Chapter 6

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

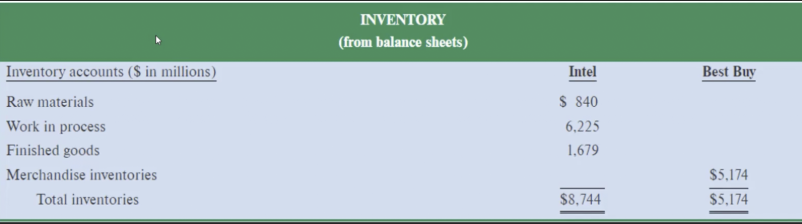

Manufacturing items

Raw materials – what we need to make goods

Work in process – starting to build goods

Finished goods

Merchandising items

Merchandise inventories

Inventory - manufacturing and merchandising

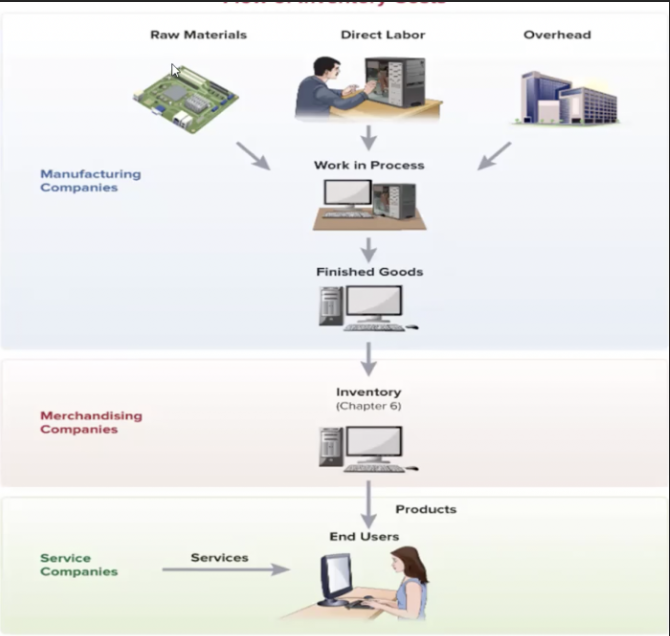

Flow of Inventory Costs visual

Raw materials, Labor, and Overhead lead to work in progress then finished product (manufacturing companies)

merchandising companies have inventory

service companies give products and services to end users

Relationship w inventory and cost of goods sold

Cost of goods sold shows up as expense the income statement and inventory shows up as asset the balance sheet

Cost of goods sold

amount of inventory that we moved away from ending inventory that has been sold

Ex. 10 units of chairs in inventory and 5 are sold. Cost of 5 chairs are the cost of goods sold

