ECON 2113 Final Exam Set

1/56

Earn XP

Description and Tags

Exam 1,2,3,4 = Finale

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

57 Terms

What percentage of the world’s economics expereince scaracity?

100%

The “invisible hand” directs economic activity through

prices

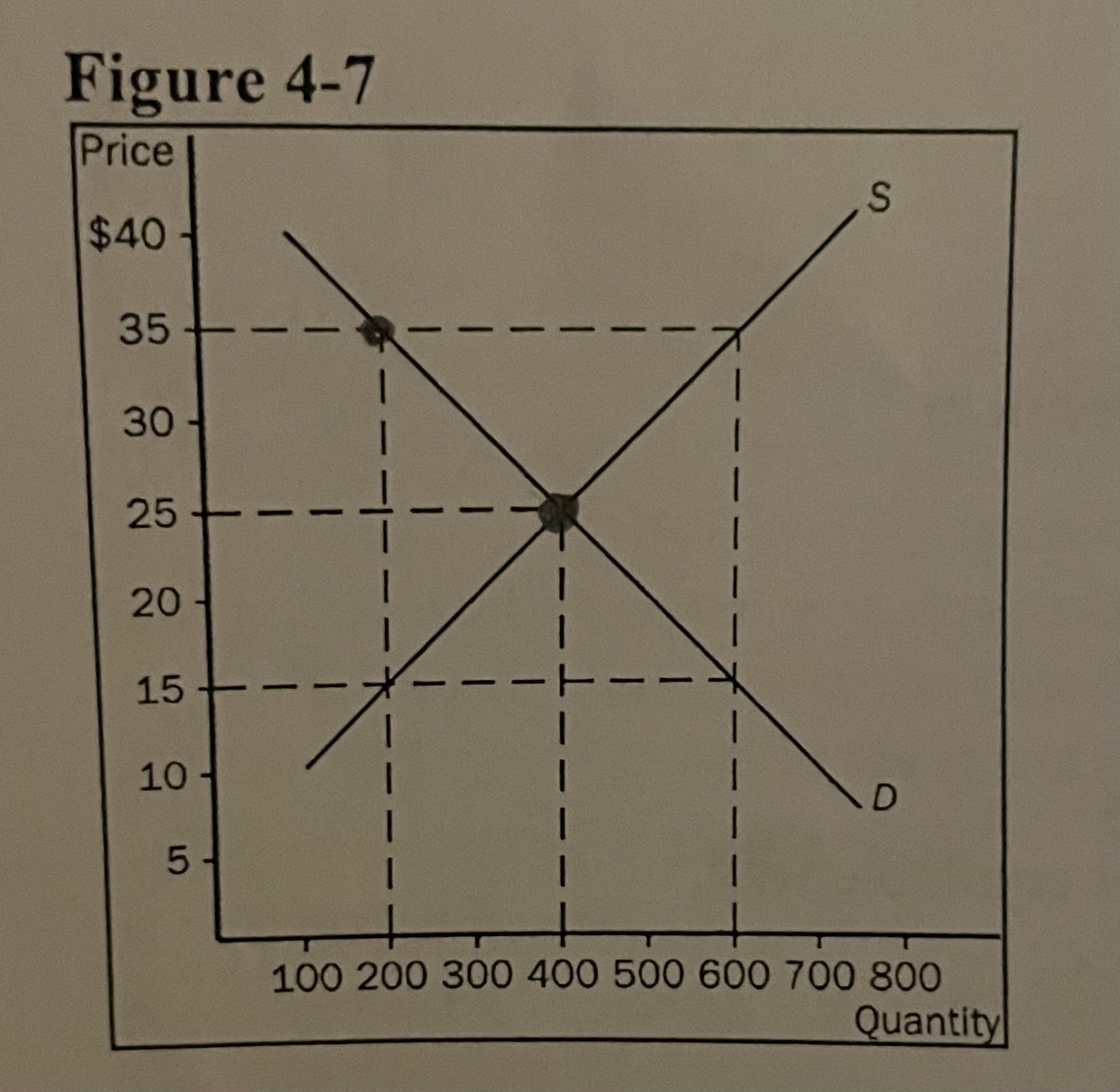

Refer to the image. At a price of $35. . .

