Economics, Microeconomics 2.1-2.3 Demand, Supply, & Market Equilibrium

1/29

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

30 Terms

Demand

quantity of a good or service that customers are willing to buy at different prices in a given time period (effective demand = willing and able)

“law of demand”

as the price of a product falls, the quantity demanded of the product will usually increase, (ceteris paribus)

because of the law of demand

the demand curve is always downward sloping, showing the inverse relationship between price and quantity

the income effect

if the price of a product falls peoples income has more purchasing power

the substitution effect

as prices for a good increase, the quantity demanded decreases as consumers seek cheaper substitutes

the law of diminshing marginal utility

the more units of something is consumed, the less satisfaction it gives the consumer

therefore, as more units are consumed the price must decrease to offset the decreasing utility

a change in price therefore results in a

change in quantity demanded or a movement along the demand curve

Shifters of demand are

Change in number of buyers

Change in consumer income

Change in taste and preferences

Change in expectations for future

Related Goods

the two types of related goods are

Compliments

goods that may be bought with the product

these often share an inverse relationship between the price of one and the demand for the other

Substitutes

goods than can act as a repacement for the product

these often have a direct relationship between the price of one and the demand for the other

Normal goods are when

the demand for the product increases when the consumer income increases

inferior goods are when

the demand for the product decreases when the consumer income increases (or demand increases when income decreases) -

the law of supply is

as the price of a good rises, the quantity supplied will usually increase (ceteris paribus)

suppliers will often produce more to

take advantage of the higher prices

there is a direct relationship between price and quantity, therefore

the supply curve is upward sloping

a change in price will result in

a change in quantity supplied or a movement along the supply curve

the shifters of supply are

Subsidies and taxes

Technology

Other goods

Number of sellers

Expectations

Resource costs

Shocks

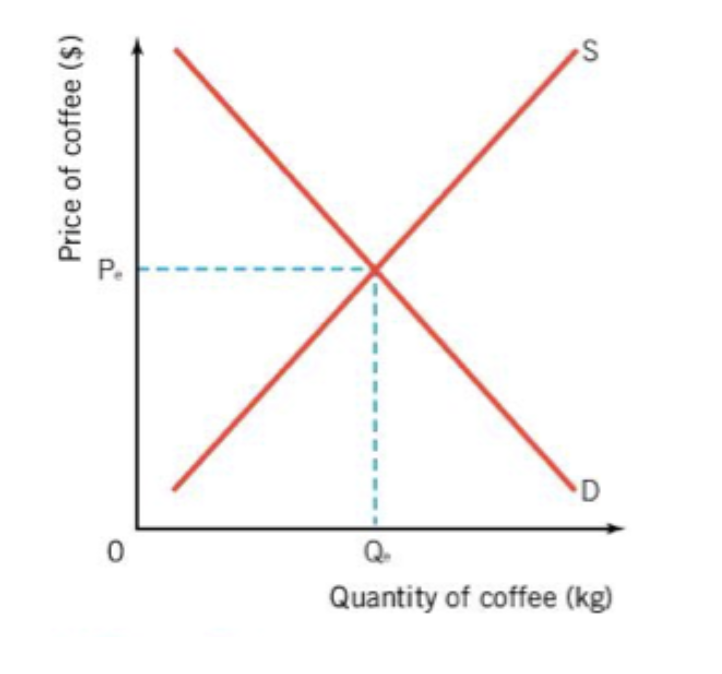

market equilibrium is where

the amount of goods people are willing to buy at the equilibrium price is equal to the amount of goods suppliers want to sell at the price

the market equilibrium is also known as

the market clearing price and will remain until it is changed by an outside factor

market equilibria are self correcting

meaning they will always return to equilibrium unless supply or demand are shifted by an outside factor

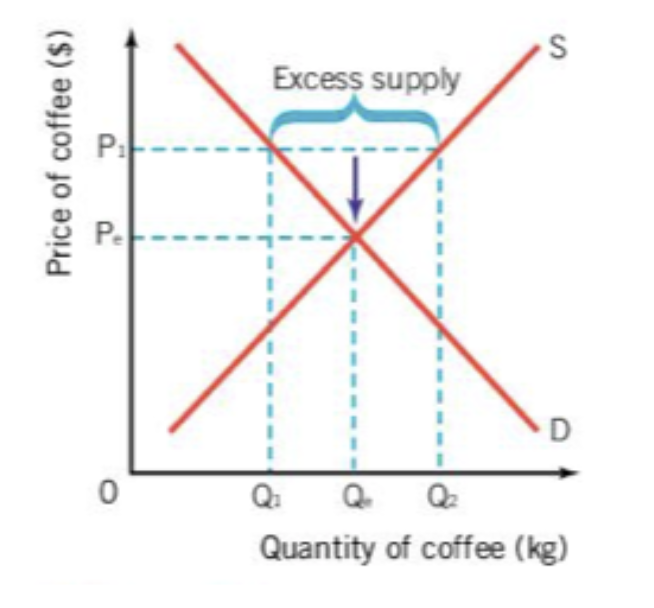

when there is excess supply this causes a

surplus

if producers were to raise the price of coffee to P1, the demand for coffee will fall to Q1 and the supply of coffee will increase to Q2

in reality this means the price of coffee is too high for consumers to willingly buy it, leading to an excess amount of coffee

to sell off the excess amount of coffee producers will have to lower the price resulting in an increase in demand and a return to equilibrium price and quantity