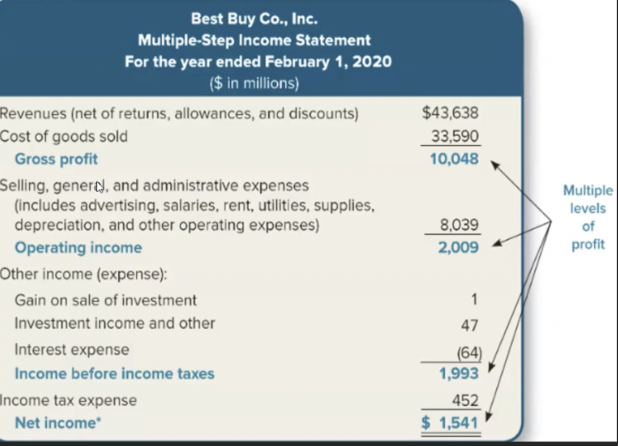

Multiple-step income statement / 4 things

Shows Gross Profit, Operating Income, Income before income taxes, and net income

Valuation: Inventory and cost of goods sold

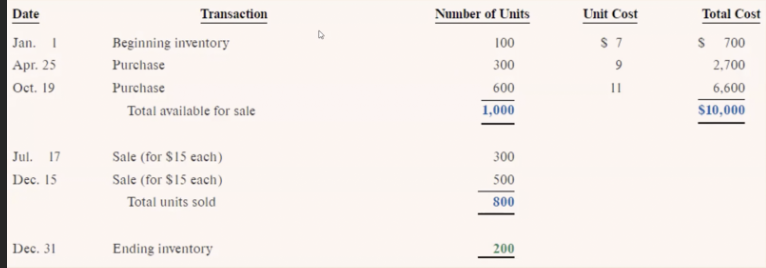

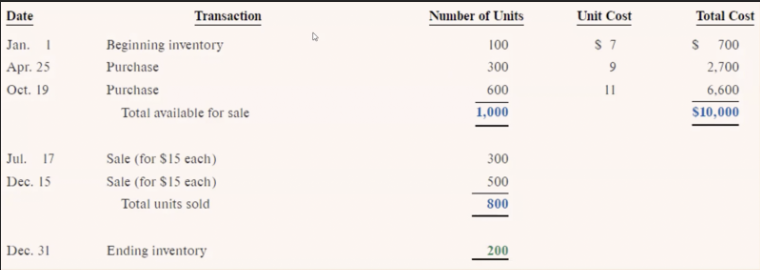

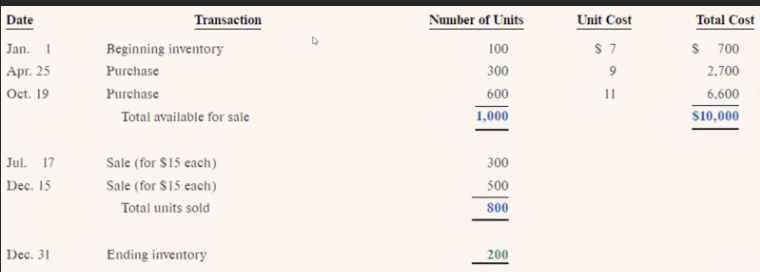

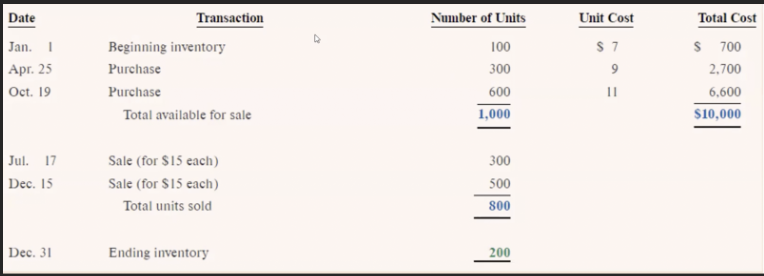

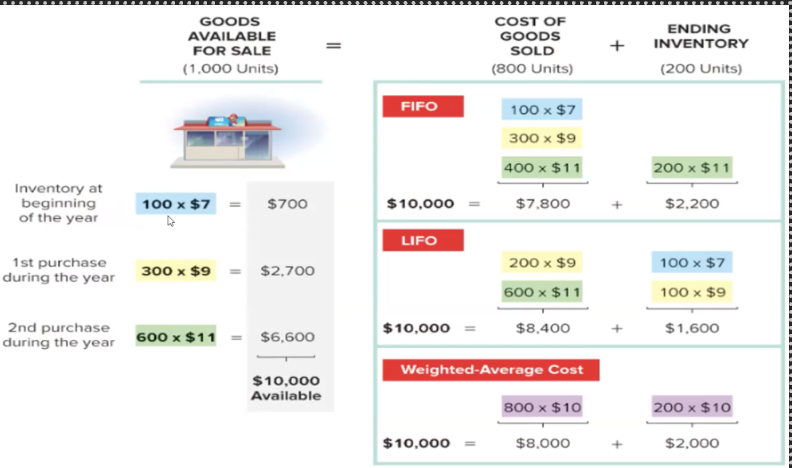

Inventory transactions for a game shop

Pay attention to unit cost and how it goes up in during dif dates

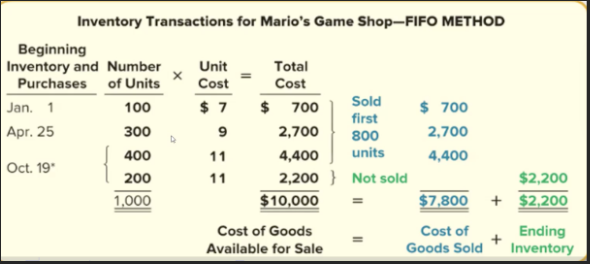

First in first out (FIFO) inventory method

First in you look at the first units sold and work your way down, $7 per unit, then $9, then $11

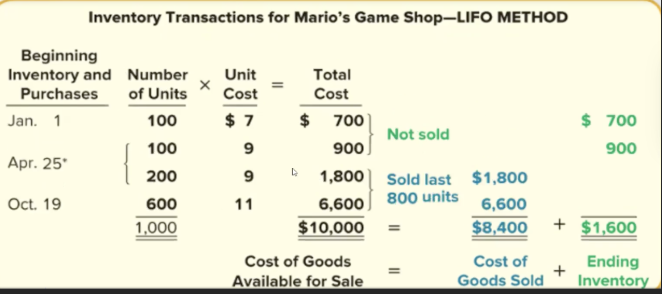

Last in first out (LIFO) inventory method

Start with the units that are $11 per unit first

With graph if you sell 500 units

FIFO 100 units are sold at $7; 300 units are 9$, and the remaining 100 units are $11

