IB Economics SL - Quarter 1

1/48

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

49 Terms

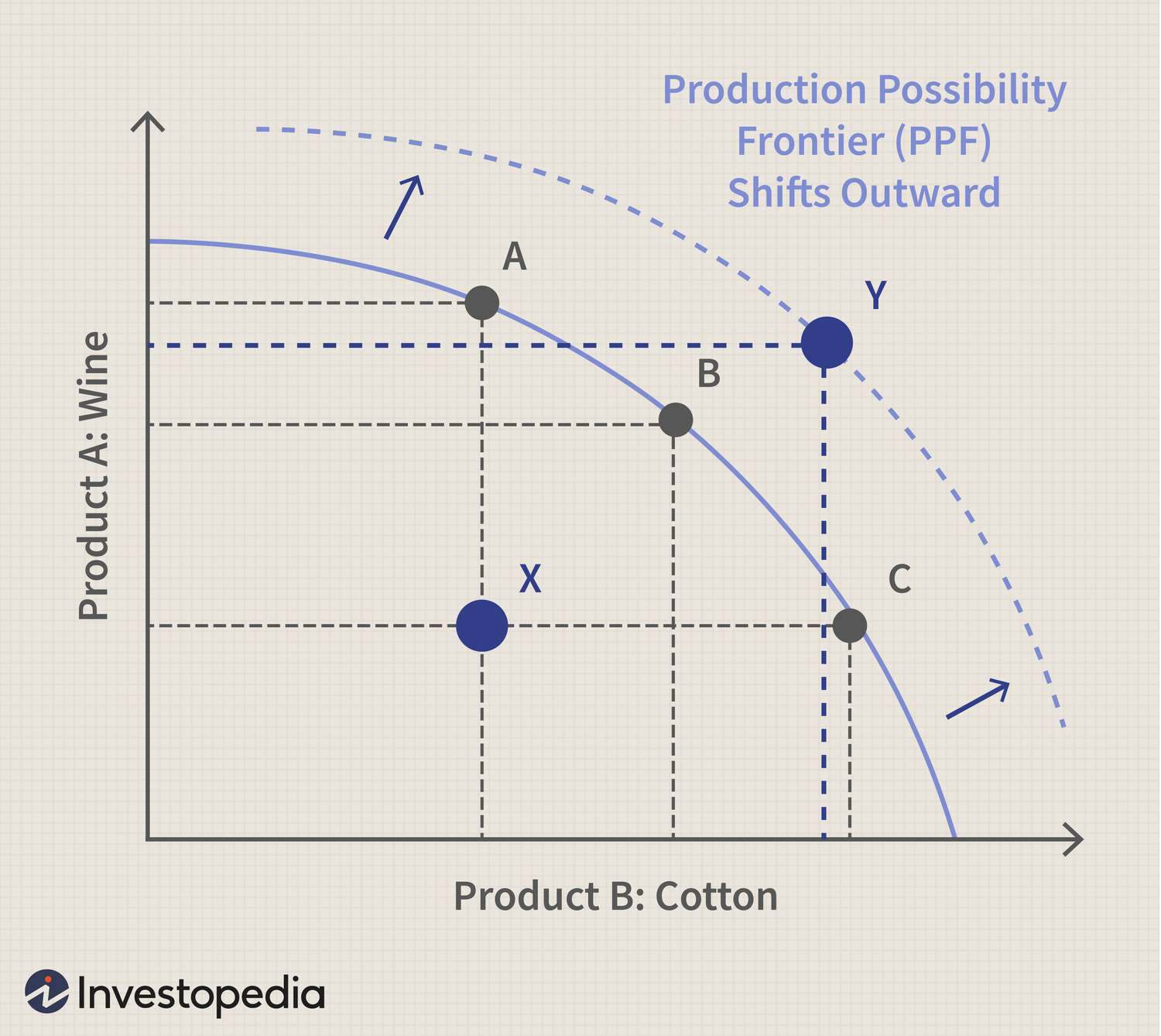

Production Possibility Fronteir (PPF)

A type of model that illustrates the trade-offs facing a business that produces only 2 goods.

