Economics ALL

1/67

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

68 Terms

What is a market

A place or situation where commodities are exchanged

Provides an opportunity for buyers and sellers to interact

What is a market economy

A system where individuals own most of the resources and control the use and price of these resources through voluntary decisions made in the marketplace

Microeconomics focuses on…

the study of a market structure and the efficiency of market equilibrium

What are the 4 structures of the market

Perfect Competition - Many sellers and many buyers

Monopoly - Few sellers and many buyers

Monopsony - Many sellers and few buyers

Bilateral Monopoly - Few sellers and few buyers

What conditions must be met to call a commodity market Perfect Competition

Firms produce a homogeneous commodity (exactly same)

Large number of buyers and sellers (no exploitation)

Perfect information (for both buyers and sellers)

All resources are perfectly mobile (labor and capital)

These conditions are rarely satisfied in any real market.

Provides a base for comparing the performances of various kinds of market imperfections

Forest productions are close to a perfect competition

What is Price Determination?

Prices set by consumers or producers or both. Prices governed by relative power of each group, creating Imperfect Markets

Consumers face price determined by the producer

Consumers select a combination of commodities that would maximize his/her utility from a given budget

Producers also face labor and capital prices

Producers decide how much to produce to maximize their profits based on prices of inputs and consumer prices

What are the 3 kinds of producer powered markets in Imperfect Market Conditions

Few sellers and many buyers

Monopoly (one seller)

Duopoly (two sellers)

Oligopoly (few sellers)

Info on a Monopoly

Single seller with a large number of buyers

No good substitutes for a product in a monopolist

Public utility industries (water, power)

Public monopolies are seen as more efficient by the public, however they are inefficient

Government regulated monopolies often used to achieve social objectives beyond the product they supply

Governments usually act to break up monopolies in the private sector

Monopoly vs Perfect Competition

Monopoly - Prices are higehr, Output is lower. There are welfare implications, and monopolies affects consumers and producers’ welfare

Perfect Competition - Prices are lower, output is higher

Disadvantages of Monopoly

Outputs tend to be lower than the social optimum

Prices tend to be higher than the social optimum

Profits tend to be lower than the social optimum

Efficiency of production is lower due to lack of competitive pressures

Advantages of Monopoly

Resource conservation

Concern for future generations

Concern for research

Technological improvement are possible

Patent and intellectual property protections can create short term monopolies. This is considered an incentive to invest and innovate (some research suggests that this benefit may be over estimated)

What is consumer surplus

The difference between the prices consumers are willing to pay and the actual price

Varies by individual and product

Higher demand products that experience production shortages have higher surplus, although sometimes short lived

In theory, over the long - term consumer surplus tends to get reduced as prices move to equilibrium

Consumers’ surplus of the society is the surplus enjoyed by the entire group

Price gouging and natural disasters

What are secondary markets (Sometimes called Black Market)

(high demand products with production shortages = high surplus) Often in these situations the secondary market takes advantage and reduces the consumer surplus (i.e. ticket scalpers)

What is Price Gouging?

The practice of increasing the price of goods or services to a level much higher than is considered reasonably fair

Most jurisdictions have enacted laws to prevent price gouging

Sellers take advantage of the increase in prices to move their goods into an area experiencing scarcity

However, it also allocates more in-demand resources to an area in need

Higher prices discourage hoarding behavior, as consumers are less likely to stock up on an item whose price is artificially increased by shock, and thus create a more equitable distribution of necessary commodities

Why is Law of Supply & Demand important?

It helps investors, entrepreneurs, and economists understand and predict market conditions

It is the main model of price determination used in economic theory

Price of a commodity is determined by the interaction of supply and demand in a market

What is Demand?

The desire, ability, and willingness to buy a product or service

What is a demand schedule?

Is a listing that shows the quantity demanded at all prices

As price increases, quantity demanded _____

Decreases

What causes a shift in demand?

Non - price determinants

What are the 6 non price determinants of demand?

Buyer’s income

Price of substitutes

Market size (immigration)

Consumer tastes (popularity

Consumer expectations

Complement goods (the use of one product increases the use of another. Ex. phone and cellular providers)

What is Demand Elasticity?

The extent to which changes in price cause changes in quantity demanded

What is Elastic and Inelastic demand

Elastic - Occurs when a relatively small change in price causes a relatively large change in the quantity demanded

Inelastic Demand - Occurs when a change in price causes a relatively smaller change in the quantity demanded

5 Factors that determine Elasticity of Demand

Substitutes

Percentage of income

Necessity

Duration

Breadth of definition

3 questions for estimating elasticity of demand

Can the purchase be delayed?

Are there adequate substitutes?

Does purchase use a large portion of income?

2 or more yes = elastic

2 or more no = inelastic

What is supply

The desire, ability, and willingness to offer products for sale

Anyone who offers an economic product for sale is a supplier

When you work at a job, you are offering your services for sale. Your economic product is labor, and you would probably supply more for a higher wage

Law of Supply - as price increases, quantity supplied _____

Increases

What changes the quantity supplied?

Non price determinants of supply

What are the 7 non price determinants of supply

Number of products

Input costs

Labor productivity (skilled workers more productive) (taxes or subsidies) affect cost

Technology

Government action

Number of sellers

Producer expectations (change in production based on whether they believe price will go up or down)

What is market equilibrium, what is the equation?

Situations where prices are relatively stable and the quantity of goods or services supplied is equal to the quantity demanded

QS = QD

What is Equilibrium Price

The price that “clears the market”. No shortage or surplus

What is Surplus?

