Ch 10: Depreciation, Impairments and Depletion

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

36 Terms

depreciation

cost allocation of an asset and not to valuation of an asset

- the process of allocating the cost of tangible assets to expense in a systematic and rational manner to those periods expected to benefit from the use of the asset

- cost allocation of PPE. Land is not depreciated but land improvements are

Allocating costs of long-lived assets:

• Fixed assets = Depreciation expense

• Intangibles = Amortization expense

• Natural resources = Depletion expense

Book Value/Carrying Value

shows how much of the tangible asset's cost is left to be depreciated or expensed

- companies report BV on their BS and notes to the financial statements

- BV is used in the calculation of gains and losses on disposal of the equipment, as well as in some depreciation calculations

Depletion

Cost allocation of natural resources (timber, gravel, oil, coal)

-- allocating the cost of natural resources over the period they are consumed

Amortization

Cost allocation of intangible assets (patents and copyrights)

Factors Involved in Depreciation Process

1. What depreciable base is to be used for the asset?

2. What is the asset's useful life?

3. What method of cost apportionment is best for this asset?

Depreciable Base for the Asset

1. Original cost of the asset: The determination of original, or historical cost

2. Salvage Value (disposal value): The estimated amount that a company will receive when it sells the asset or removes it from service. The SV is not depreciated because the company expects to receive that amount when the asset is later sold or scrapped. It is the amount to which a company writes down or depreciated the asset during its useful life.

Estimation of Service Life

- the service, or useful, life of an asset often differs from its physical life. A piece of machinery may be physically capable of producing a given product for many years beyond its service life.

- retire assets: Physical factors: (casualty/expiration of physical life) or Economic factors: (obsolescence)

Methods of Depreciation

1. Activity Method (units of use or production)

2. Straight line method

3. Decreasing charge methods (accelerated)

a. Sum of the years digits

b. declining balance method

Activity Method

- aka variable charge or units of production approach

- assumes that depreciation is a function of use or productivity, instead of the passage of time

- more depreciation should be recognized the more the asset is used

- a company considers the life of the asset in terms of either:

--- an output measure, such produced from equipment or miles driven on a vehicle =

--- an input measure, such as the number of hours a machine works

Straight-line Method

- considers depreciation as a function of time rather than a function of usage

- simple

- when obsolescence is the primary reason for a limited useful life, the decline in usefulness may be constant from period to period

- results in the same amount of depreciation exp recognized each year

- major objection to SLM is that it rests on two assumptions:

1. the assets economic usefulness is the same each year. In reality the asset may not be utilized the same each year

2. the maintenance and repaid expense is essentially the same each period. In reality, as the asset gets older, it will probably have more down time as it will need more repairs to maintain operating utility

Decreasing Charge Methods

- provides for a higher depreciation expense in the earlier years and lower expense in later years

- bc these methods allow for higher early year expenses that in the SLM, they are often called accelerated depreciation methods

- main justification for this approach

--- companies should recognize more depreciation in earlier years bc the asset is most productive in its earlier years

--- accelerated methods likely provide a constant total cost bc the depreciation expense is lower in the later periods, at the time when the repair and maintenance costs are often higher

- Two decreasing charge methods:

1. sum of the years digits

2. declining balance method

Sum of the Years' digits

- results in a decreasing depreciation expense based on a decreasing fraction of the depreciable base (original cost-salvage value).

- Each fraction uses the sum of the years as a denominator

- at the end of the assets useful life, the balance remaining should equal the salvage value

- declining rate of depreciation (depreciation fraction) multiplied by the constant depreciable base