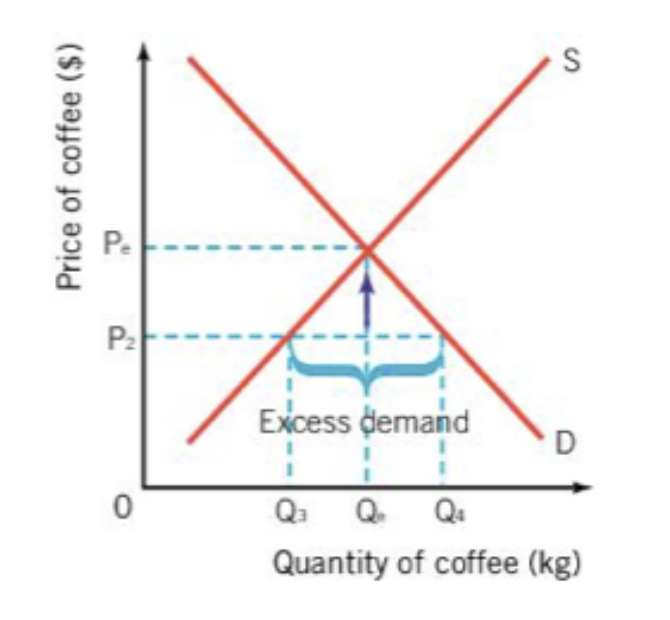

when there is a lack of supply this causes a

shortage

if producers lower the price of coffee to P2 the demand for coffee will increase to Q4 and the supply of coffee will decrease to Q3

in reality this means that consumers demand for coffee exceeds the supply at price P2, resulting in a shortage of coffee

to eliminate the shortage suppliers will have to raise the price to result in a decrease in demand, increase in supply and a return to equilibrium price and quantity

the price mechanism, or the forces of supply and demand

is what moves the market to equilibrium and allocates scarce resources

the price mechanism has three functions

signalling function

Prices of goods act as a signal, providing information for consumers and producers

incentive function

the price signal creates an incentive for producers and consumers to act in the market

rationing function

producers and consumers action ration and allocate resources within the market

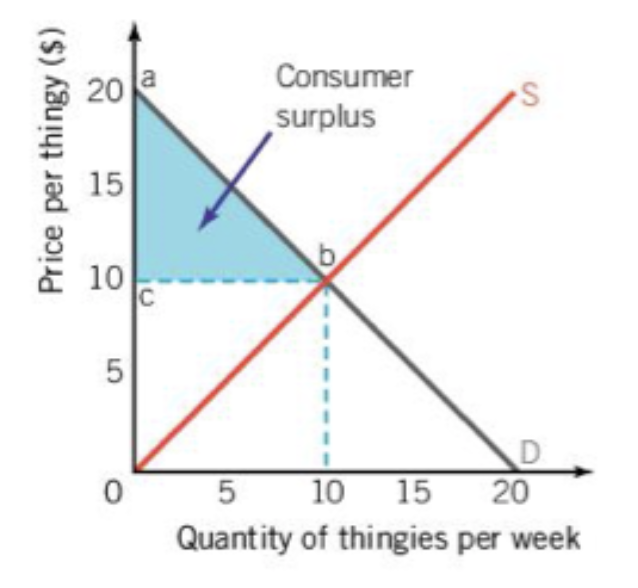

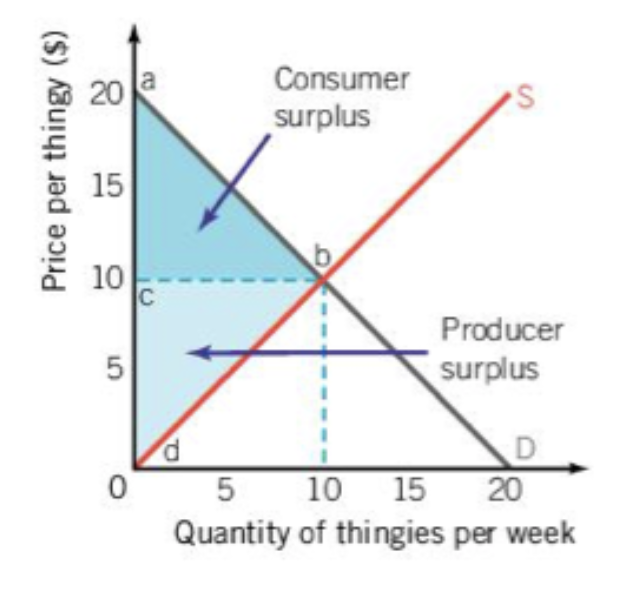

if you have wanted to buy something and then learnt you are paying less than what you were willing to pay, this is called

consumer surplus

if a producer was willing to sell their product at a lower price but didn’t have this would be called

producer surpluss

when the space of consumer surplus and producer surplus are combined it creates

community surplus

when a market has achieved equilibrium it has reached

allocative efficiency

allocative efficiency means that

the market is producing the optimal level of goods to satisfy customers and producers in society