Chapter 4

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

Cash Equivalents

Short-term investments that have a maturity date no longer than 3 months from the date of purchase

Total Cash Balance is derived from (these are also things that are considered cash) (a)

Coins and currency

Checks Received

Savings Accounts

Total Cash Balance is derived from (these are also things that are considered cash) (b)

Checking Accounts

Credit Card Sales

Debit Card Sales

Cash Equivalents (ex. short term investments)

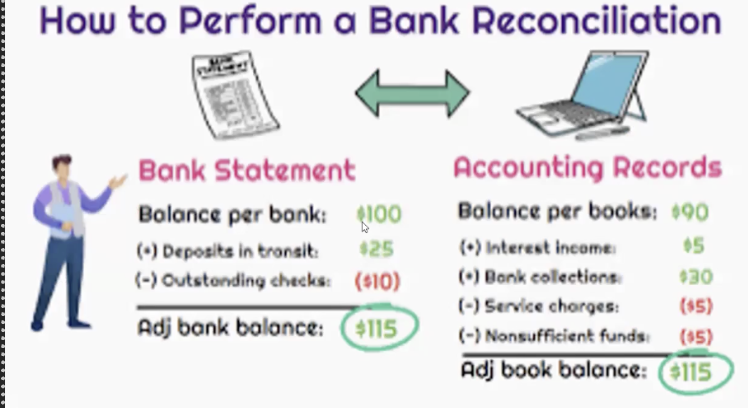

Bank Reconciliation

process of comparing the company's cash records (cash book) with the bank's records to make sure they match and to identify any differences.

Things that may explain difference in cash balance in accounting records and balance on bank statement