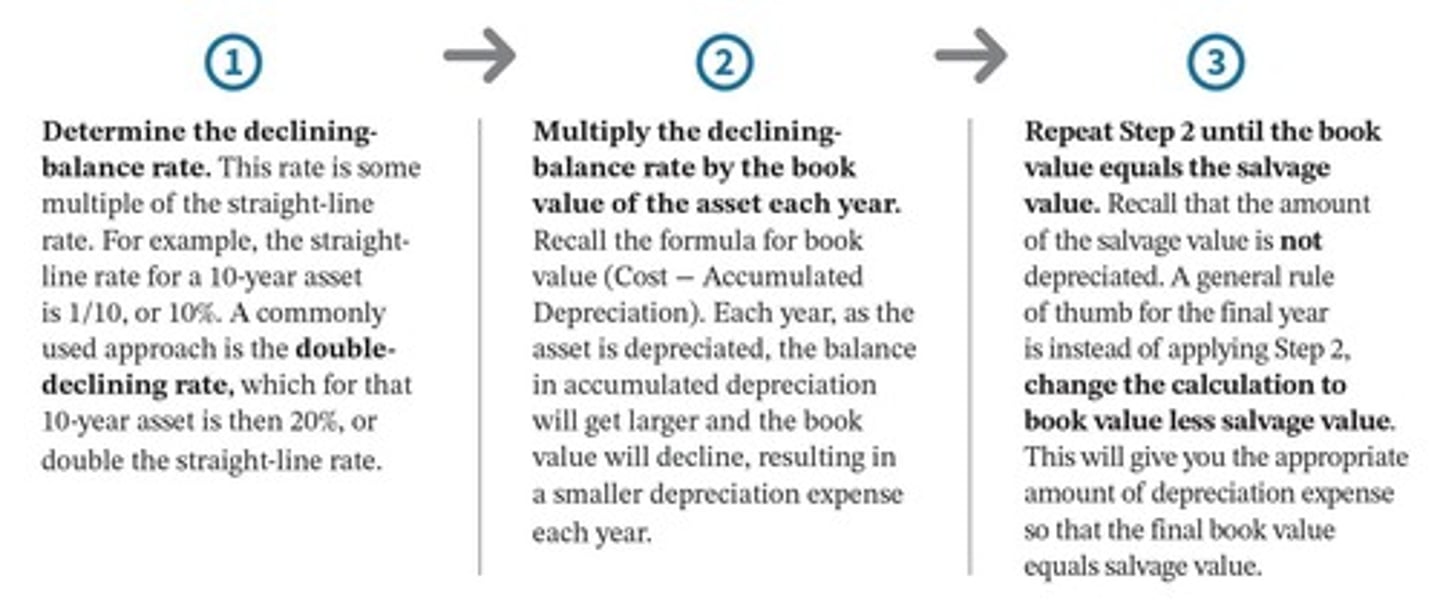

Declining Balance Method

- determines depreciation expense by applying a constant percentage to the declining book value of the asset each year. This method does not deduct the salvage value in computing depreciation expense

- rate of depreciation is the same but is multiplied by a declining depreciation base

Depreciation and Replacement of PPE

- depreciation, like other expenses, reduces net income

- depreciation in no way provides funds for the replacement of assets

- the funds for the replacement of the assets come from the revenues generated through use of the asset

Revision of Depreciation Rates

- companies may need to revise their estimate during the life of an asset

- unexpected physical deterioration or unforeseen obsolescence may decrease the estimated useful life

- improved maintenance procedures, revision of operating procedures, or similar developments may prolong the life of the asset beyond the expected period

- Revised Depreciation Expense= (Book Value- Revised Salvage Value)/Remaining Useful Life

Impairment

- the write off of all or part of the carrying value of a PPE

- examples of events that might lead to an impairment:

--- a significant decrease in the fair value of an asset

--- a significant change in the extent or manner in which the asset is used

--- a significant adverse change in legal factors or in the business climate

--- an accumulation of costs significantly in excess of the amount of the amount originally expected to acquire or construct an asset

--- a projection or forecast that demonstrates continuing losses associated with an asset

