AP Micro unit 1 and 2 review

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

40 Terms

scarcity

the inability of our limited resources to satisfy human wants

How to tell if an item is scarce?

positive price

system of allocation (distribution)

Less available than wanted

opportunity cost

Factors of Production

Land

Labor

Physical Capital (Machines and tools used to produce)

Entrepreneurship

PPC (Production Possibility curve)

Maximizing combinations of 2 different goods (or categories of goods) that can be produced with fixed resources

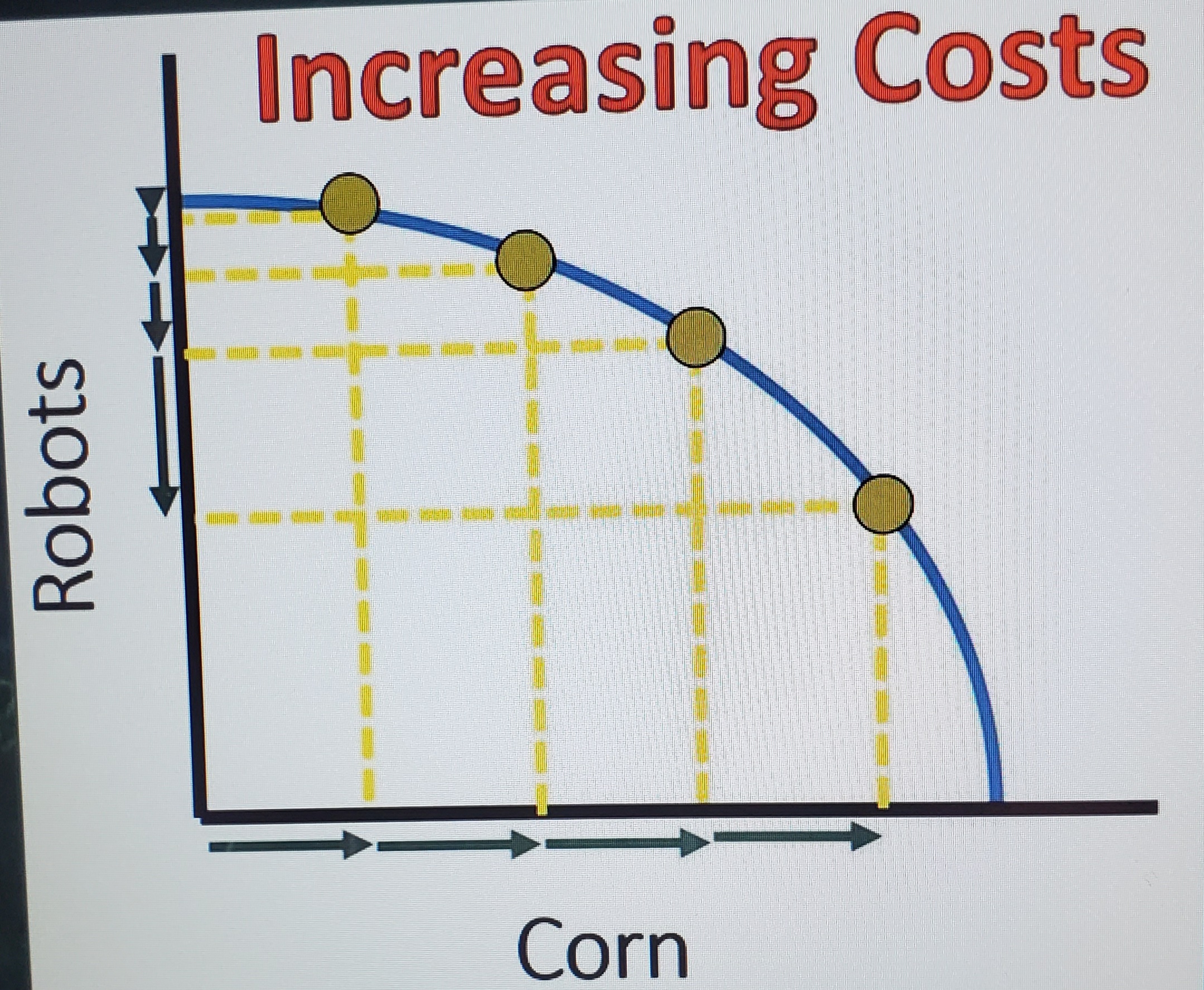

Increasing costs PPC

Resources used to make robots are not adaptable with the product with corn

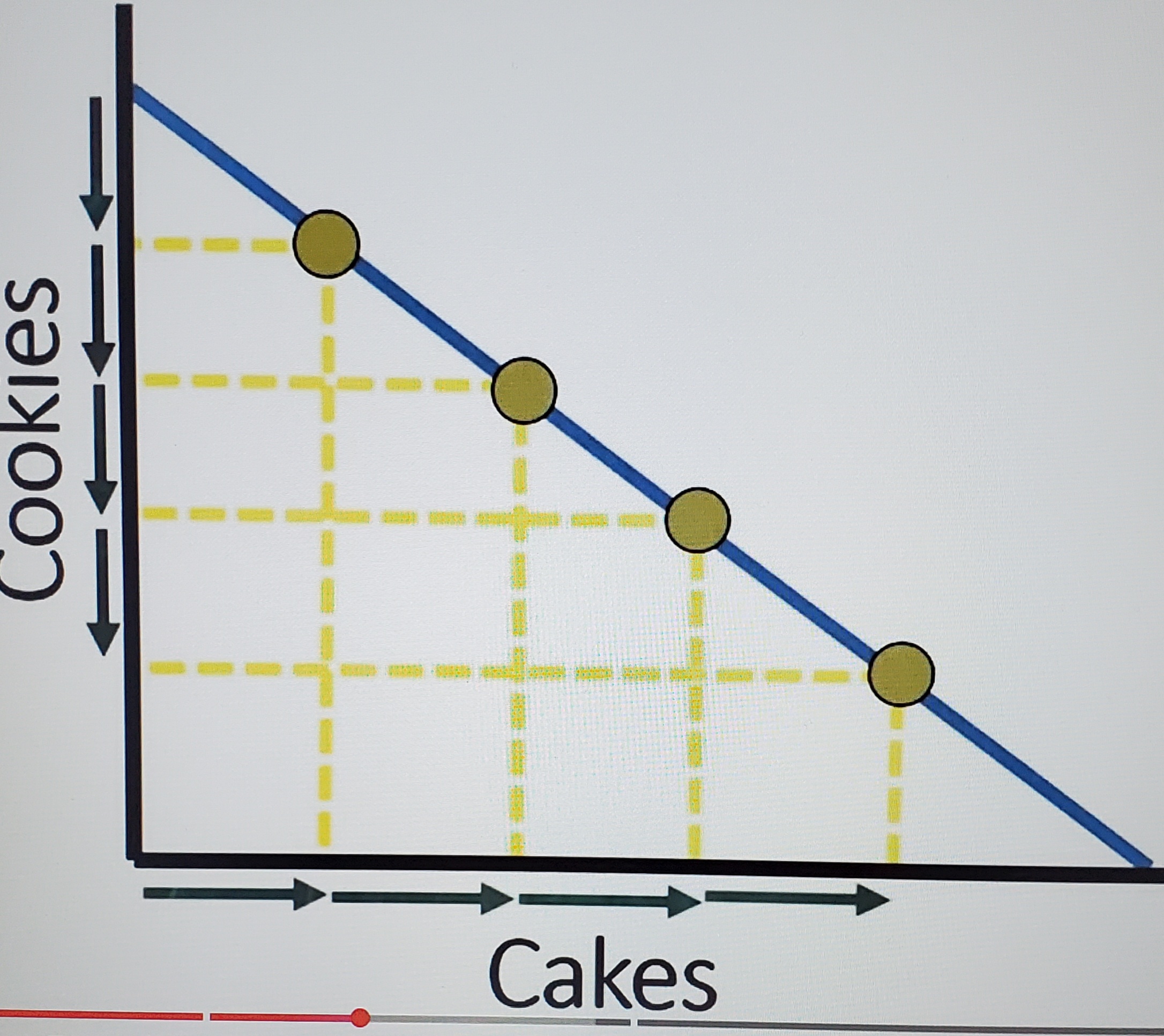

