Production, Productivity and Cost

1/25

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

26 Terms

What is production in economics?

The converting of inputs, or factors of production such as labour and capital, into outputs of goods and services.

What role do producers play in the economy?

make goods and services sold in the economy

provide jobs

influence prices while aiming to make a profit

Who can be considered producers?

Small businesses, multi-national corporations, governments, and individuals.

How can individuals act as producers?

Produce non-market goods and services, such as cleaning and cooking, and can be self-employed.

What types of firms can be producers?

Small businesses or large national companies that employ factors of production to produce goods or services.

How do large firms compete in the market?

power to limit supply

exert pressure on prices

What is the government's role as a producer?

spends money on public transport, infrastructure, and public goods like education

welfare/household benefits

healthcare

How is productivity defined?

Measure of efficiency in using factors of production to produce a good/service

What is the productivity equation?

Productivity = total output / total input.

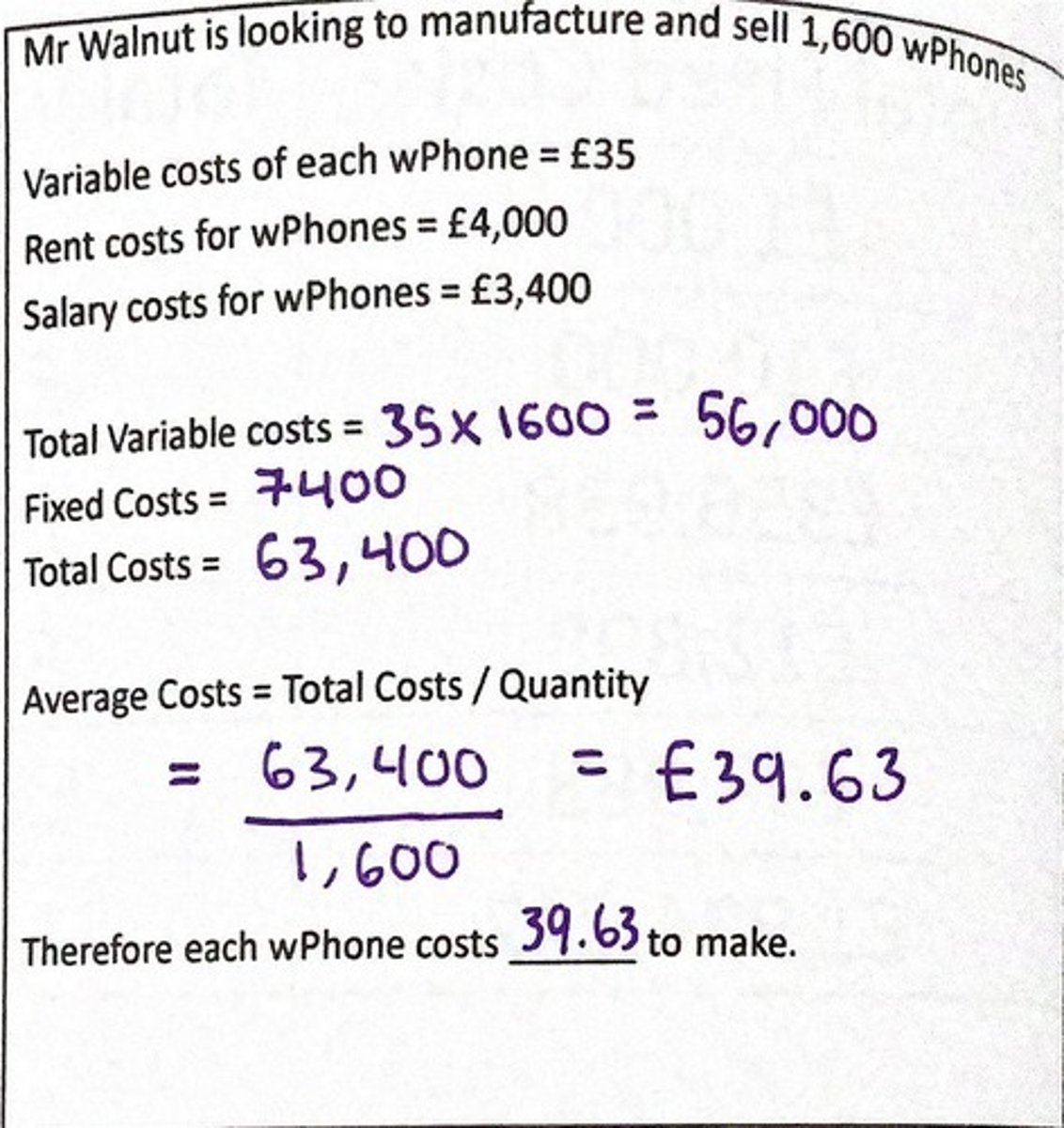

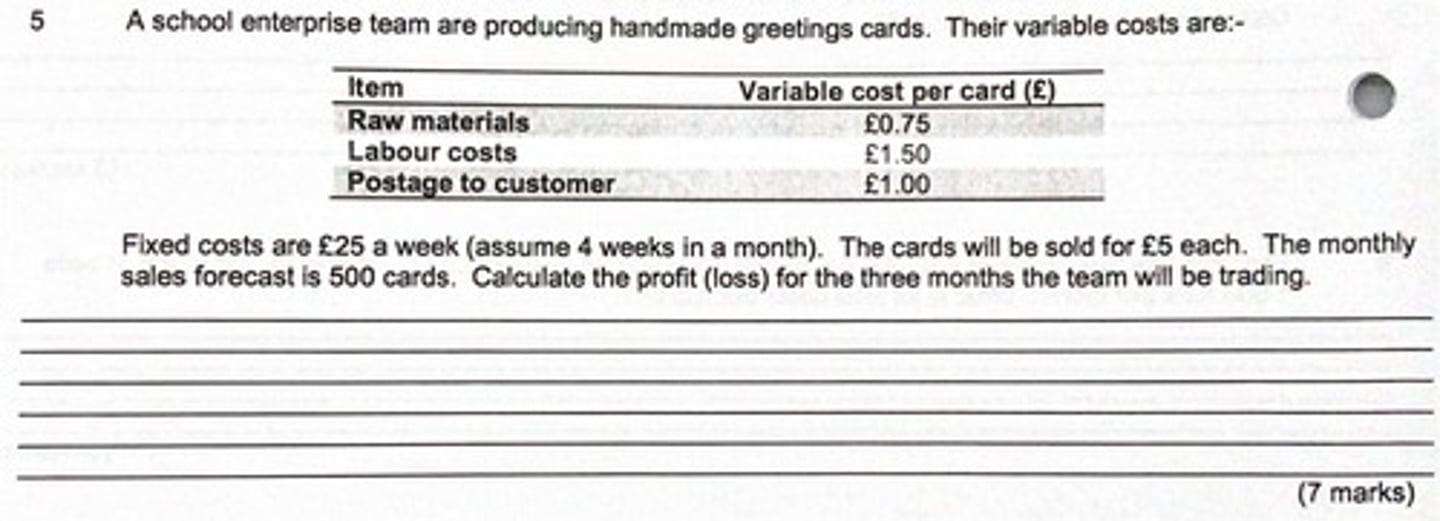

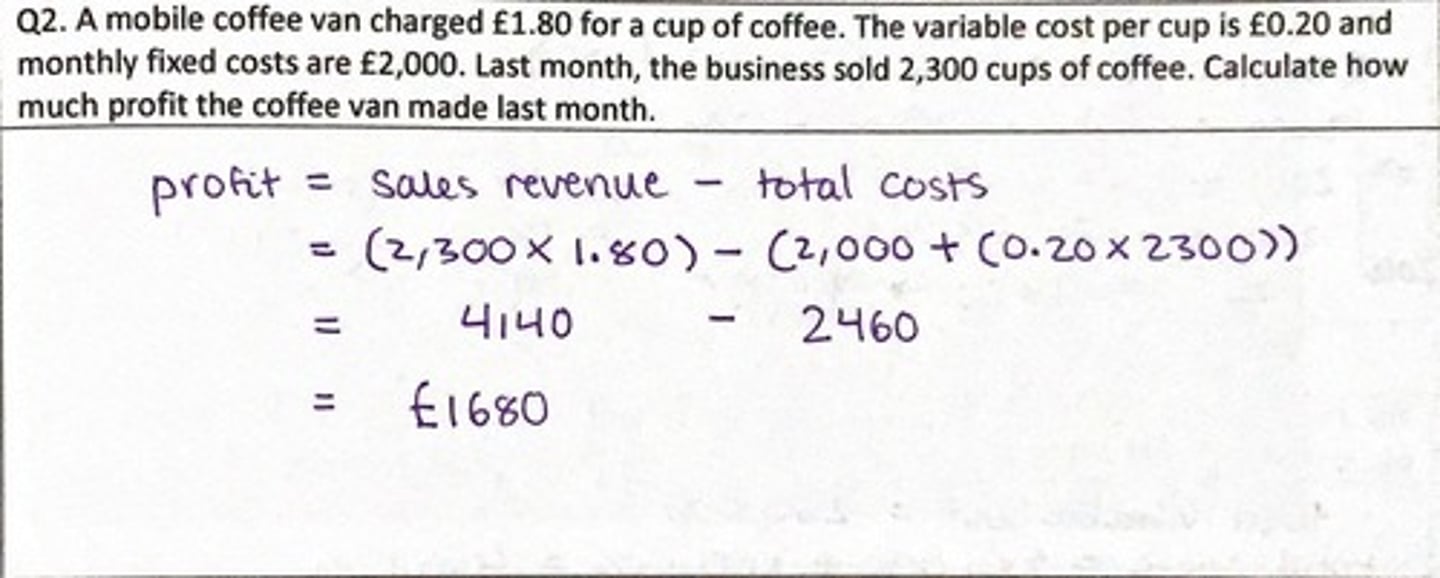

What are fixed costs in production?