Production Possiblity Curve (PPC)

A graphical representation that shows scarcity and opportunity cost

Market

where buyers and sellers come together to carry out an economic transaction

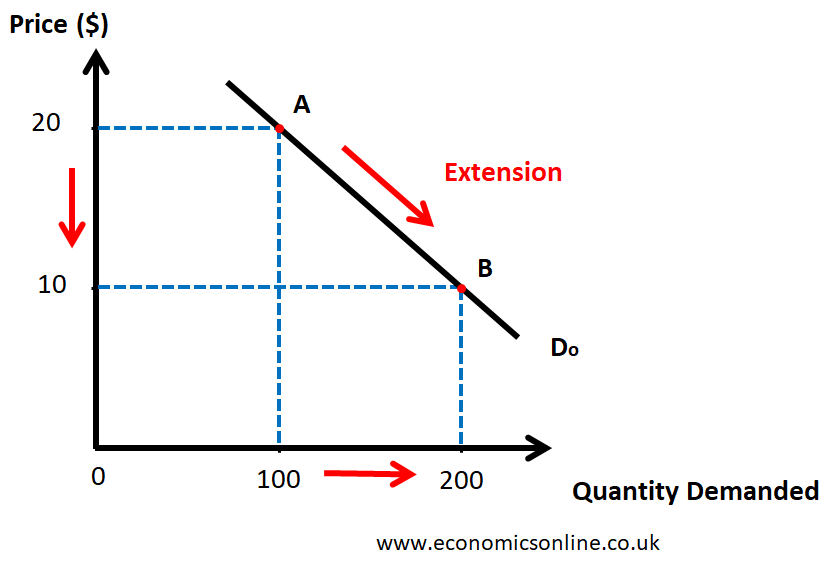

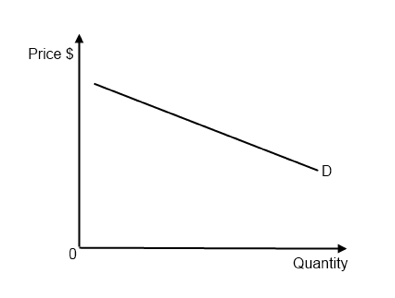

Demand

the quanity of a good/service that consumers are willing and able to purchase at a given price in a given able

law of demand

as the price of a product falls, the quanity demanded of the product will usually increase (ceteris paribus)

determinants of demand

Factors that cause the demand curve to shift (change in price)

income effect

when a price of a good falls, people will have an increase in their real income, which will cause people to buy more goods

real income

amount their incomes will buy

substitute effect

when the price of a good falls, then the good will be relatively more attractive to people over goods whose prices have not changed

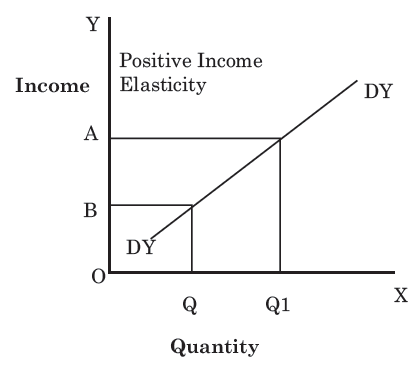

normal goods

as income increases, the demand for this good increases (the demand curve shifts right)

inferior goods

as income increases, the demand for these goods will fall because the consumer will begin to buy higher priced substitutions

demand curve

complements

products that are often purchased together, a change in price of one product will lead to change in demand for the other

unrelated goods

a change in the price of one good will have no effect on the demand for the other goods

law of diminishing marginal unity

as a consumer consumes more units of a good, the additional satisfaction (utility) they get from consuming an additional unit falls.

supply

the willingless and ability of producers to produce a quanity of a good/service at a given price in a given time period.

law of supply

as the price of a good/service increases, the quanity supplied of the good/service will increase

cost of production

if there is an increase in the cost of a factor of production (wages), then this will increase the cost and will supply less.

the price of other products

which the producer could produce instead of the existing product

state of technology

improvements in technology in a firm or industry should lead to an increase in supply, shifting the supply curve to the right.

expectations

producers make decisions about what to supply based on their expectation of future prices

equilibrium price

when a price has moved to a level at which the quanity of the good/service demanded equals the quanity of that good/service supplied.