LIFO all 500 units are sold at $11

First-in First-out game shop

Look at how 800 units are sold and the way they work down line

Last-in First-out game shop

See how all 800 units are covered by the last units that came in

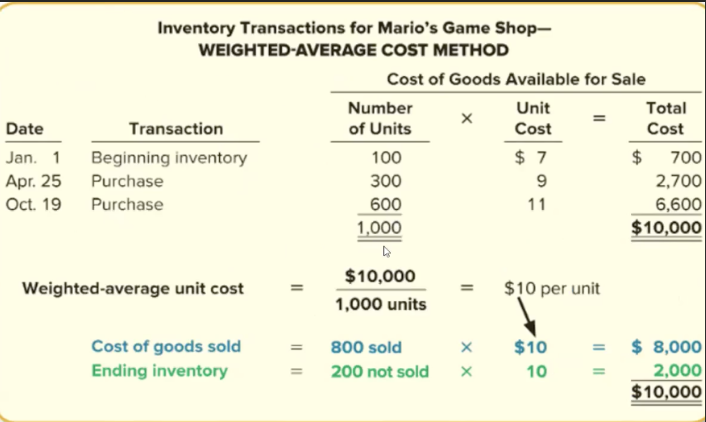

Weighted-average cost

Take total cost and divide by total units, here you find the cost of the unit

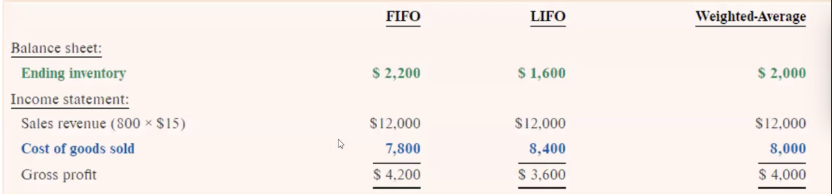

Ending effect of FIFO, LIFO, and Weighted-Average

LIFO and FIFO specs

FIFO: Lower COGS → Higher gross profit and net income → Higher ending inventory.

LIFO: Higher COGS → Lower gross profit and net income → Lower ending inventory.

Ending effects of FIFO, LIFO, and Weighted average cost

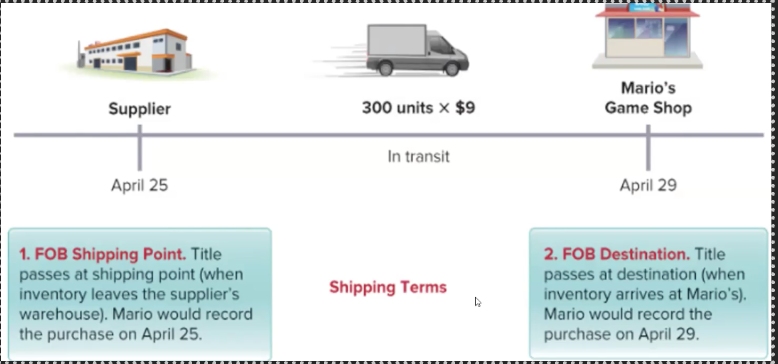

Shipping terms

2 terms are FOB shipping point and FOB destination

FOB stands for freight on board

FOB shipping point

Ownership transfers when the seller ships the goods.

The buyer owns the goods while they are in transit.

The buyer is generally responsible for shipping costs and any loss or damage during transit (unless the contract says otherwise).

FOB destination

Ownership transfers when the goods arrive at the buyer's location.

The seller owns the goods while they are in transit.

The seller is generally responsible for shipping costs and bears the risk of loss until delivery.

Journal entry for FOB destination and FOB shipping point

FOB shipping point entry is made as soon as items ship

FOB destination entry is made when goods are received

Formula for COGS

Beginning inventory + Purchses - Ending Inventory

Gross Profit

revenues - COGS

Types of operating expenses

advertising, salaries, rent, utilities, supplies, depreciation,

aka selling, general, and administrative expenses

Operating income

Gross profit - operating expenses

Income before income taxes

Operating income - Other income expenses

other income expenses may be investment income and interest expense

Net income

income before taxes - income tax expense

Journal entry of goods costing 550k being sold for 335k