Lvl2: Quantitative Methods

1/59

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

60 Terms

Dependent variable is continuous vs discrete

Continuous: the traditional regression model

Discrete: logistic regression

Regression Process

Analyze the residuals

Examine the goodness of fit - significance of fit

Assumptions in a simple regression

Linearity - Dependent & independent

Homoskedasticity - same variance of regression residuals

Independence of errors - observations are independent; regression residuals are uncorrelated

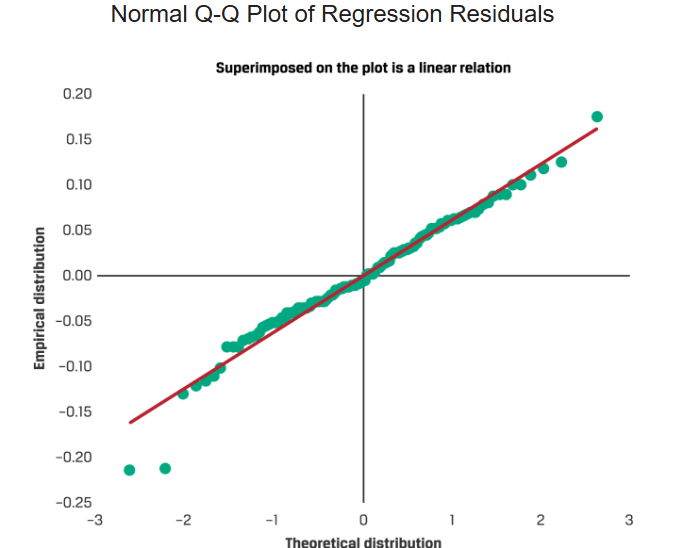

Normality - regression residuals normal distribution

Independence of independent variables - not random; no linear relation between ind variables

normal Q-Q plot

visualize the distribution of a variable (regression residual) by comparing it to a normal distribution

coefficient of determination (R-squared)

ratio of the variation of the dependent variable explained by the independent variables (sum of squares regression) to the total variation of the dependent variable (sum of squares total)

Disadvantages of R-squared

cannot provide information on whether the coefficients are statistically significant

biases in the estimated coefficients and predictions

cannot tell whether the model fit is good - bad model may have a high R2 due to overfitting and biases in the model

overfitting

model is too complex - too many independent variables relative to the number of observations in the sample

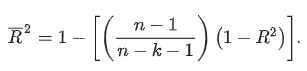

adjusted R-squared

does not automatically increase when another independent variable is added to a regression

R2 is strictly greater than adjusted R2

adjusted R2 may be negative, whereas the R2 has a minimum of zero

Akaike’s information criterion (AIC)

lower AIC indicates a better-fitting model

Schwarz’s Bayesian information criterion (BIC)

BIC assesses a greater penalty for having more parameters in a model

AIC vs BIC

AIC is preferred if the model is used for prediction purposes

BIC is preferred when the best goodness of fit is desired

Test whether a variable is significant in explaining the dependent variable’s variation

H0: bj = 0 and Ha: bj ≠ 0

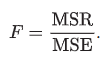

F-distributed test statistic

q is the number of restrictions

How to test for significance

Define hypothesis

Find critical value

Reject the null if calculated statistic exceeds critical value

If fail to reject the null i.e. null is correct

general linear F-test

test the null hypothesis that slope coefficients on all variables are equal to zero

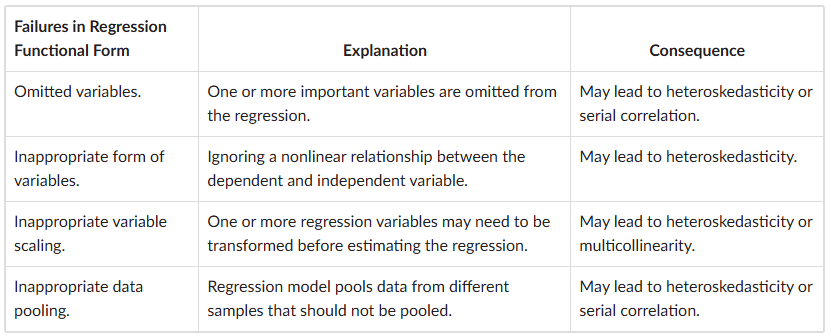

Omitted variable bias

omission of an important independent variable

If the omitted variable is uncorrelated with X1, the coefficient for X1 will still be estimated correctly

