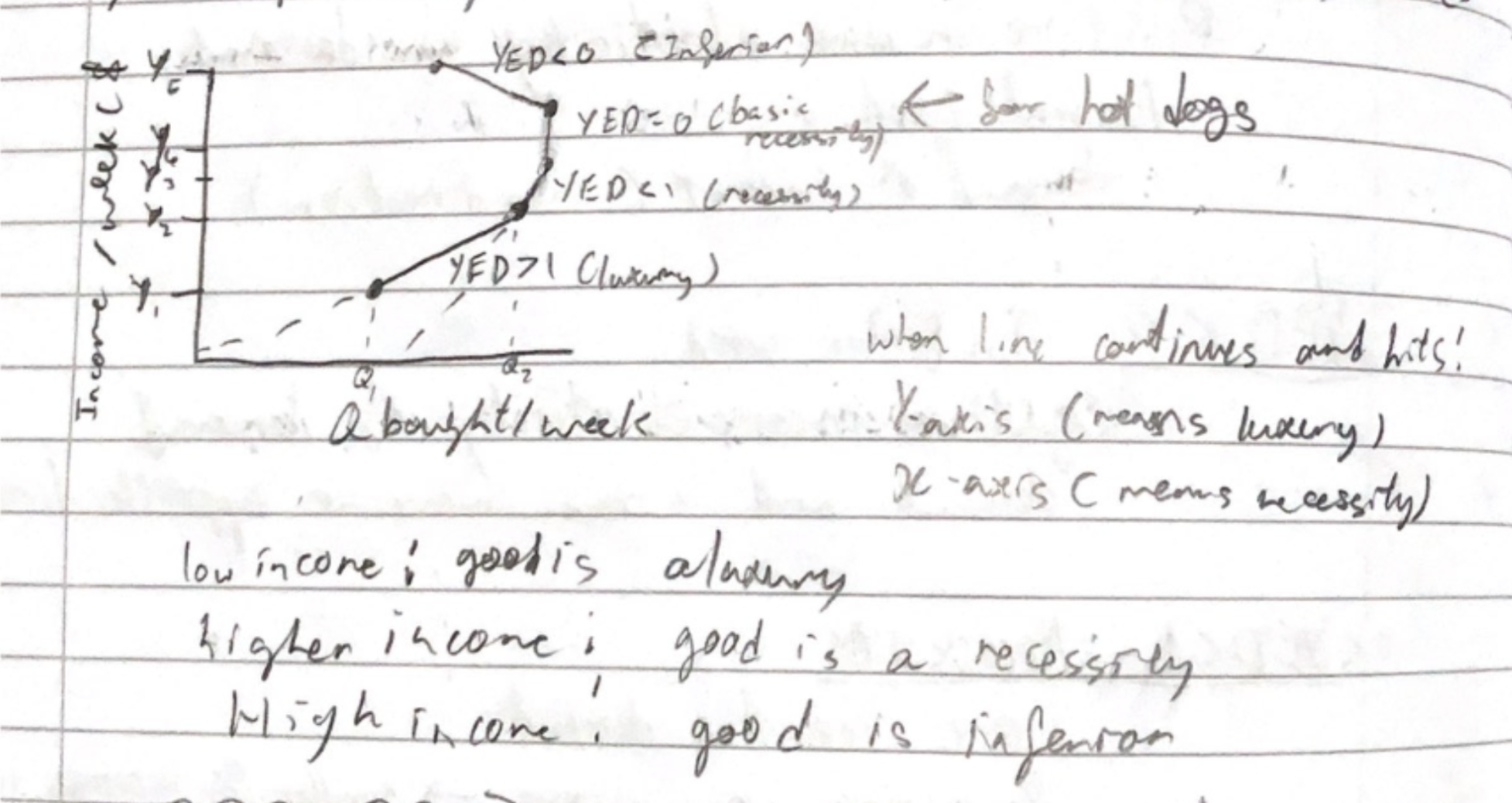

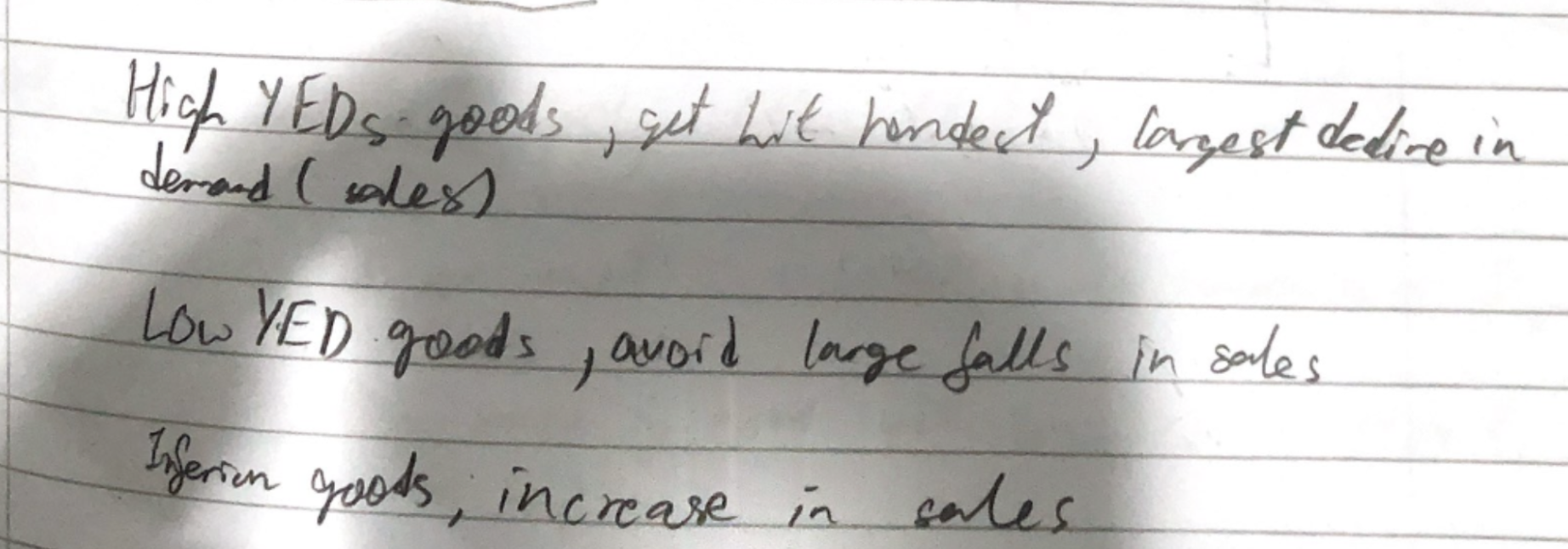

YED

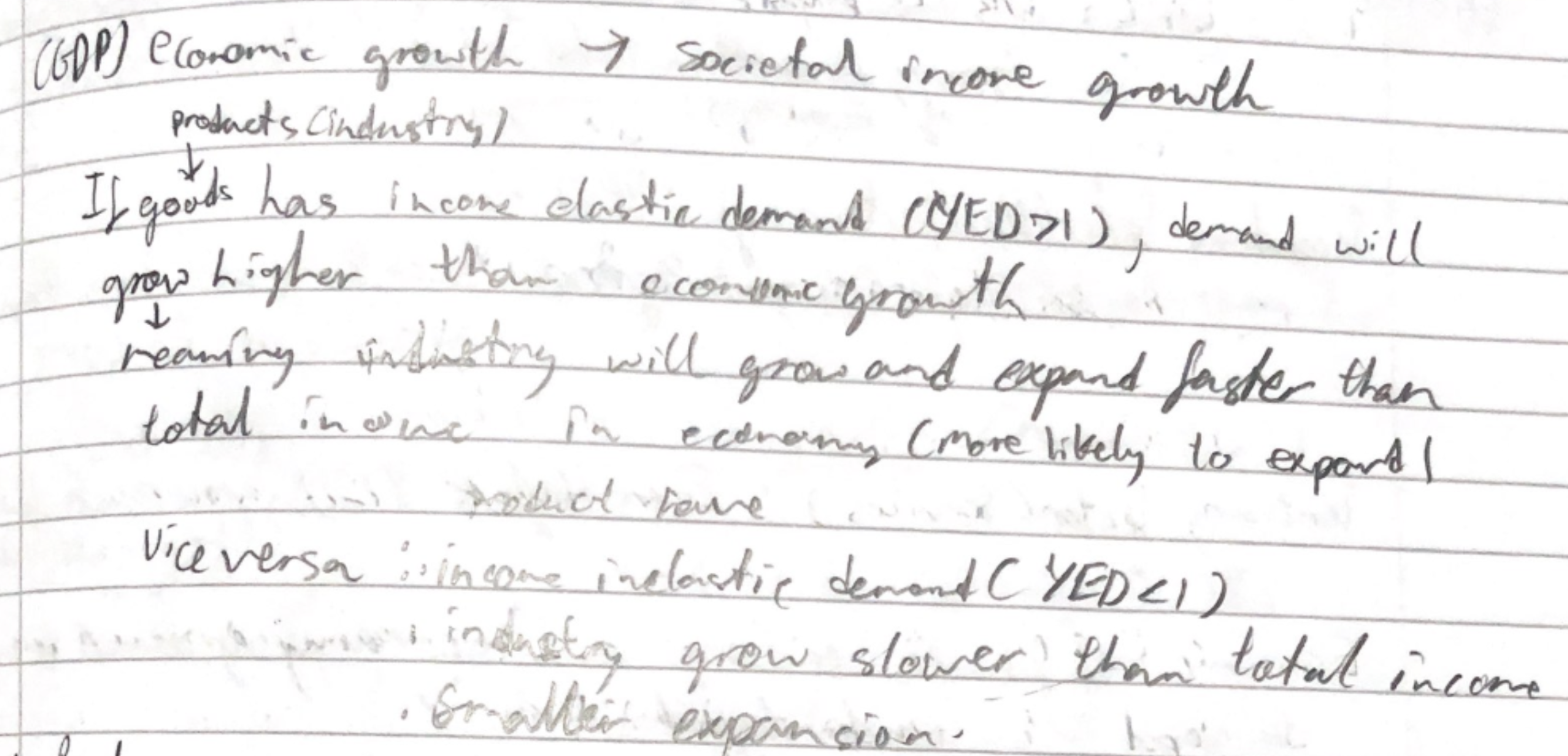

YED on the economy/industries

YED on recessions

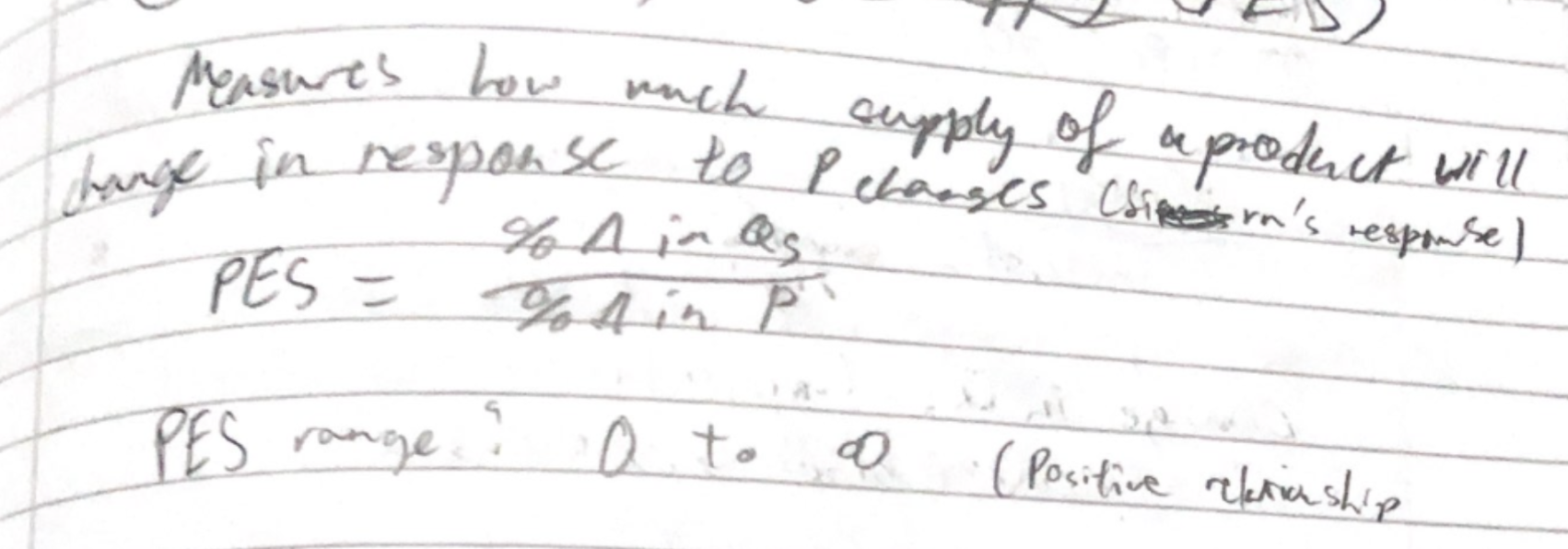

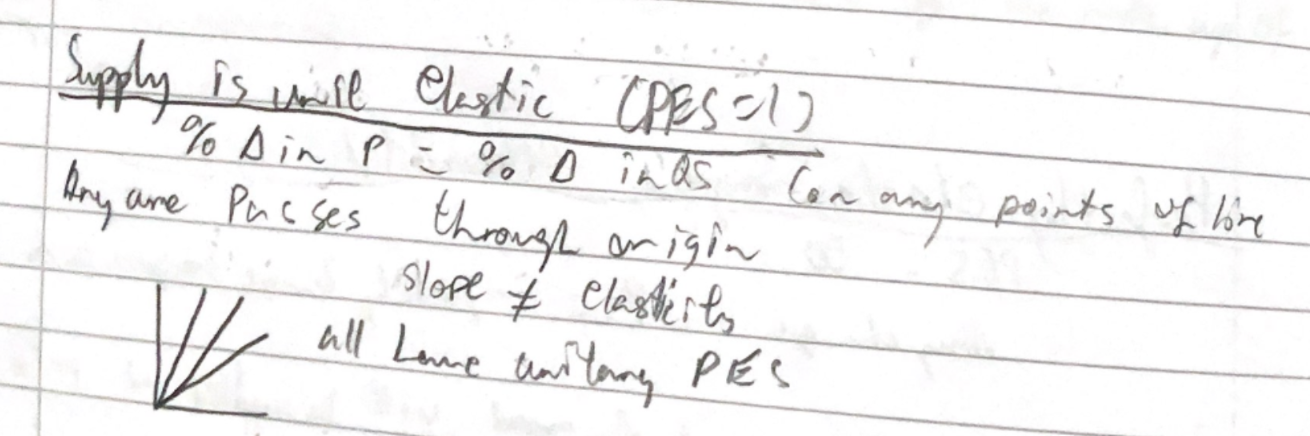

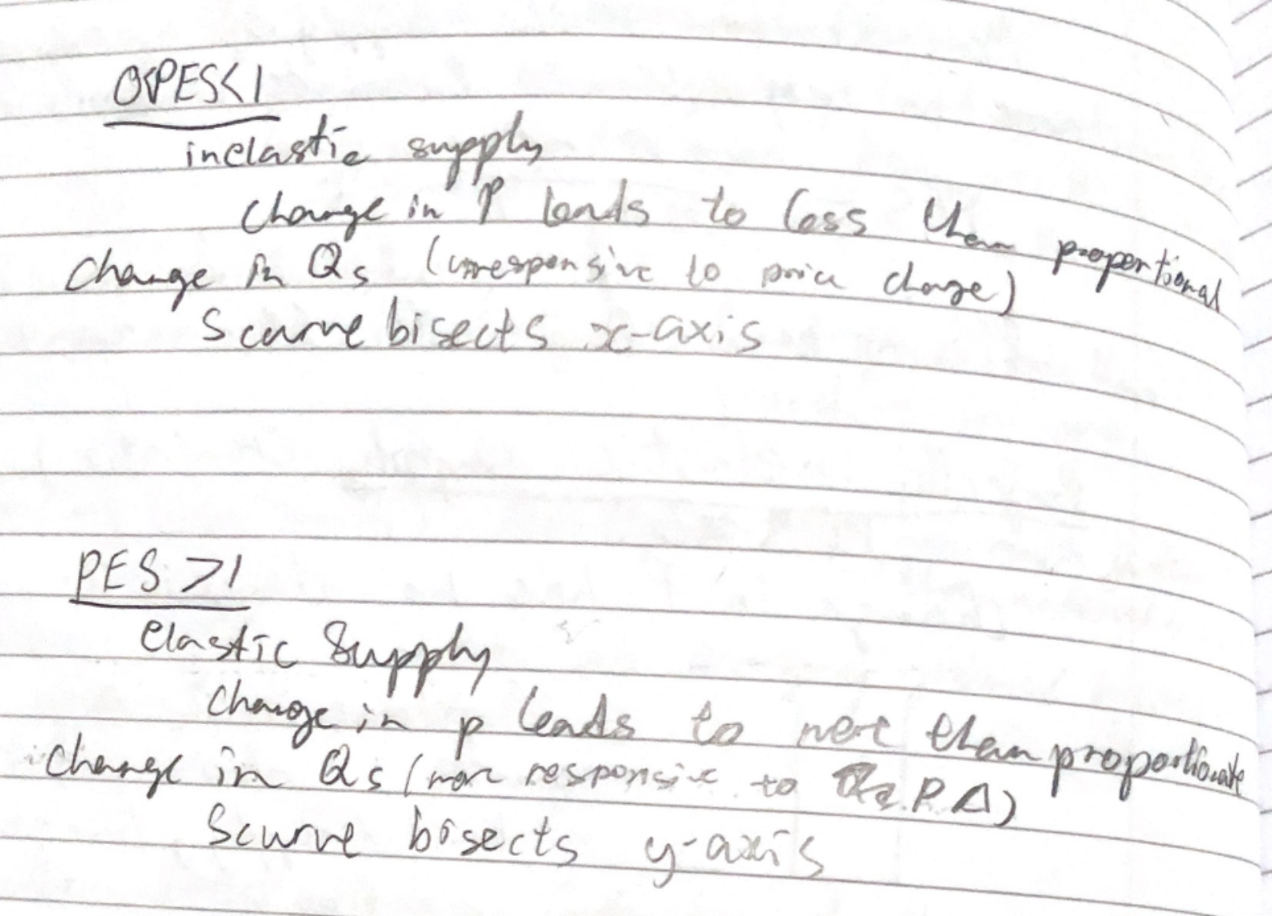

PES and graph intersecitons

* more time higher PES

* Mobility of FOP

* Ease of shifting FOP

* Spare/unused capacity of firms

* More capacity higher PES

* Ability to store stocks

* Quicker to react

* Rate of input cost increases

* Higher rate - lower PES

* Don’t want the costs, harder to get FOP

* \

* so gov will support

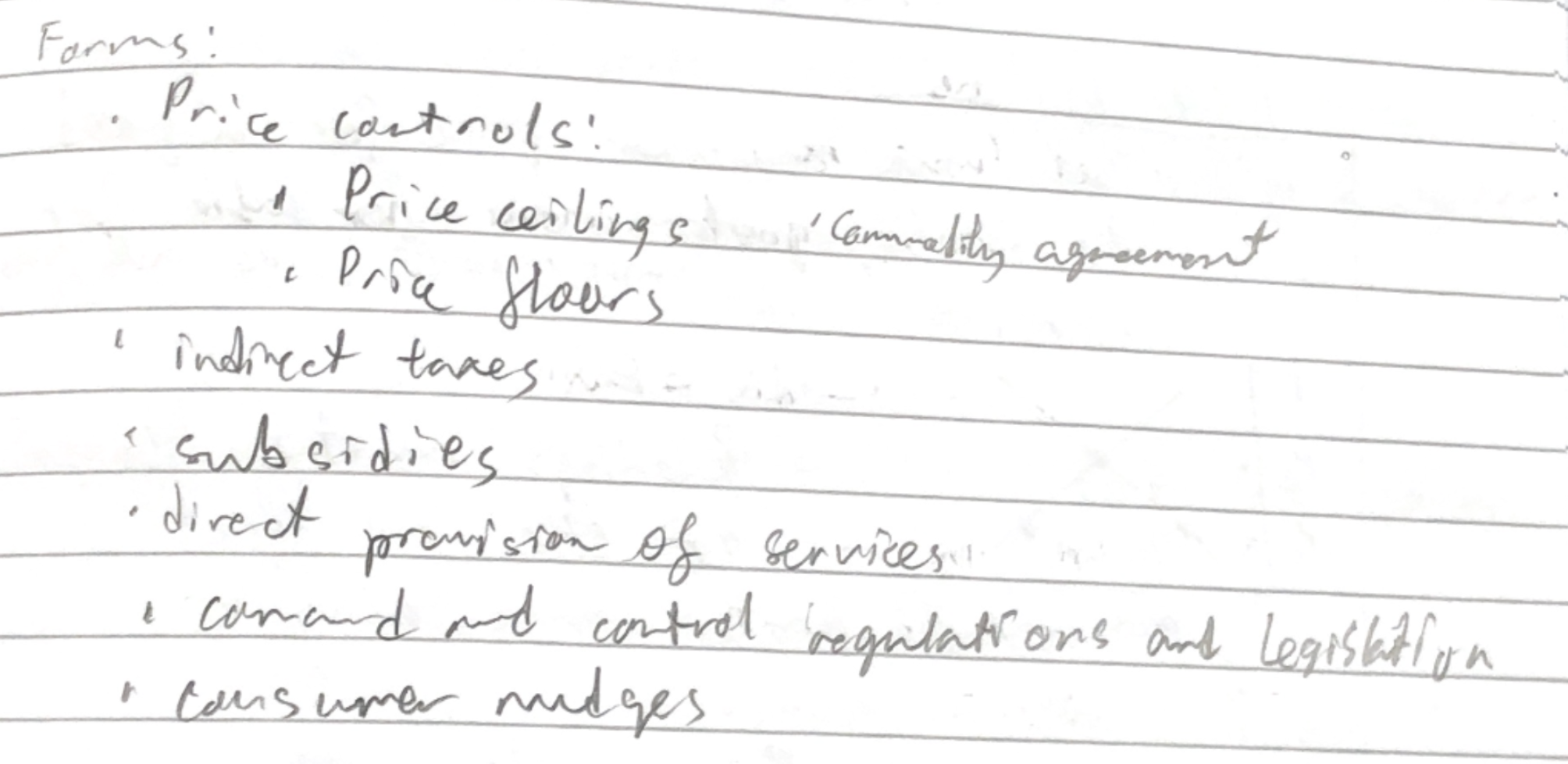

Why govs intervene + Methods

Tax revenue

low ped good

Support for firms

Smaller firms to be able to compete with larger

Encourage the production of certain good

Protect domestic firms

tariffs, import quotas