a surplus would exist and the price would tend to fall

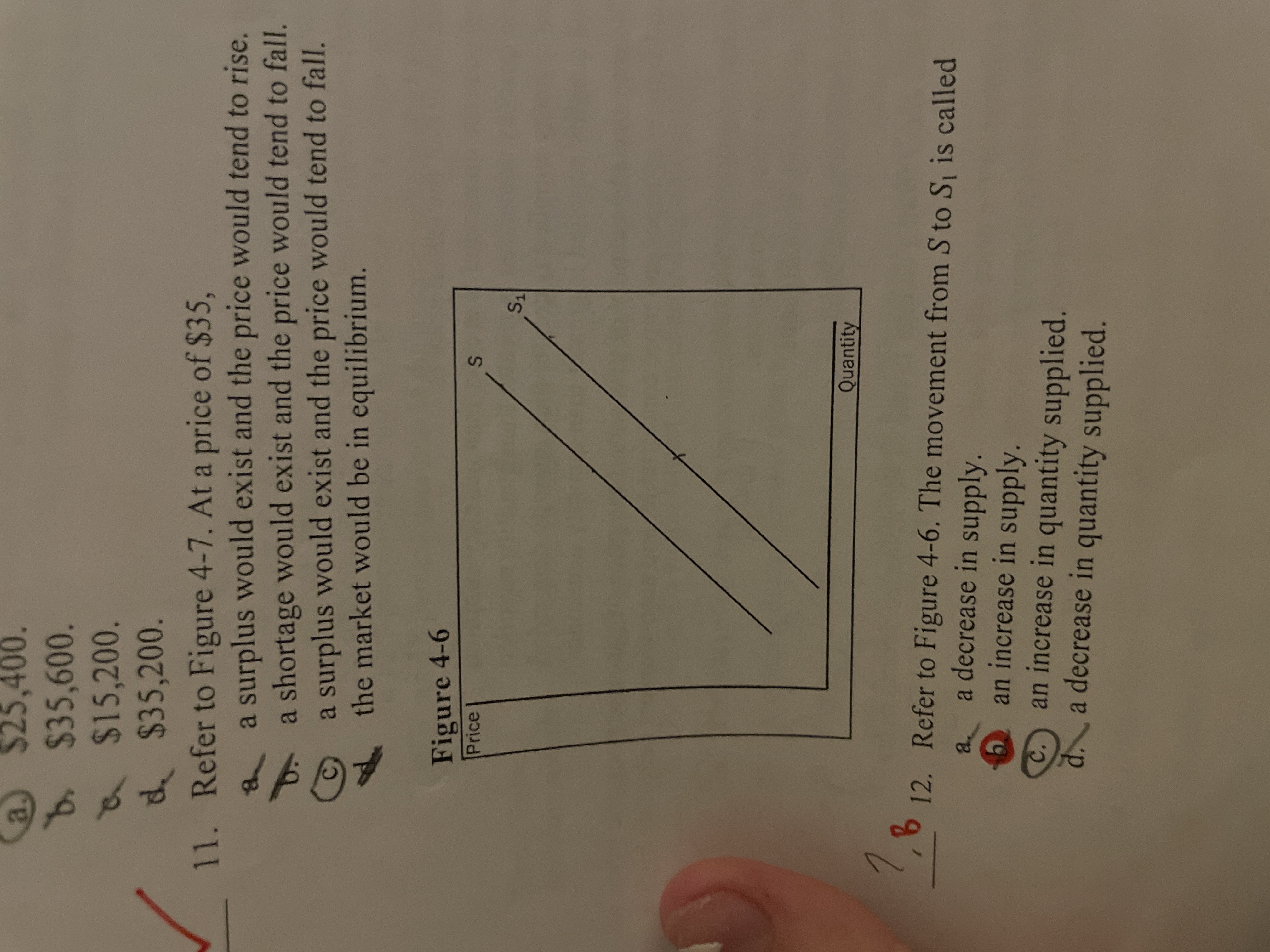

Refer to the image. The movement from S to S1 is called

an increase in supply

What will happen to the equilibrium price and quantity of new cars if the price of gasoline rises, the price of steel rises, public transportation becomes cheaper and more comfortable, and auto-workers negotiate higher wages?

