Unit 1: Basic Economic Concepts

1/68

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

69 Terms

Equilibrium

When supply = demand, there is equilibrium in the market

Equilibrium creates a single price and quantity for a good/service for that market

Requirements for a supply & demand graph

Label ACES

Axis

Curves

Equilibrium

Shifts

Changes in Equilibrium

When supply or demand changes, the equilibrium price & quantity change

Increase in Demand graph

D →

P increase

Q increase

Decrease in Demand graph

D ←

P decrease

Q decrease

Increase in Supply graph

S →

P decrease

Q increase

Decrease in Supply graph

S ←

P increase

Q decrease

Simultaneous Increase in Supply and Demand

P ? indeterminate

Q increase

Simultaneous Decrease in Supply and Demand

P ? indeterminate

Q decrease

Simultaneous Supply decrease & Demand increase

P increase

Q ? indeterminate

Simultaneous Supply increase & Demand decrease

P decrease

Q ? indeterminate

Market Disequilibrium

Surplus (Price Floor)

Shortage (Price Ceiling)

Surplus

Price is TOO high, so consumers’ demand is lower than supply

Shortage

Price is TOO low, so consumers’ demand is higher than supply

Price Floor

Minimum price for a good/service determined outside of the market (typically by govt.)

ex. minimum wage

raises the bar

Price Ceiling

Maximum price for a good/service or resource determined outside of the market

like a lid

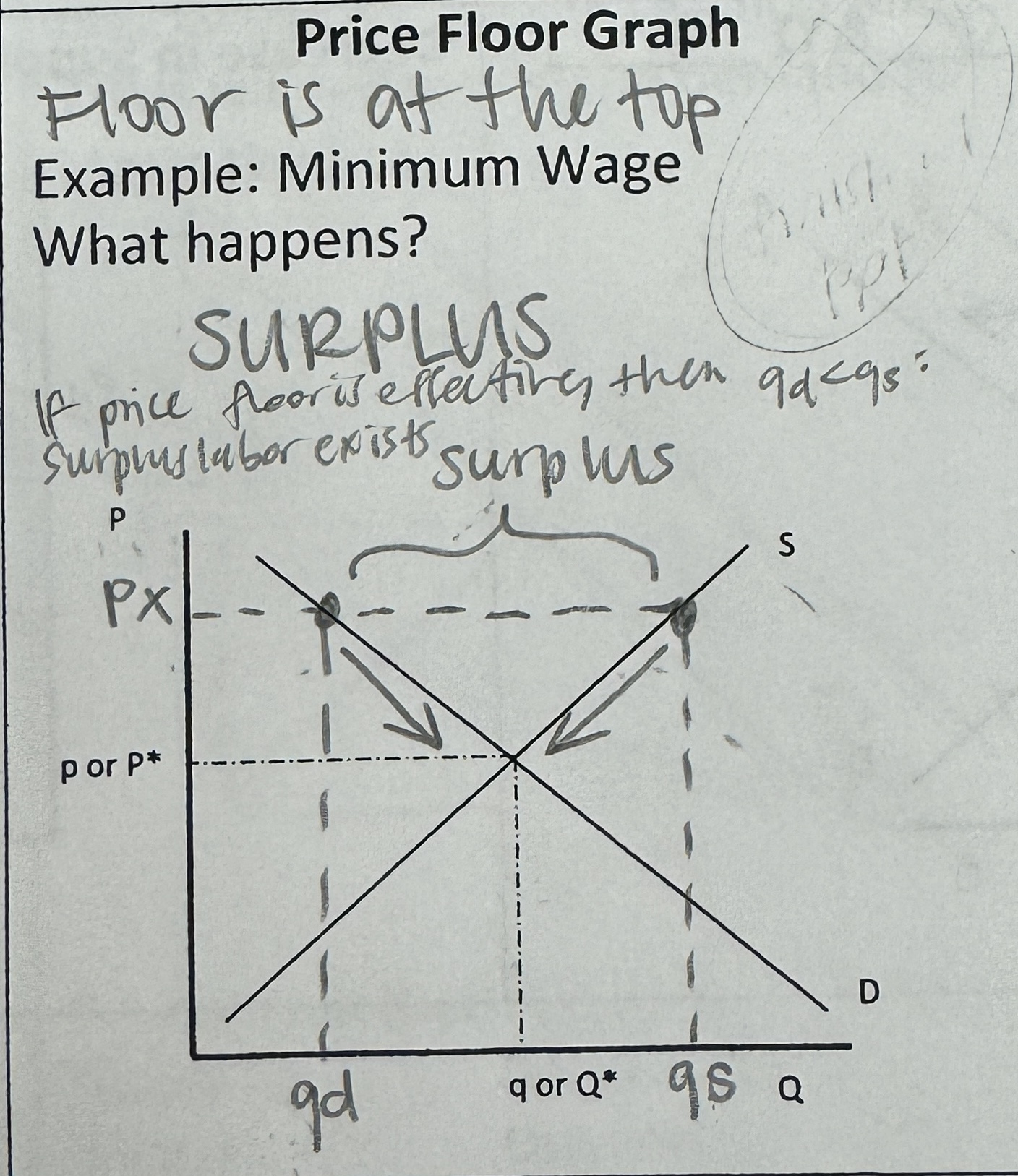

Price Floor Graph

=SURPLUS of goods/services

(Price, px, below Equilibrium price, pe)

Floor is at the top

ex. Minimum Wage - meant to increase standard of living but creates a labor surplus because companies can’t have as many employees