Trade protection measures

Support low-income households

Meet basic needs

Decourage production of certain good

tax

Influence consumption levels

Demerit merit goods

With subsidies, direct provision of goods, nudges, taxes

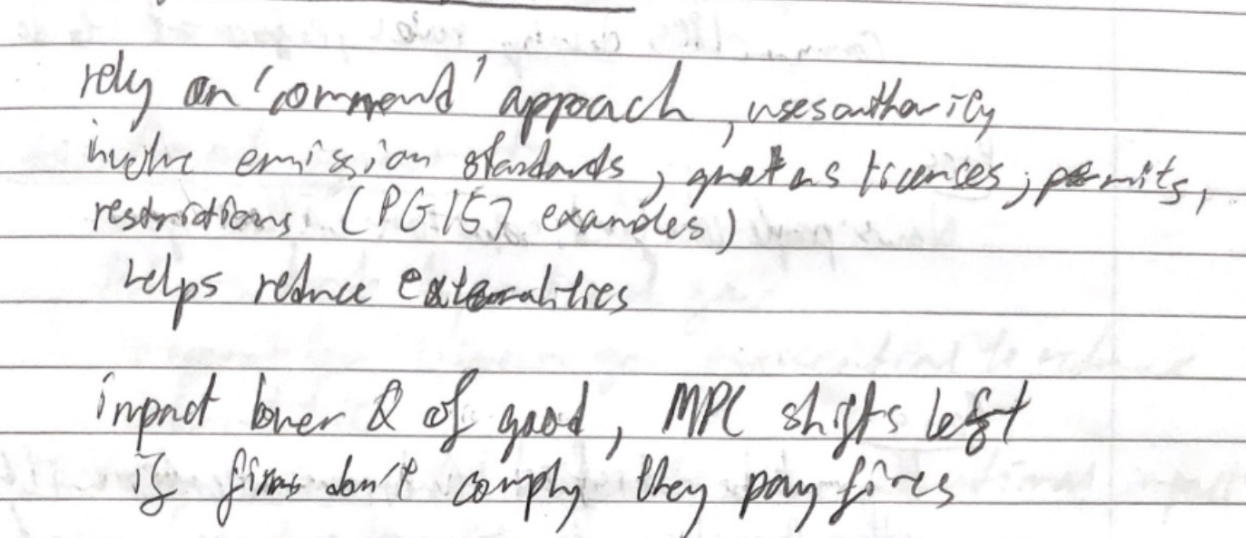

Command and control methods

compulsary education

Correct market failure

Not allocative efficient

Promote equity

Fairness

Helps redistribute income

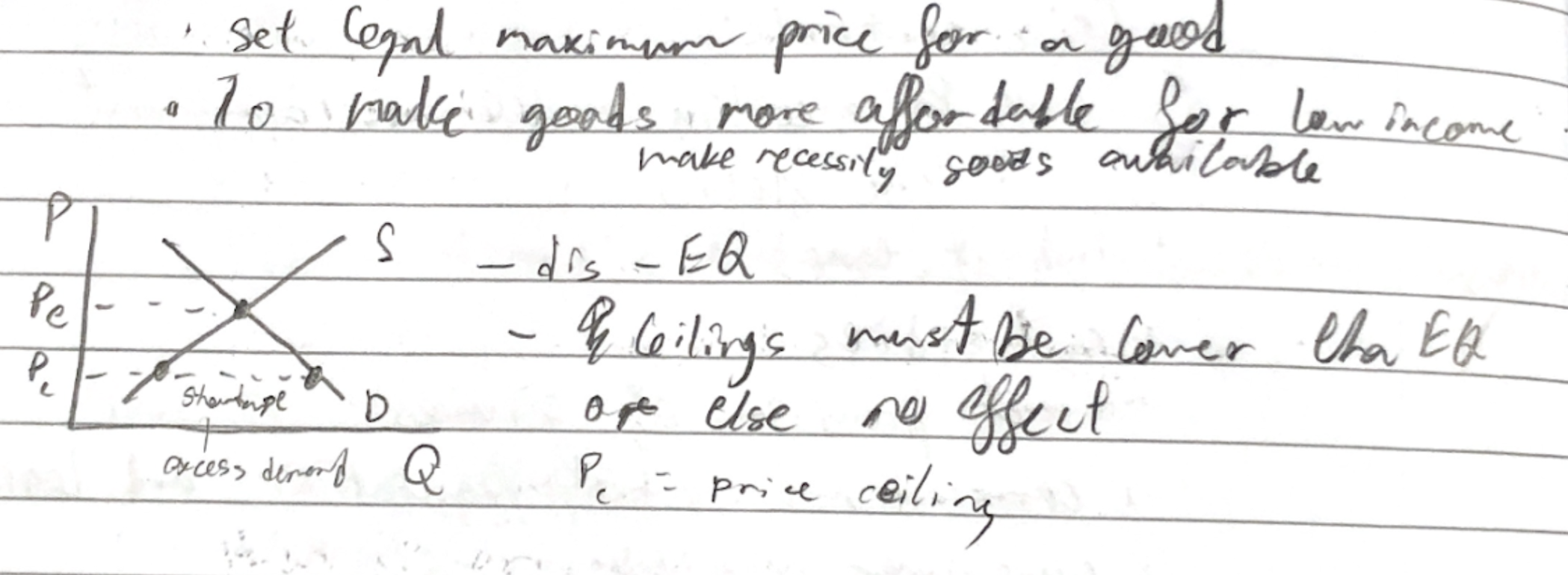

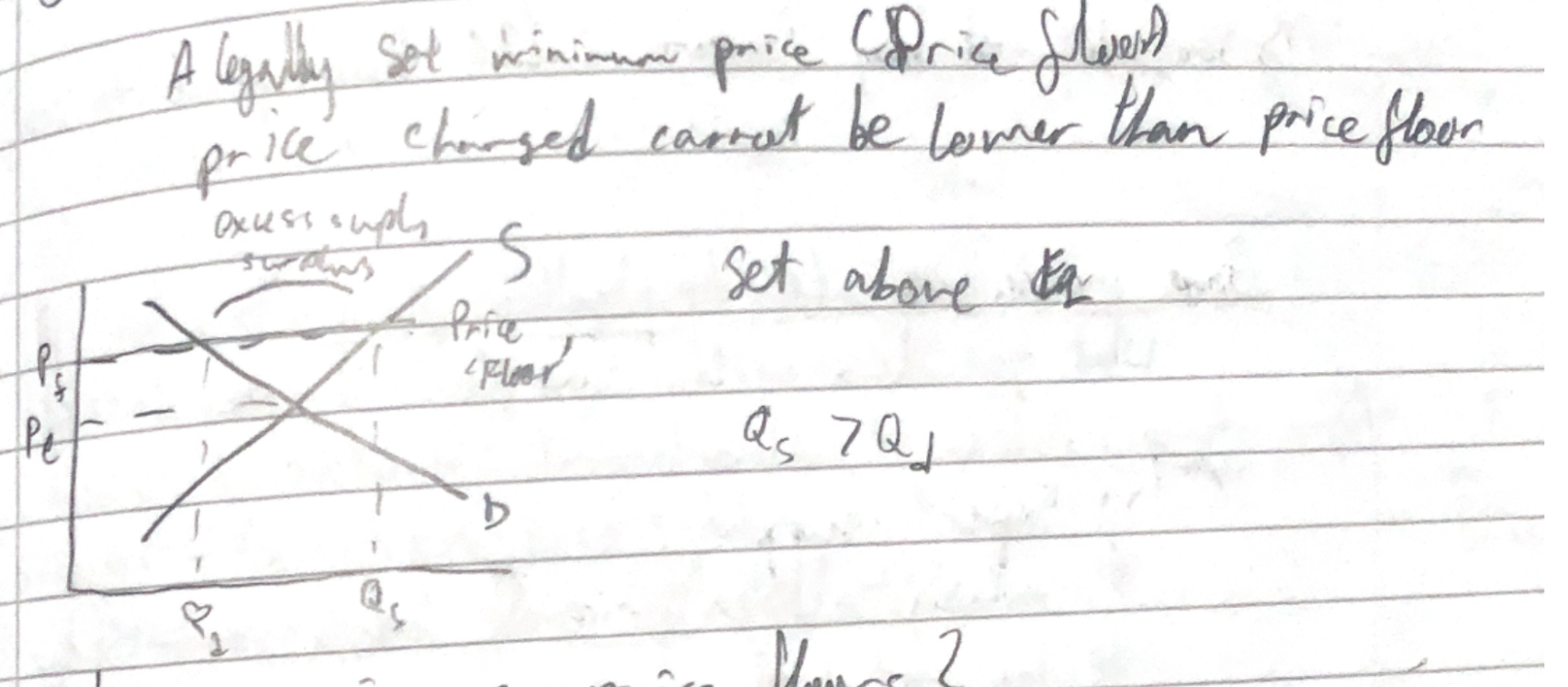

Price ceilings - consequences, how it looks

Lower P

Lower Qs

Lower Rev

Higher Qd

Disequilibrium

Shortage

Not enough resources allocated

* Divide up resources

* no longer use price

* Underground markets

* Buying/selling that isn’t recorded

* illegal

* Those willing to pay more

Consumers gaining more benefit than cost of society to produce

* Consumers partially gain and lose