Quantity will fall and the effect on price is ambigous

Elasticity of demand is closely related to the slope of the demand curve. The more responsive buyers are to a change in price, the demand curve will be

flatter

Suppose the price elasticity of demand for basketballs is 1.20. A 15% increase in price will result in

an 18 percent decrease in the quantity of basketballs demanded

T/F: Tuition is the single-largest cost of attending college for most students

false

T/F: The law of demand states that the quantity demanded of a product is postively related to price

false

T/F: If the demand for a good falls when income falls, the good is called an inferior good

false

T/F: A movement along a supply curve is called a change in supply while a shift of the curve is called a change in quantity supplied

false

T/F: A market economy cannot produce a socially desirable outcome because individuals are motivated by their own self-interest

false

T/F: A supply curve slopes upward because, all else equal, a higher price means a greater quantity supplied

true

T/F: The demand for Rice krispies is more elastic than the demand for cereal

True

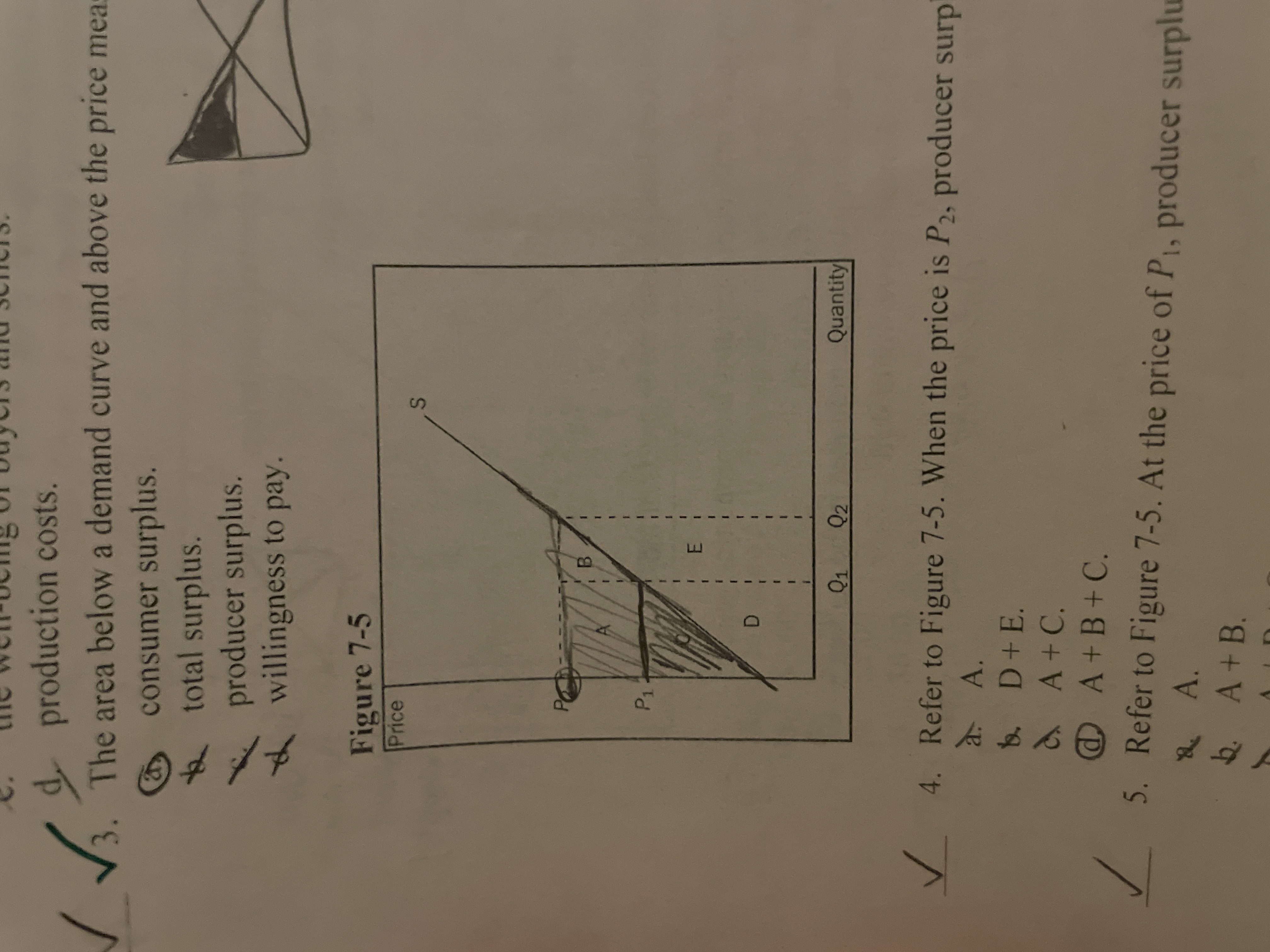

The area below a demand curve and above the price measures

consumer surplus

Refer to the image. Area A represents

the increase in producer surplus to those producers already in the market when price rises from P1 to P2

