Financial Accounting

1/117

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

118 Terms

Definition Accounting

Business transactions that capture and monitor flows of funds and payments, in terms of amount and value

Financial accounting: purpose

external communication

Financial accounting: requirement

mandatory

Financial accounting: stakeholders

external

Financial accounting: regulations

German Commercial Code (GCC)/International Financial Reporting Standards (IFRS)

Financial accounting: period

annual

Financial accounting: enforcement

auditors, regulators

Financial accounting: focus

past economic situation

Financial accounting: scope

company

Financial accounting: areas

financial statement (balance sheet, income statement, etc.)

functions of accounting

documentation

payments (taxes and dividends)

information

documentation function

chronological, systematical and complete recording of business transactions

protection against legal suits

information function

inform stakeholders of the financial status

analysis of financial value; annual profit/loss comparing income and expenses

focus on financial items, no sustainability aspects

internal stakeholder

employees, board of directors, top management

external stakeholders

investors, banks, customers, suppliers, NGOs, government

payment function

annual profit is used to calculate dividends and tax payments

inventory

list of assets and debts

stocktaking

determination of assets and debts

§ 1, 2, 3, 6, GCC

every trader must determine his/her assets and debts at the founding of his/her company and by the end of every accounting period (one year)

§ 242 GCC

all traders must calculate their assets and debts by the start and end of every accounting period in the balance sheet

equity

total assets - total debts = equity stock

assets

structured by liquidity

non current assets (e.g. properties, buildings, machinery)

current assets (e.g. raw materials, supplies, goods)

liquidity status

ratio of current and non current assets

high ratio of current assets preferred

debts

structured by maturity

long-term debts (e.g. bank credit)

short-term debts (e.g. supplier debts)

higher ratio of long-term debts preferred

long-/short-term = more/less than one year

structure inventory

A. Assets

I. Non current assets

II. Current assets

Total Assets

B. Debts

I. Long-term debts

II. Short-term debts

Total debts

C. Equity

opening balance

assets and debts at the start of accounting period

closing balance

assets and debts at the end of accounting period

principle of balanced equity

closing balance year 0 = opening balance year 1

structure balance sheet

left side: assets

A. Non current assets

I. intangible assets (e.g. license, data purchase)

II. property, plant and equipment

III. financial assets

B. Current assets

I. Goods

II. Recievables (e.g. pending payments)

III. Shares

IV. Cash/cash equivalents

Total assets

right side: capital

A. equity

B. Debts

I. long-term debts

II. short-term debts

Total capital

balance sheets must ALWAYS be balanced

Assets = …

capital

non current assets + current assets

Capital =

assets

equity + debt capital

application of funds = …

source of funds

non current + current assets = …

equity + debt capital

assets

equity = …

assets - debt capital

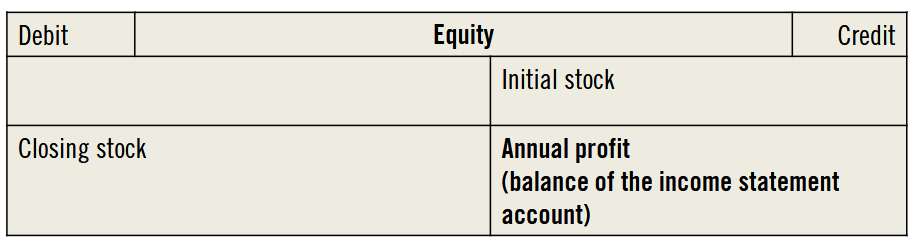

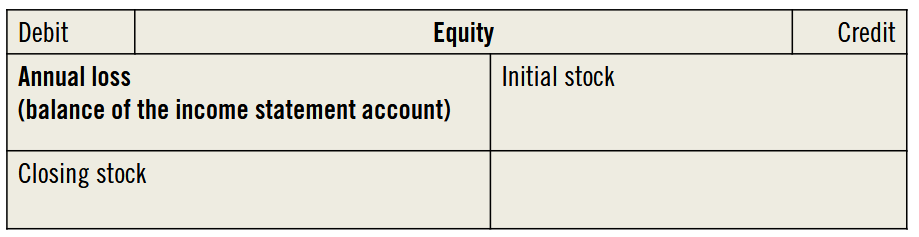

annual profit or loss

calculated by the comparison of equity stocks:

equity stock by the end of the period

(-) initial equity stock at the beginning of the period

(+/-) private drawings/deposits

= annual profit or loss

income statement

collect all expenses and revenues during the business year as changes of equity stock

downsides of the balance sheet

always outdated

source of annual profit/loss is unknown

revenue

total amount of income generated by the sale of goods and services related to the primary business operations

→ increase of equity stock

expenses

total amount of outflow of mone or any form of fortune as payment for an item, service, or other category of costs