* Those buying lower price win

* Cannot then lose

* Producers are worse off

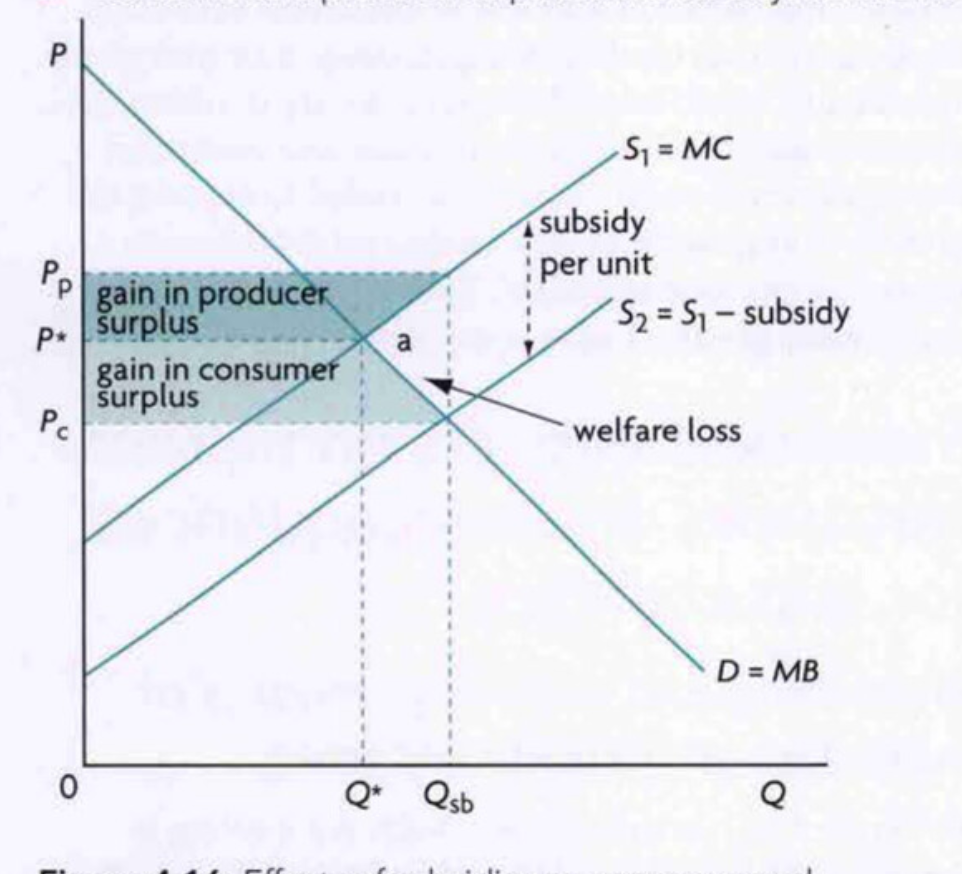

* Reduce price for substitute goods, using subsidies

* Or rationing good

* Shift s curve right

* Subsidies, less tax

* Direct provision

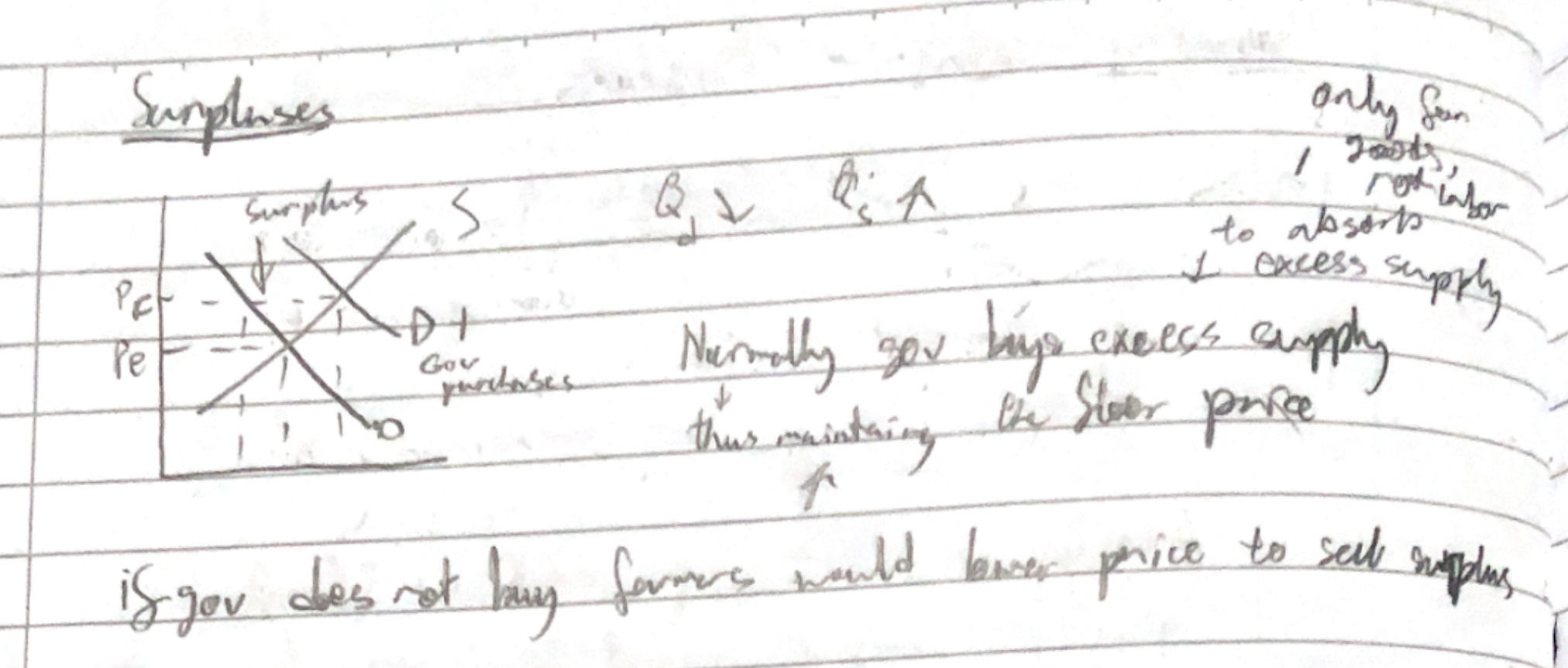

* Buffer stock

* Protect product markets

* Minimum wages

* Dispose surplus through

* Exports

* Storing

* Or just pay them the money but don’t produce good

* No incentive to reduce costs

* Overallocation

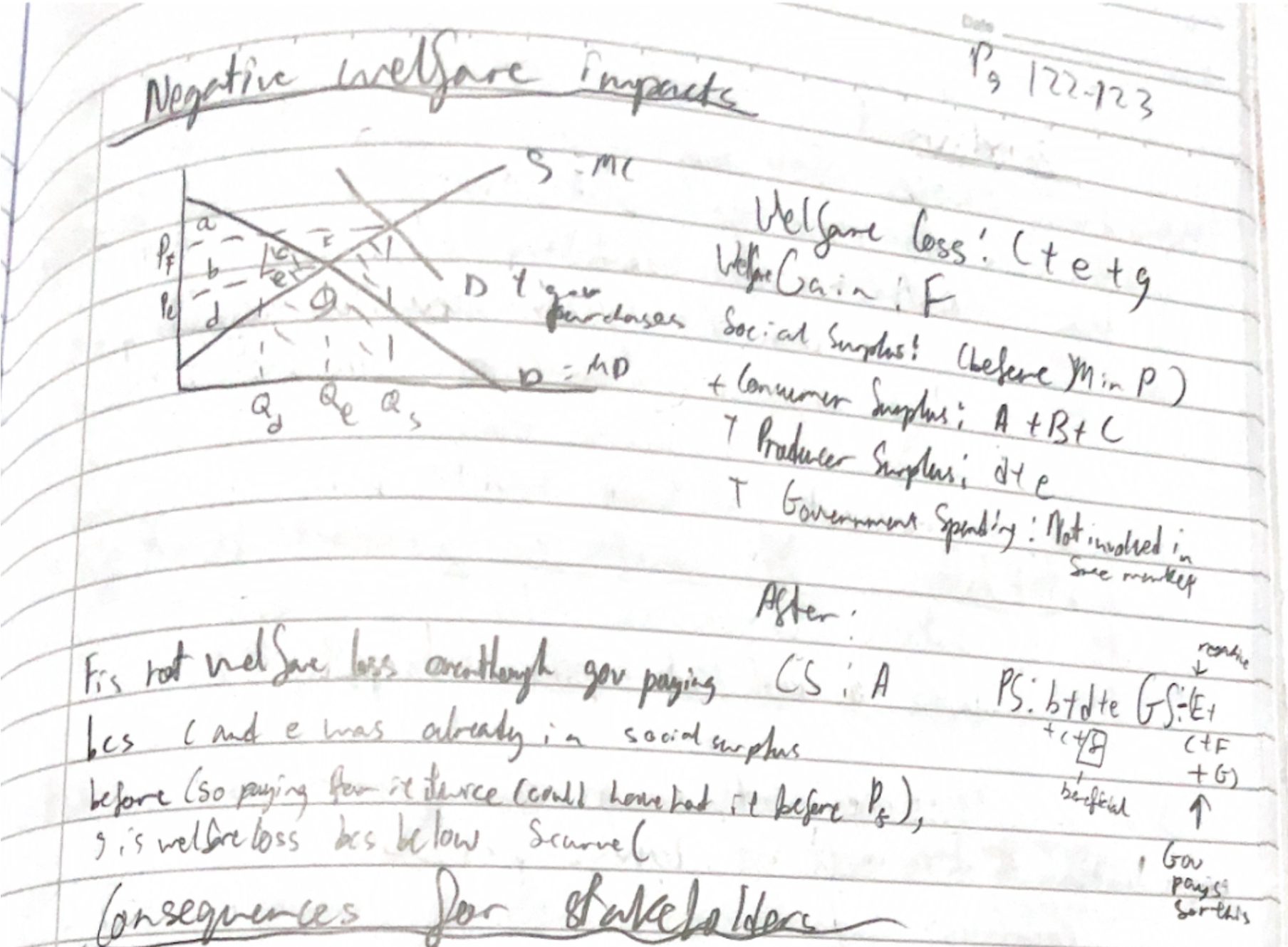

* Welfare impacts

* Consumers: a

* Producers gain from S above to Qs, below Pf

* F is not welfare loss bcs it’s gained through this

* Gov must buy the excess supply from Qs to Qd rectangle

* Welfare loss = rectangle-f

* Other countries

* Worse off for them bcs selling at lower price so may lower market price in world