The marginal seller is the seller who

would leave the market first if the price were any lower

Efficiency occurs when

total surplus is maximized

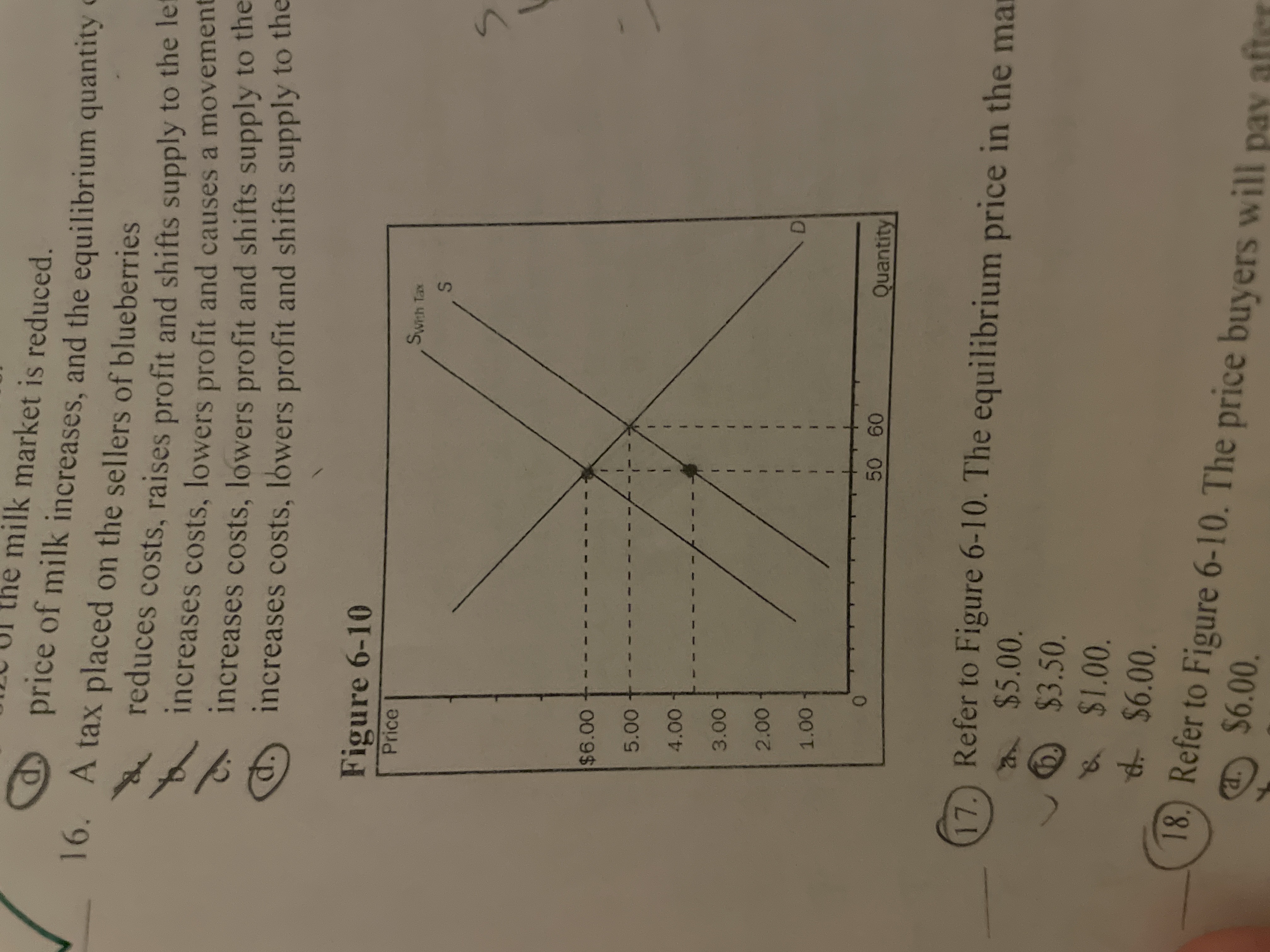

A tax placed on the sellers of blueberries

increases costs, lowers profits and shifts supply to the left (upward)

Refer to the image. The amount of tax imposed in this market is

$2.50

Refer to the image. The price sellers recieve after the tax is

P1

Refer to the image. The amount of tax revenue recieved by the government is equal to the area

P3 A C P1

Refer to the image. The amount of deadweight loss associated with the tax is equal to

A B C

T/F: If a tax is imposed on the buyer of a product, the tax incidence will fall entirely on the buyer to pay more

false

T/F: The area above the demand curve and below the price measures the consumer surplus in a market

false

T/F: Consumer surplus is the amount a buyer actually has to pay for a good minus the amount the buyer is willing to pay for it

false

T/F: The incidence of a tax depends on whether the tax is levied on buyers or sellers

false

T/F: Often, the tax revenue collected by the governement equals the reduced welfare of buyers and sellers caused by the tax

false

T/F: Because taxes distort incentives, they cause markets to allocate resources inefficiently

true

T/F: When there is deadweight loss we can be certain that the entire society experiences a loss

