Topic 3 - Mundell's 2 country model / interdependence

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

Why do we care about interdependence

We are motivated by spillover effects of a shock in 1 country on another

e.g. financial crisis

Assumptions of Interdependence model

2 symmetric countries → H & F

Perfect Capital mobility → UIP holds

Adoptive expectations → expected change in ER = 0

makes model static

Fixed prices → S & Q move together

Marshall-Lerner condition is satisfied

Real depreciation → rise in NX

Output determined by Demand

Channels of interdependence

Marginal propensity to import (MPI)

AD changes affecting trading partner

AD UP leads to increased imports and higher NX in F

Interest rates (i)

i change may affect i*

Exchange rate (when flexible)

If p fixed, then a change to nom ER (S) will affect relative p and lead to expenditure switching

If S increases -> depreciation -> dom good relatively cheaper -> dom output may increase

H output equation - Flexible ER

H Money Market equation - Flexible ER

M = MS

RHS - MD (as a function of i & y)

no P as Fixed P so we say p=0

M is a level so not log transformed

UIP with adoptive expectations

i = i*

what is the term u

Captures FP or government spending

What relationship do i & y have

if real i increases then I falls -> AD falls -> output falls

- Negative relationship of i & y

What relationship do s & y have

s increases (nom depreciation) -> q changes -> relative p changes -> NX increase -> y increase

If ML condition holds which we assume

- Positive relationship between s & y

Exogenous variables - Flexible ER

M & u

Used for FP & MP + shocks

Relationship between y & y*

MPI drives y* effect

y* increase -> higher D for imports → H exports increase -> NX increase → y increase