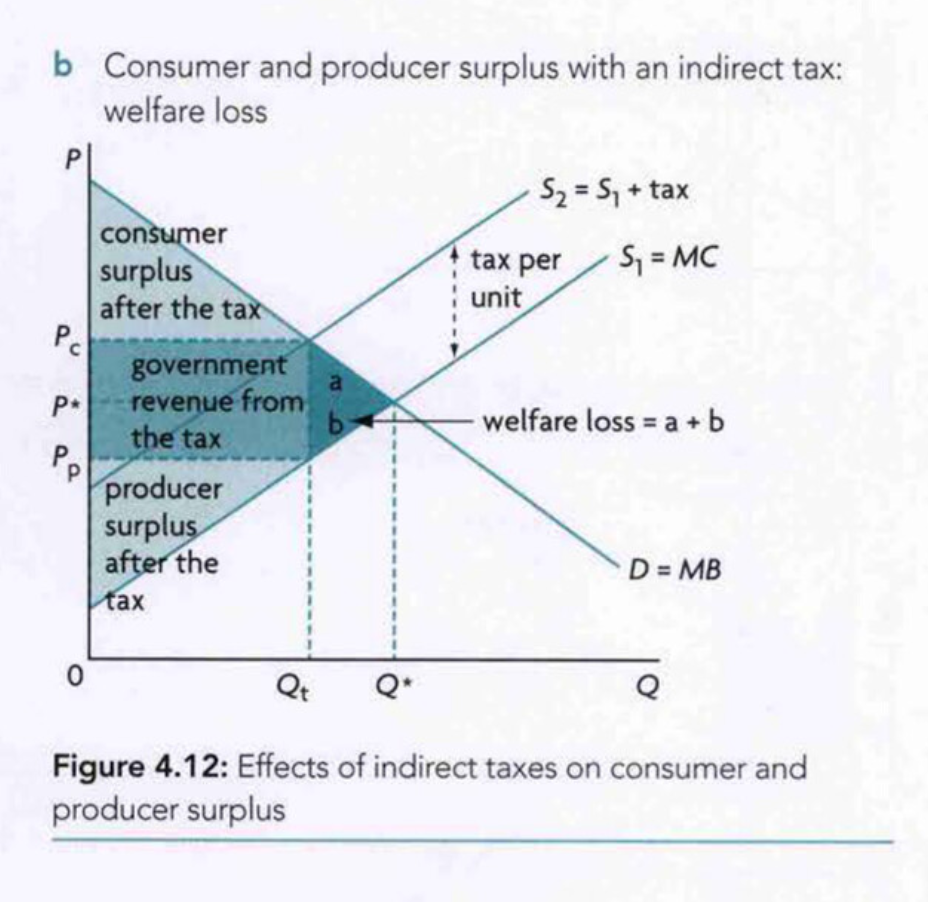

* Tax burden

* shared by consumers and producers

* Producer rev = Pp x Qsb

* Consumer surplus gained bcs of lower price

* Calculating

* just add on the surplus

* Producer: ((Pp - S1 int) x Qsb)/2

* Consumer: ((D int-Pc) x qsb)/2

* Foreign producers cannot compete with lower price

\

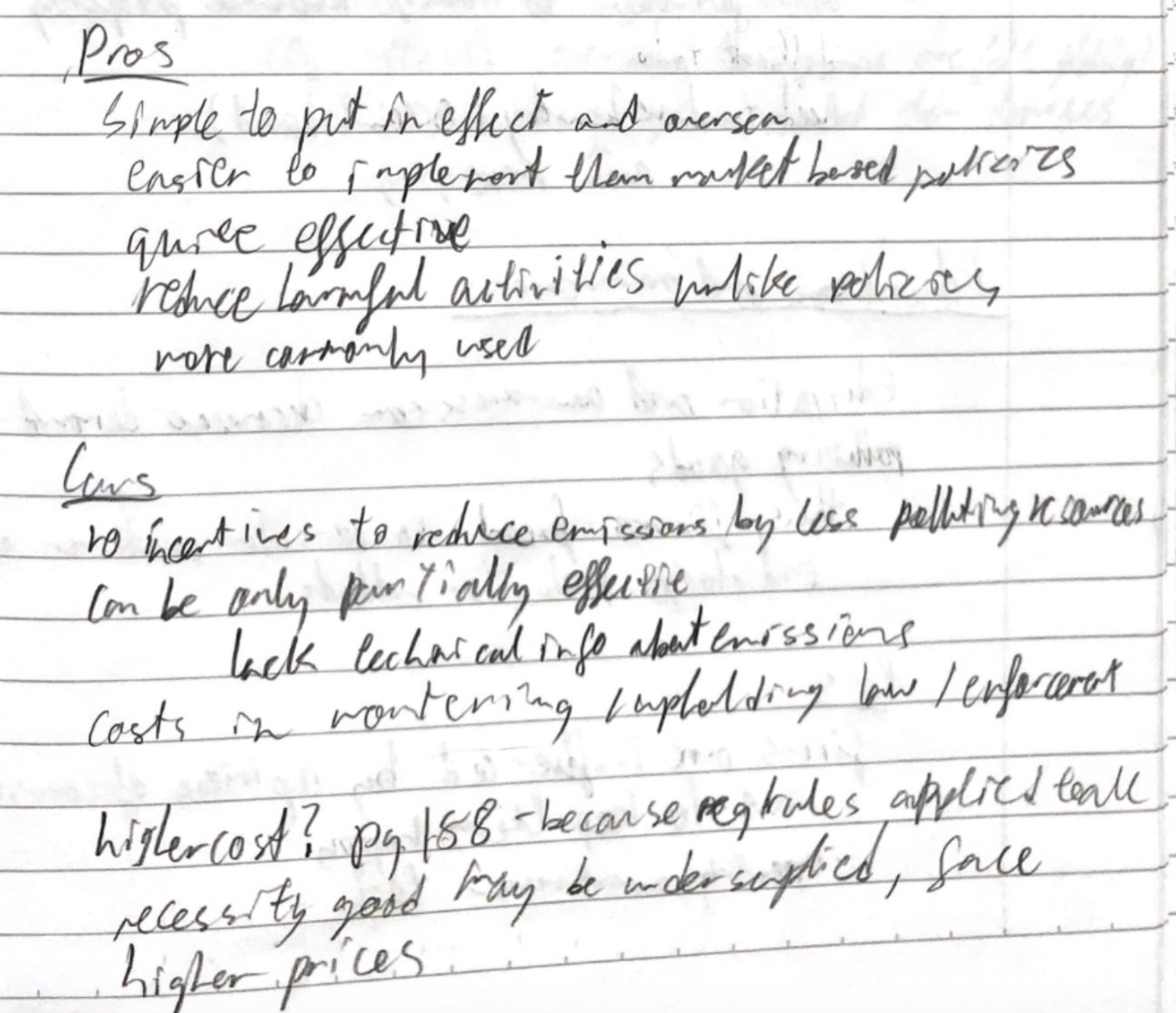

* No incentive to improve quality beyond standard

* Not applicable for all firms

* smaller firms cannot handle

* Large firms can lobby

* Sacrifice quality/effectiveness

* Not the most efficient in reducing environemental impacts