True

Economic profit is equal to

total revenue minus the opportunity cost of producing goods and services

The efficient scale of the firm is the quantity of output that

minimizes average total cost

Average total cost is increasing whenever

marginal cost is greater than avergae total cost

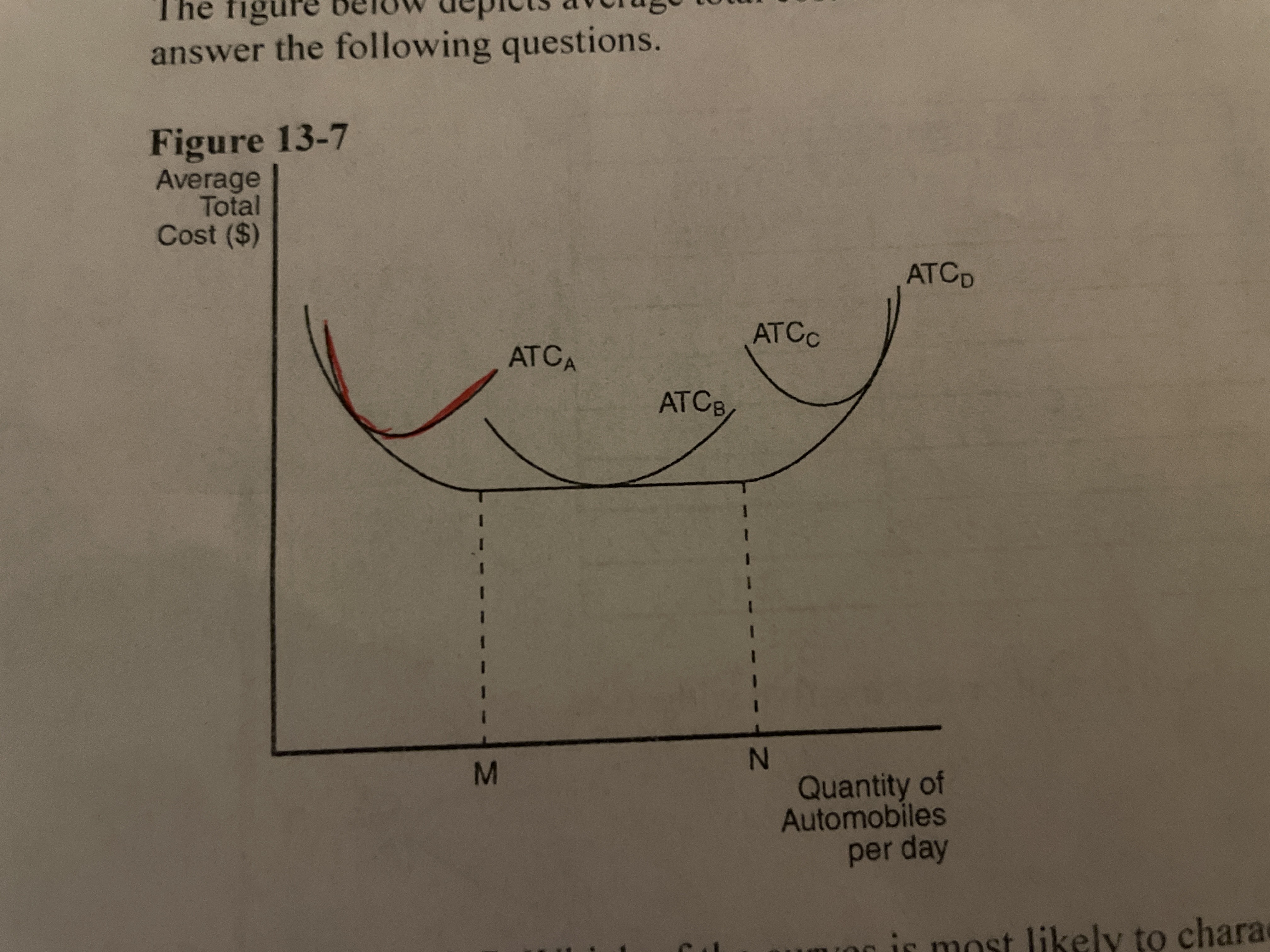

Refer to the image. Which of the curves is most likely to represent marginal cost?

Curve A

Refer to the image. Which of the curves is most likely to characterize the short-run avergae total cost curve of the smallest factory?

ATC A

Economies of scale arise when

workers are able to specialize in a particular task

The marginal product of labor can be defined as

change in output/change in labor

T/F: When economists speak of a firms costs, they are usually excluding the opportunity costs

false

T/F: Diminishing marginal product exists when the total cost curve becomes flatter as outputs increases

false

T/F: Average total cost reveals how much total cost will change as the firm alters its level of production

False

T/F: Fixed costs are those costs that remain fixed no matter how long the time horizon is

false

T/F: Accountants often ignore implicit costs

true

T/F: If the marginal cost curve is rising, so is the average total cost curve

false

T/F: Diseconomies of scale often arise because higher production levels allow specialization among workers

false

For a competitive

average revenue, marginal revenue, and the price of the goodare all equal to one another