→ decrease of equity stock

calculation annual profit/loss via the income statement

total revenues - total expenses = annual profit/loss

balance sheet + income statement = …

financial statement

income statement: total cost method

comparison of revenues and total production expenses for all produced units

recongnize changes in inventory: initial & final stock of finished and unfinished products

cost-type-oriented structure of expenses

preferred by small- to medium-sized firms

income statement: cost of sales method

comparison of revenues and expenses of goods sold

product-oriented structure of expenses

demands more resources

preferred by large firms

income statement (total cost method): structure

(+ / -) increase/decrease of inventories

(-) material expenses

(-) staff expenses

(-) other operating expenses

(+ / -) financial profit/expenses

= annual profit/loss

income statement (total cost method): changes in inventory

increase (amount produced > amount sold): credit side of income statement account; revenue

decrease (amount produced < amount sold): debit side of income statement account; expense)

income statement (cost of sales method): structure

(-) Expenses

(+ / -) Financial profit/loss

= annual profit/loss

Questions for booking transactions

Which accounts are affected

Are stock accounts or profit & loss accounts affected?

Which account increase or decrease?

On which account(s) do I debit and credit?

debit side in transaction posting

left

credit side in transaction posting

right

stock accounts

further structured in asset accounts and liability accounts

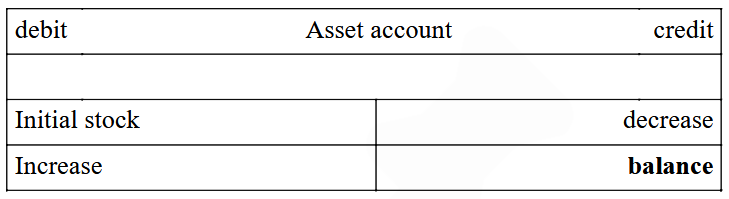

structure asset account

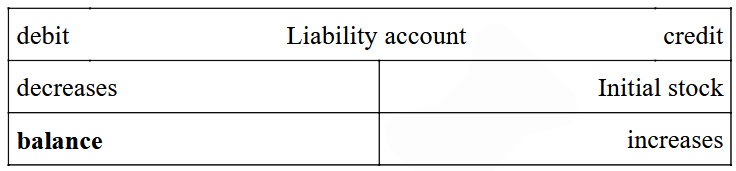

structure liability account

initial stock + increases - decreases =

final stock (balance)

single posting

business transaction affects exactly two accounts

composed posting

business transactions affects more than two accounts

example: deposit of 1000€ from bank account to cash account

cash debit 1000€; bank credit 1000€

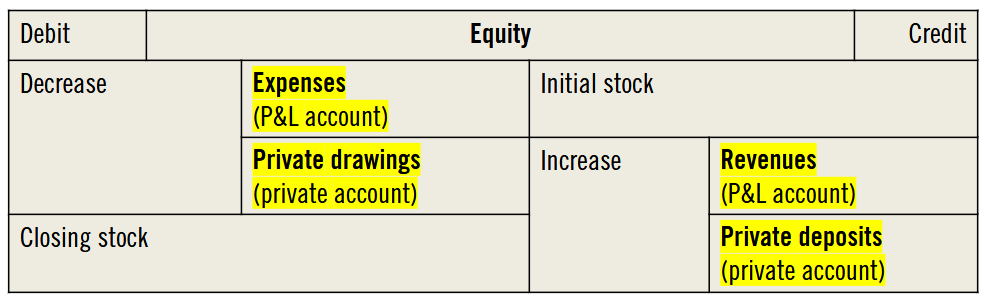

changes in equity (categorization)

do not affect income:

private account

private drawing

private deposit

affect income:

income statement account

expenses

revenues

definition expenses

decrease stock of equity

outflows, uses of assets, incurring of liabilities from delivering goods or services

show on the debit side of the income statement account

definition revenues

increase stock of equity

total amount of income generated by sales of products and services

show on the credit side of the income statement account

structure equity account

structure expense account

structure revenue account

equity account with annual profit

equity account with annual loss

private transactions …

never affect income

must be recorded seperately

private drawings …

decrease equity stock (debit side equity account)

private deposits …

increase equity stock (credit side equity account)