* Taxes better

* solutions to problems are well-known

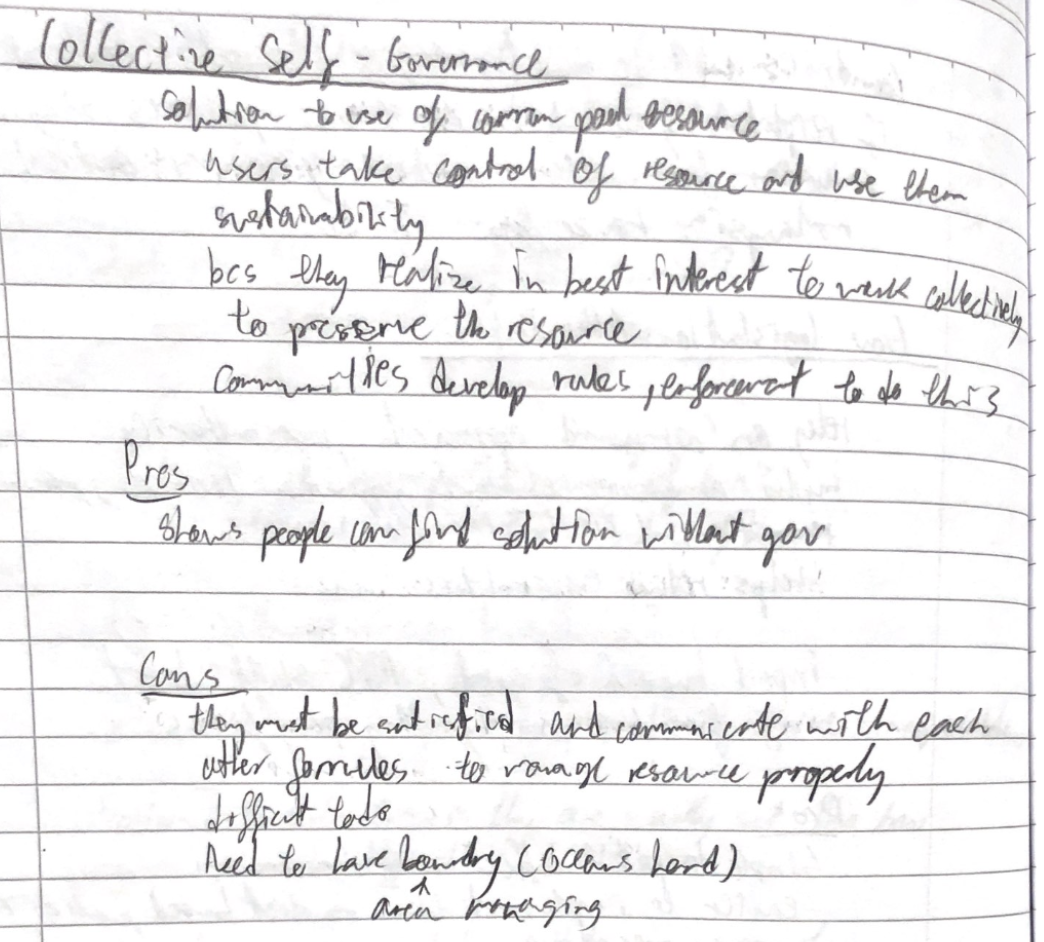

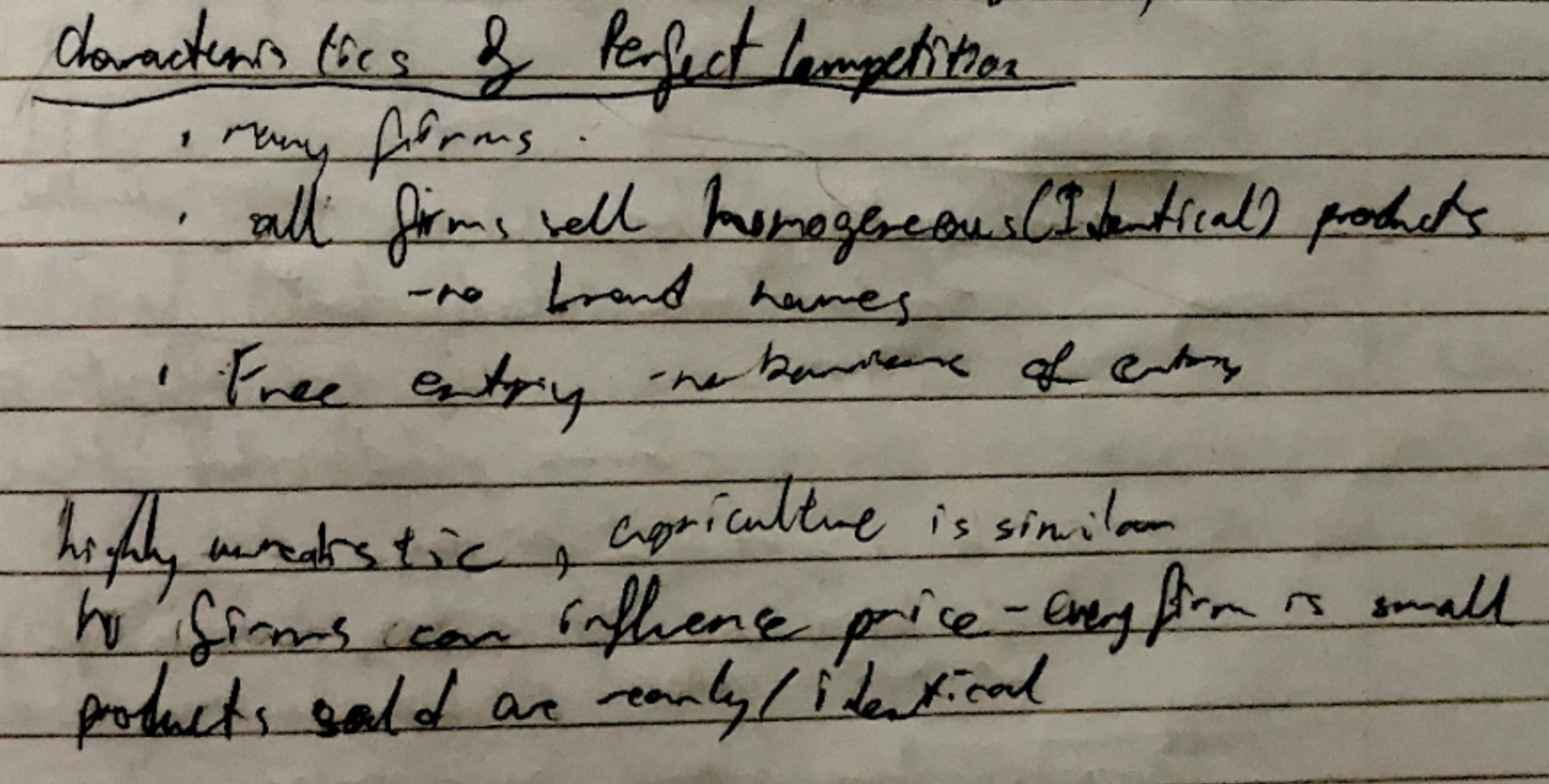

Perfect comp Characteristics (HL)

Monopoly (HL)

Monopolistic competition (HL)

Oligopoly (HL)

homo or hetero

Competition and market power (HL)

Theory of firm (HL)

Firms acts in interest of maximizing profits

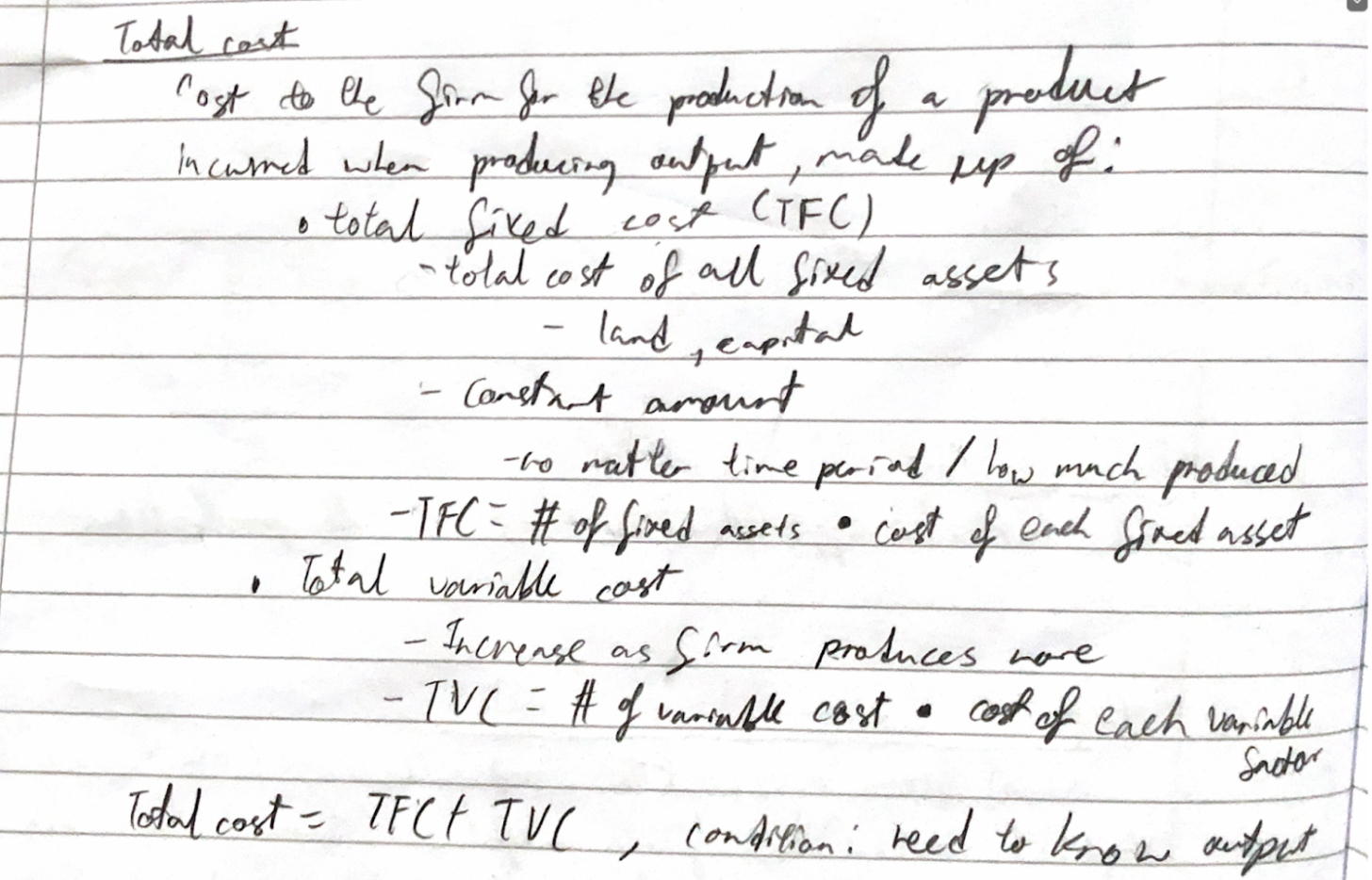

Calculating costs of firms (HL)

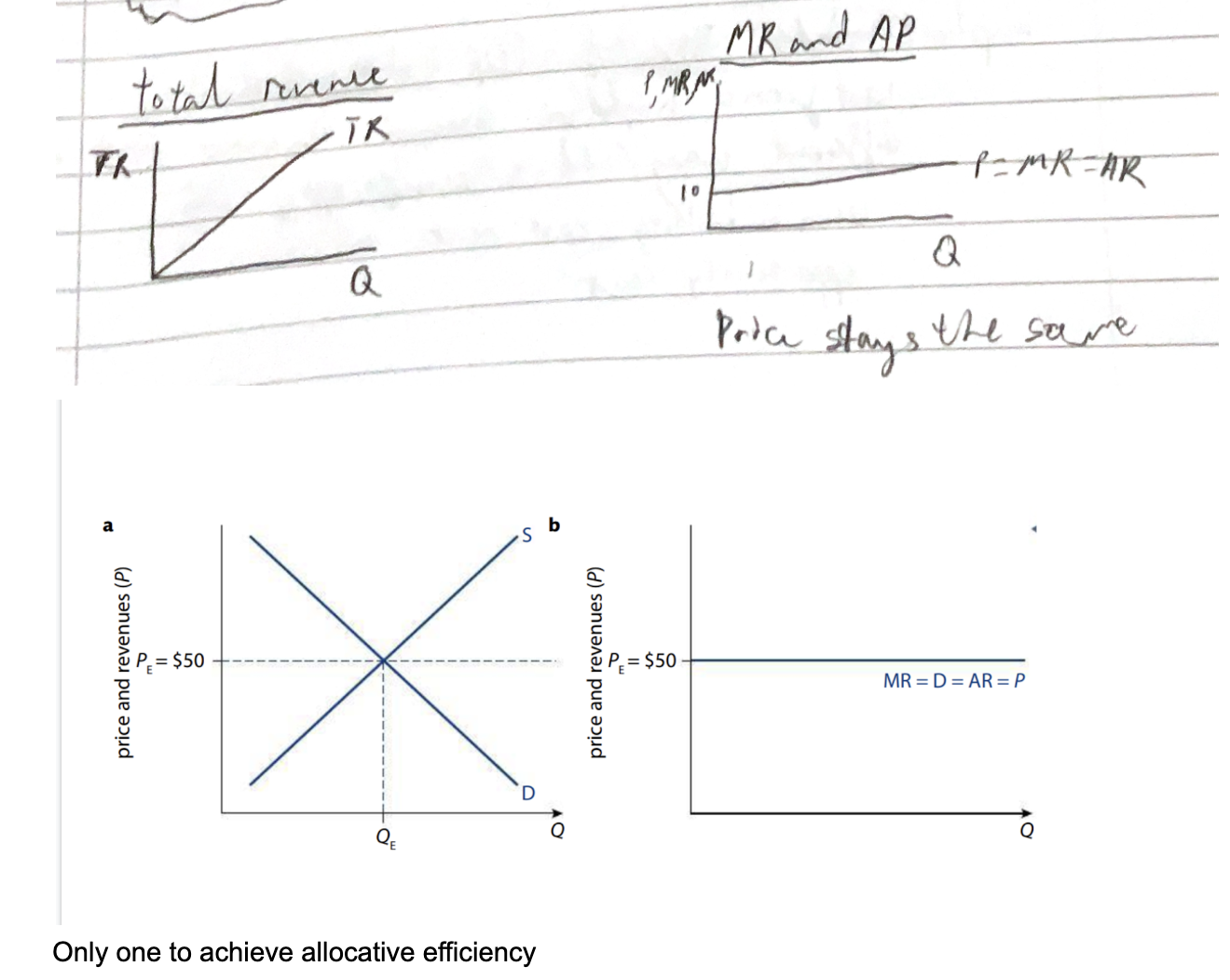

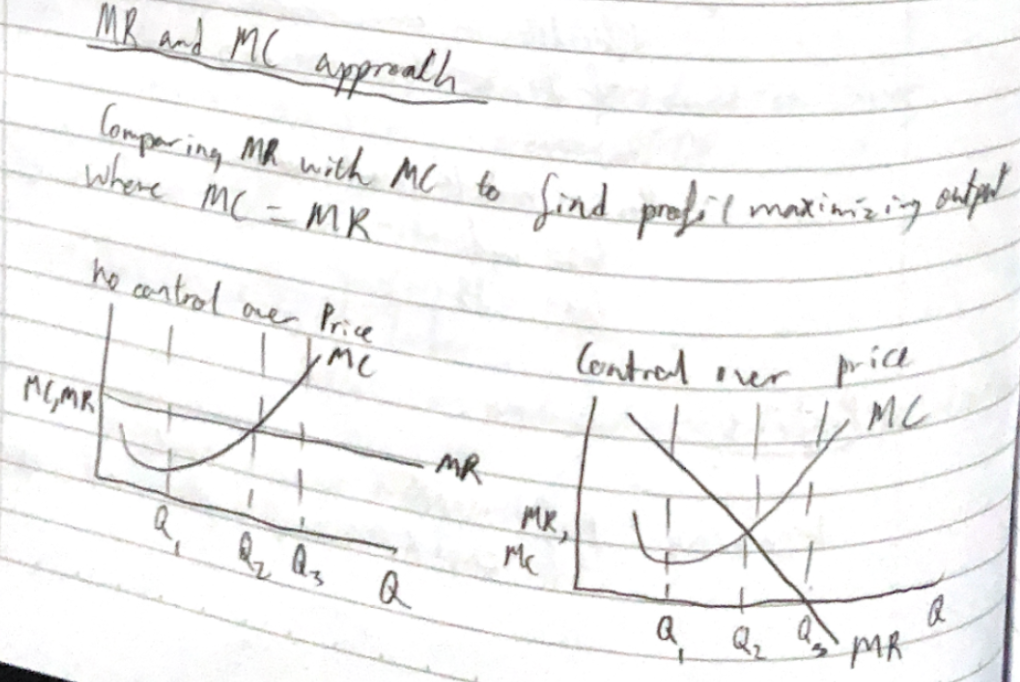

Perfect competition price and revenue graph (HL)