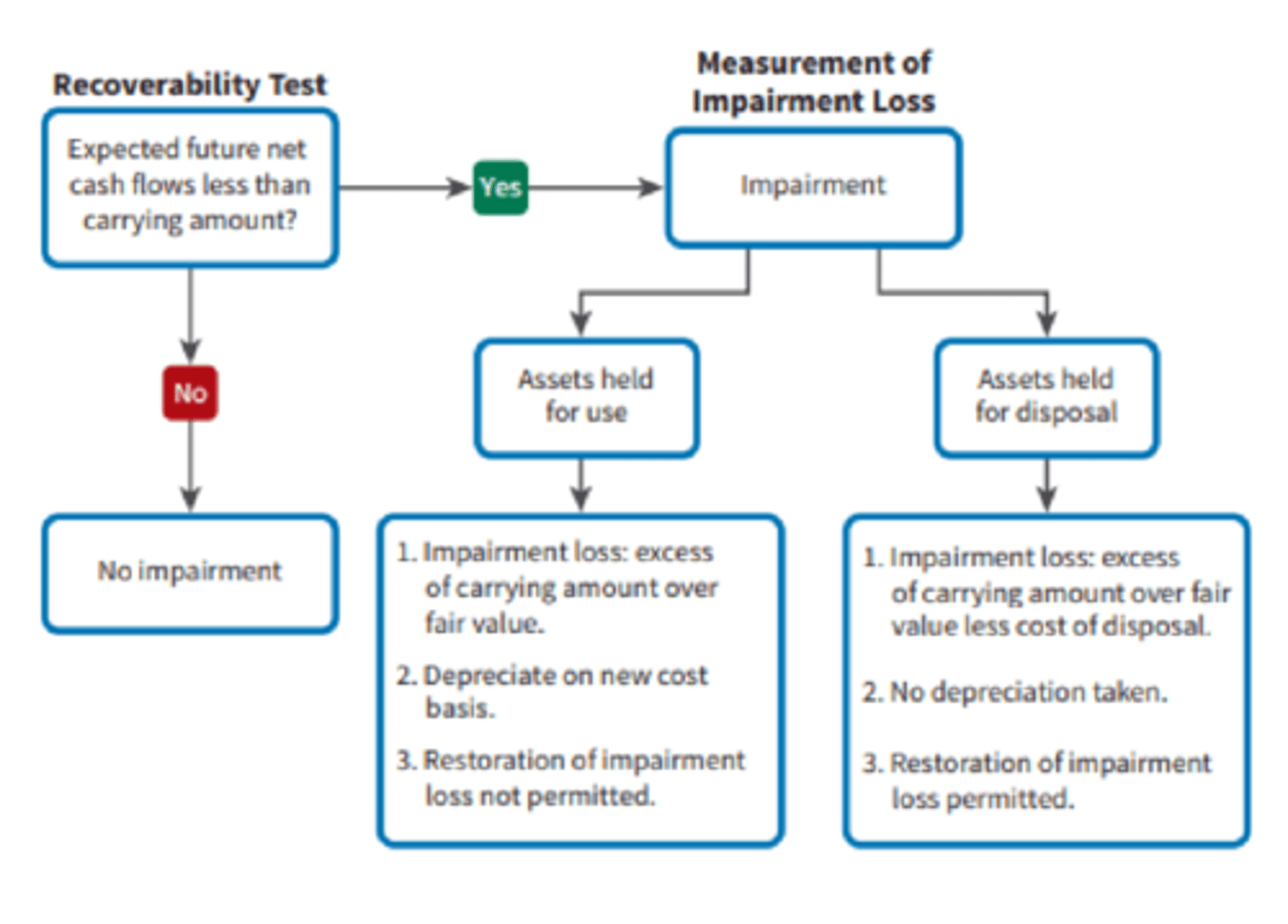

- recoverability test: determine whether an impairment has occurred.

--- a company estimates the future net cash flows expected from the use of that asset and its eventual disposition, and compares it to the carrying amount as follows

---- if the sum of expected future cash flows (undiscounted) is greater than the carrying value of the tangible asset, there is no impairment

---- if the sum of the expected future cash flows (undiscounted) is less than the carrying value of the tangible asset, there is an impairment loss

Measuring Impairments

- if the recoverability test indicates an impairment, a company computes a loss

- The impairment loss is the amount by which the carrying amount of the asset exceeds its fair value

- fair value is measured based on the market price if an active market for the asset exists. If no active market exists, a company uses the present value of expected future net cash flows to determine fair value

Restoration of Impairment Loss

- after recording an impairment loss, the reduced carrying amount of an asset held for use becomes its new cost basis. A company does not change the new cost basis except for depreciation in future periods or for additional impairments

Impairment of Assets to be Disposed of

- assets held for disposal are like inventory; companies should report them at the lower of cost or net realizable value

- bc the company will recover the carrying value of the assets held for disposal in future periods, as long as the carrying value after the write up never exceeds the carrying amount of the asset before the impairment. Companies should report losses or gains (recoveries) related to these impaired assets as part of income from continuing operations

accounting for impairments diagram

Natural Resources

wasting assets

- two main features:

1. the complete removal (consumption) of the asset

2. Replacement of the asset only by an act of nature

- consumed physically over the period of use and do not maintain their physical characteristics

Computation of the depletion base involves four factors:

1. Acquisition Cost

2. Exploration Costs

3. Development Costs

4. Restoration Costs

Acquisition Cost

- price paid to obtain the property rights to search and find an undiscovered natural resource

- can also be the price paid for an already discovered resource

- can also be the lease payments for property containing a productive natural resource

- included in these acquisition costs are royalty payments to the owner of the property

- the acquisition cost of natural resources is recorded in: Undeveloped Property Account

- A company later assigns that cost to the natural resource if exploration efforts are successful

- if the efforts are unsuccessful, it writes off the acquisition cost as a loss

Exploration Costs

- as soon as the company has the right to use the property it incurs exploration costs to find the resource

- when exploration costs are substantial, some companies capitalize them into the depletion base

- in the oil and gas industry, where the costs of finding the resource are significant and the risks of finding the resource are very uncertain, most large companies often capitalize these exploration costs

- smaller oil and gas companies often capitalize these exploration costs

- expensed as incurred

Development Costs

- Two parts:

1. Tangible equipment costs: include all of the transportation and other heavy equipment needed to extract the resource and get it ready for market. Companies do not include tangible equipment costs in the depletion base. Instead they use separate depreciation entries to allocate the costs of such equipment

--- some tangible assets (drilling rig foundation) cannot be moved

--- companies depreciate these assets over their useful life or the life of the resource, whichever is shorter

2. Intangible development costs: such items as drilling costs , tunnels, shafts, and wells

--- these costs have no tangible characteristics but are needed for the production of the natural resource

--- intangible development costs are considered part of the depletion base

Restoration Costs

Companies sometimes incur substantial costs to restore property to its natural state after extraction has occurred

- companies consider restoration costs part of the depletion base

- the amount included in the depletion base is the fair value of the obligation to restore the property after extraction

- companies deduct from the depletion base any salvage value to be received on the property

Cost Allocation

- normally companies compute depletion (cost depletion) on a units of production method (an activity approach)

- depletion is a function of the number of natural resources less salvage value is divided by the number of units estimated to be in the resource deposit, to obtain a cost per unit of product.

- to compute depletion, the cost per unit is then multiplied by the number of units extracted

Estimating Recoverable Reserves

- change the estimate of recoverable reserves bc they have new information or because more sophisticated production processes are available

- same as accounting for changes in estimates for the useful lives of PPE. The procedure is to revise the depletion rate on a prospective basis: A company divides the remaining cost by the new estimate of the remaining recoverable reserves

Liquidating Dividends

- if the company does not expect to purchase additional properties it may gradually distribute to stockholders their capital investments by paying liquidating dividends, which are dividends greater than the balance in retained earnings

- The major accounting problem is to distinguish between dividends that are a return of capital and those that are not. Bc the dividend is a return of the investor's original contribution, the company issuing a liquidating dividend should debit Paid-in Capital in Excess of Par for that portion related to the original investment, instead of debiting Retained Earnings.

Continuing Controversy: Full-Cost Concept

- those who support this argue that the cost of drilling a dry hold is a cost needed to find commercially profitable wells

Continuing Controversy: Successful Efforts Concept

- other think companies should capitalize only the costs of successful projects

- the only relevant measure for a project is the cost directly related to that project, and that companies should report any remaining costs as period charges.

- they say an unsuccessful company will capitalize many costs that will make it appear, over a short period of time, as profitable as a successful company

Because of the significant impact on the financial statements of the depreciation method(s) used, companies should disclose the following

1. Depreciation expense for the period

2. Balances of major classes of depreciable assets, by nature and function

3. Accumulated depreciation, either by major classes of depreciable assets or in total

4. a general description of the method or methods used in computing depreciation with respect to major classes of depreciable assets