Misspecified Regression

Unconditional heteroskedasticity

error variance is not correlated with the regression’s independent variables - no major problems for statistical inference

Conditional heteroskedasticity

error variance is correlated with (conditional on) the values of the independent variables

t-statistics will be inflated

tend to find significant relationships where none actually exist

more Type I errors (rejecting the null hypothesis when it is actually true)

Breusch-Pagan (BP) test

test for conditional heteroskedasticity

heteroskedasticity-consistent standard errors

robust standard errors

adjust the standard errors of the regression’s estimated coefficients to account for the heteroskedasticity

serial correlation or autocorrelation

regression errors are correlated across observations

incorrect estimate of the regression coefficients’ standard errors

no adjustment required if none of the regressors is a lagged value of the dependent variable

more Type I errors

positive vs negative serial correlation

positive residual for one observation increases the chance of a positive residual in a subsequent observation

a positive residual for one observation increases the chance of a negative residual for another observation

Durbin-Watson (DW) test

measure of autocorrelation

compares the squared differences of successive residuals with the sum of the squared residuals

applies only to testing for first-order serial correlation

ranges from 0 to 4 (~2 = no autocorrelation, < 2 positive. >2 negative)

Breusch-Godfrey (BG) test

can detect autocorrelation up to a pre-designated order p, where the error in period t is correlated with the error in period t – p

n – p – k – 1 and p degrees of freedom, where p is the number of lags

serial -correlation consistent standard errors

adjust the coefficient standard errors to account for the serial correlation

multicollinearity

when two or more independent variables are highly correlated or when there is an approximate linear relationship among independent variables

impossible to distinguish the individual impacts of the independent variables

diminished t-statistics, so t-tests of coefficients have little power (ability to reject the null hypothesis)

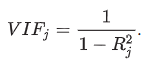

Variance inflation factor (VIF)

VIFj > 5 warrants further investigation of the given independent variable

VIFj >10 indicates serious multicollinearity requiring correction

correct for multicollinearity

excluding one or more of the regression variables

using a different proxy for one of the variables

increasing the sample size

influential observation

an observation whose inclusion may significantly alter regression results

high-leverage point

data point having an extreme value of an independent variable

outlier data point

data point having an extreme value of the dependent variable

leverage (hii) - detecting high-leverage point

distance between the value of the ith observation of that independent variable and the mean value of that variable across all n observations

value between 0 and 1

if an observation’s leverage exceeds

studentized residuals - detecting outliers

compared to the critical value of the t-distributed statistic with (n − k − 2) degrees of freedom

|ti*| > 3 - outlier

|ti*| > critical value of t-statistic - potentially influential

dummy variable

takes on a value of 1 if a particular condition is true and 0 if that condition is false

to distinguish among n categories, we need n − 1 dummy variables - the category not assigned becomes the “base” or “control” group

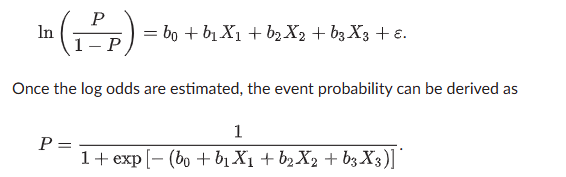

Logistic regression (logit)

The natural logarithm (ln) of the odds of an event happening

maximum likelihood estimation (MLE) method

estimates logistic regression coefficients

a chi-square-distributed test statistic

likelihood ratio (LR) test

to assess the fit of logistic regression models

LR = −2 × (Log-likelihood restricted model − Log-likelihood unrestricted model)

chi-squared with q degrees of freedom

log-likelihood metric is always negative, so higher values (closer to 0) indicate a better-fitting model

Problems with a time series

serial correlation in the error term causes estimates of the intercept (b0) and slope coefficient (b1) to be inconsistent - independent variable is a lagged variable of the dependent

The mean or variance of the time series changes over time

log-linear model

ln yt = b0 + b1t + εt, t = 1, 2, . . . , T.