if price floor is effective, then qd < qs : surplus labor exists

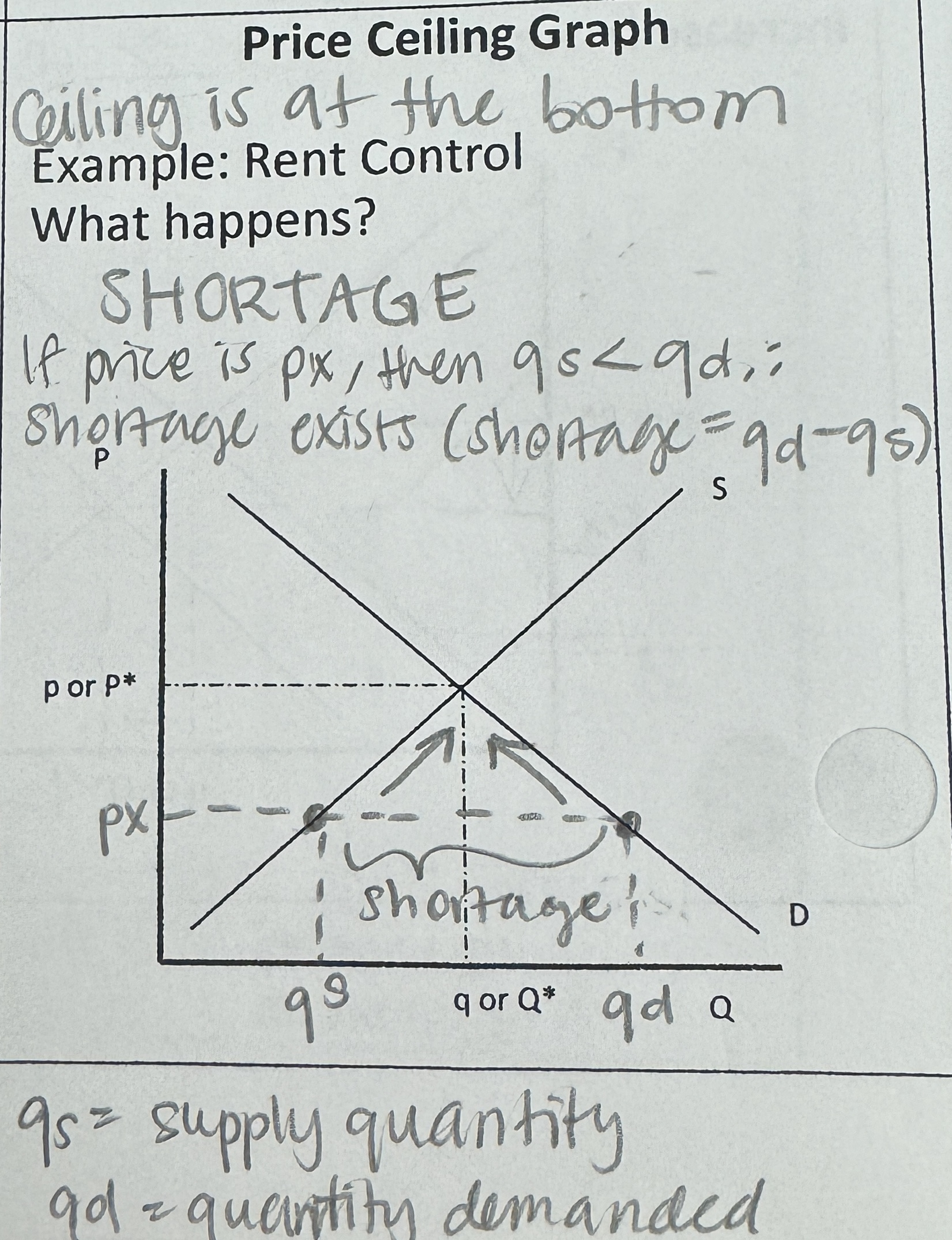

Price Ceiling Graph

= SHORTAGE of goods/services

(Price, px, below Equilibrium price, pe)

Ceiling is at the bottom

Ex. Rent control

if price is px, then qs < qd : shortage exists (shortage = qd - qs)

Market

a group of buyers and sellers of a particular product

Competitive Market

a market with many buyers and sellers, each having a negligible impact on price

Perfectly Competitive Market

All goods are exactly the same (quality)

Large number of buyers and sellers so that no one (individual) can affect market price

Demand

Consumers’ willingness and ability to buy an item at a given price

“How much we want something” - it is important to understand that this does not refer to an numerical amount but instead to a behavior

Law of Demand

The price of an item determines the quantity demanded

Therefore, the price of a good/service is inversely related with the quantity demanded

Lower price = more quantity demanded

Higher price = less quantity demanded

**Changing the price of a good does NOT change demand for that good, it merely changes the quantity demanded (movement along the curve)

Changes in Demand (Shifts of Demand Curve)

Increase in Demand = More quantity demanded at all prices = Demand Curve shifts →

Decrease in Demand = Less quantity demanded at all prices = Demand Curve shifts ←

Determinants of Demand

TRIPE

Tastes & Preferences

Related Goods

complements

substitutes

Income of Consumers

Population

Expectations of Future Price Changes

Tastes & Preferences

Preferences and tastes are affected by advertising, trends, health considerations, etc.

Related Goods

Complements - goods/services used with another

Substitutes - goods/services used instead of other goods/services