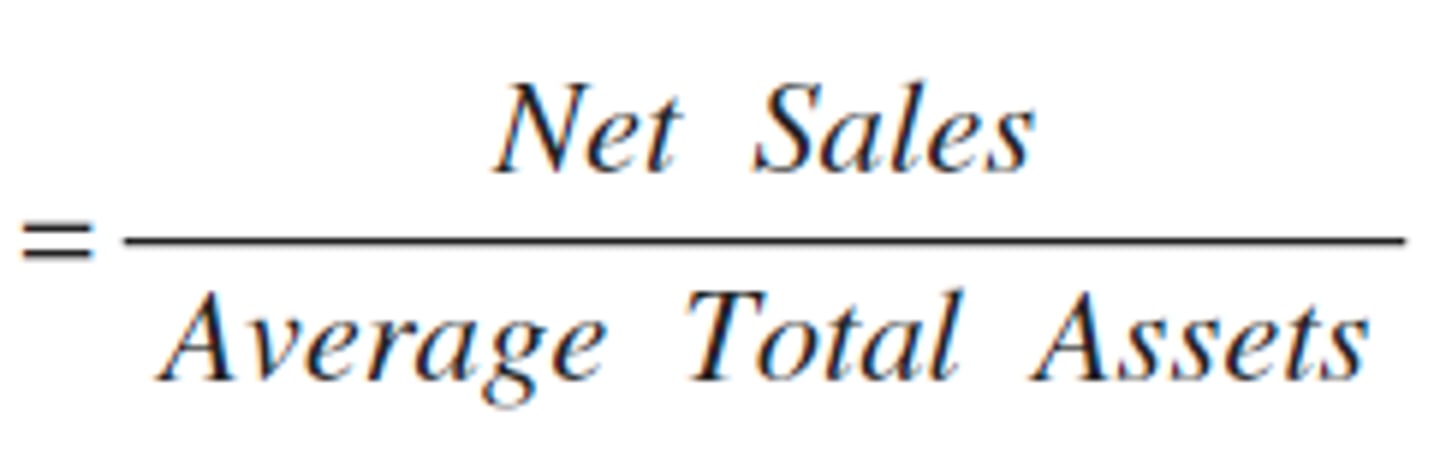

Asset Turnover

how efficiently a company uses its assets

Profit Margin on Sales

measure for analyzing the use of property, plant and equipment

- return on sales

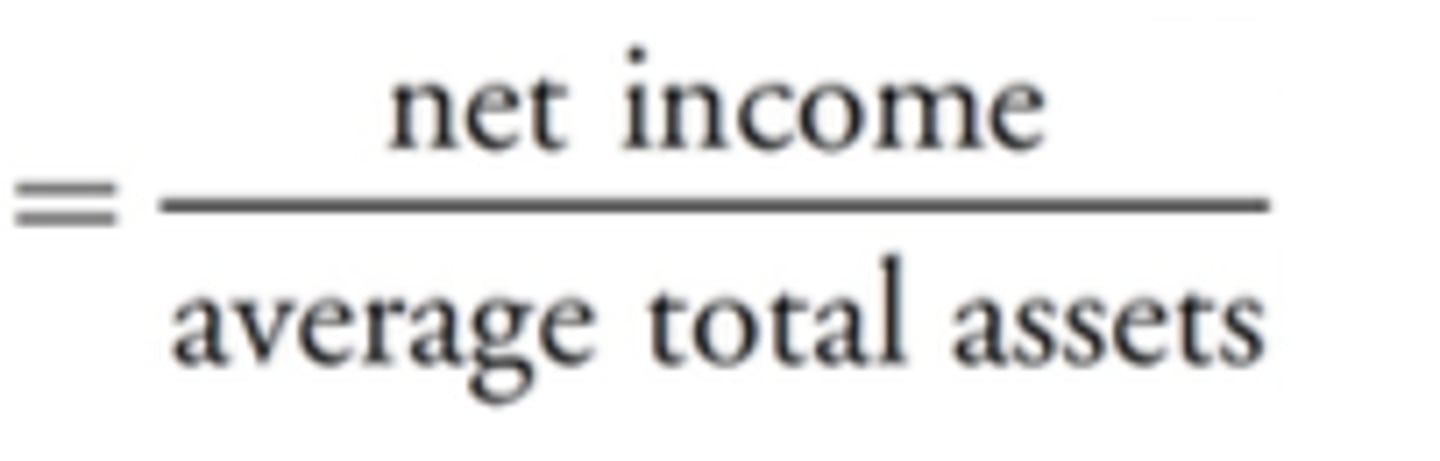

Return on Assets

how profitability the company used its assets during that period in a measure of the return on assets

profit margin * Asset turnover