No influence on price

So must accept the market

Non-Perfect competitiion revenue graph (HL)

MR. DARP

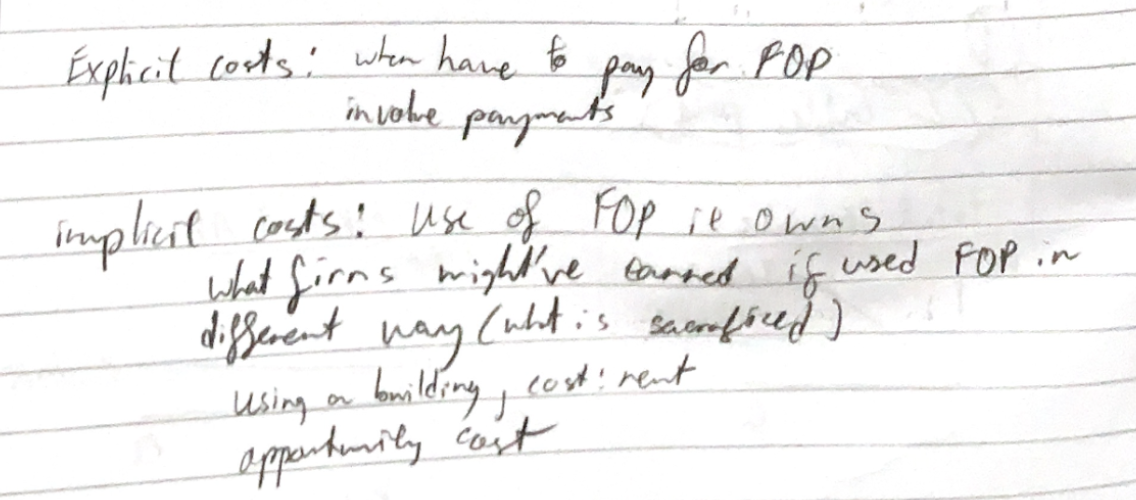

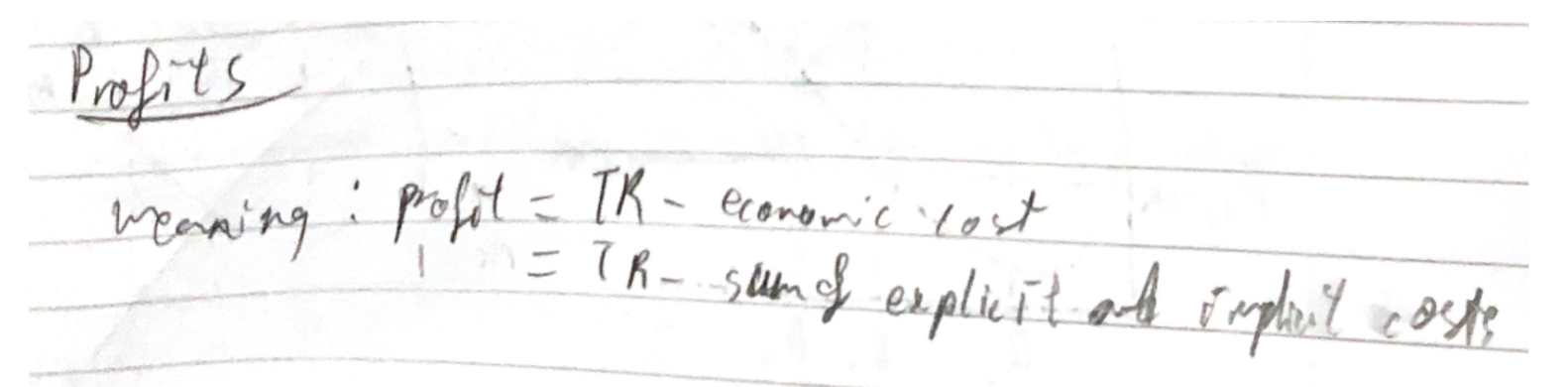

explicit vs implicit costs (HL)

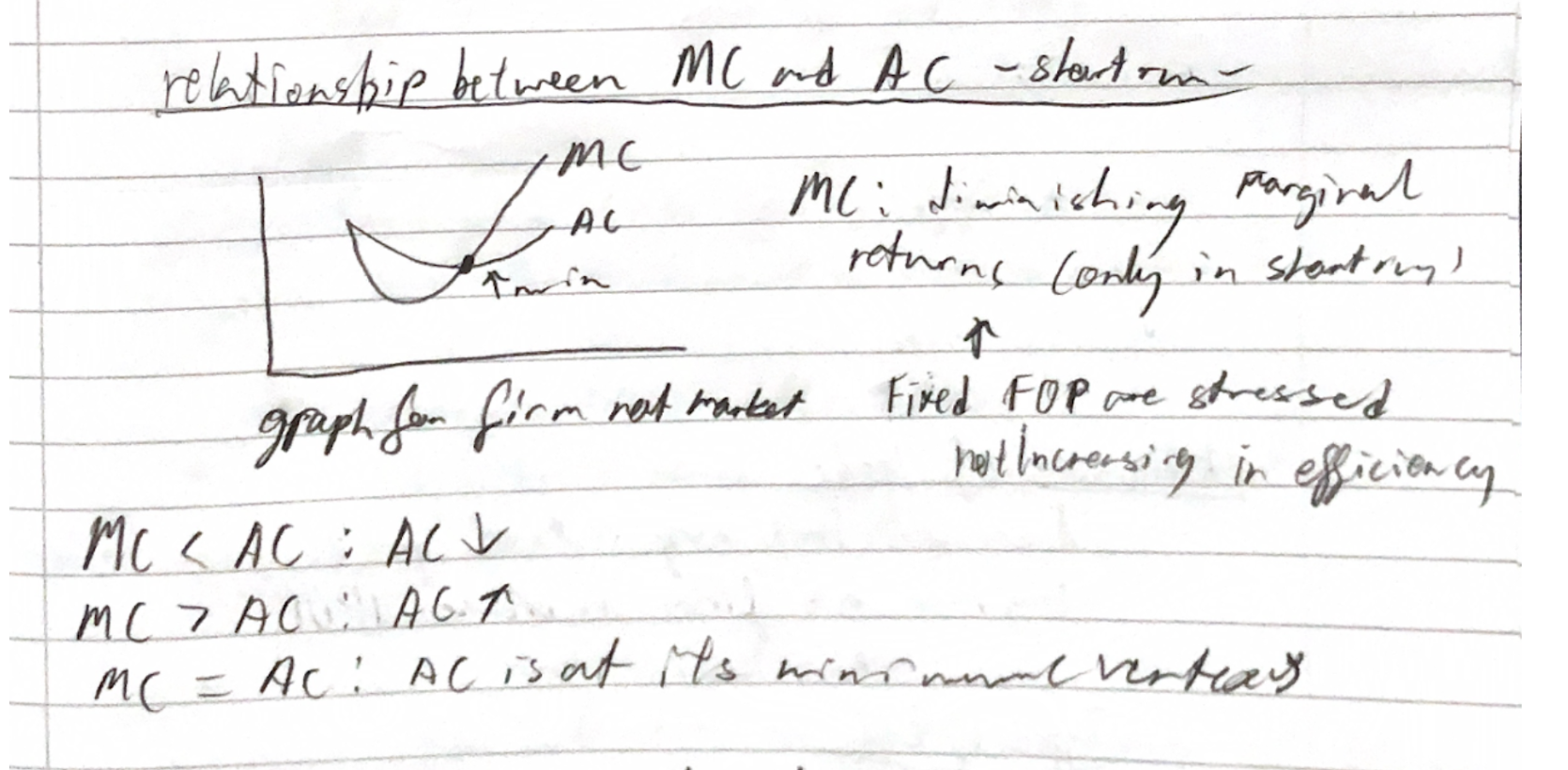

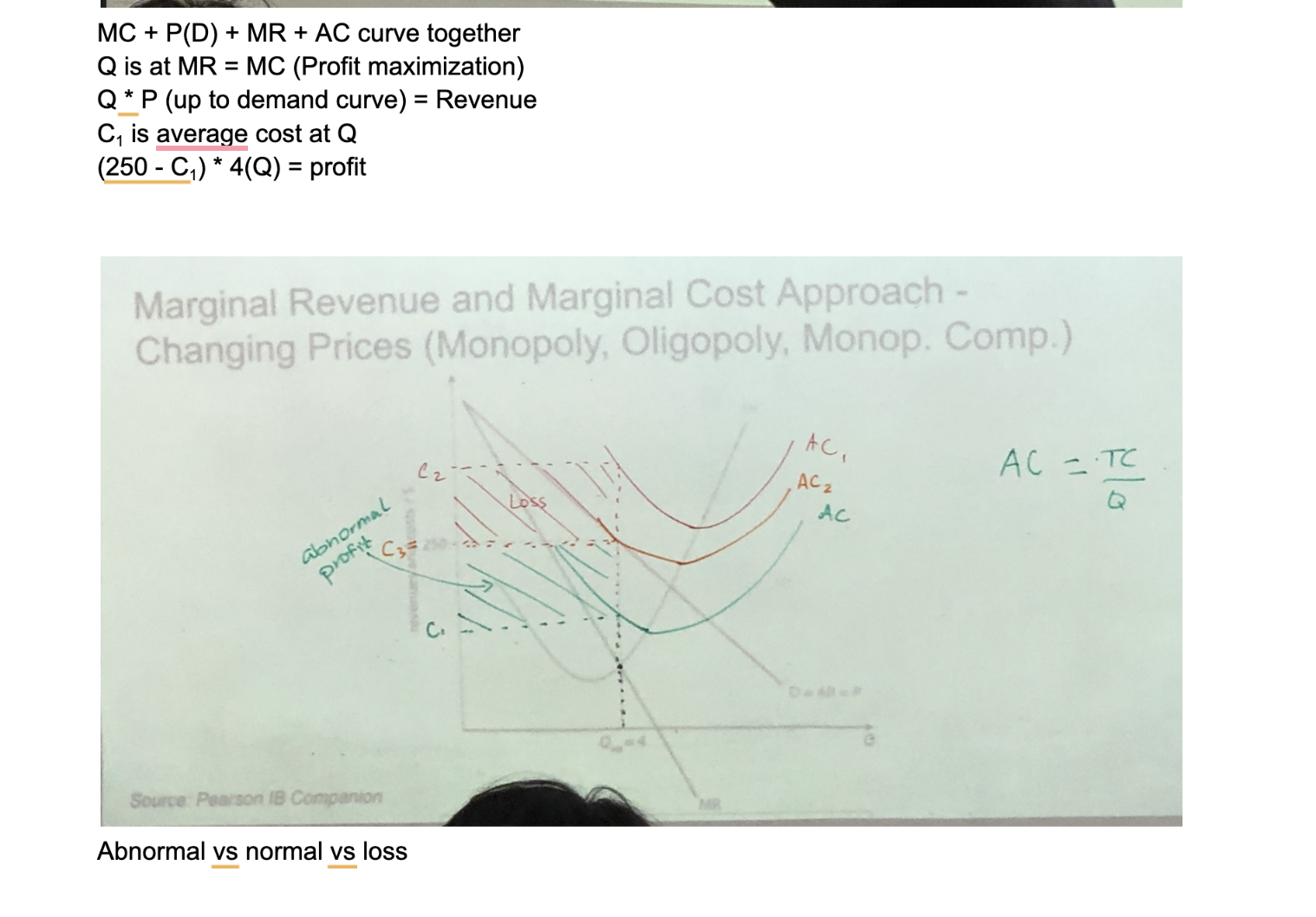

MC vs AC (HL)