Where the quantity supplied is greater than the quantity demanded at a given price

QS > QD

P decreases

If there is a surplus, prices generally fall

What is a Shortage

Where the quantity demanded is greater than the quantity supplied

QD > QS

P increases

How does supply and demand reflect in forestry

Boom and Bust cycles of highs and low prices

Forestry is highly sensitive to market fluctuations

Demand for forest products can vary significantly based on economic conditions, housing markets, and global trade dynamics

Forest products are commodities, subject to price volatility

When demand surges, prices rise, leading to a boom

Oversupply or reduced demand can trigger a bust

Revenue = Sales price * number of units sold

Types of revenue

Sales revenue - Generated from sales

Service revenue - Generated from providing services

Interest revenue - Generated from lending money

Rental revenue - Generated from renting assets

Royalties revenue - Generated from licensing intellectual property

Importance of revenue

Measure of a firm’s financial performance

Used to calculate other important financial metrics, such as profitability, revenue growth, and revenue per employee

What are the limitations of revenue

Not a complete measure of a firm’s financial performance. Does not account for expenses that a firm incurs in generating revenue.

Revenue does not account for changes in inventory levels or other balance sheet items

Operating income is revenue less or more than operating expenses?

less

What is Non operating income

Infrequent or non recurring income derived from secondary sources

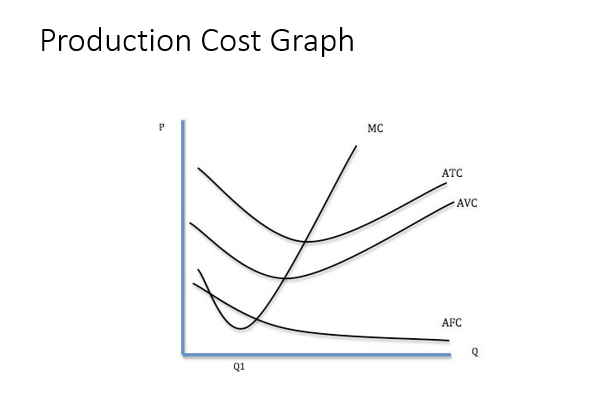

What are production costs

Reflect all costs a business pays associated with manufacturing or providing a service

Ex. Labor, raw materials, overhead, consumable manufacturing supplies

Total production cost = total direct materials + labor costs + manufacturing overhead costs

Examples of Direct and Indirect costs

Direct - Materials like plastic, metal, worker’s salaries

Indirect - Overhead, rent, utilities

What is marginal cost of production

The total cost to produce one additional unit

Production costs VS Manufacturing costs

Production costs includes both direct and indirect costs, refers to all expenses associated with a business

Manufacturing costs include only direct costs

Examples of a fixed cost

Equipment rental, property tax, office space rent, employee’s salaries and benefits, insurance,

Examples of variable costs

Cost of purchasing materials, hourly employees, utility bills, advertising,

Quantity produced

Determining the number of units a company is producing is also necessary for the cost per unit calculation

What are economies of scale

when the average costs per unit of output decrease as the volume of the output manufactures or sells increases

It cam provide a competitive edge with a cost advantage

What is Survivor Technique

Involves identifying the most efficient firms in a given industry and using their performance as a benchmark to estimate the production frontier

“survivors” because a firm survived the industry by bring more efficient than competitors

What is Size Efficiency in relation to Survivor Technique

Refers to when a firm is able to achieve the maximum possible level of output given its size. Measures how well a firm is able to utilize its scale of production to achieve efficient levels of input

An economic profit or loss id the difference between the __ __ _ _ __ _ _ ___ and the __ _ _ __ and any ____ ____

An economic profit is the difference between the revenue received from the sale of an output and the cost of all inputs used and any opportunity costs

What are opportunity costs

Represent the benefits an individual, investor, or business misses out on when choosing one alternative or another

Opportunity cost calculation

= FO - CO

FO = Return on best foregone option

CO = Return on chosen option

What is time value of money also known as?

Present Discounted Value

What is the idea of Time Value of Money

Money available at the present time is worth more than the identical amount in the future due to potential earning capacity

Present Value Formula

PV = FV / (1+I) ^N

PV = present value

FV = the future value

I = Required return

N = the number of time periods before receiving the money

To determine the current value of future cash flow, evaluate… (2)

Time value of money

Uncertainty risk

How do you determine discount rate (the current value of future cash flow)?

Evaluate the time value of money and the uncertainty risk

What changes TVM? (time value of money)

Inflation causing cash flow of tomorrow to not be worth as much as cash flow today

All prediction models have a level of ________ to their predictions

Uncertainty

Lower discount rate would imply _____ uncertainty the _____ the present value of future cash flow (ans. lower or higher)

Discount rate would imply LOWER uncertainty the HIGHER the present value

What is Net Present Value? What is it used for?

The difference between the present value of cash inflows and the present value of cash outflows over a period of time.

It is used in capital budgeting and investment planning to analyze the profitability of a projected investment or project.

What are Cash Flow Projections?

Cash produced by a company’s business operations after paying for operating expenses and capital expenditures

What is Discount Rate?

The cost of capital (dept and equity) for the business. This rate, which acts like an interest rate on future cash inflows, is used to convert them into current dollar equivalents

What is Terminal Value?

The value of an investment at the end of the projection period

What is Production Function?

The relationship between the flow of quantities of various inputs and the maximum flow of quantity of output

Gives information about increasing or decreasing returns to scale and the marginal products of labor and capital

5