Deposit in transit

Outstanding check

NSF (bounced) check

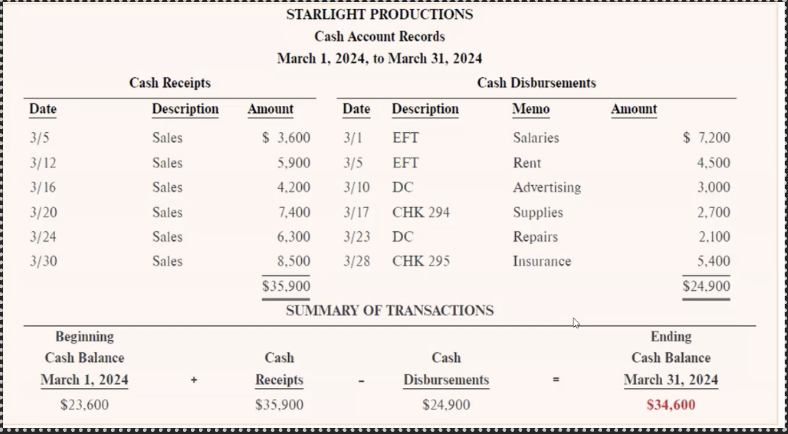

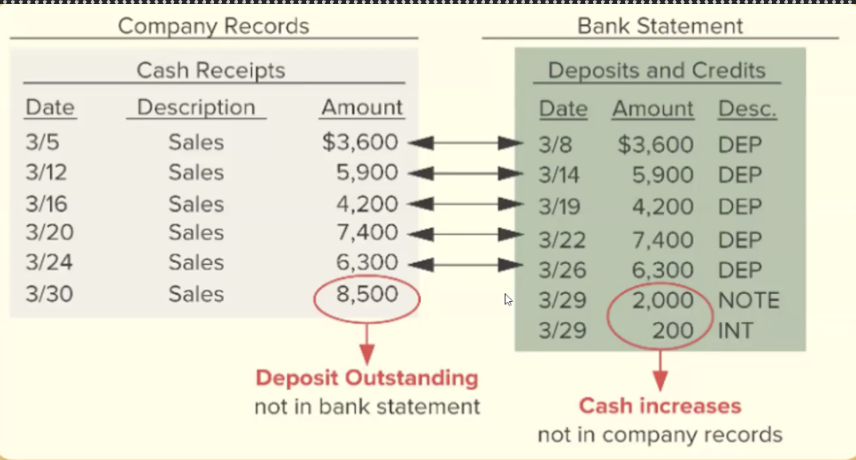

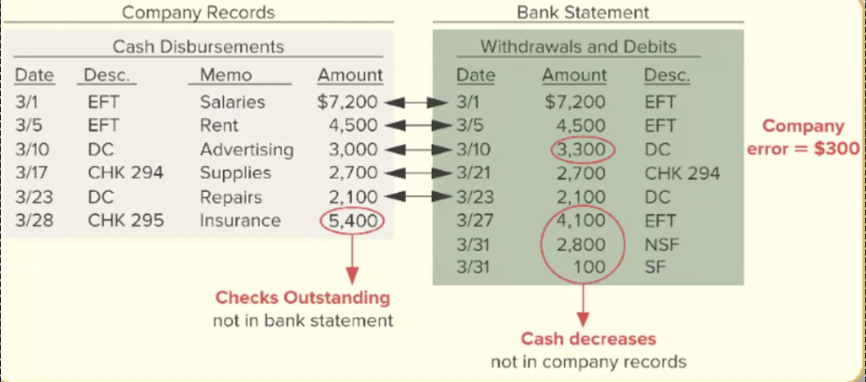

Company Records of Cash Activities

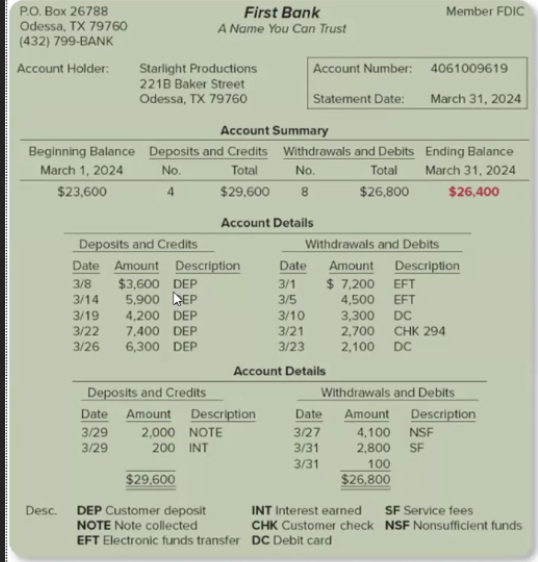

Bank Records

Looking at both records (IN RED), the cash amounts are not the same

Bank records say company spent more than company records say

Questions to ask if you find a discrepancy in bank records

Why is our cash amount higher?

Why is our disbursement lower?

Differences in Company Records and Bank Statement (a)

2 differences highlighted in red

Differences in Company Records and Bank Statement (a)

We must do a journal entry for any amounts that are in Bank Statement but not in Company Records

