ACIS2115 CH9-11

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

Current liability

Due within 1 year or the operating cycle

Examples:

Accounts Payable

Sales Taxes Payable

Wages Payable

Notes Payable due soon

Unearned Revenue

Warranty Liability

Payroll Tax Payable

Long-term liability

Due after 1 year or the operating cycle

Examples of:

Long-term Notes Payable

Bonds Payable

Long-term Lease Liabilities

Short-term notes payable

A note payable is a written promise to pay a certain amount on a future date within one year.

Notes payable usually include interest.

Interest formula

Principal × Rate × Time = Interest

Known liabilities

are liabilities where the amount and timing are mostly known.

Examples:

Accounts Payable

Sales Taxes Payable

Unearned Revenue

Notes Payable

Payroll Liabilities

Warranty Liabilities

Net pay formula

Net Pay = Gross Pay - Deductions

warranty

is a company’s promise to repair or replace a product if something goes wrong.

contingent liability

is a possible liability that depends on a future event.

Example: A company is being sued.

The company might have to pay, but it depends on the outcome of the lawsuit.

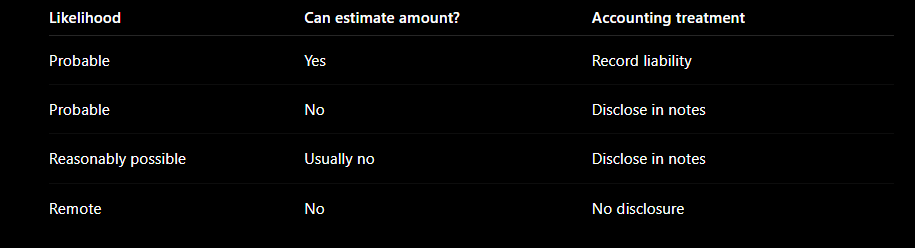

Accounting treatment depends on two things:

How likely the loss is.

Whether the amount can be estimated.

Rules for contingent liabilities

Simple version:

Probable and estimable = record it

Reasonably possible = disclose it

Remote = ignore it

installment note

is a liability that requires the borrower to make a series of payments over time.

Each payment usually includes: Interest expense + reduction of the note payable

Example: A car loan or mortgage is like an installment note because you pay it off in repeated payments.

Par

means the bond’s face value — the amount the company promises to pay back when the bond matures.

Contract rate / Stated rate / Coupon rate

is the interest rate printed on the bond.

Market rate

Interest rate investors currently want in the market

bond

is a company’s written promise to pay back borrowed money plus interest.

Companies issue bonds when they need a lot of money for big projects.

Maturity date

Date the bond principal is repaid

Bond indenture

Legal contract between issuer and bondholders

Bond Interest Payment =

Par Value × Contract Rate × Time

Example:

Par value = $100,000

Contract rate = 8%

Interest is paid every 6 months.

Semiannual interest:

$100,000 × 8% × 1/2 = $4,000

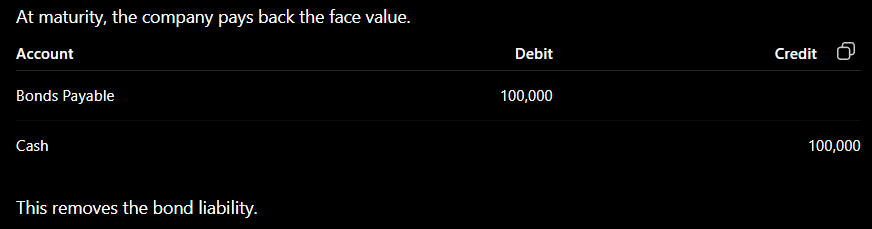

Paying bonds at maturity

At maturity, the company pays back the face value.

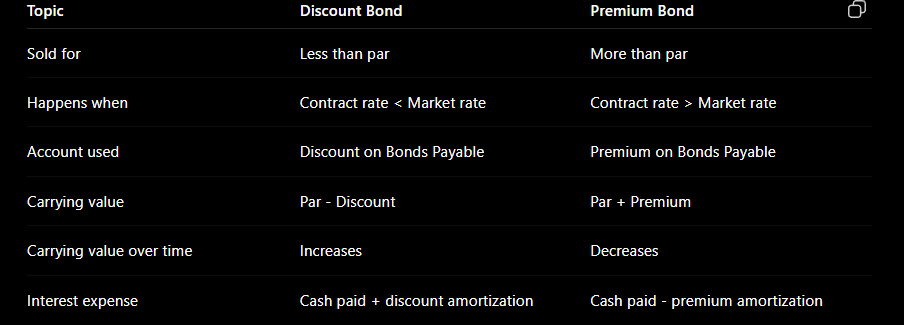

Bonds at discount or premium

A bond does not always sell for exactly face value.

It depends on the contract rate compared to the market rate.

Situation | Result |

|---|---|

Contract rate = Market rate | Bond sells at par |

Contract rate < Market rate | Bond sells at discount |

Contract rate > Market rate | Bond sells at premium |

Simple meaning:

If the bond pays less interest than investors want, it sells for less.

If the bond pays more interest than investors want, it sells for more.

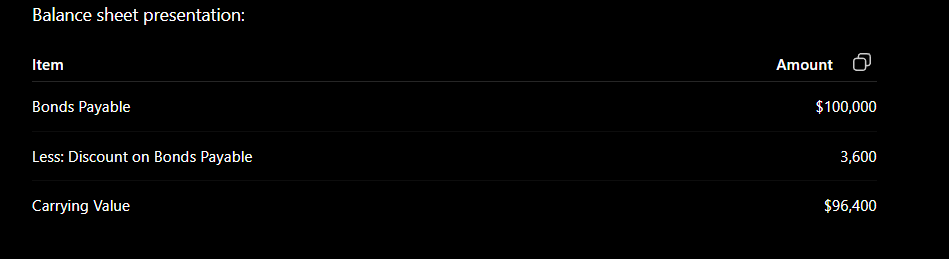

Discount on Bonds Payable

is a contra-liability account.

That means it reduces the carrying value of the bonds.

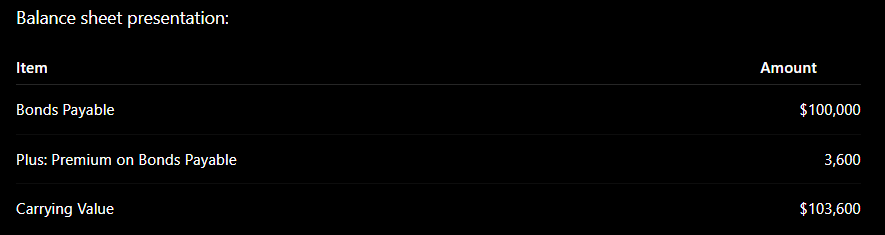

Premium on Bonds Payable

is an adjunct-liability account.

That means it increases the carrying value of the bonds.

Discount vs. premium comparison

Easy memory:

Discount adds to interest expense.

Premium subtracts from interest expense.

Straight-line amortization

Discount or Premium ÷ Number of Interest Periods = Amortization per Period