Covariance-Stationary

properties, such as mean and variance, do not change over time

the expected value of the time series must be constant and finite in all periods

variance of the time series must be constant and finite in all periods

covariance of the time series with itself for a fixed number of periods in the past or future must be constant and finite in all periods

standard error of the residual correlation

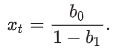

mean-reverting level

root mean squared error (RMSE)

compare the out-of-sample forecasting performance

square root of the average squared error

smallest RMSE is judged the most accurate

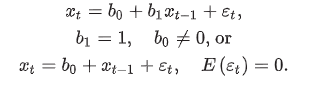

random walk

value of the series in one period is the value of the series in the previous period plus an unpredictable random error

error term, εt, has constant variance and is uncorrelated with the error term in previous periods

b0 = 0 and b1 = 1

the expected value of εt is zero

best forecast of xt that can be made in period t − 1 is xt−1

currency exchange rates

undefined mean-reverting level

for any period t, the variance of xt = (t − 1)σ2

not a covariance-stationary time series, because a covariance-stationary time series must have a finite variance

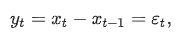

first-differencing

subtracts the value of the time series in the first prior period from the current value of the time series

mean-reverting level of the first-differenced model as b0/(1 − b1) = 0/1 = 0

variance of yt in each period is var(εt) = σ2

variance and the mean of yt are constant and finite in each period, yt is a covariance-stationary time series

random walk with drft

random walk with drift has b0 ≠ 0, compared to a simple random walk, which has b0 = 0

unit root

lag coefficient is equal to 1.0

all random walks, with or without a drift term, have unit roots

not covariance stationary

Dickey and Fuller test

unit root test

xt − xt−1 = b0 + (b1 − 1)xt−1 + εt —→ b0 + g1xt−1 + εt

a test of g1 = 0 is a test of b1 = 1

H0: g1 = 0; Ha: g1 < 0

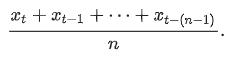

n-period moving average

to remove short-term fluctuations or noise by smoothing out the time series of sales

moving average of the current and past n − 1 values

MA(1) - moving-average model of order 1

moving average of εt and εt−1

First: examine the variance of xt and its first two autocorrelations

first autocorrelation is not equal to 0, but the second and higher autocorrelations are equal to 0

MA(1) model has a memory of one period

AR vs MA

autocorrelations of most autoregressive time series start large and decline gradually, whereas the autocorrelations of an MA(q) time series suddenly drop to 0 after the first q autocorrelations

autoregressive moving-average (ARMA) model

p autoregressive terms and q moving-average terms, denoted ARMA(p, q)

parameters in ARMA models can be very unstable

criteria for deciding on p and q for a particular time series are far from perfect

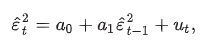

Autoregressive Conditional Heteroskedasticity Models (ARCH)

If the estimate of a1 is statistically significantly different from zero, we conclude that the time series is ARCH(1)

ARCH - predict variance of errors in period t+1

2 time series - one dependent, one independent variable

test for unit root - DF test

one of them has a unit root - not covariance stationary; one or more of linear regression assumptions violated; coefficients and standard error inconsistent; coefficient appears significant but is not

both have a unit root - establish if cointegrated

cointegrated

long-term financial or economic relationship exists between them such that they do not diverge from each other

cointegrated vs not

not; error term not covariance stationary; some regression assumptions will be violated; regression coefficients and standard errors will not be consistent, and we cannot use them for hypothesis tests

yes; error term is covariance stationary; regression coefficients and standard errors will be consistent, and we can use them for hypothesis tests; may not be the best model of the short-term relation

cointegration test

use the critical values computed by Engle and Granger

fails to reject - not cointegrated

reject - cointegrated

expected total holding period cost

trading costs = round-trip commission + bid-ask spread

management fees = fee * period