Constant costs PPC

resources used to make both goods are well adapted to each other

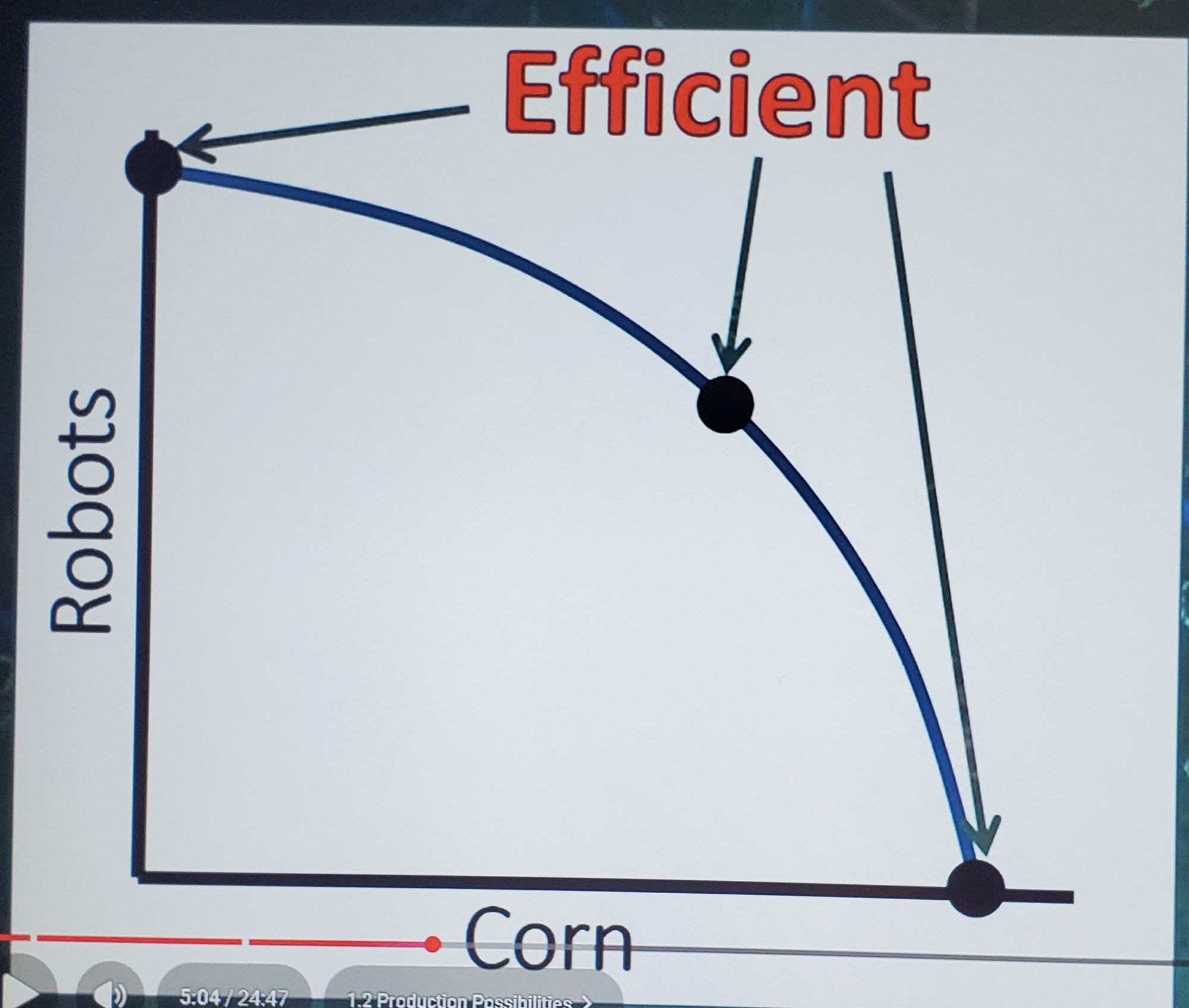

Efficient PPC

Any point on the curve is considered efficient

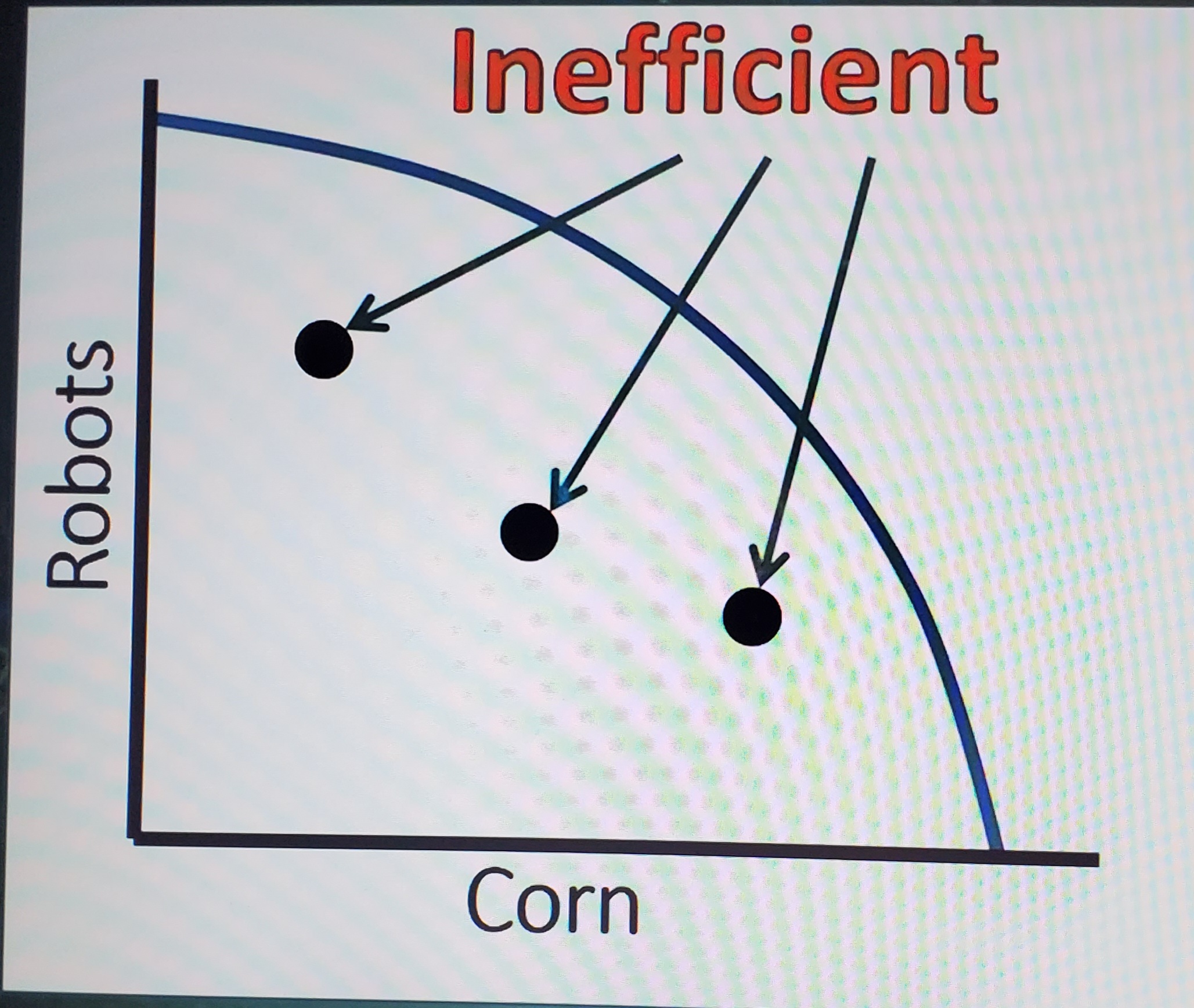

Inefficient PPC

Any points inside the curve are inefficient. The resources aren't being used correctly. Less production

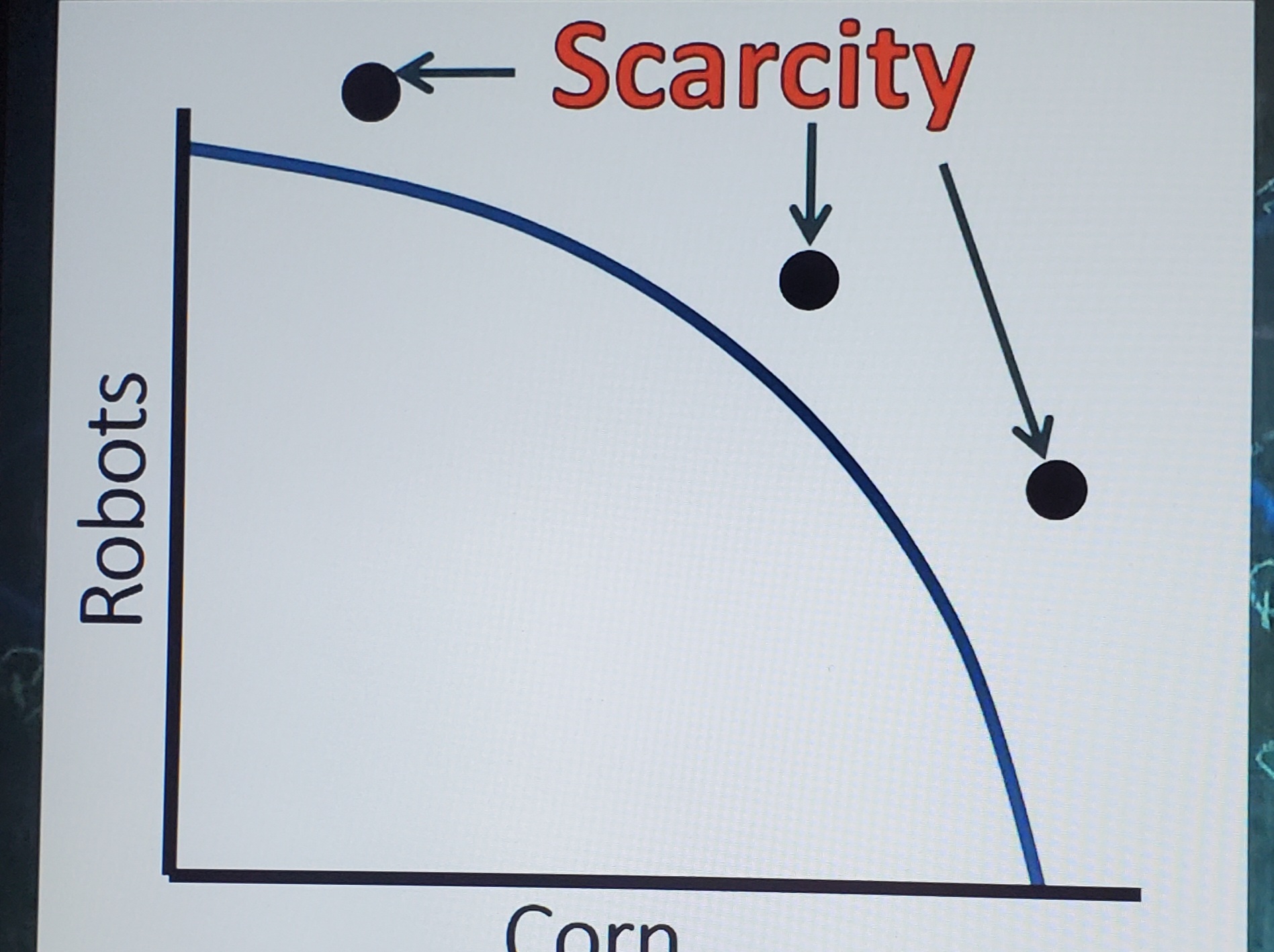

Scarcity PPC

Impossible, you cannot produce these. Must have economic growth to reach them

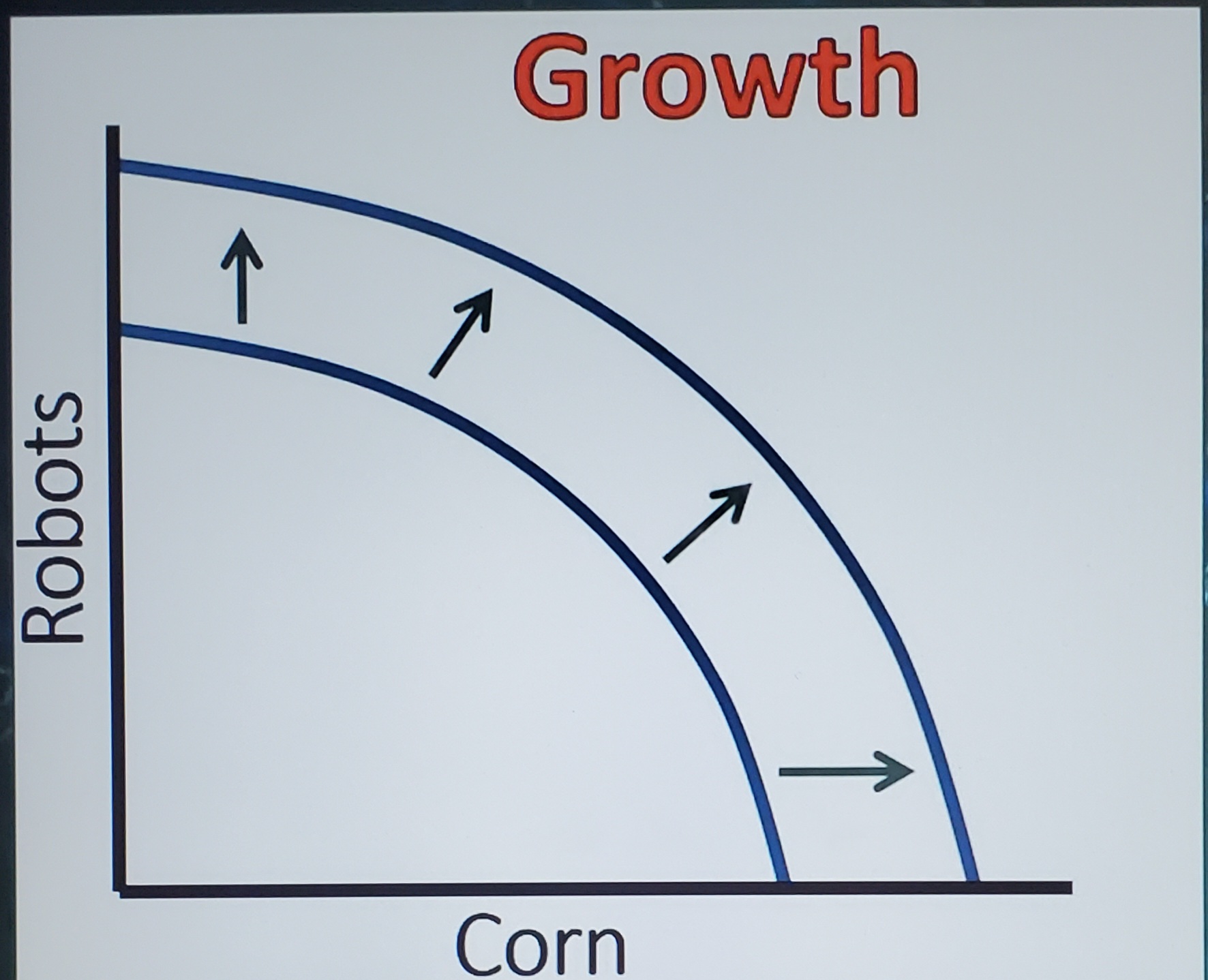

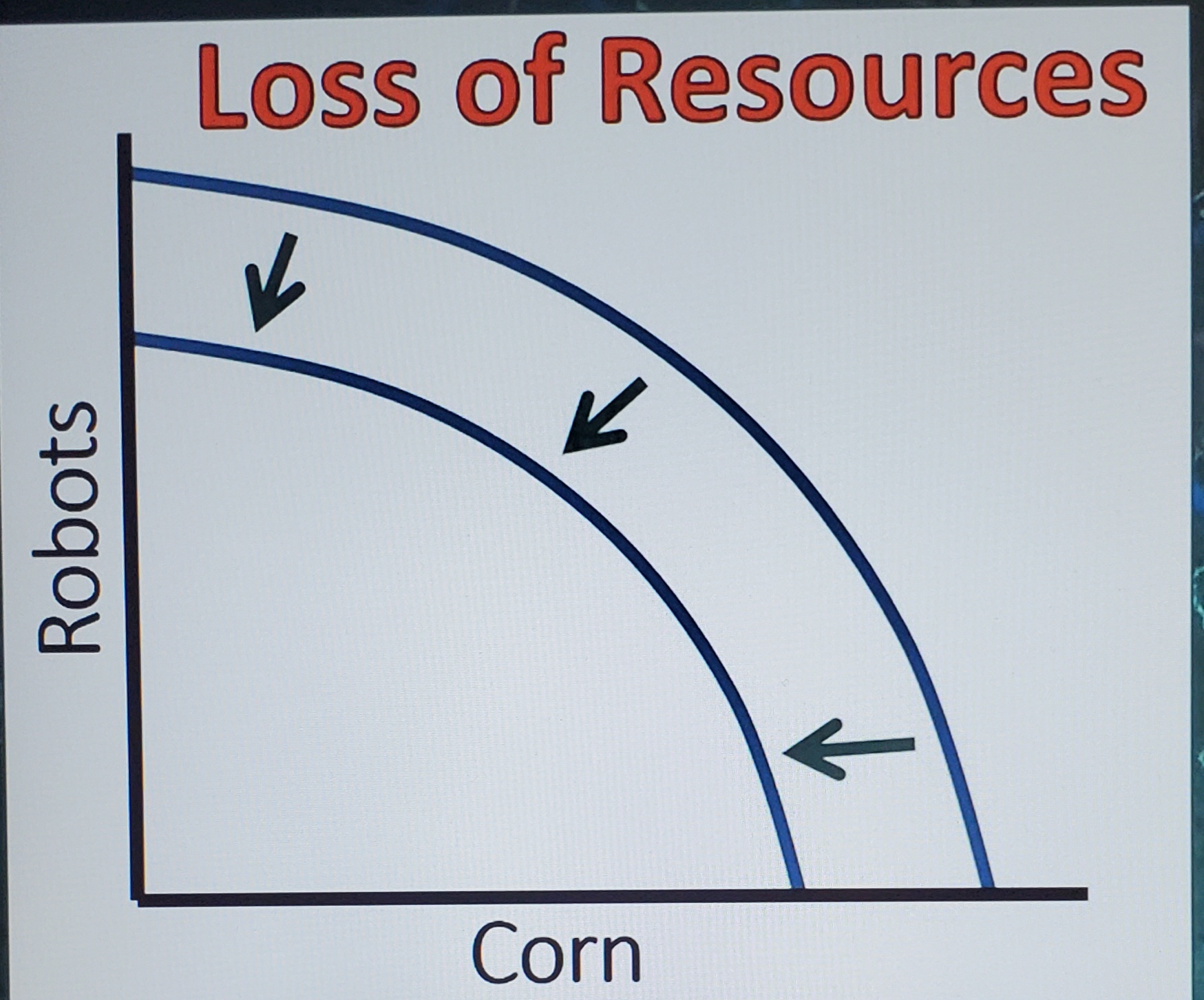

PPC Shifts

with changes in the quality or quantity of resources

Growth PPC

Increases in productivity, better resources, or more resources can cause the curve to go outwards