- Positive relationship between y & y*

Relationship between u & y

u increases -> AD increases -> y increases

- Positive relationship between y & u

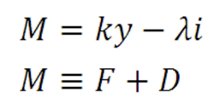

M & CB balance sheet

M = D + F

D - CB holding of govt bonds

F - Foreign exchange reserves

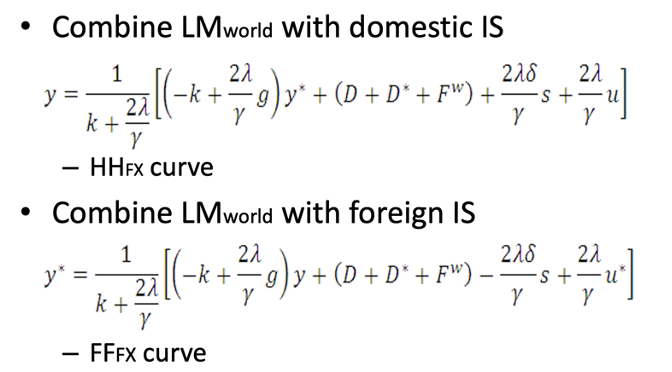

F output & money market equation - Flex ER

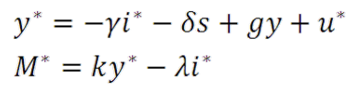

Conversion into y, y* space - Combine IS

Incorporate i = i*

Sum IS + IS* = ISW

Conversion into y, y* space - Combine IS & LM

Combine ISW with LM curves

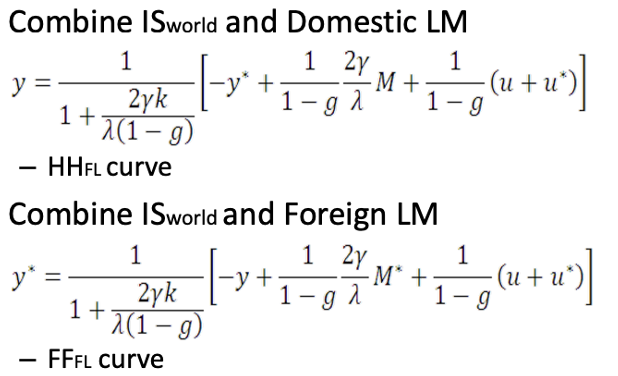

If FFFL slope < 1 - diagram

g

MPI

<1 as only part of the increase falls in increased imports

Therefore slope in HHFL < 1 in absolute terms

As denominator > 1

Why is HHFL & FFFL equilibrium on 45o

countries identical / symmetrical initially

HHFL slope vs FF

Inverse

-0.5 = -2

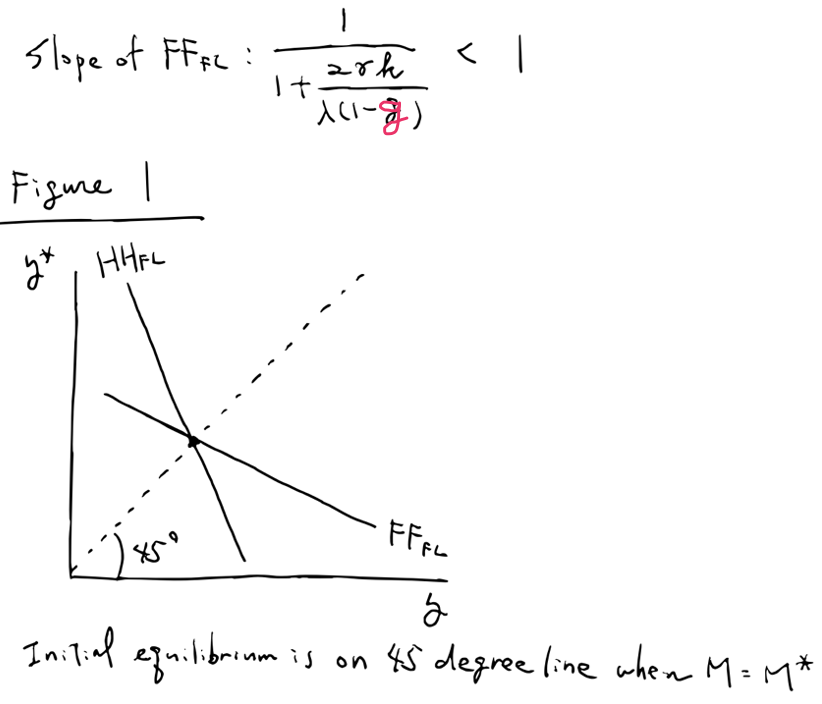

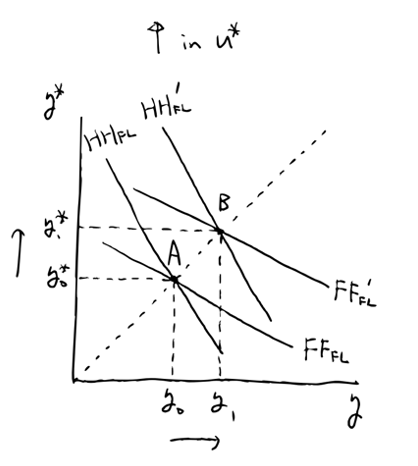

Negative shock in Foreign Money supply - graph

- M* only part of intercept term in FFFL not the slope -> shifts curve

- not in HHFL at all -> no shift

Positive shock in foreign FP or GS

u*

- in both FFFL & HHFL intercept term -> shifts both curves

- stays on 45o line (increase in y = increase in y*)

Breakdown of channels from u* increase

MPI - expansionary

u* increase → ADF increase → D for imports increase → XH increase

y* increase = y increase

Relatively small impact as g < 1

Interest rate - Contractionary

M exogenous so fixed

To balance money market equilibrium as y* rises, i* must rise too

i = i* because of UIP (nom & real i rise as inflation rate = 0 from fixed prices)

i increase → I decrease → y decrease

Exchange rate channel - Expansionary

i has fallen + g < 1

To keep equilibrium s needs to rise to match fall in i

s rises → depreciation

As p is fixed, real ER falls as well (nom = real depreciation)