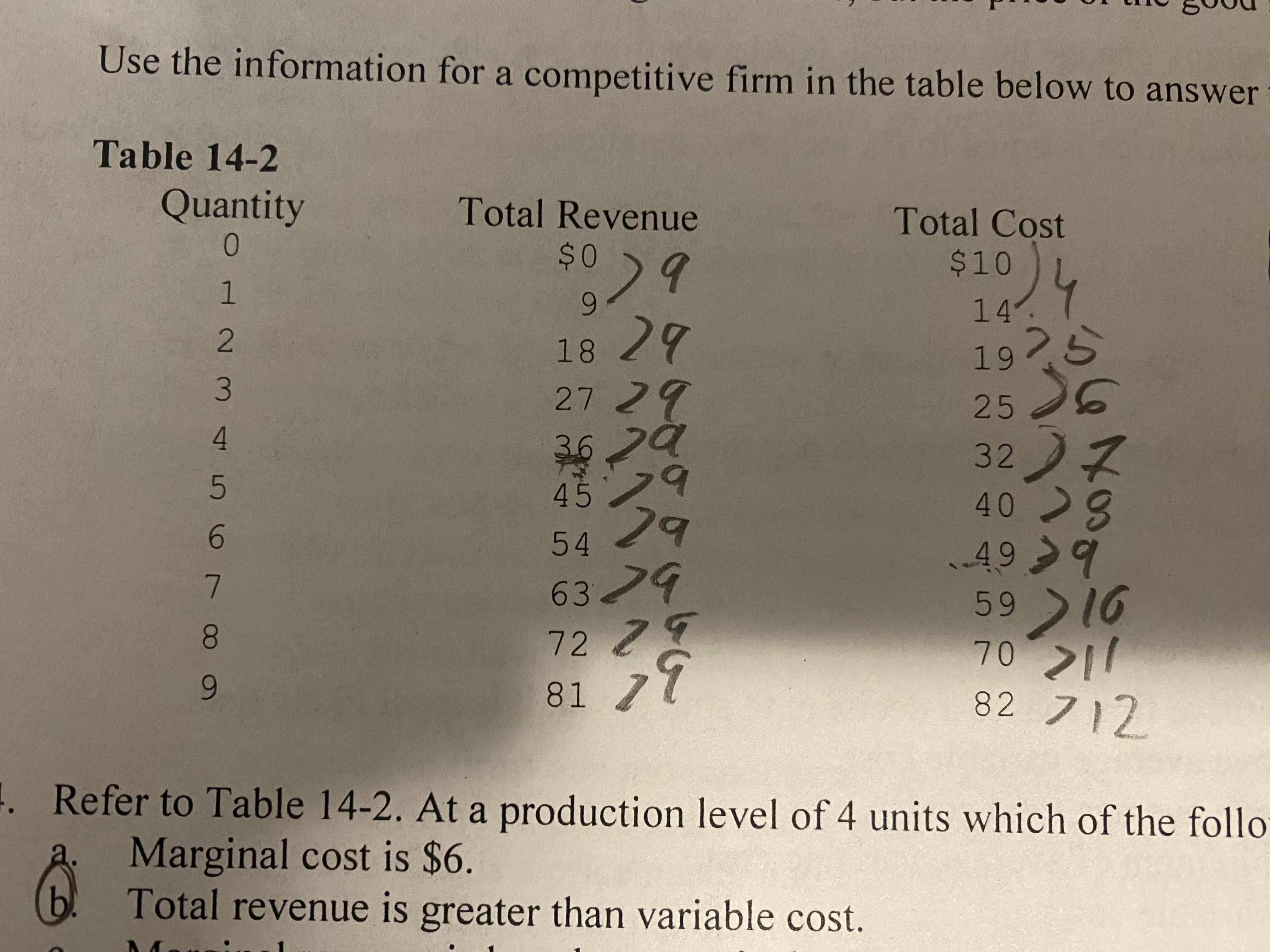

Refer to table 14-2. If this firm chooses to maximize profit it will choose a level of output where marginal cost is equal to

9

when a perfectly competitive firm makes a decision to shut down, it is most likely that

price is below the minimum of average variable cost

Profit-maximizing firms enter a competitive market when, for existing firms in that market,

Price exceeds average total cost

If a profit - maximizing monopolist faces a downward-sloping market demand curve, its