Loss of resources PPC

Loss of resources causes a shift inward

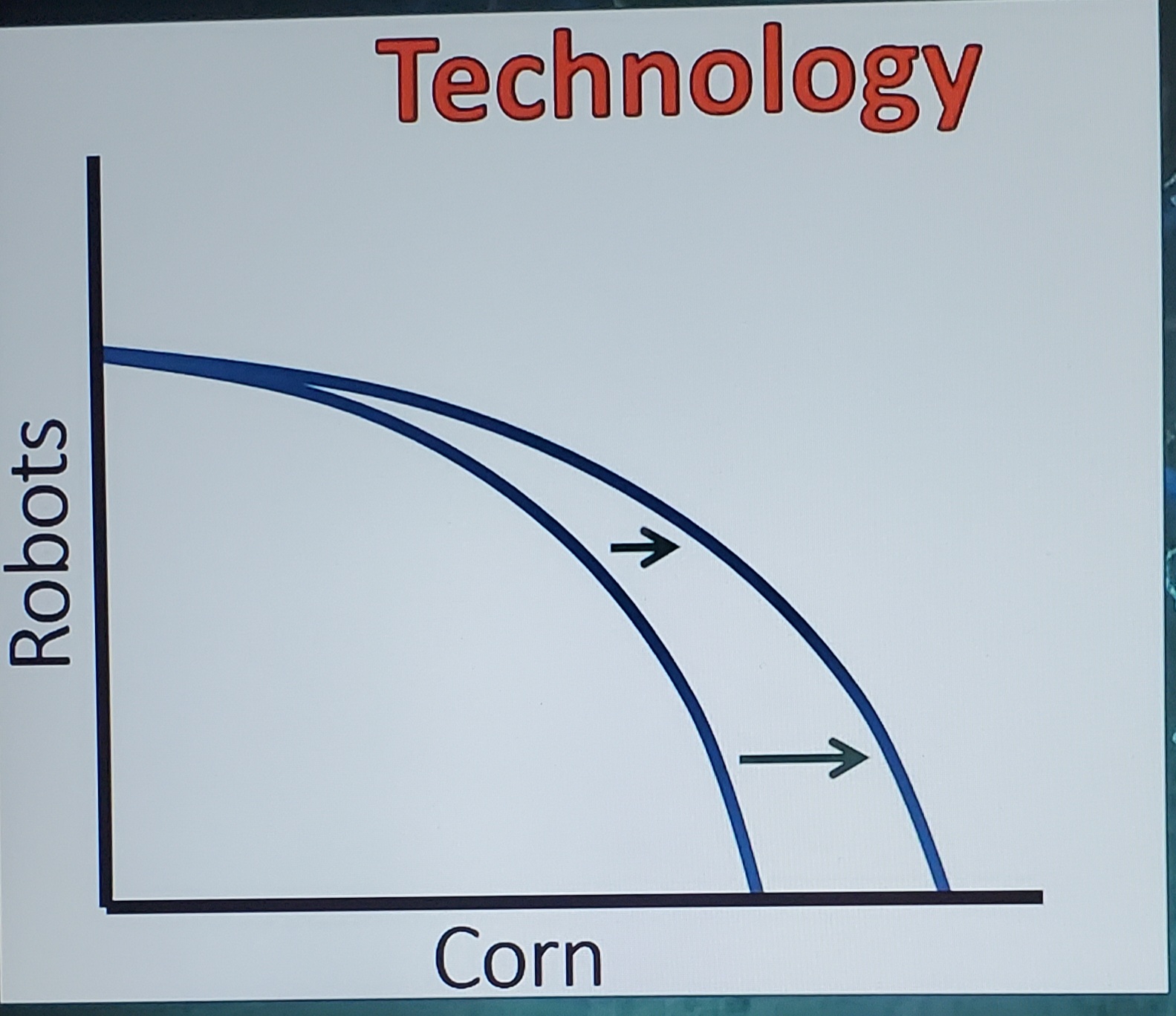

Technology PPC

produces in one curve but not the other

Absolute Advantage

ability to produce more or using fewer resources

Comparative advantage

The ability to produce something at a lower opportunity cost

Input opportunity cost equation

“It’s over” A = A/B

Input opportunity cost examples

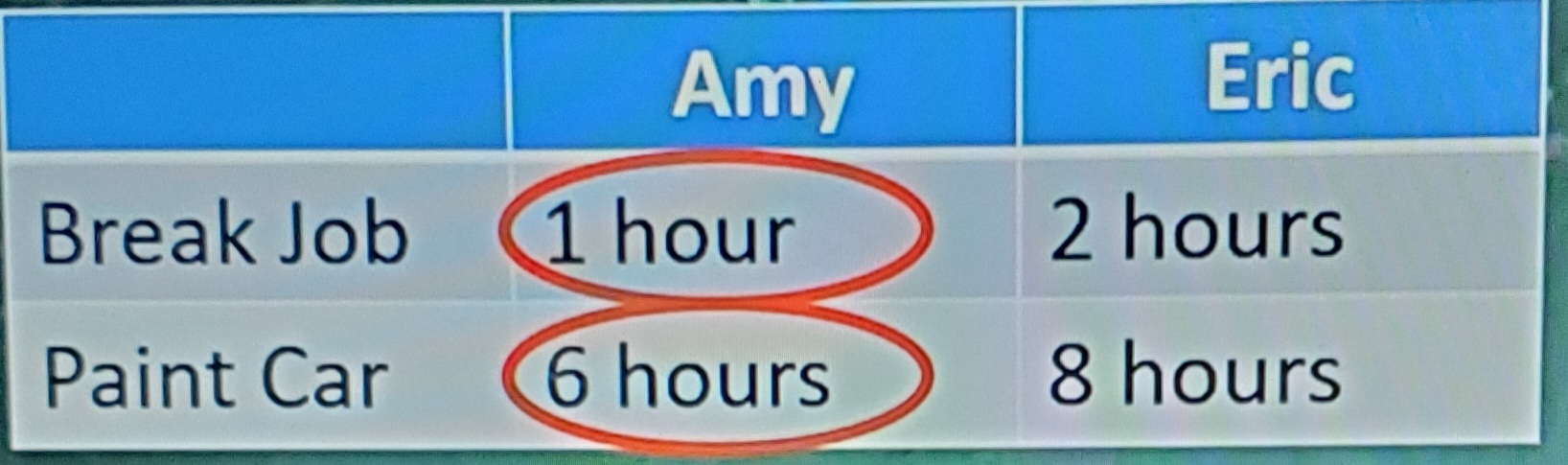

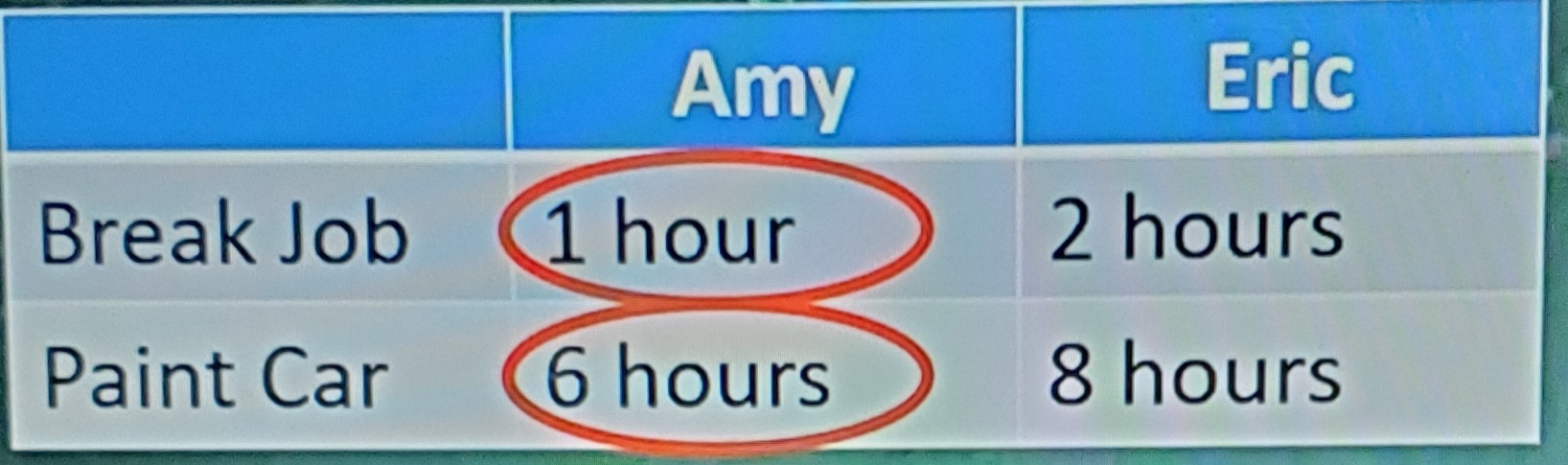

AMY:

1 Break job = 1/6 painted cars

1 Painted Car = 6 break jobs

ERIC:

1 break job = 2/8 = ¼ painted cars

1 painted car = 8/2 = 4 break jobs

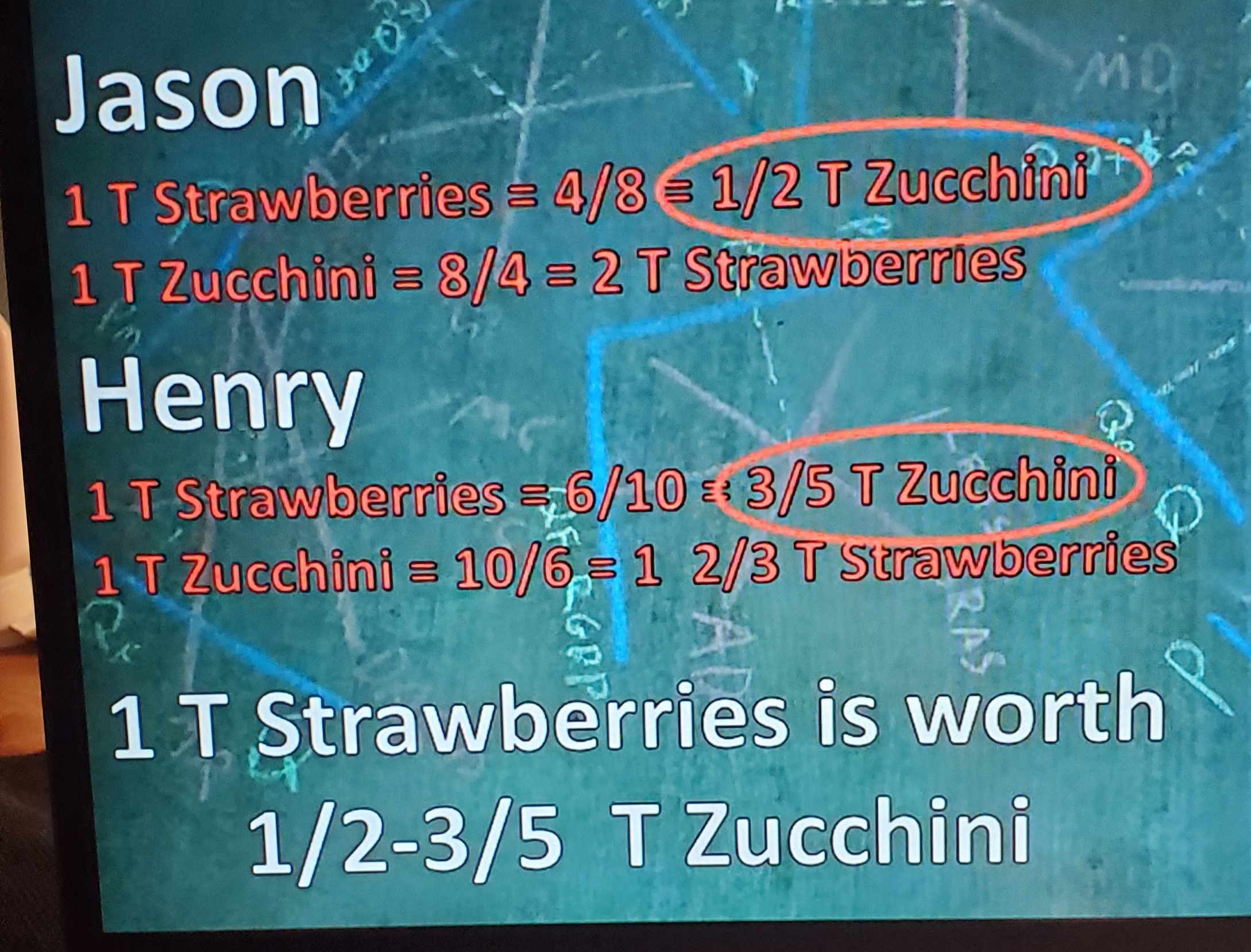

Output opportunity costs equation

“Other Over”