asset swap

balance sheet total remains constant

change in the structure of the assets

example: goods purchase via cash

capital swap

unchanging balance sheet total

change in the structure of equity and/or debt capital

example: conversion of a short-term liability into a long-term liability

balance sheet extension

increase of assets and capital of the same amount

example: goods purchase on credit

balance sheet contraction

decrease of assets and capital of the same amount

example: paying a trade payable account via bank transfer

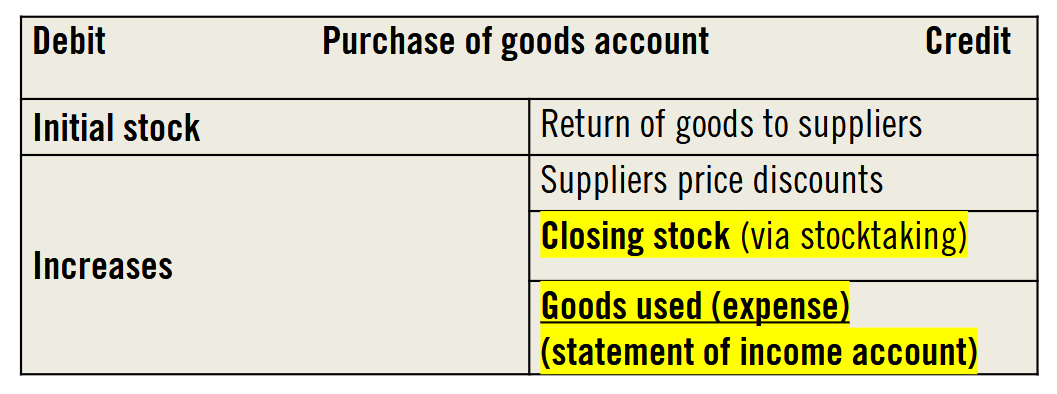

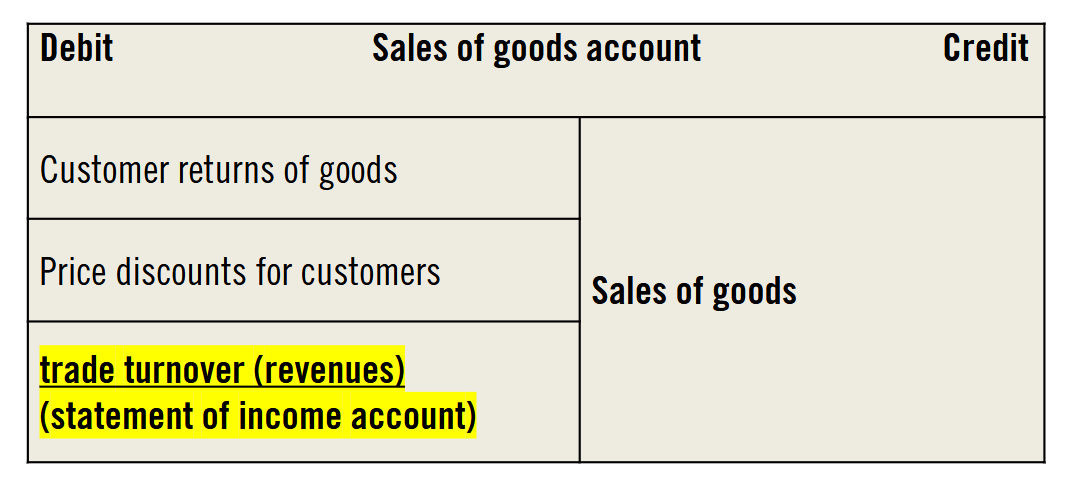

goods account is structured into …

purchase account

sales account

structure purchase of goods account

= asset account

structure sales of goods account

= profit and loss account

gross method

close purchase and sales account directly through the statement of income account

goods used and trade turnover are unbalanced in the statement of income account for better readability of profitability

value added tax (VAT)

= consumption tax

only the consumer pays it

only paid when additional value is created

VAT > input tax

payment charged on the debit side of the VAT account

debt to tax authorities

VAT < input tax

input tax account contains a balance on the credit side

recievable from tax authorities

liability account increases…

on the credit side

asset account increases…

on the debit side

types of stock account

liability account

asset account

types of profit & loss account

revenue account (increase on credit side)

expense account (increase on debit side)

cash discount

deduction from the gross invoice amount for payment within a specific period of time

incentives for early payments

advances from demand

supplier recieves a payment in advance: liability to the customer (+VAT)

advances to supply

customer holds a claim against the supplier amouting to the advance: recievables from the supplier (+input tax)

wage

recieved by workers, based on worked hours/produced quantities

salary

recieved by employees, independent from hours/quantities

compulsory social security expenses

50/50 between employer and employee

pension

health

unemployment

nursing care

casualty insurance

social security expenses employer

compulsory social security expenses

voluntary social security expenses (e.g. wedding/birth benefits)

expenses for pensions

employer withholds … from salary payments

wage tax

church tax

solidarity tax

employee contribution to social security

gross wages and salaries are posted …

on the debit side of the expense account “wages and salaries”

retained tax reductions are posted…

on the credit side of the liability account “charges still to be paid”

transferred by the 10. of the following month

employer contribution to social security is posted…

in the expense account “social security expenses”

raw materials

main component of production (e.g. wood)

asset account

supplies

minor component of production (e.g. glue)

asset account

consumables

supporting role for production (e.g. electricity)

asset account

consumption of materials are posted…

in the according expense account

amortization of assets

spreading the initial cost of an asset over its estimated useful life

depreciation by …

time or performance

use most appropriate method

stay consistent over following periods and for similar assets