market shortage

when the price decreases (pe to p1), quantity supply will decrease (qe to q1), but quantity demand will increase

price mechanism

forces of supply and demand that moves prices towards equilibrium

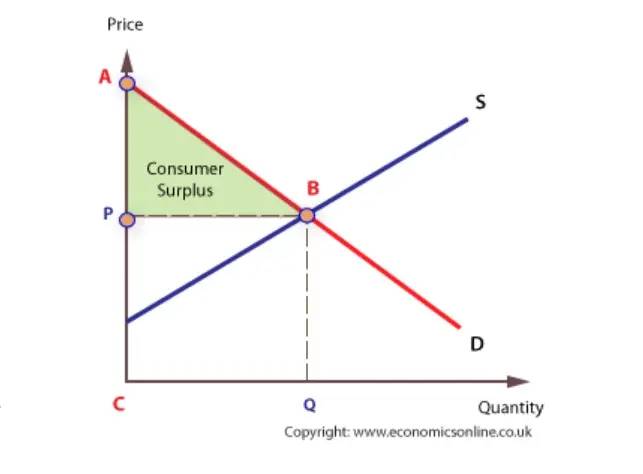

consumer surplus

the extra satisfaction (utility) gained by consumers from paying a price that is lower than that which they are prepared to pay.

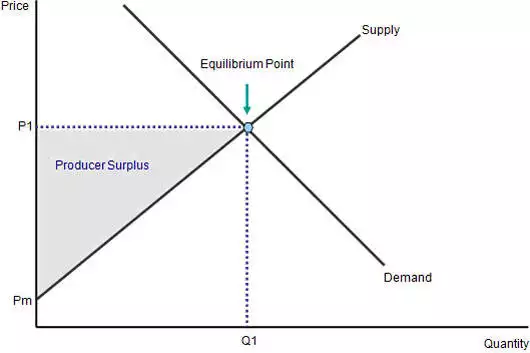

producer surplus

the amount below market price that a producer is willing and able to produce a good for.

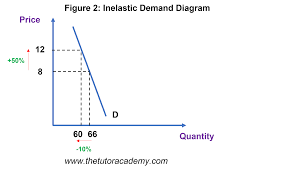

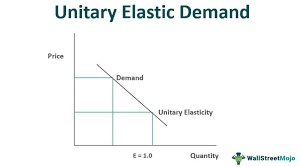

price elasticity of demand (PED)

the responsiveness of quanity demanded to changes in the selling price

formula for calculating PED

% change in quanity demand / % change in price

ped elastic good

a good where change in price leads to a greater than proportional change in quanity demanded (PED is > 1)

ped inelastic good

where change in price leads to a smaller than proportional change in quanity demanded (ped < 1)

ped unitary good

where change in price leads to a proportional change in quanity demanded. (ped = 1)

determinants of ped

Factors that influence the price elasticity of demand

number and closeness of substitutes

more substitutes for a product, more elastic demand, closer substitutes for a product, more elastic demand

necessity of the product

necessary goods are inelastic

share of income spend on good

inexpensive goods will be less elastic

the time period considered

as the price of a product changes, it often takes time for the consumer to change their habits. PED tends to be more inelastic in the short run, amd more elastic in the long term

income elasticity of demand (YED)

measure of how demand for a product changes when there is a change in consumer’s income

formula for YED

% change in demand / % change in income

sticky goods

goods that’s demand does not likely change

elasticity of supply (PES)

a measure of how much the supply of a product changes when there is a change in the price of a product

formula for calculating pes

% change in quanity supplied / % change in price

cost of production

as cost of production increases supplier will not raise supply

unused capacity

if unused capacity (of good) exists, PES is elastic

mobility of factors of production

if factors of production can be easily changed PES is elastic.

time period considered (PES)

the longer the time period considered, the more elastic the supply will be

ability to store stock

if a firm can store high levels of stock, they’ll be able to react to price with supply, pes will be relatively elastic

commodities

raw materials such as cotton or coffee.

commodities ped

tend to have inelastic demand because they are necessities

commodities supply

tend to have an inelastic supply.