A = B/A

Output Opportunity Cost example

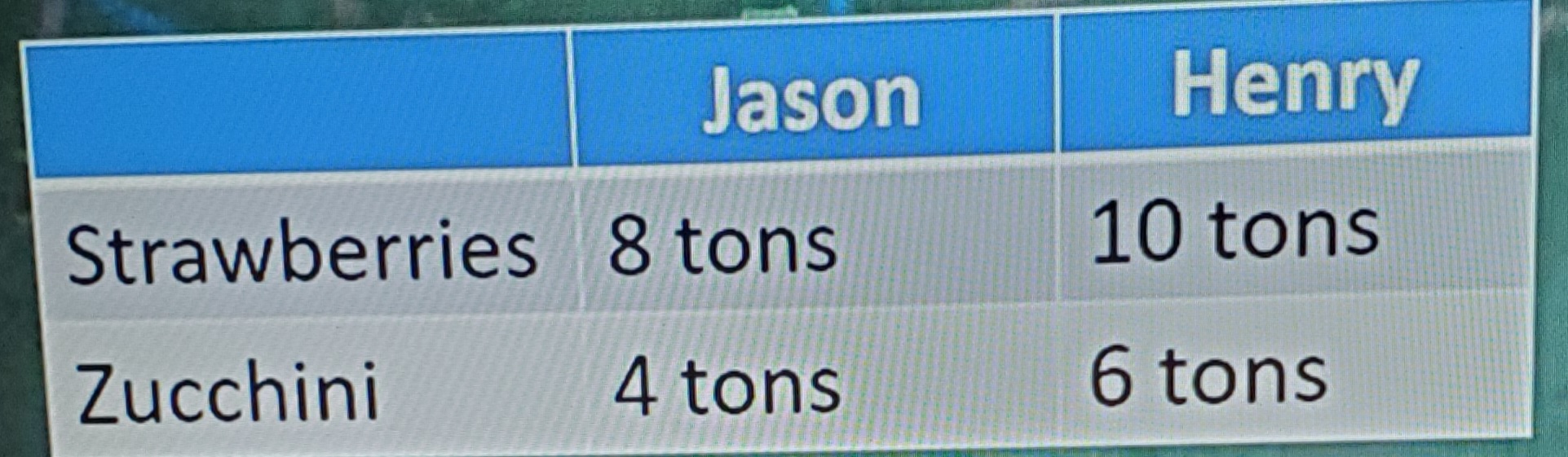

JASON:

1 T Strawberries = 4/8 = ½ Zucchini

1 T Zucchini = 8/4 = 2 T Strawberries

HENRY:

1 T Strawberries = 6/10 = 3/5 Zucchini

1 T Zucchini = 10/6 = 1 2/3 T Strawberries

Mutallt Beneficial terms of trade

will fall between opportunity costs. If outside of range, somebody is getting ripped off

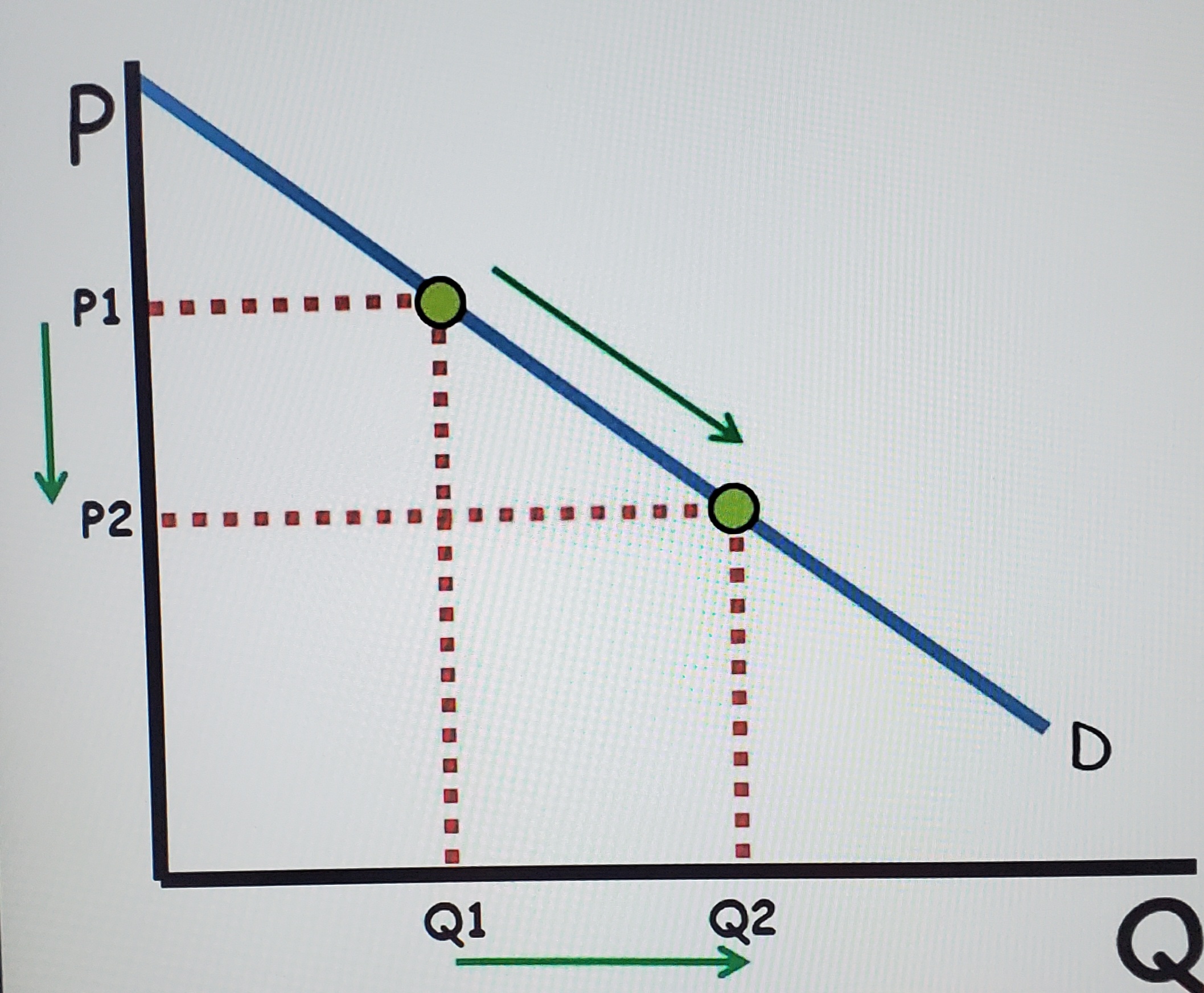

Law of demand

Ceteris Paribus, consumers buy more at low prices and less at high prices. Inverse relationship

What does price change

quantity demand (not demand)