Costs firms face to run a business, do not change despite production or sales volume.

salaries, rent

What are variable costs?

Costs faced by a firm in the production of a good/service, changes depending on production or sales volume

raw materials, wages for production workers.

What are total costs?

Sum of all costs of producing goods/services and running the business.

What is the equation for total costs?

Total costs = total fixed costs + total variable costs.

What are average costs?

Cost of producing a unit of a product, useful for setting prices.

How do you calculate average costs?

Average cost = total costs / quantity.

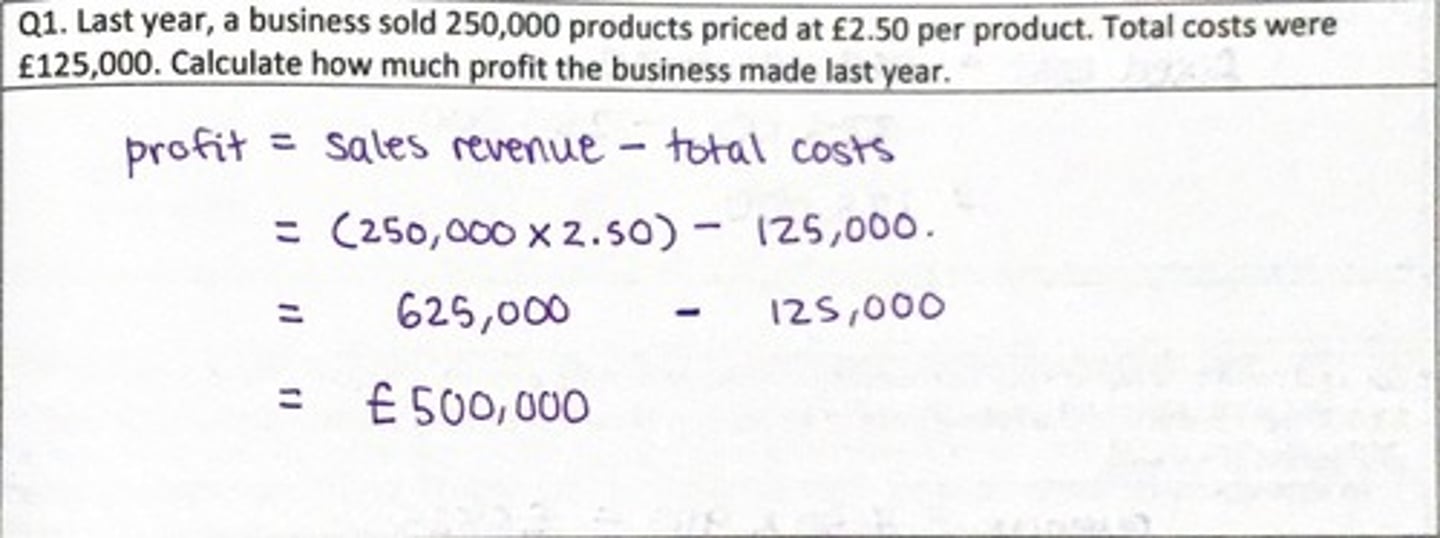

What is total revenue?

Total income of a firm from selling of goods/services.

What is the equation for total revenue?

Total revenue = price of item * quantity sold.

What is average revenue?

Revenue per unit of output sold.

What is the profit equation?

Profit = total revenue - total costs.

When does a firm incur a loss?

When total revenue is less than total costs.

What is the profit-maximizing objective of a firm?

Main objective of a firm to make the largest possible profit.

How do production costs affect supply?

If production costs fall, the incentive to supply increases; if costs rise, the incentive decreases.

Why is revenue important for producers?

Must exceed costs for businesses to make a profit.

allows for investment and expansion.

Why is profit important for producers?

generates finance for investment

signals potential profitability to other producers

attracts resources

What happens if a firm consistently makes a loss?

It may need to close down.

What is the importance of average costs in firm operations?

Indicates how efficiently scarce resources are being used and helps firms set prices.