microeconomics

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

the economic problem

humans wants are unlimited BUT resources to fulfil such are limited.

what four questions must an economic system answer?

what to produce

how much to produce

how to produce

for whom to distribute production

subsistence economy

characterised by

self-support (i.e. you get your own food, shelter, clothes etc

rather than paying for things, you barter or trade for goods and services

command/planned economy

The government controls all businesses

The government dictates what is produced and the prices of such

typically part of “communist” political systems

free market economy

private ownership of goods and services

prices of goods and services are determined by supply and demand

part of a pure capitalist system

relative scarcity

When certain goods and services are in limited supply compared to other goods and services. in a free market economy, the prices of scarce goods are higher due to a decrease in supply

opportunity cost

the loss of other alternatives when one alternative is chosen (oxford dictionary). essentially, the value of the next best option, of which you can no longer satisfy

assumes consumers are

rational

production possibility frontier (PPF)

represents opportunity cost in a graphical manner from a business/producer perspective. i.e. if i make more of good a, how much of good b must i sacrifice? curve of ppf is a line of maximum efficiency.

production possibility frontier (PPF) assumptions/limitations

only 2 goods or services

all resources are fixed

all resources are fully employed

no change in the state of technology

resources are 100% substitutable

cost benefit analysis (cba)

measure of determining whether a project is economically viable. is done through giving benefits and negatives a monetary value. if benefits outweigh the costs, a project is typically seen as worthwhile.

the cba helps determine allocation of scarce resources by helping to identify what usage of resources maximises economic welfare and provides other benefits

how do we put monetary values on non-monetary things? (i.e. views, noise, environmental damage)

surveys

replacement costs (estimated costs of replacing/restoring lost benefits)

willingness to pay (i.e. how much would you be willing to pay to avoid a negative externality? or to use a good/service?)

Clean air isn’t sold in a market, but we can ask:

"How much would you be willing to pay each year for cleaner air in your city?"

If many people say they’d pay $100/year, economists can use that to estimate a monetary value for cleaner air by aggregating those responses.

factors of production + examples of each

land (natural resources, energy, physical land)

labour (employees)

capital (tools, buildings, things used to produce consumer goods)

entrepreneurship (technology, expertise)

increasing opportunity cost

The increase in the production of good a leads to a greater forgone production of good b.

constant opportunity cost

the trade off opportunity cost between goods/services is constant

income of resources

Income is the reward for the owners of a resource.

land = rent

capital = interest

labour = wages

enterprise = profit

mixed market economies

economies with aspects of both planned and free market economies, hence the name mixed market.

capitalist elements of australia’s mixed market economy

economic freedom (individuals choose what they do with their disposable income)

competition (more than one producer of goods and services, allowing consumer choice. hence, businesses are incentivised to offer the lowest prices to entice the most customers)

private property (individuals have the right to own private property. extends to the right of companies to own businesses and firms)

self-interest (individuals can chose what is best for them)

voluntary exchange (individuals can buy and sell goods)

profit motive (businesses and individuals are driven by a desire to make profit)

command elements of australia’s mixed market economy

government regulations on some business practices (i.e. working hours, wages, safety)

limits on certain goods/services (i.e. cannot purchase unpasteurised milk, films and games with a degree of sexual violence)

government aid to the needy (Medicare, Centrelink)

the price mechanism

the process by which supply and demand determine the equilibrium price and quantities of goods and services.

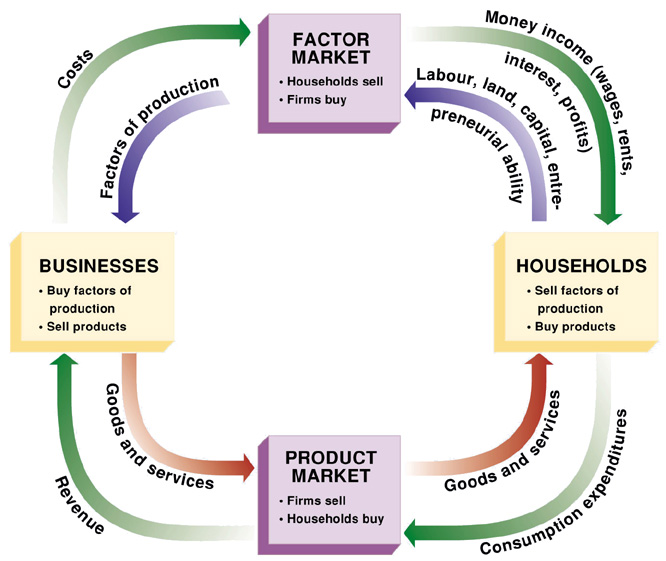

product market

markets used to exchange final stage goods and services

factor market

the market where the resources used to produce goods and services are bought and sold.