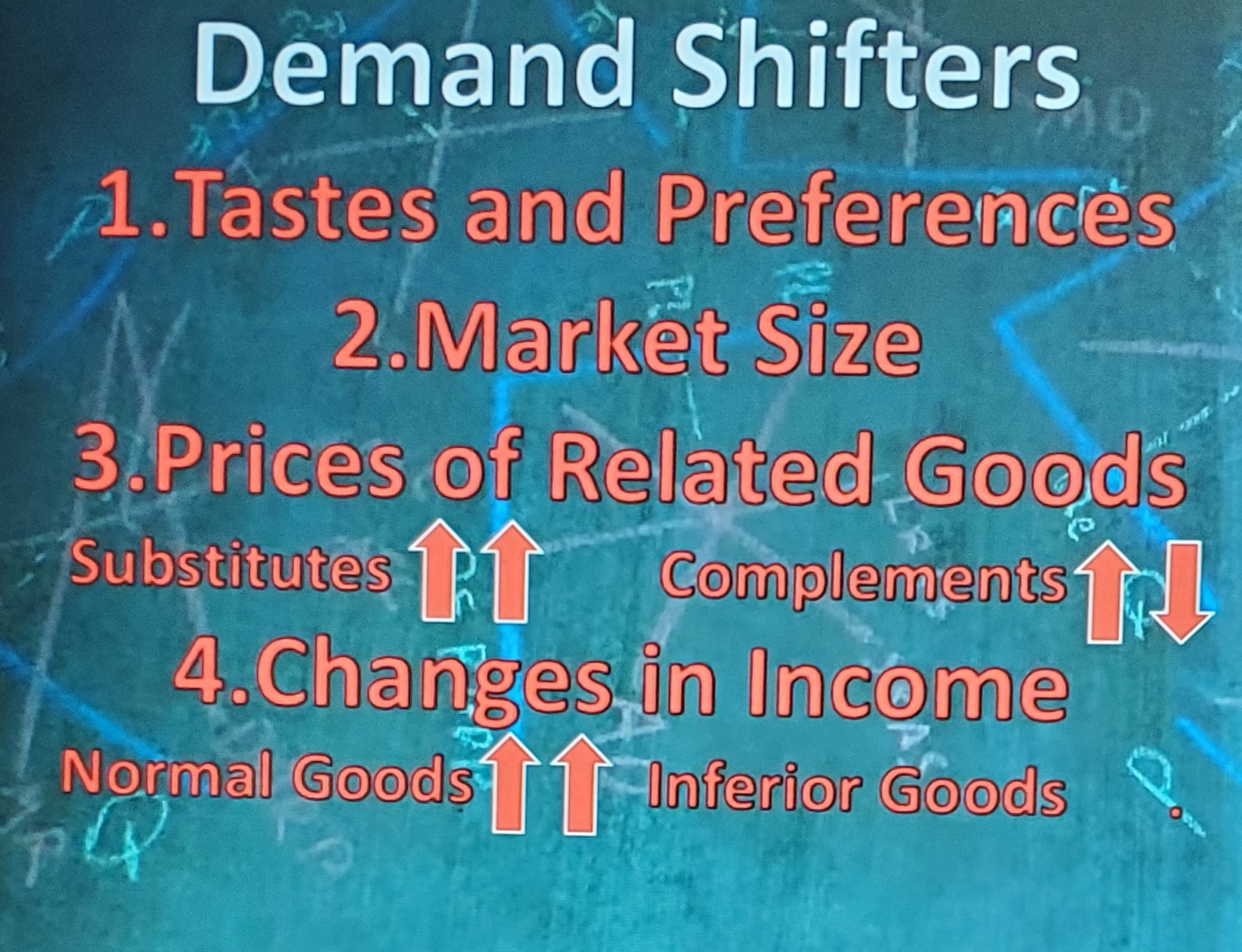

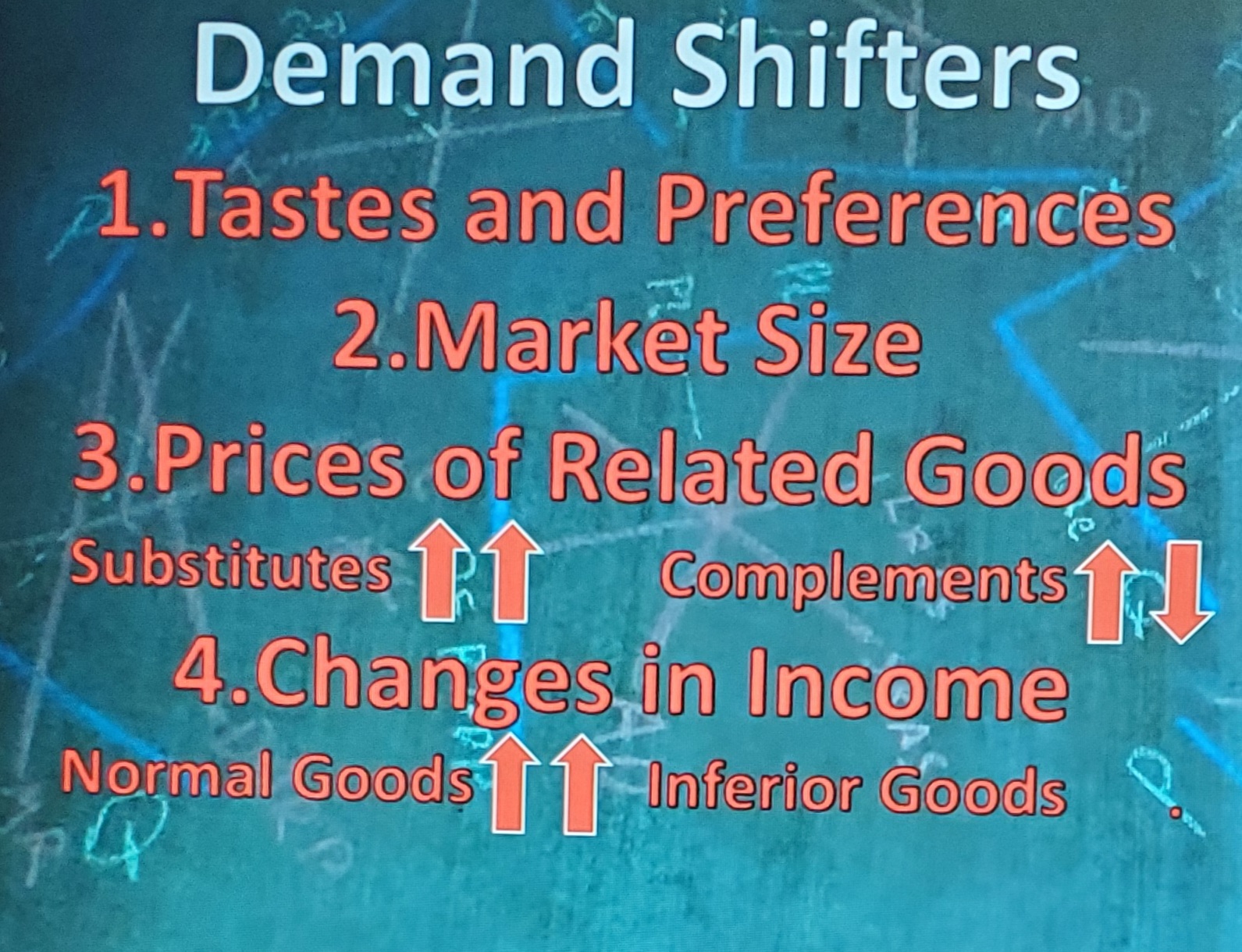

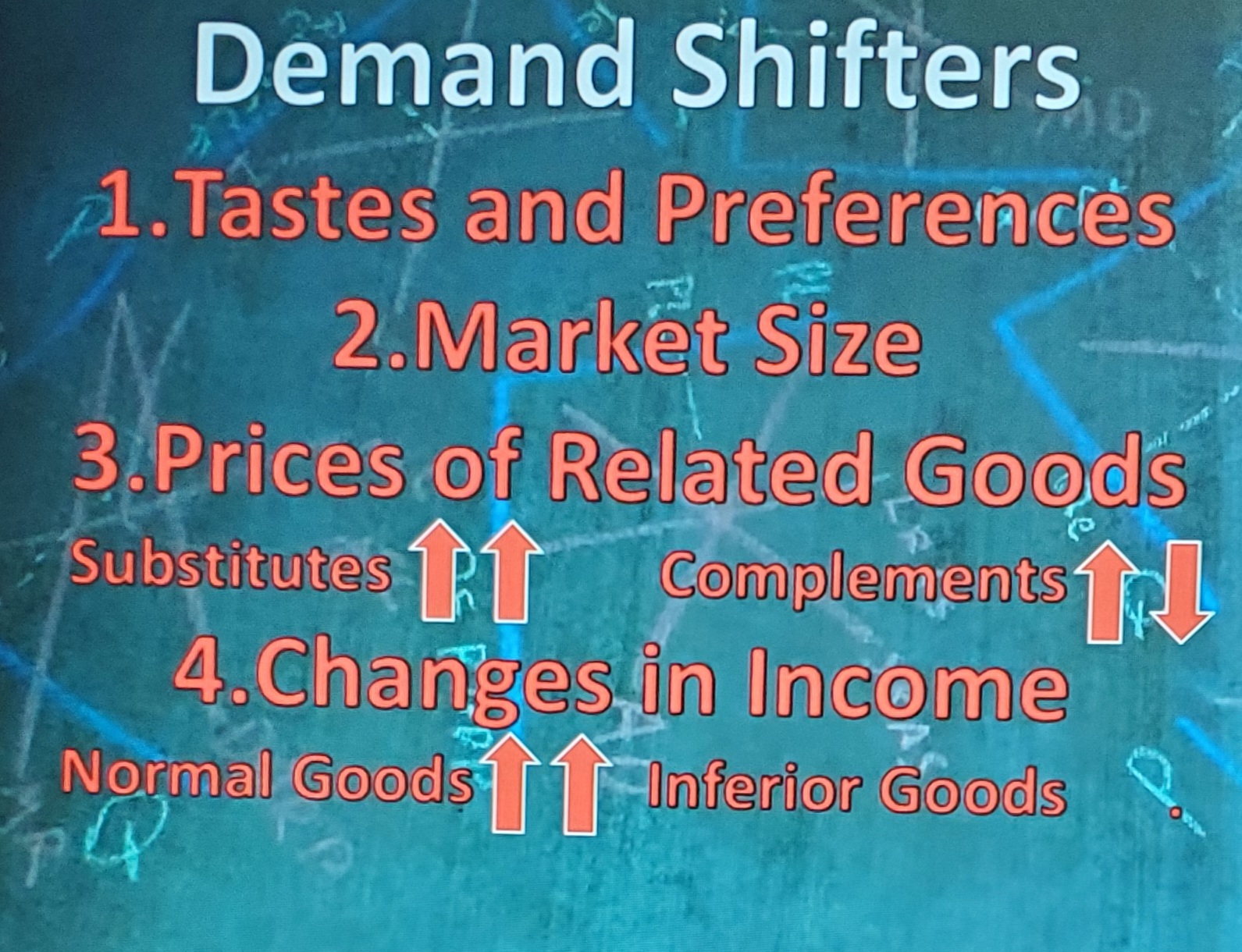

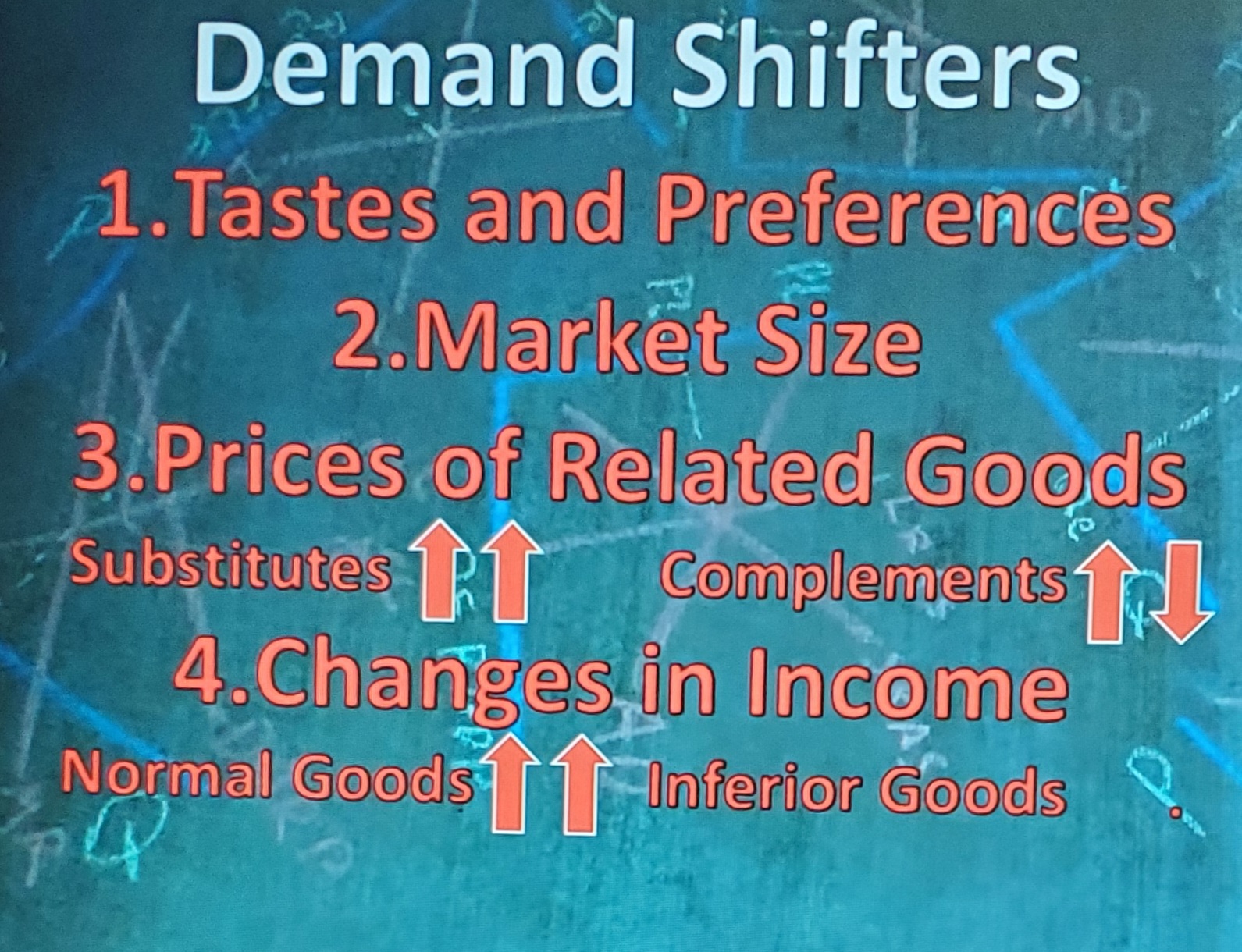

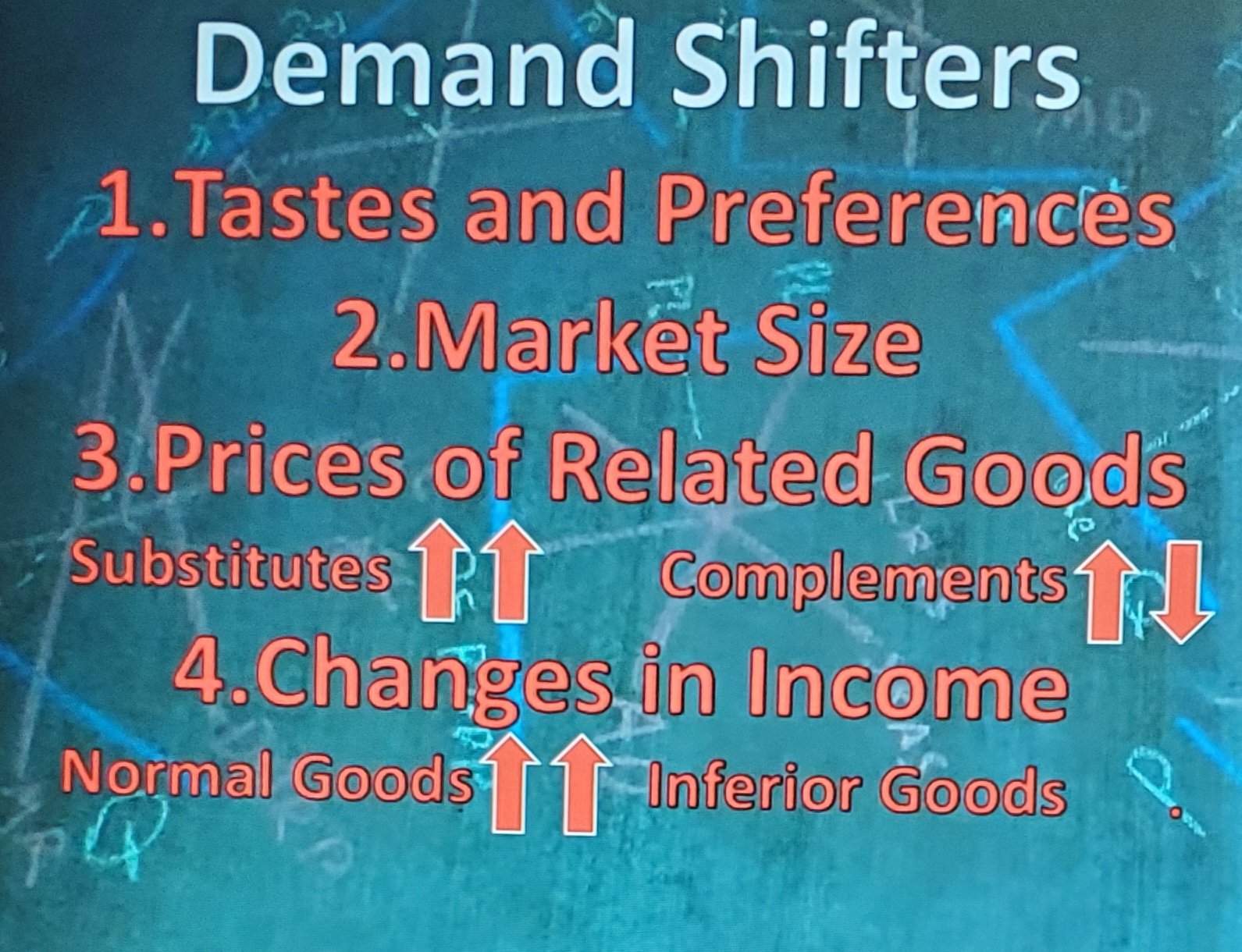

Demand shifters

Tastes and Preferences

Market size (buyers)

Prices of related goods

Changes in income

Expectations (Black friday)

Substitute

When the price of one good goes up, the demand for the substitute of that good goes up

Complements

When the price of one good goes up, the demand for the complement goes down

Normal goods

Increase in consumer income, increase demands and vice versa

Inferior goods

When income rises, demand for inferior good decrease

Demand curve right

Increase in demand (graph)