don’t need company records bc it may for items that have not made it to bank yet

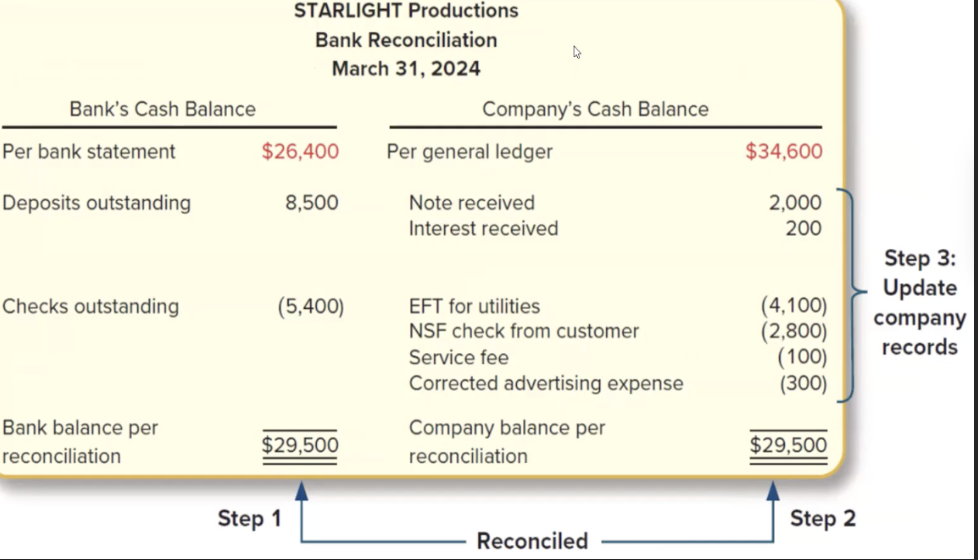

Bank Reconciliation / Adjusting bank cash balance

Start w bank balance which is 26.4k

Then adjust, in previous ex. We saw deposit of 8.5k didn’t make it so you adjust

Also, the disbursement of 5.4k has not been made yet so you take it away

Adjusting Company Cash Balance

Things in bank were deposits so they must be added to bank total (2k) (200)

Need to reduce balance from withdrawals

Equaling out

After adjusting the bank cash balance and the company cash balance both should equal each other

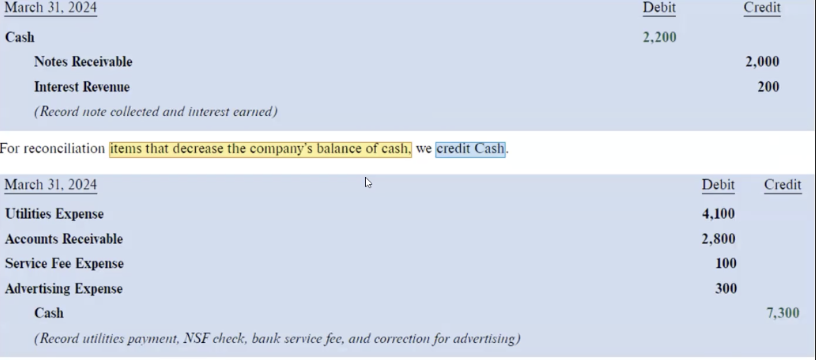

Update Company Records

Looking at records cash must be increased 2.2k so it will be adjusted in journal

Debit items that increase company cash and debit items that lower company cash

Make sure to do two journal entries one reducing cash and one adding cash

In actual business you can do additions and reductions all on one journal

Actions that increase cash

Notes Received

Interest Received

Actions that decrease cash

EST for utilities (utilities expense)

NSF check from customer (accounts receivable)

Service fee expense

Adverting expense

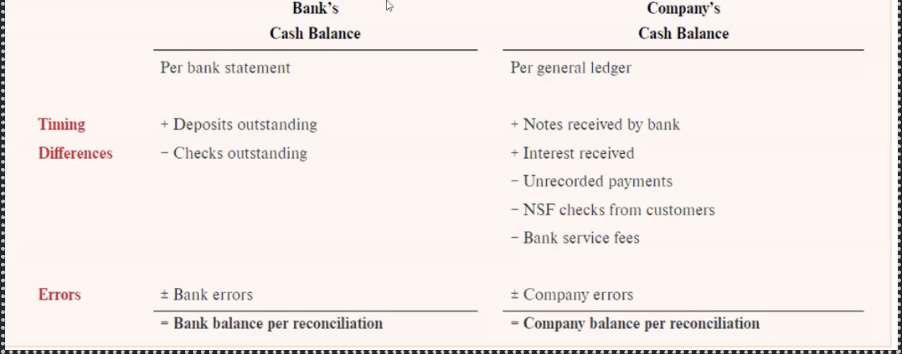

Summary of what will be seen in records

Checks outstanding

Checks written by the company that have not yet cleared the bank.

Subtract from the bank statement balance during reconciliation.

Deposits outstanding (deposits in transit)

Cash received and recorded by the company that has not yet been credited by the bank.

Add to the bank statement balance during reconciliation.

NSF (bounced) check

customers check is returned unpaid

bank removes money must update records