Income of Consumers

Increased income = more demand for normal goods

Decreased income = less demand for normal goods

Demand for inferior goods increases as income decreases

knock-offs, cheap fast food, ramen noodles

Population

More population = more demand

Expectations of Future Price Changes

If consumers expect prices to rise in the future, then demand increases now and vice versa.

Supply

producers’ willingness and ability to sell (supply) a good/service

Just like demand, supply is not an amount but a behavior

Specifically, “supply” is not the supply of something, but the willingness and ability to sell (their desire to sell)

Law of Supply

The price of an item determines the quantity supplied

The lower the price the lower the quantity supplied and vice versa

Therefore, the price of a good/service is directly related with the quantity supplied

**Changing the price of a good changesthe quantity supplied of that good, not supply.

Changes in Supply

Increase in Supply = More quantity supplied at all prices = Supply curve shifts →

Decrease in Supply = Less quantity supplied at all prices = Supply curve shifts ←

Determinants of Supply

ACEJIP

Alternative goods in supply

Competition

Expectations

Joint-Supply on market

Input Costs

Phenomenon

Alternative goods in supply

goods that a supplier can make that require similar resources

resources are limited so suppliers have to pick what to make & transfer resources b/w goods they make

Competition

Number of producers in the market

Fewer producers = less supply

More producers = more supply

(like population in TRIPE)

Expectations

If producers expect prices to rise in the future, then they supply less now so that they can sell their good/service at the future higher price.