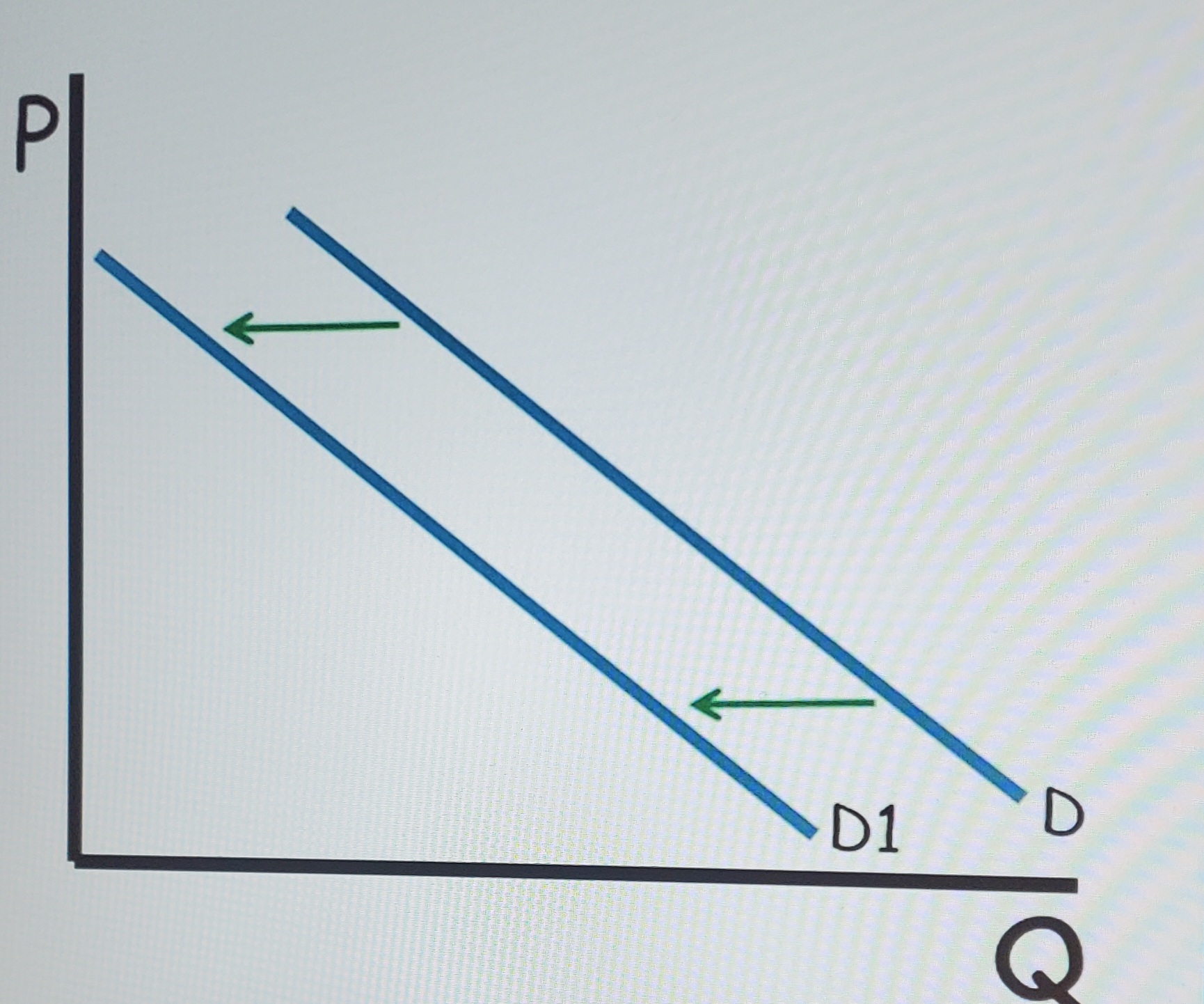

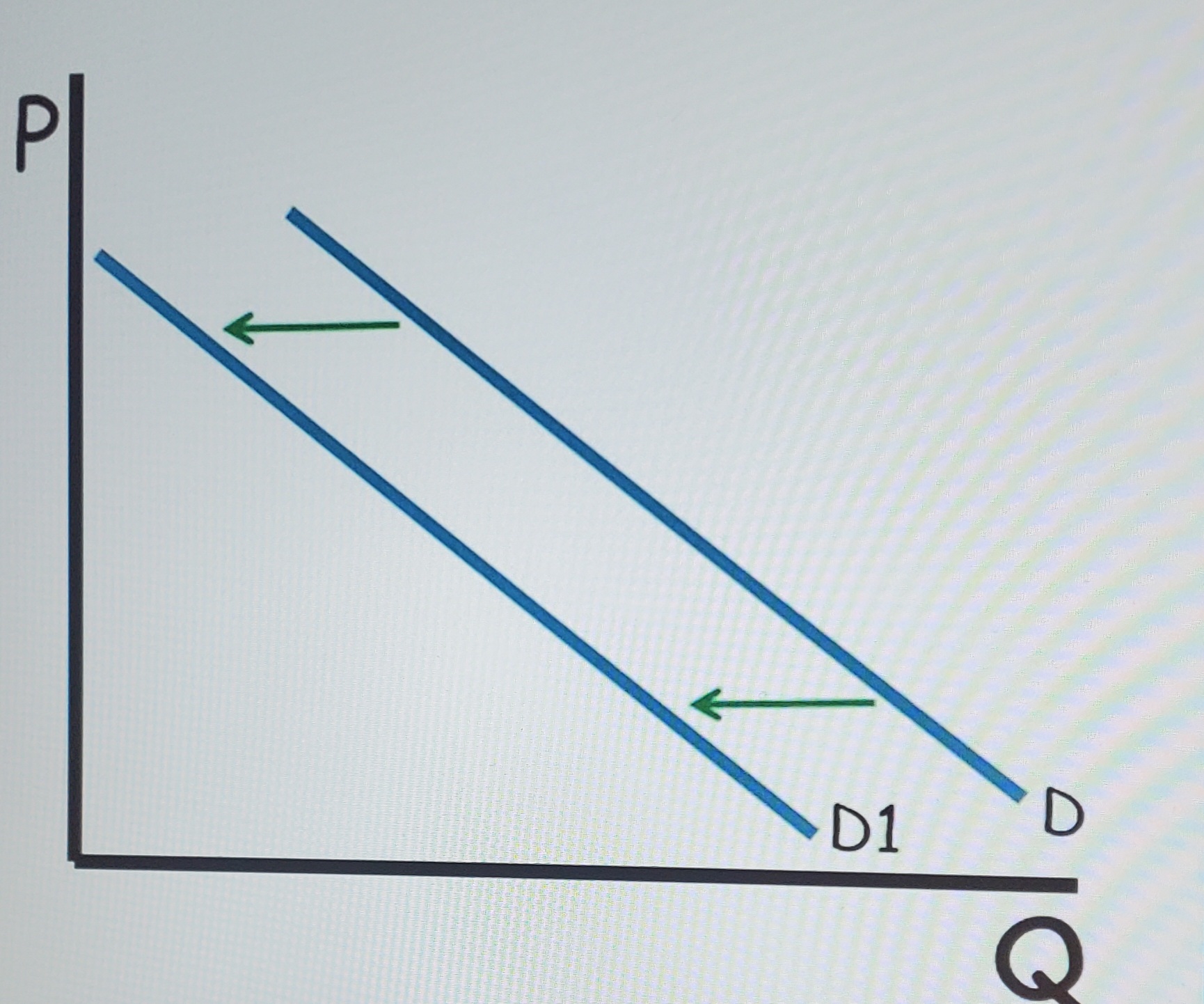

Demand curve left

decrease in demand (graph)

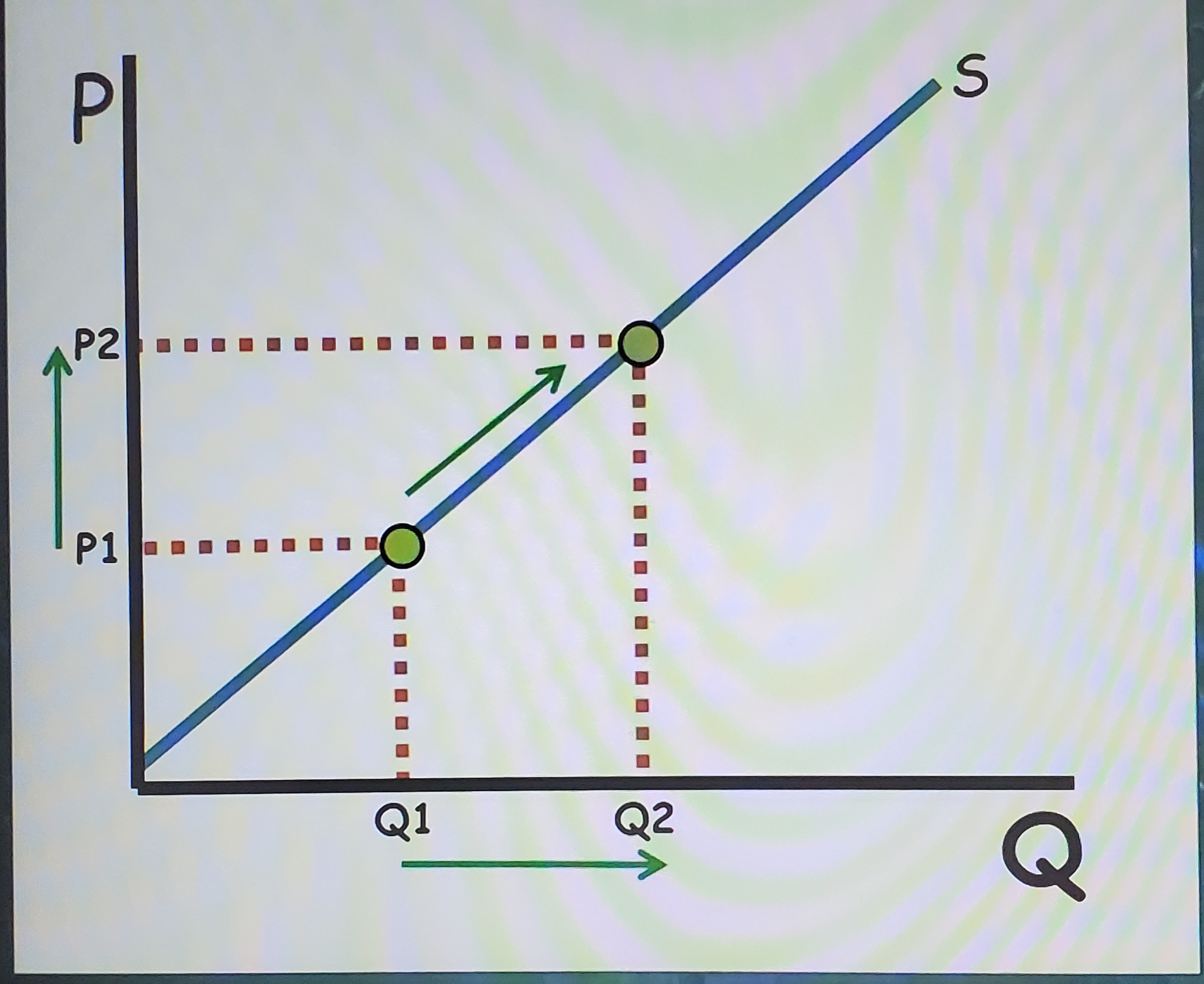

The law of supply

Ceteris Paribus, producers sell more at high prices and less at low prices

Price changes… (Supply)

Quantity (not supply)