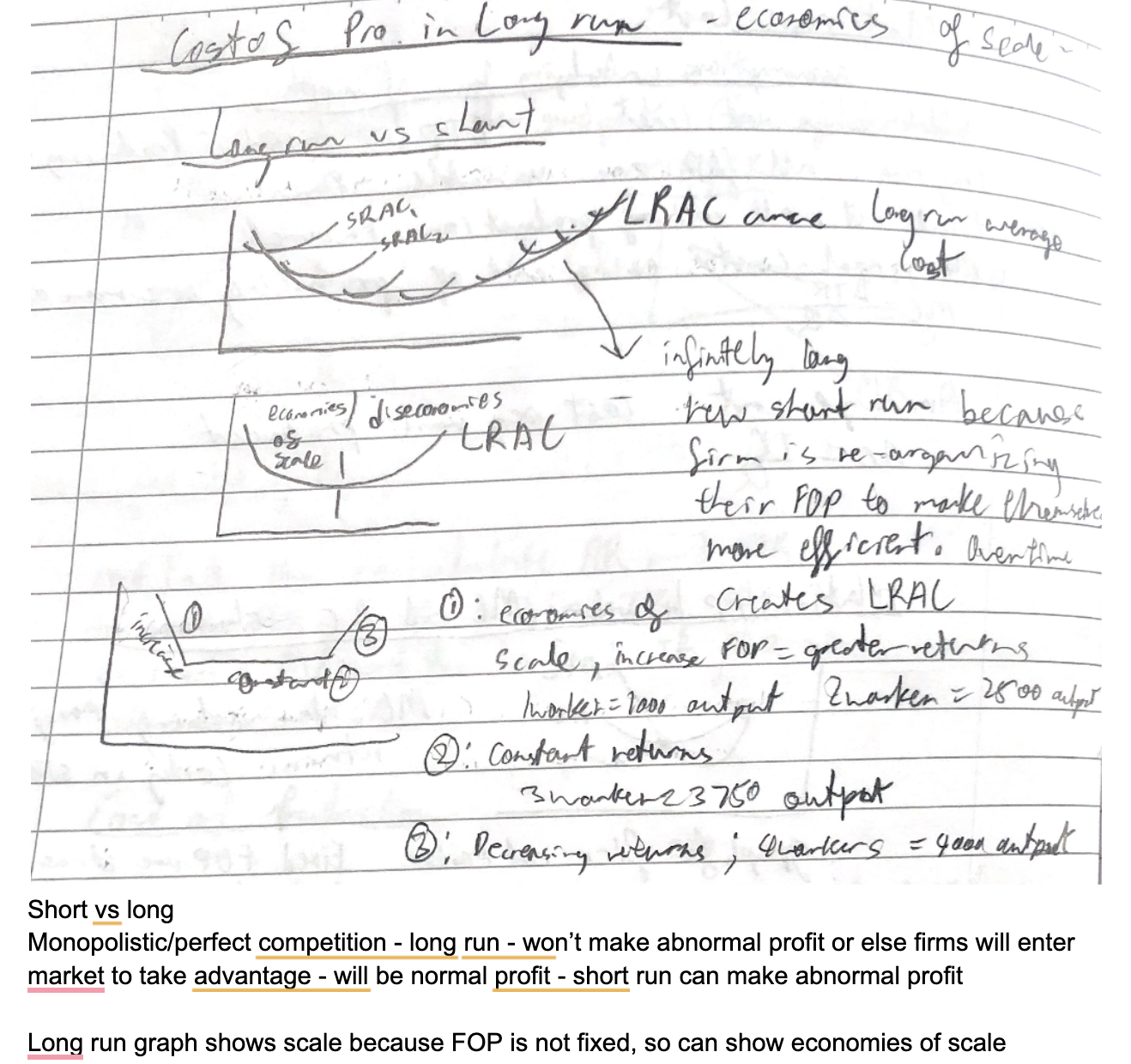

Long run AC curve - short vs long (HL)

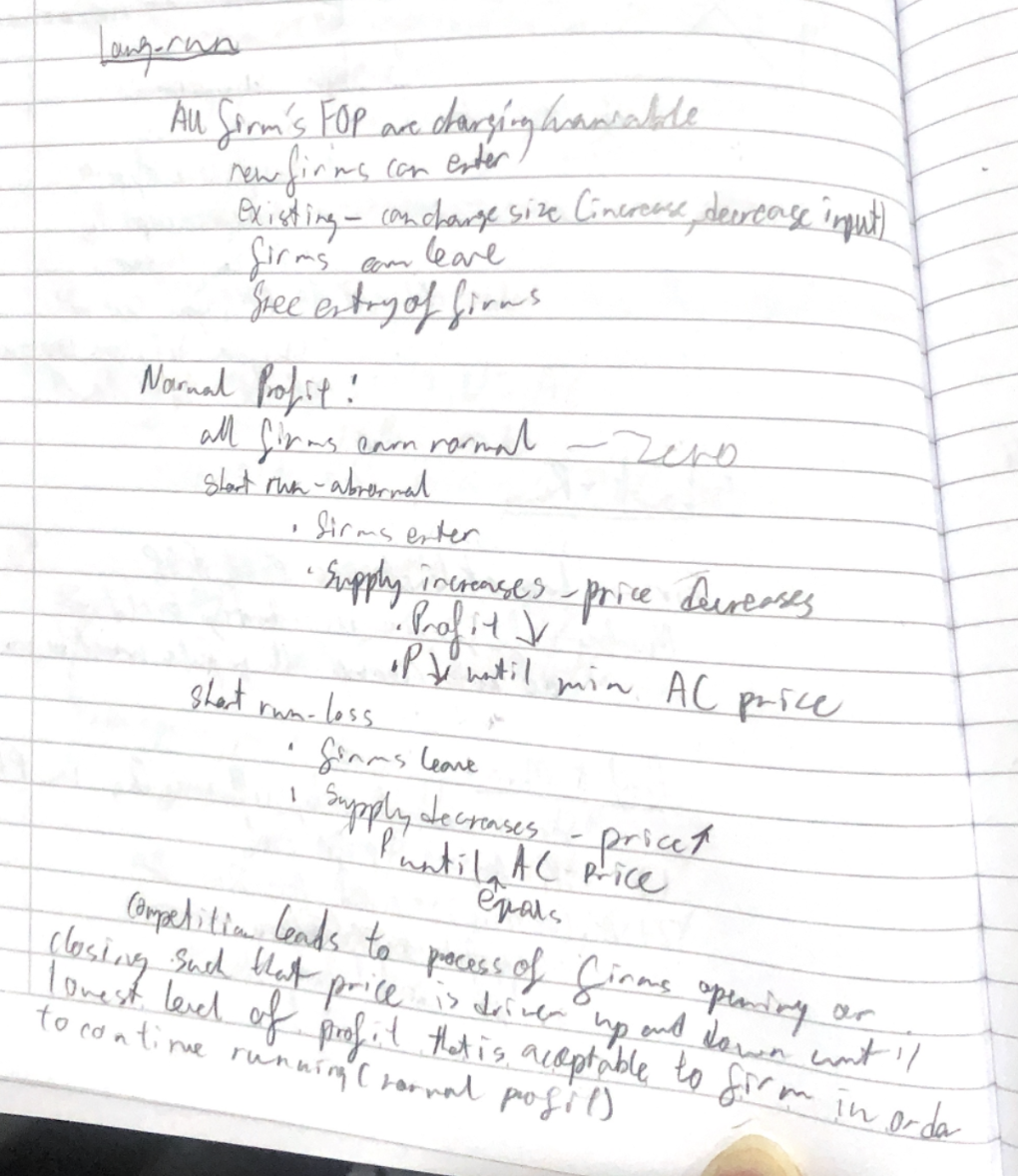

Long run = normal profit in PC and MPC

Economies of scale (HL)

the property whereby long-run average total cost falls as the quantity of output increases / FOP increases

Profit (HL)

Short run only can have abnormal profit in Mon Comp and Perfect comp

Profit max output (HL)

For non-perfect, need to go up to D

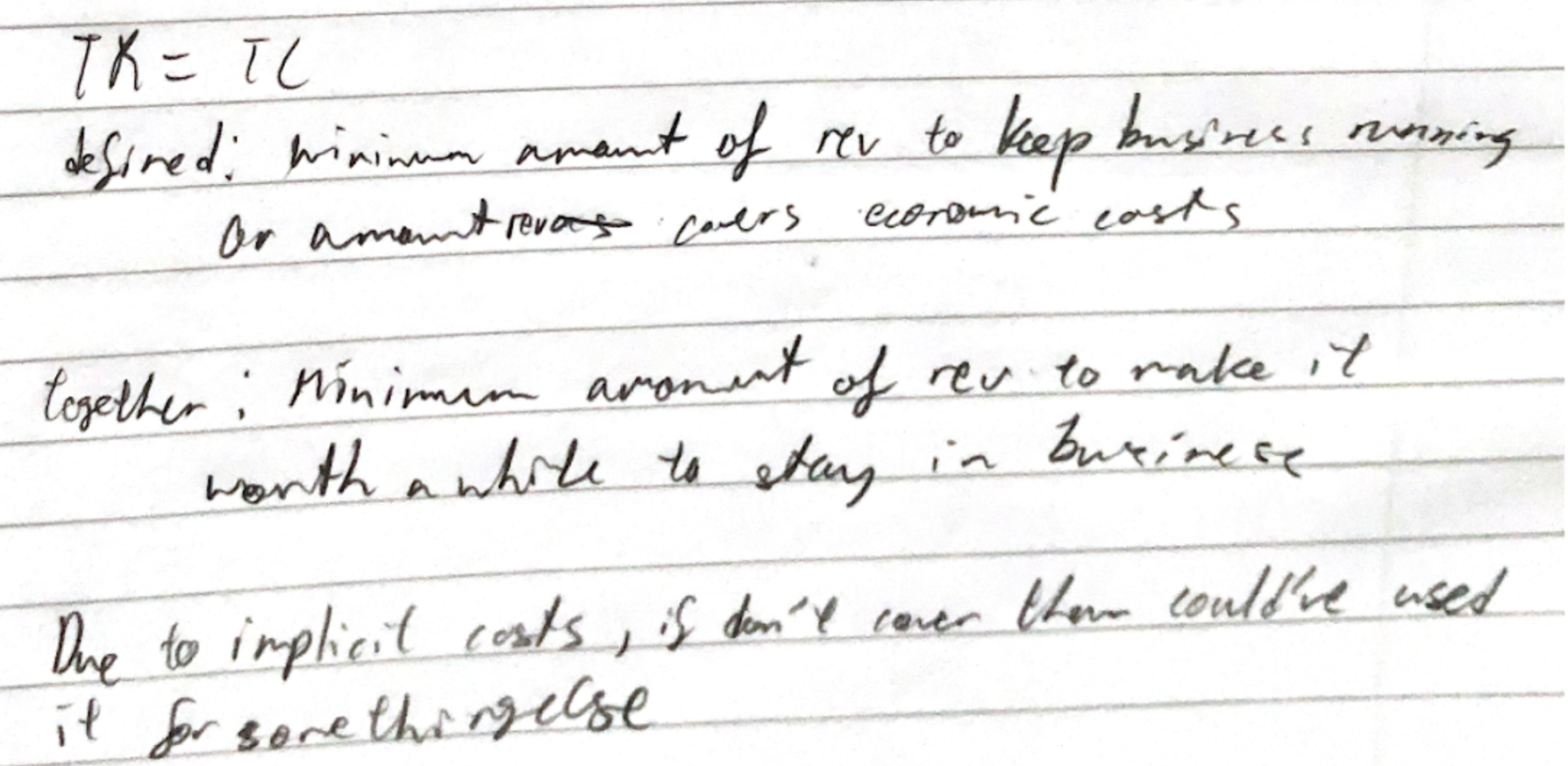

Normal profit meaning (HL)