law of demand

if all else (factors) remain equal, the higher the price of a good/service, the fewer people that will demand the good/services AND vice versa. suggests an inverse relationship between supply and demand

price factors influencing demand

the price of the good/service

very easy to remember lol

non-price factors influencing demand

the price of substitute goods

the price of complementary goods

level of consumer income

expected future prices

expected future income

size of population

population age distribution

education levels

change in consumer tastes

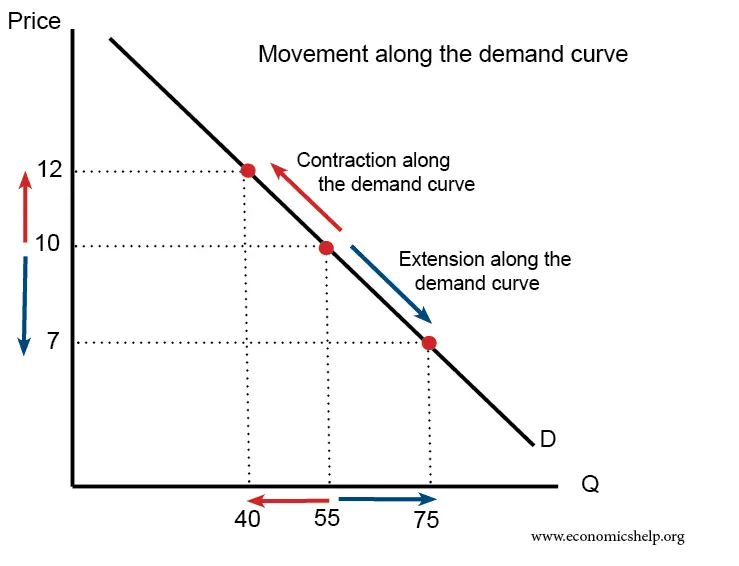

movements along the demand curve

A movement along the demand curve happens when a change has occurred in both the price and quantity of a good/service. implies that the relationship between supply and demand has remained constant.

a movement left/up on the demand curve is called a contraction in demand

a movement down/right on the demand curve is called an expansion in demand

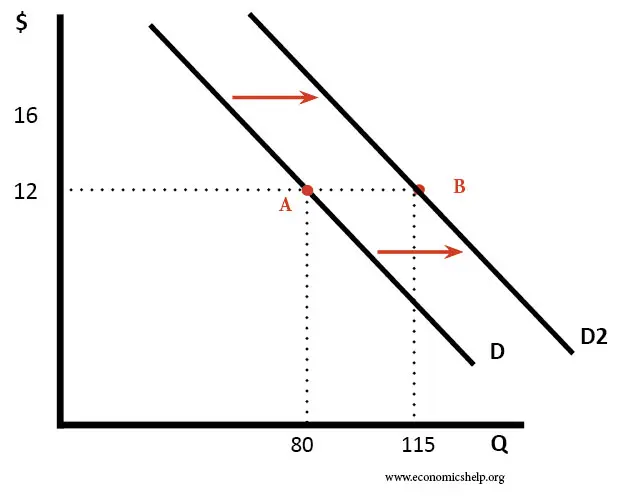

shifts of the demand curve

occurs when the quantity demanded of a good has changed, even though the price remains the same. implies that the original relationship between supply and demand has changed, and that quantity demanded has been impacted by non-price factors.

increase in demand = rightward shift

decrease in demand = leftward shift

normal goods

a good where as income increases, as does demand

for example, if someone goes from earning $500/week to $1000/week, they will likely increase their demand for good quality, brand name foods instead of supermarket brand.

inferior goods

a good where as income decreases, demand increases

for example, if someone goes from earning $1000/week to $500/week, they will likely increase their demand for supermarket-brand goods rather than good-quality brand-name foods

complementary goods

two goods that are typically used together. so, consuming more of one will lead to an increase in consumption of another.

for example, if there is an increase in demand for chips, there will likely be an increase in demand of tomato sauce

substitutable goods

Two alternate goods that could be used for the same purpose. therefore, an increase in demand in one usually leads to a decrease in demand for another

for example, butter and margarine

law of supply

a higher price will lead to producers to supply a higher quantity and vice versa

The relationship between the law of demand and the law of supply

The law of supply and demand states that if a product has a high demand and low supply, the price will increase. Conversely, if there is low demand and high supply, the price will decrease. Market equilibrium occurs when demand and supply intersect to create a stable price. this is the price mechanism

price factors impacting supply

the market price of a good/service

😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭😭

non-price factors impacting supply

costs associated with the factors of production (like labour, raw materials)

expected future prices

number of suppliers/competition

price of complimentary goods

price of substitute goods

technology

climate and seasonal influences

movements along the supply curve

when price factors impact the price of goods/services, hence quantity supplied changes in accordance.

suggests the relationship between demand and supply remains constant

shifts of the supply curve

supply is impacted by non-price factors.

indicates the relationship between price and supply has changed

market equilibrium

occurs when quantity supplied = quantity demanded. means the market has been cleared.

market surplus

The quantity demanded is much less than the quantity supplied.

Hence, producers reduce prices to incentivise buyers.

thus, the “invisible hand” drives prices down, re-establishing equilibrium at a lower point.

market shortage

when quantity demanded is much greater than quantity supplied. as a result, consumers effectively bid up prices until equilibrium is re-established at a higher price point.

elasticity of demand

the measure of the relationship between a change in the quantity demanded and a change in its price. used when discussing price sensitivity

when is something unit elastic? (formula)

when PED (%change in demand/%change in price) = 1

when is something elastic? (formula)

when PED (%change in demand/%change in price) > 1

when is something inelastic? (formula)

when PED (%change in demand/%change in price) < 1

Relatively elastic goods

goods where demand is highly sensitive to price changes

e.g. luxury goods

relatively inelastic goods

goods where demand is insensitive to price changes

e.g. milk, bread

total revenue definition

total revenue = total income of a business. calculated by multiplying the goods sold by the price of the goods.

total revenue — elastic product

total revenue increases as price decreases

total revenue decreases as price increases

total revenue — inelastic product

total revenue increases as price increases

total revenue decreases as price decreases

significance of price elasticity to governments and businesses

helps them determine how much to supply and the price of goods and services.