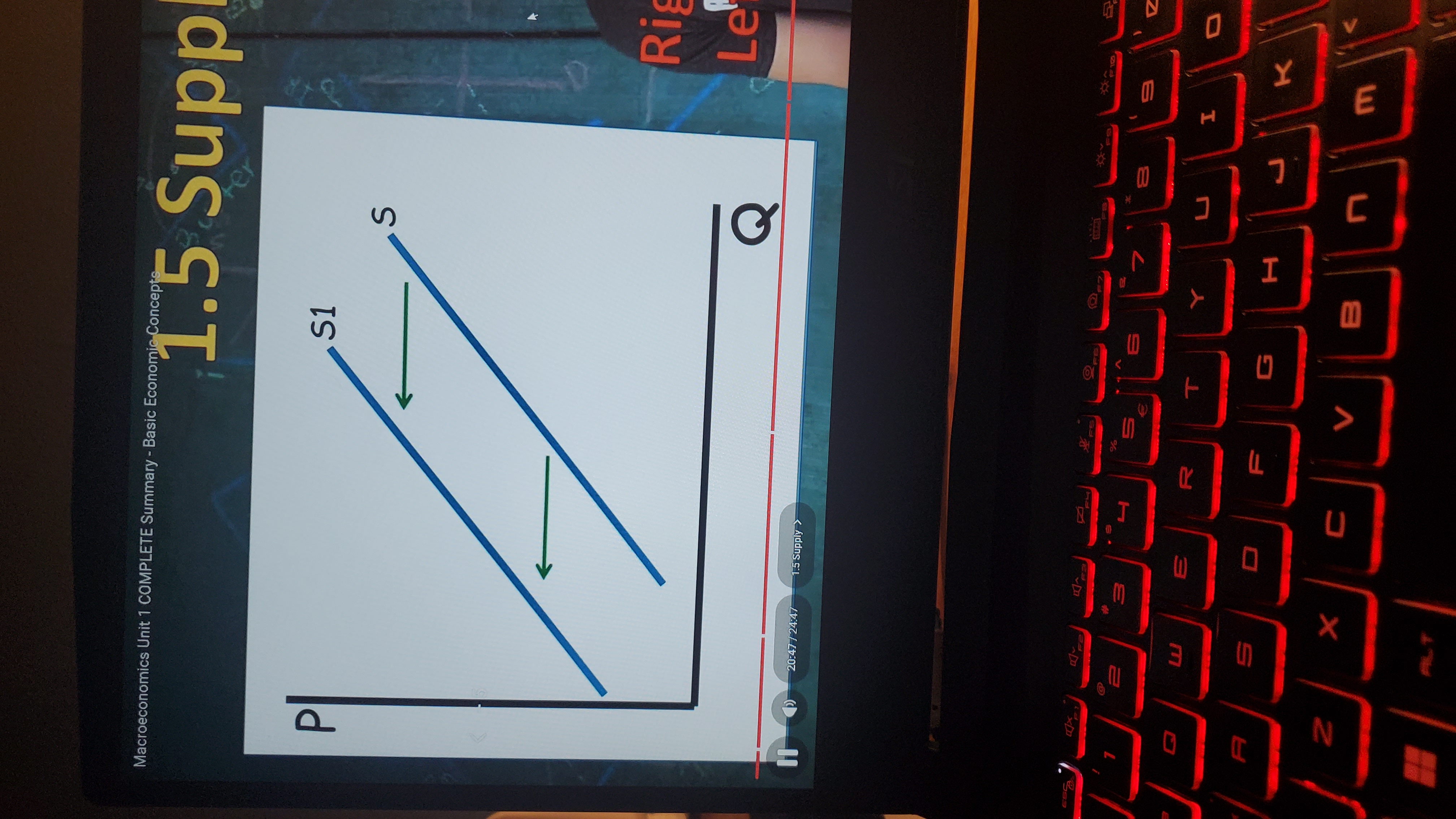

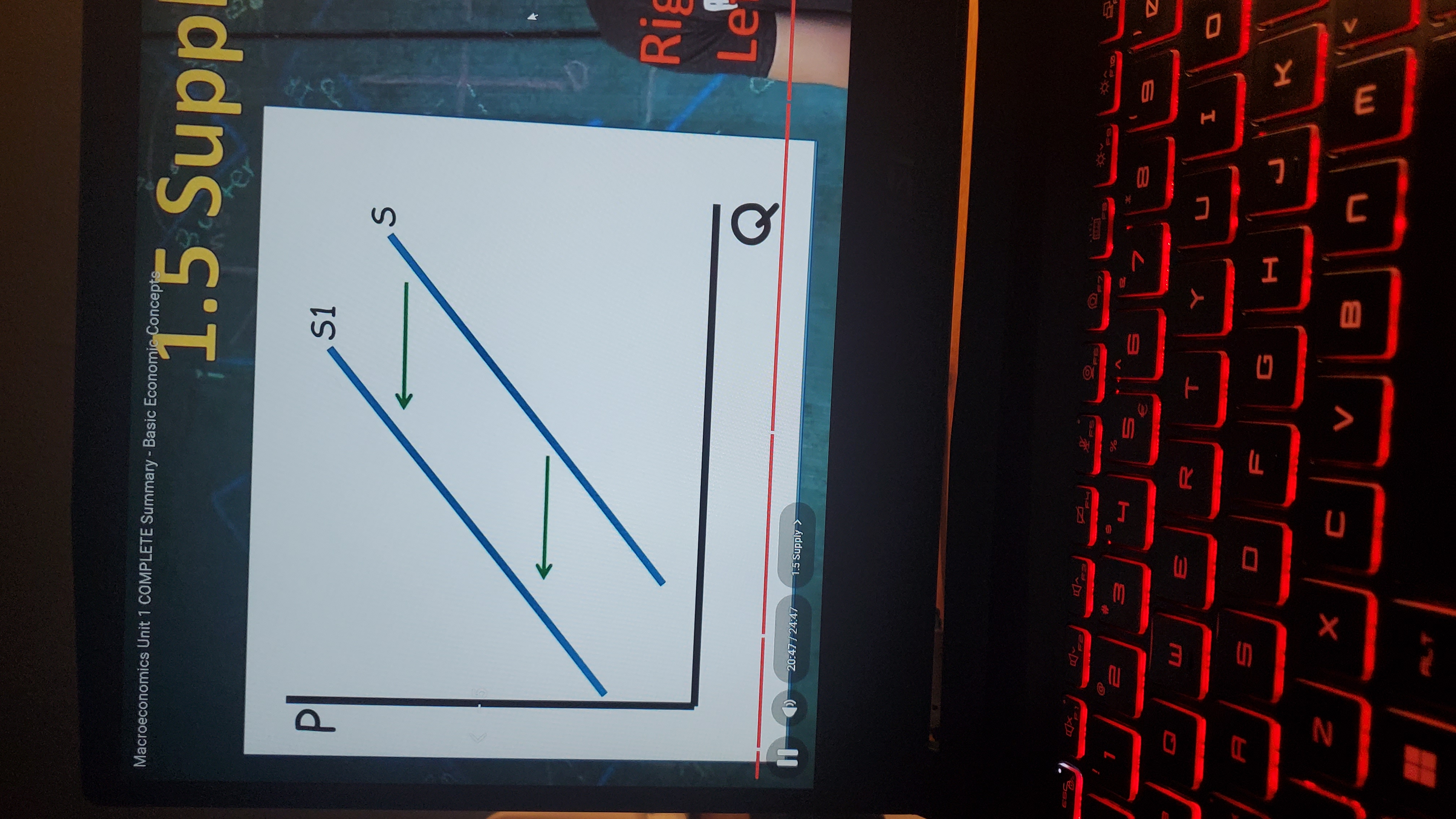

Supply shifters

input prices (if price of resource goes up, supply goes down, vice versa)

Government tools (subsidies)

Number of sellers (competition)

Technology

Prices of other goods (if price of wheat goes up, farmers make more wheat and decrease supply of corn)

Producer Expectations

Supply shift right

increase in supply (graph)

Supply shift left

decrease in supply (graph)

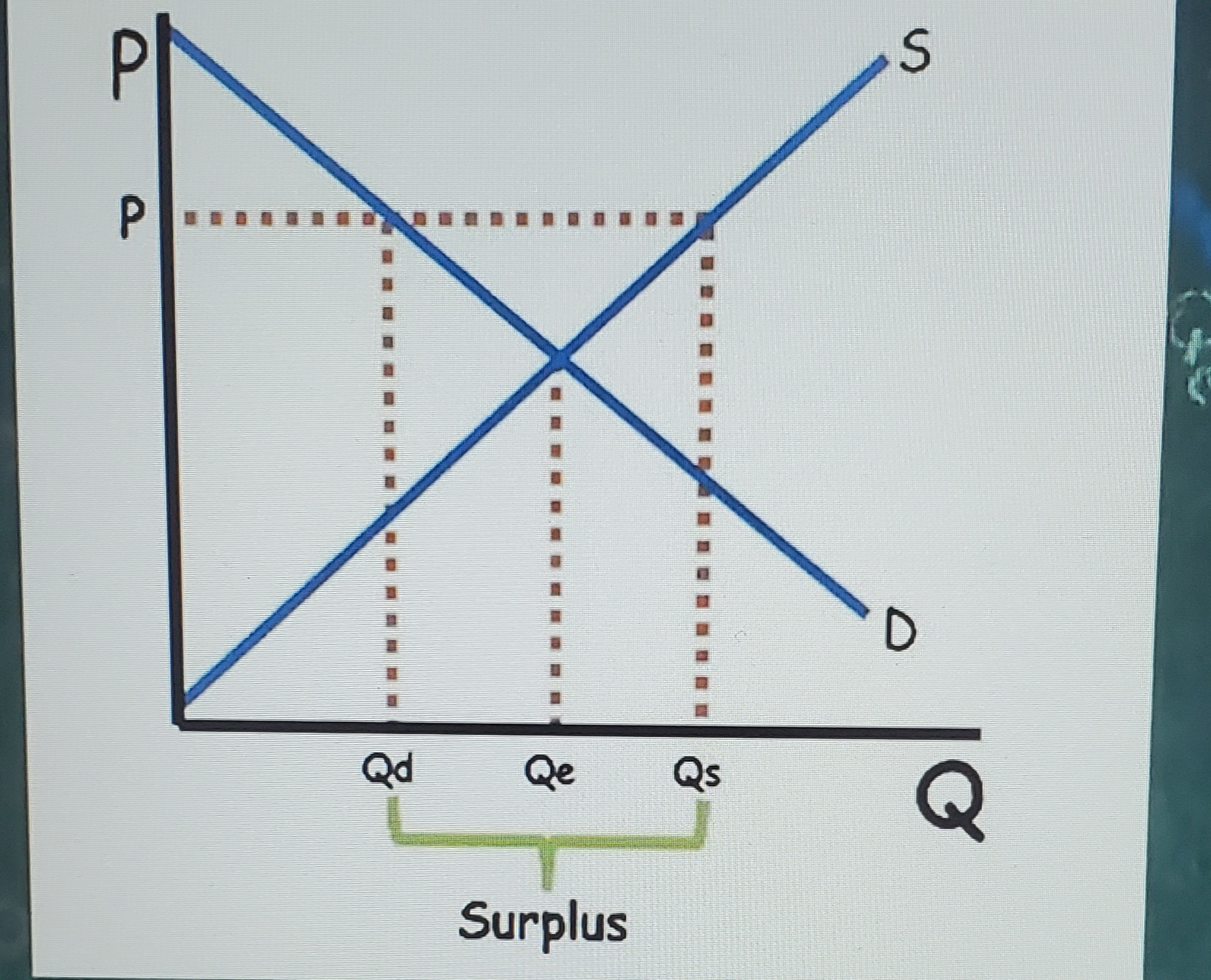

Price above equilibrium

Surplus - Price falls to equilibrium

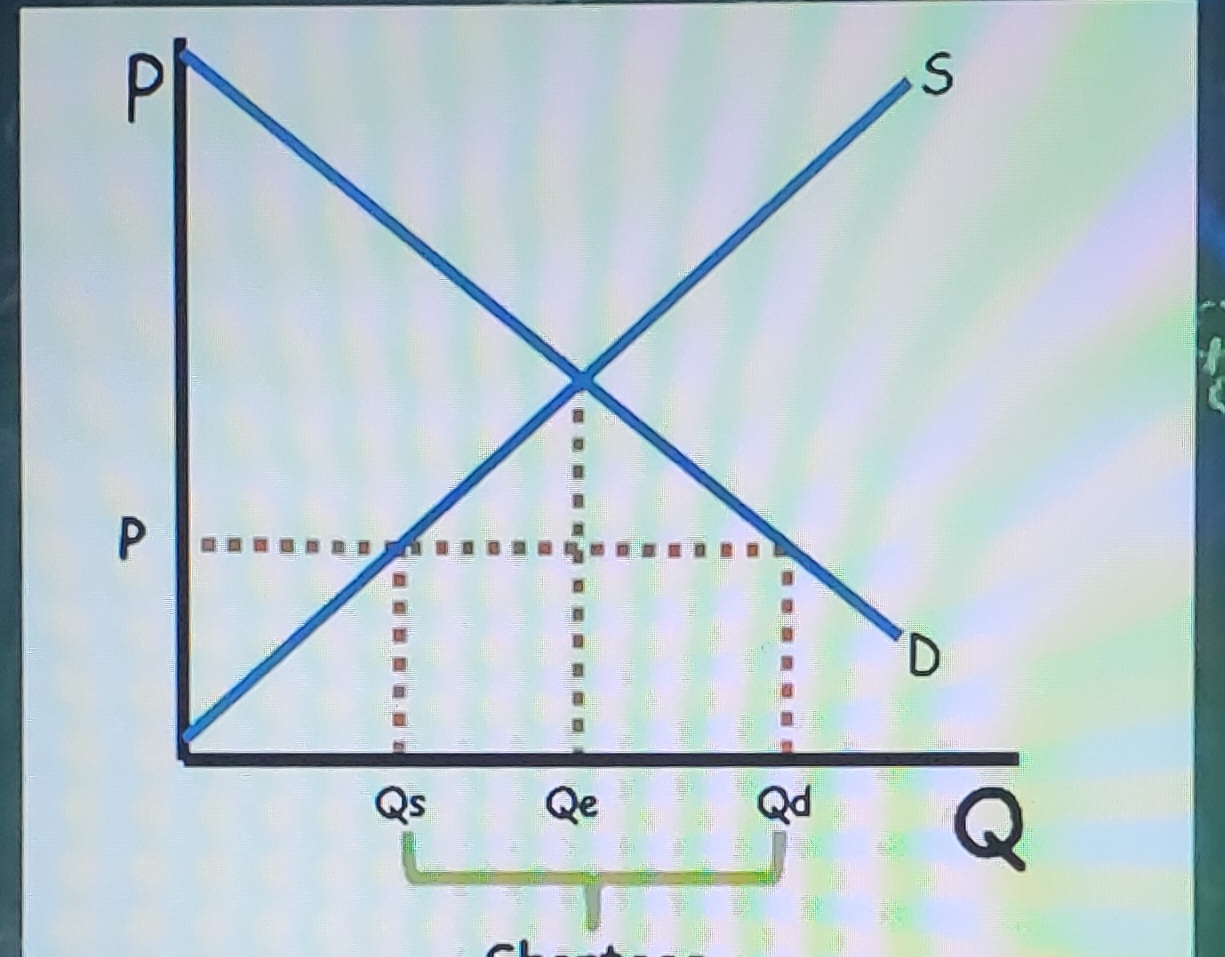

Price below equilibrium

Shortage - price rises to equilibrium

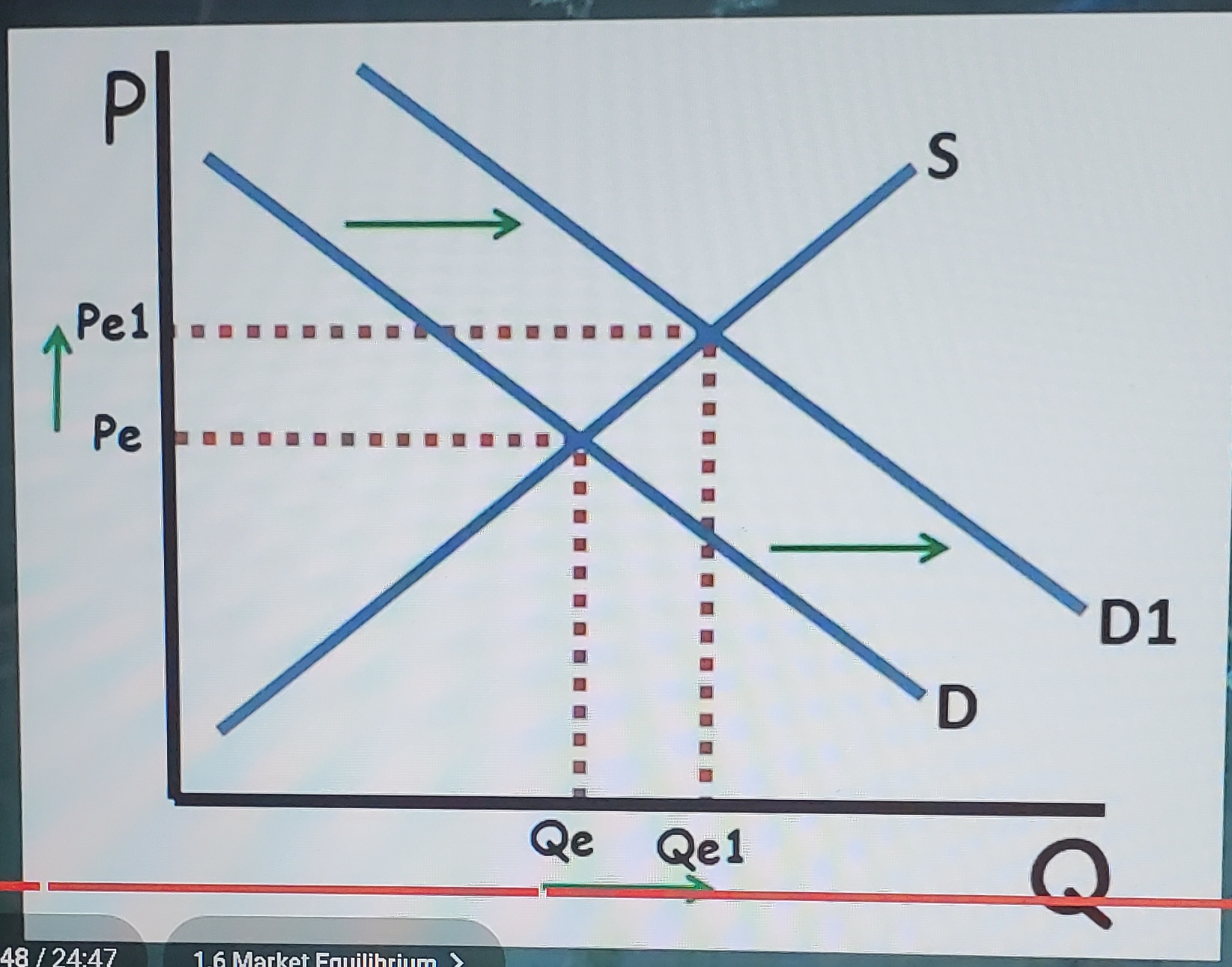

Increase in demand (Changes in Equilibrium)