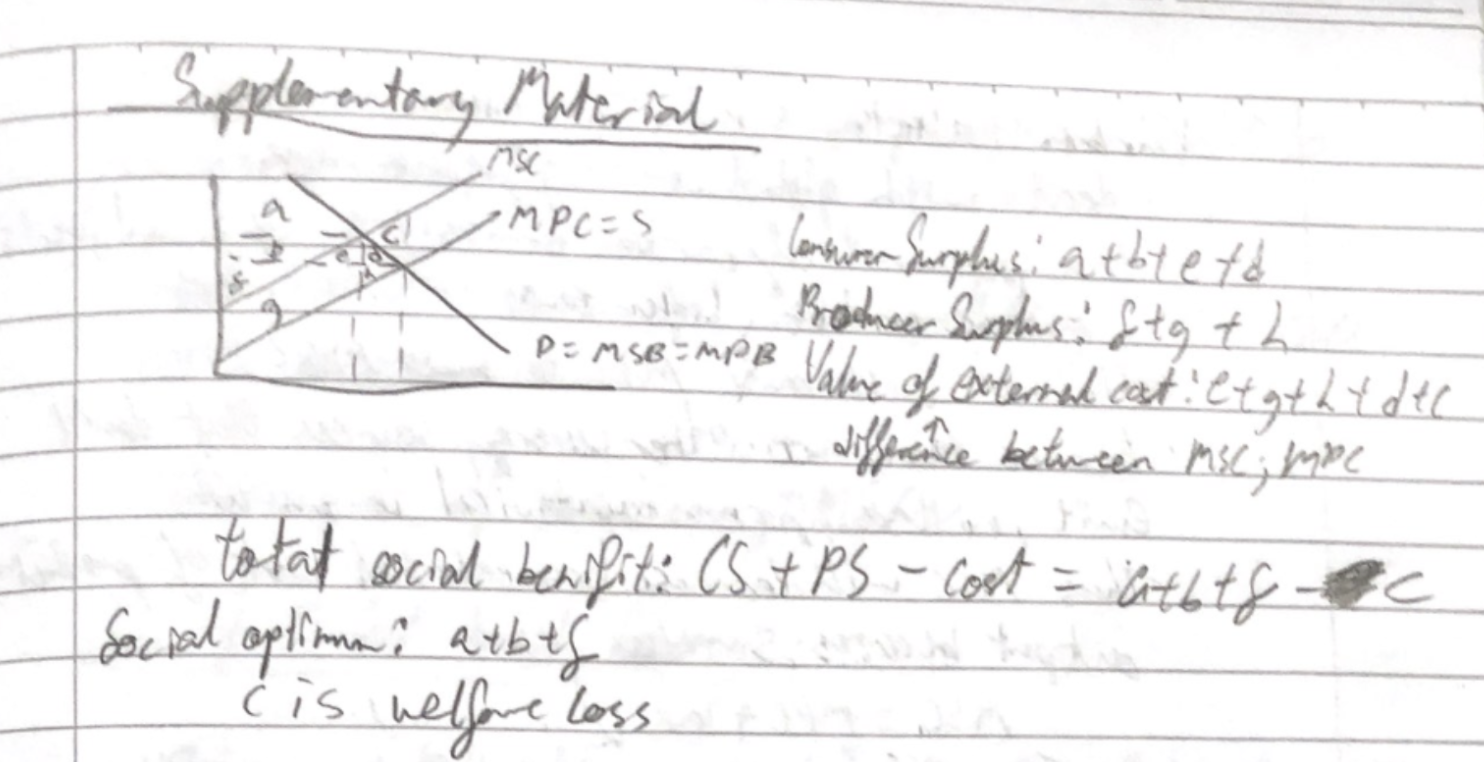

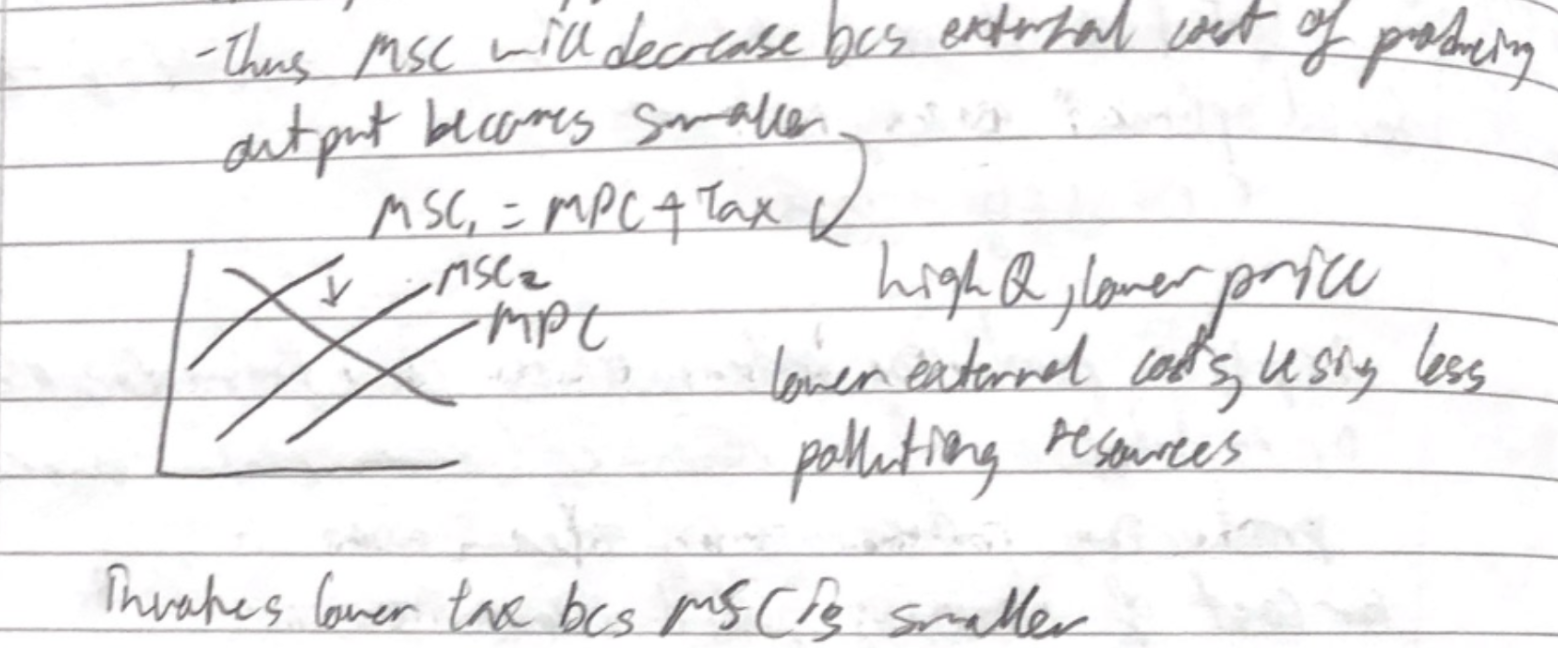

* It is a loss of social benefits due to overproduction of the good caused by the externality.

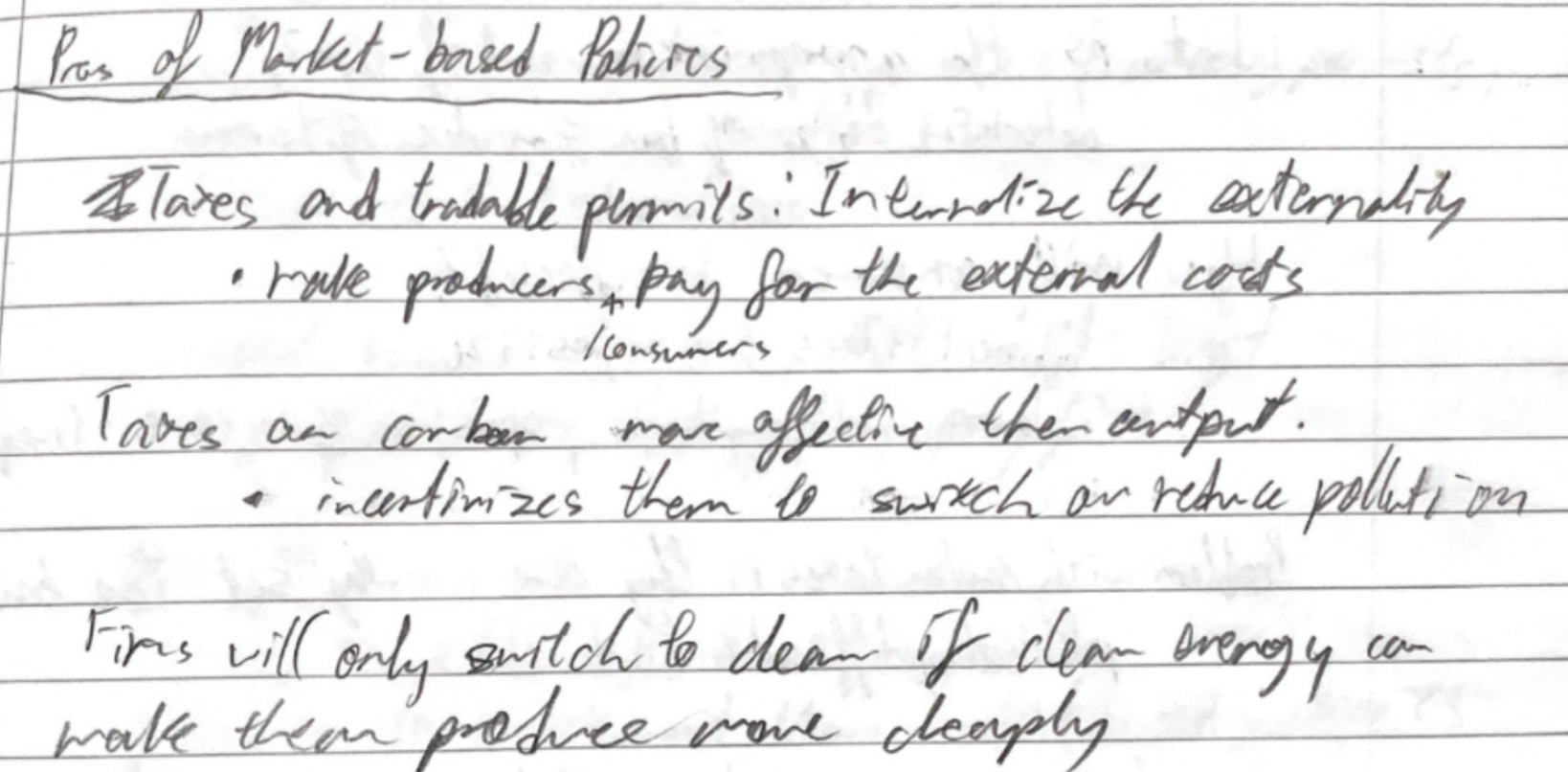

* Carbon taxes

* Taxes on emissions

* Firms are incentivized to switch to greener sources

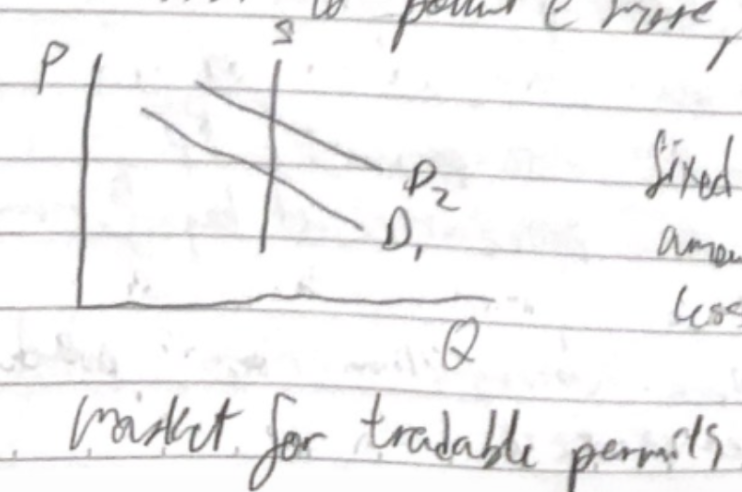

* Tradable permits

* Permits to pollute issued to firms

* over particular time period

* Traded in market

* Firms can sell the permits unused

* Incentivizes to switch

* MSC decrease

* need to determine cap

* cap too high, no effect

* too low, hardships for firms

* How to distribute fairly

* Big firms won’t feel cost of permits

* requires strong gov to uphold

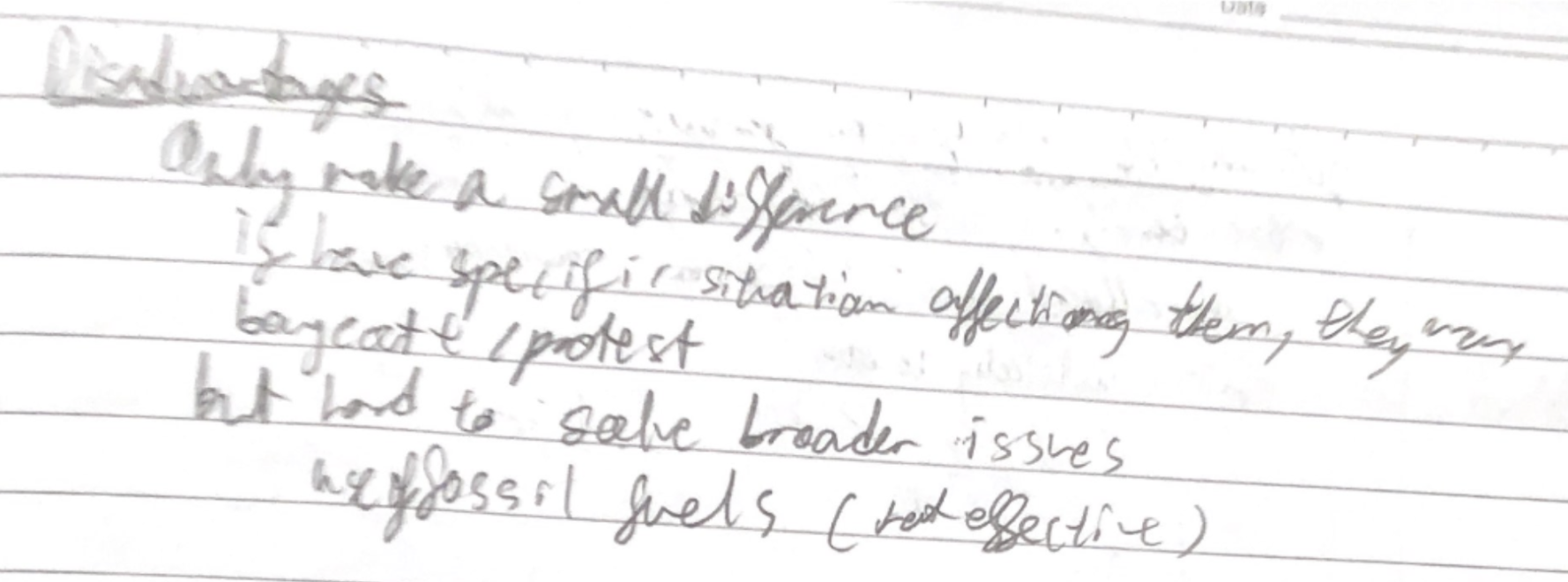

* Taxes

* politically difficult

* How will it affect consumers

* low income cannot pay a higher price

* Large firms can just pay tax

* Identifying which pollutant is harmful and how to value the harm

* Countries

* Disadvantaging themselves against other countries

* Output will decrease

* If other country doesn’t use

* Malaysian haze, indo