marginal revenue is less than the price of the product

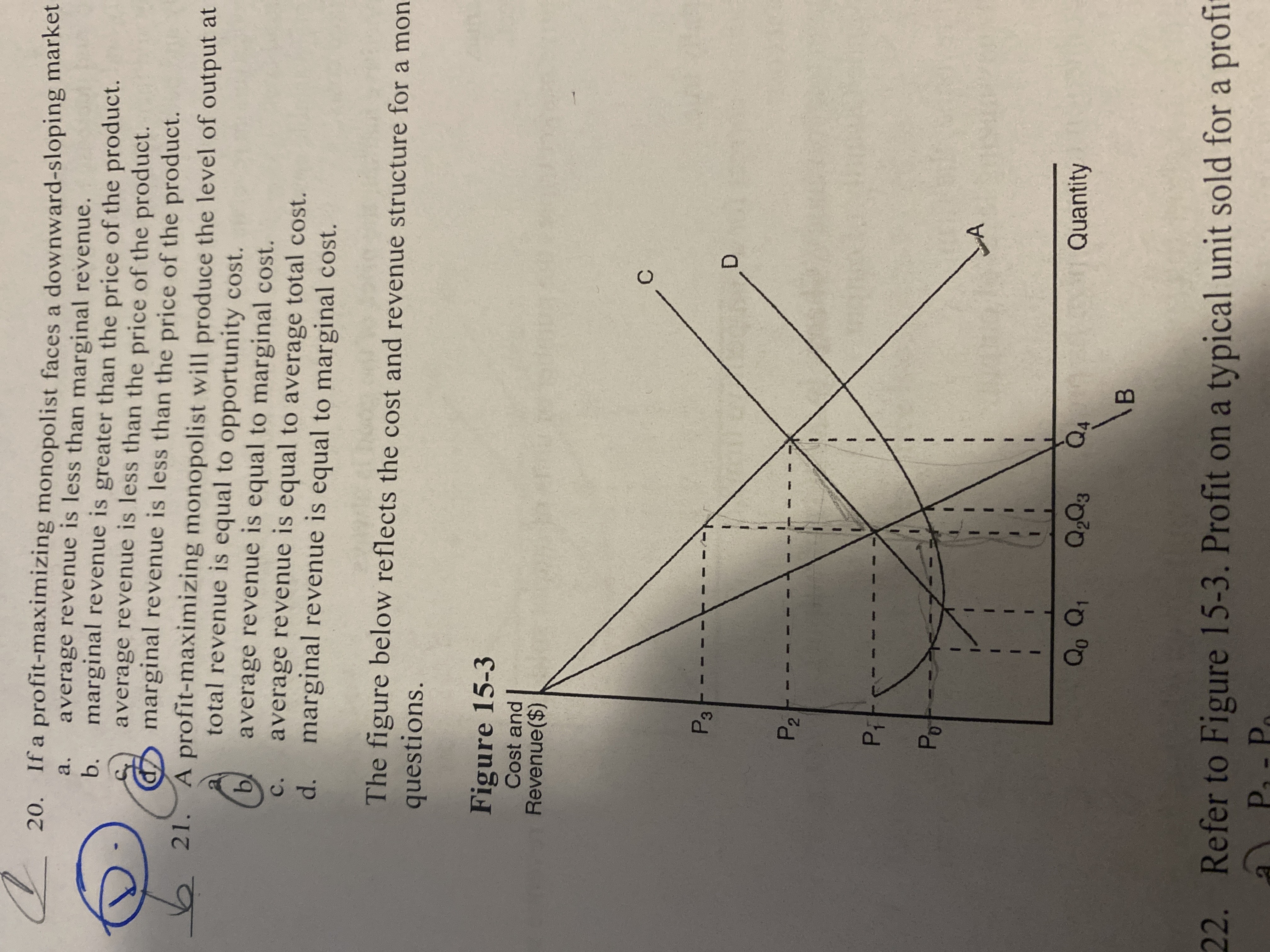

Refer to Figure 15-3. At the Profit-maximizing level of output,

Average revenue is equal to P3

For a firm in a competitive market, marginal revenue is always equal to average revenue

True

When a Profit-maximizing firm in a competitive market experiences rising prices, it will respond with an increase production

True

When a firm experiences zero-profit equilibrium, the firms revenue must be sufficient to cover all opportunity costs.

True

A firm will shut down in the short run if revenue is not sufficient to cover all of its fixed costs of production.

False

The De Beers Diamond company advertises heavily to promote the sale of all diamonds, not just its own. This is evidence that they have a monopoly position to some degree

True

Declining average total cost with increased production is one of the defining characteristics of a natural monopoly

True

For a monopoly, marginal revenue is often greater than the price they charge for their good

False