causes equilibrium price and the equilibrium quantity to increase

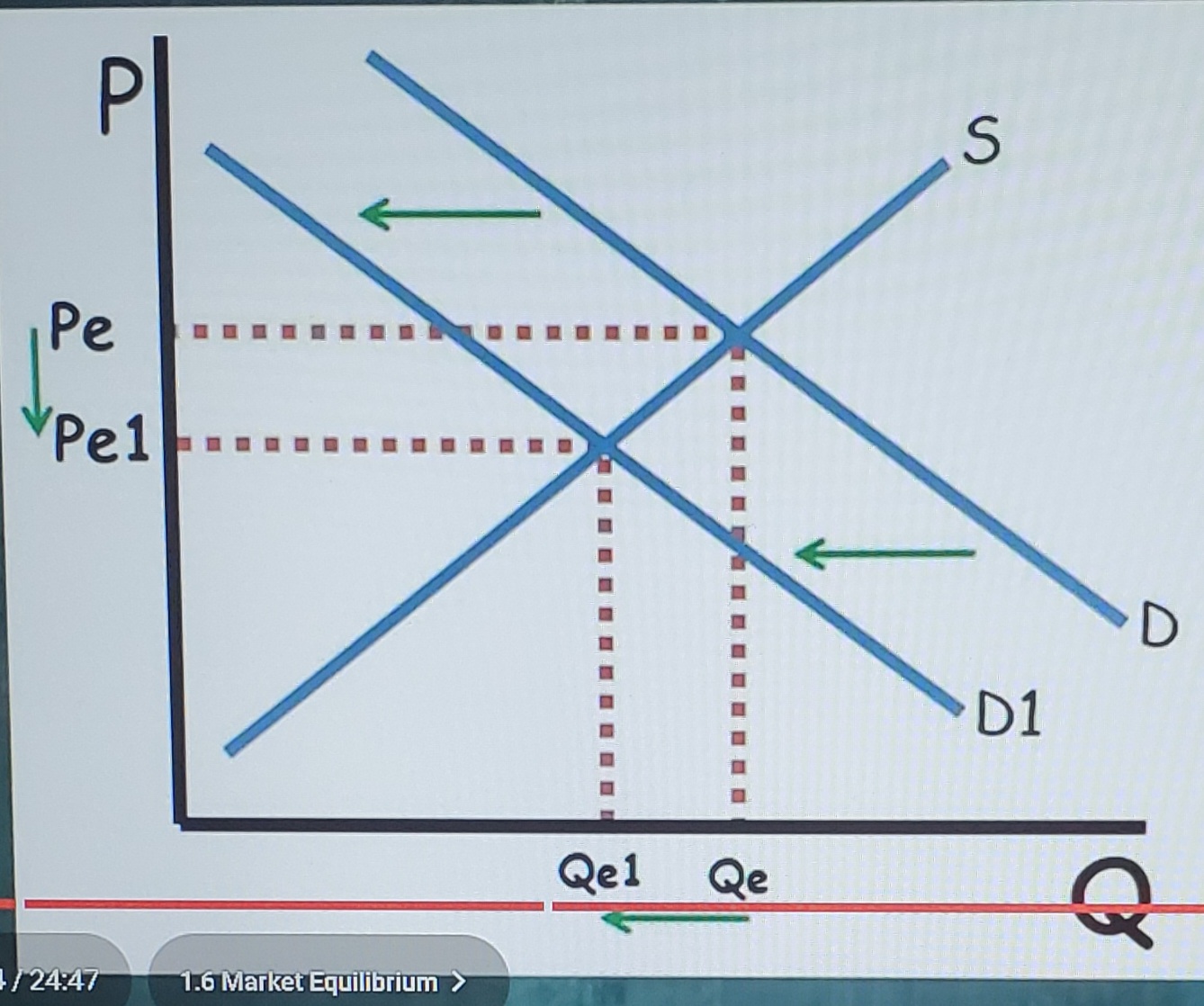

Decrease in demand (Changes in equilibrium)

causes equilibrium price and equilibrium quantity to decrease

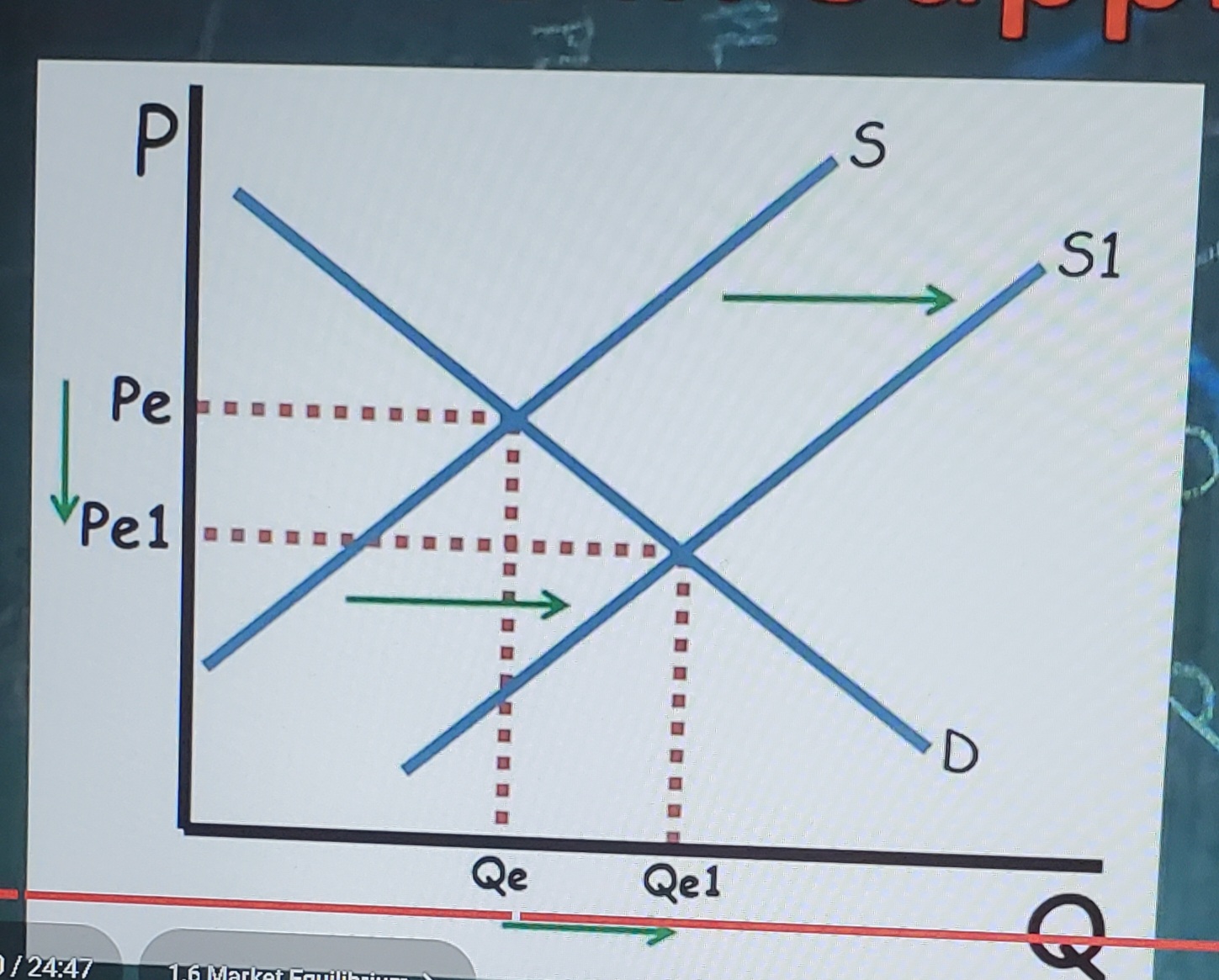

increase in supply (changes in equilibrium)

causes equilibrium price to decrease and equilibrium quantity to increase

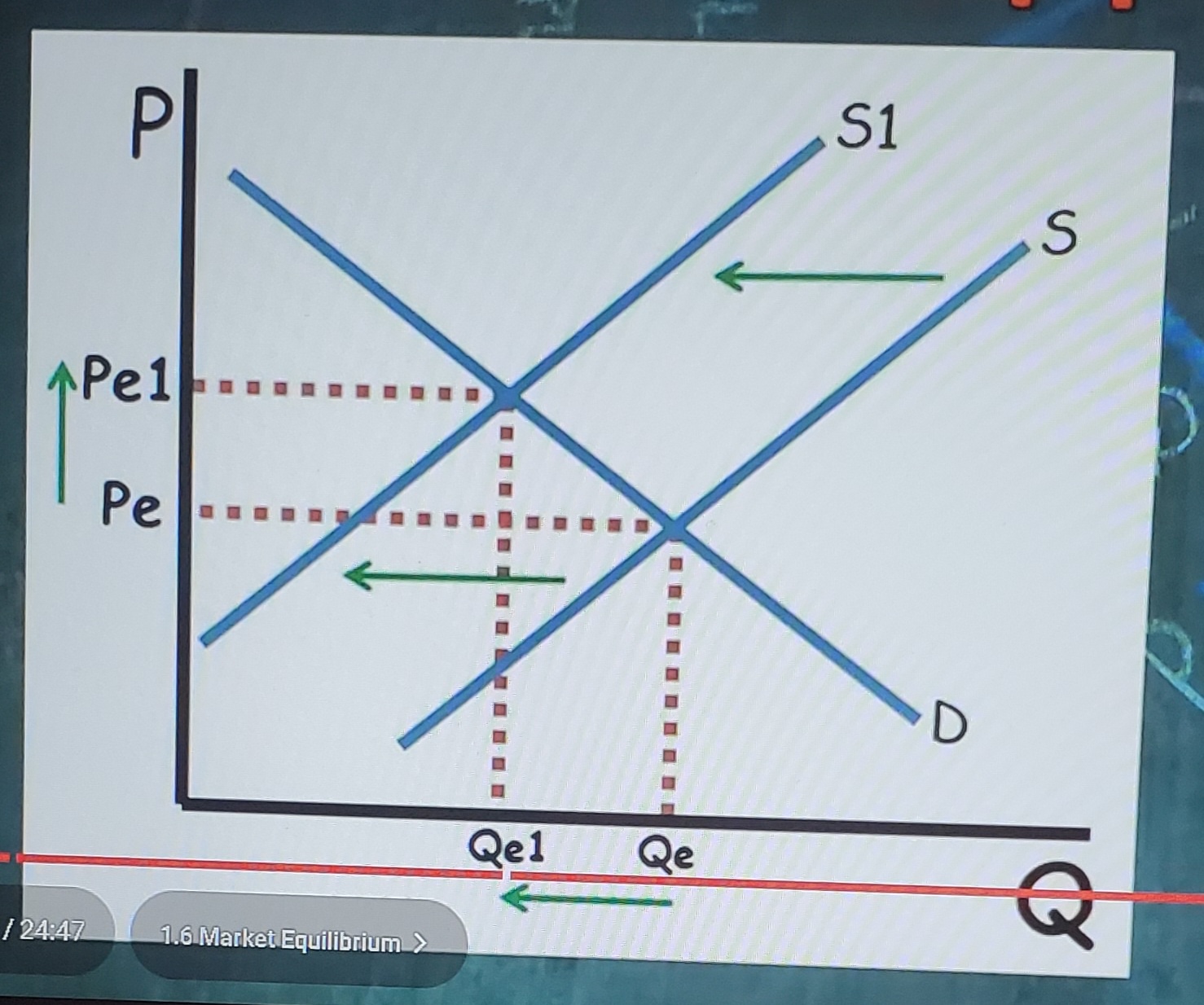

decrease in supply (changes in equilibrium)

causes equilibrium price to increase and equilibrium quantity to decrease