Joint-Supply on Market

Products that yield multiple outputs (products)

ex. cows (leather, milk, beef) - if there are more cows, then supply of any products made by cows increase

Input Costs

The more expensive it is to make a product, the less of the product that can be made. A change to any of the following would impact the cost of production:

Raw materials, technology, productivity (efficiency gain/losses), Government policies (taxes, regulations)

(very common scenario)

Phenomenon

Certain events can cause a sharp decline in supply such as: natural disasters, weather, wars, riots, strikes

(natural or man-made)

Absolute Advantage

Exists when a person/nation can produce more of a certain good/service than someone else in the same amount of time

Who can produce more?

Comparative Advantage

Exists when a person/nation can produce a good/service at a lower opportunity cost than someone else in the same amount of time/resources

Who has the LOWER opportunity cost?

= more efficient

Input problems

an INPUT problem presents the data as amount of resources needed to produce a fixed amount of output.

ex. # of labor hours to produce 1 pen

When identifying abs. adv., input problems want who can produce using the least amount of resources

IOU - Input: Other goes Under

Output problems

an OUTPUT problem presents the data as products produced given a set of resources.

ex. Number of pens produced

OOO - Output: Other goes Over

Specialization

A country focuses on producing 1 good to gain greater efficiency

ex. USA producing ONLY Wheat

Countries can be made better off if they will produce goods they have a comparative advantage in and then trade with others for whatever else they want/need

Countries should trade if they have a relatively LOWER opportunity cost

They should specialize in the good that is “CHEAPER” for them to produce (costs less labor/resources)

Terms of Trade

Fair Trade Agreement - agreed upon condition that would benefit both countries

will need to answer if both countries benefit on quizzes/tests

Production Possibilities Curve (or Frontier)

(PPC/PPF)

graph showing combinations of the amount of 2 goods/services that an economy can produce by transferring resources from 1 good to the other

Constant Opportunity Costs

resources are easily adaptable for producing either good

Straight line on PPC

Increasing Opportunity Cost

As you produce more of any good, the opportunity cost will increase

resources are not easily adaptable to producing both goods

result is a bowed out (concave) PPC

Productive Efficiency

Products are being produced in the most effective way

This is any point on the PPC

Allocative Efficiency

products being produced are the ones most desired by society

this optimal point on the PPC depends on desires of society

Per Unit Opportunity Cost (formula)

Per Unit Opportunity Cost = (Opportunity Cost)/(Unit Gained)

4 Shifters of the PPC

QQTT

Change in resource quantity

Change in resource quality

Change in technology

Change in trade

Economics

The science of scarcity

Scarcity

we have unlimited wants but limited resources → must make choices

TINSTAAFL

“there is no such thing as a free lunch”

economic concept that states nothing is truly without a cost

Goods

physical objects that satisfy needs & wants

Consumer Goods - physical objects that satisfy needs & wants

Capital Goods - purchased by businesses to produce their products

used over and over again

Services

actions or activities that one person performs for another

Rational choice

marginal benefit ≥ marginal costM

Marginal Cost

the cost of a one-unit increase in an activity

what you give up in return for something

money, time, etc.

Marginal Benefit

the gain of a one-unit increase in an activity

what you get in return for something

money, time, etc.

As you consume more of a product, the marginal benefit for it _______ with each instance of consumption.

decreases

Trade-off

ALL the alternatives that we give up when we make a choice

Opportunity Cost

the ONE most desirable alternative (or trade off) given up when you make a choice

like your second best option

Four Factors of Production

Land, labor, capital, entrepreneurship

Land

All natural resources that are used to produce goods and services

ex. water, sun, plants, animals

Not just land, but anything that comes from the land

Income is rent

Labor

any effort a person devotes to a task for which that person is paid

ex. lawyers, doctors, teachers, waiters, etc.

Income is wages and is the largest source of income for most people.

Capital

an asset that can improve productivity

2 Types

Physical capital - any human-made resource that is used to create other goods and services (tools, tractors, machinery, buildings, factories, etc)

Human capital - any skills or knowledge gained by a worker through education and experience

Income is interest

Entrepreneurship

the ability to innovate and discover new ways of utilizing resources

ex. Henry Ford, Bill Gates, inventors, store owners, etc.

take the initiative

innovate

act as the risk bearers

so they can PROFIT!

Profit = Revenue - Costs

Income is profit