NX rises from ML condition → AD rises

Fixed ER - CB intervention

CB needs to intervene to correct currency if there is a shock

- Using F reserves

Ms becomes endogenous

Home / F output equation - Fixed ER

Money market equation - H - Fixed ER

Variables with * for F version

M becomes endogenous under fixed ER

Are F reserves endogenous under fixed ER

Yes

Add together to get World reserves

F + F* = FW

Conversion into y, y* space - fixed ER

incorporate i = i*

Sum LM + LM* = LMW

Combine LMW with Dom & F IS

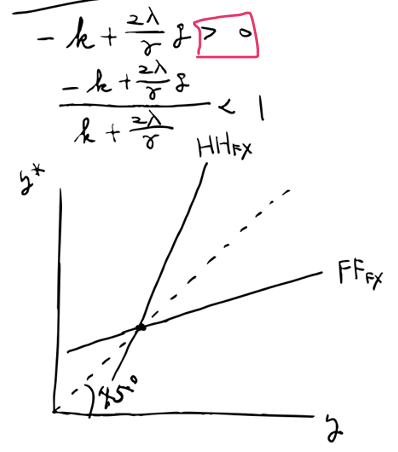

Graph if FFFX slope > 0

g<1 so slope<1 → crosses 45o

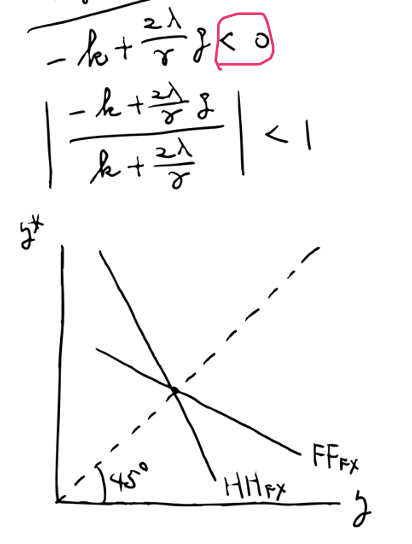

HHFX is inverse and symmetrical

equilibrium at 45o

Graph if FFFX slope < 0

-k > RHS

absolute value still < 1

FFFX still flatter than 45o

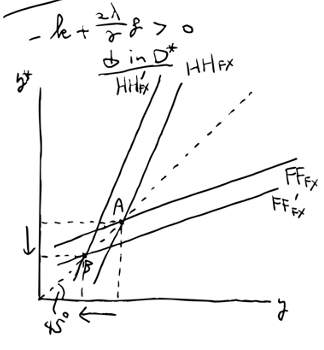

Negative shock to Foreign Govt bonds - Fixed ER - slope > 0

D* down = decrease in OMOs in F

- affects both HH & FF so both shift

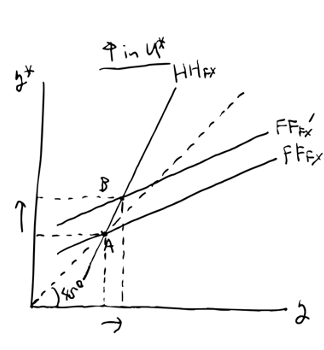

Positive shock to Foreign FP or GS - Fixed ER - slope > 0

U* change

- Only affects FF

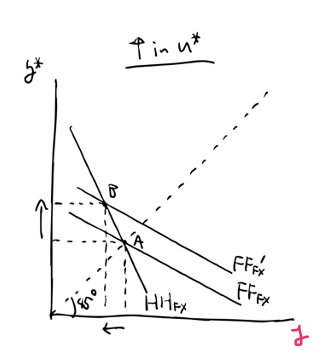

Positive shock to Foreign FP or GS - Fixed ER - slope < 0

u* change only affects FF

- However, it has flipped the sign on effect on y

Negative shock to Foreign Govt bonds - Fixed ER - slope < 0

D* change affects both HH & FF

y* falls → y fall from MPI (contractionary effect)

no ER effect as fixed ER

y* falls → g < 1 so not full effect → i rises to correct → y falls (contractionary effect)

Effects of larger g

g - MPI

larger g means greater impact on domestic output for any F shock

as g increases → higher chance of positive impact of F positive shock