Ch. 9: Labour Market Decisions of Firms (Micro) Demand for Labour

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

Wage Elasticity of Demand

Depends on:

Percentage of labour costs in total costs

Number of subs for labour

Price elasticity of th prod. or service

Labour Productivity

The output per worker

Gross Domestic Product

GDP

The value of all final goods and services produced in a year

Workers are more productive

Increases as output increases

Productity Growth: Macro Influences

The economy as a whole

Structure of the economy

Industrial composition: Manufacturing or services

Economic conditions

Recession or expansion

Govt. policies:

Fiscal Policies: Spending and taxation

Productity Growth: Micro Influences

Individuals business firms

Scale of business operations: Large businesses are more productive

Management technique: Educated managers are better at motivating staff an using better tools and equipment leading to higher productivity

Firm’s Demand for Labour

Dervied from th demand for final goods and services that require labour as an input

Also influenced by the productivity of lavour improve through experience and education

Market’s view of the value of the services

Productivity Growth: Micro and Macro

The economy as a whole

Quantity and quality of capital: Employees become more productive as the quality and quantity of the tools increase

Labour Force; Characteristics of the labour force (age, health, education, etc)

Quasi-Fixed Labour Costs

Non-wage to hiring employees that are not related to the hours of work

Hiring costs: Advertising, screening, recording keeping, payroll, etc

Training: Materials and salaries of trainers

Opportunity Costs: Lost production from those in training

Marginal Revenue

Revenue from selling one more product

Short Run

A period when at least one factor of prod. cannot be changed

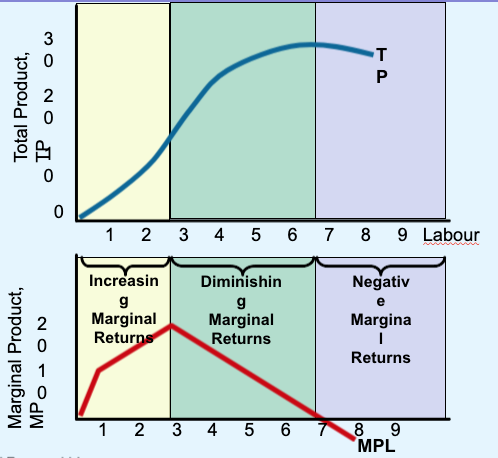

Law of Diminishing Returns

LDR

States that in the short run a point will be reached at which the extra contribution of the next worker to total output will be less than that of the previously hired worker

Contribution of the next worker to total output is the Marginal Product of Labour (MPL)

Why the Long Run Demand Curve Slopes Down

Long Run: All factors of production are variable

Scale Effect: Cost goes down as quanitity demand increases

Hire more if selling more

Subsitution Effect

Sub. Capital (machinery) for labour, making it cheaper and faster

Marginal Product of Labour

MPL

Can covert the contribution of each successive worker into a dollar of revenue

Marginal Revenue: Addition to total revenue as a result of selling an extra unit of output

MPL x MR= MPL

Employer’s Decision Rule for Hiring

Wage rate > MRP (Marginal Revenue Product)= Don’t hire

Wage rate < MRP= Hire

Wage rate = MRP= Indifferent, need to watch that line!

Scale Effect

The change in the number of employees hired as a result of changes in the amount sold

Two Reasons for Increases in Demand for Labour

Increases due to greater productivity of labour

Improvement in MPL

Can also increase due to shifts in demand for final foods or services, tus increasing MR

Demand for Labour in a Given Occupation can Change…

Increases in demand for final goods and services to make them

Change in the price of substitutes: Unions vs non-unions

Change in the price of complements: Price of steel drops= increase in demand for steel workers

Change in Quantity Demand in Response to a Change in Wage Rate

= Percentage change in the quantity of workers demanded/ percentage change in the wage rate

Ed= %△ / %△WR

Ed> 1.0 (elastic)

Cross Elasticity of Demand

Increase in wages paid to one occupation can lead to changes in another occupation

Increase= sub effect

Decrease= complementary effect

Coefficent= %△OccA / %△WROccB