Economics hell

1/79

Earn XP

Description and Tags

Save me

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

80 Terms

What is subjective and objective

Subjective value, profit

Objective - price, cost

Implicit costs

Explicit costs

sunk costs

implied/implicit cost - oppurtunity cost, it is the value of forgone benefits (that could have been saved)

Explicit costs- actual cost

Sunk cost - irreversible, it has already been spent and cannot be recovered

economic systems

traditional

barter trade system

you consume your own products

little economic progress

command

government owns everything (factors/resources)

it decides what goods or services will be produced

determines methods of productions/wages

provides healthcare/education

market

economic decision is decentralized

services/goods based on demand

private enterprises

How does job specialization increase work efficiency?

1) people can focus on what they do best

2) people can produce more quickly and high quality

3). Businesses can take advantage of ECONOMIES OF SCALE

Level of production increases, the average cost of producing each individual unit declines

Macro vs micro economics

Micro focuses on the economics of families, businesses and workers.

Macro focuses on econs as a whole. Economy of the nation

about issues like growth of production, unemployed people, the inflation increase in prices, trade balance etc.

Fiscal vs Monetary policy

Fiscal -economic policies involving taxes, exchange rates, housing etc

determined by the government

Monetary - altering interests, money supply, government budget

determined by the central bank

what are the factors that ARE and ARE NOT involved in the CIRCULAR FLOW

No:

government intervention (taxes)

foreign trade

savings (loans)

assume that :

all prices are constant

in equilibrium

always full employment

Visualize a circular flow

two main sectors - firms and households

two main markets - goods/service and factors of production (labour)

Formula for opportunity cost

Sacrifices/gains = opportunity cost

Supply demand model

demand - negative slope

supply - positive slope

X axis - quantity

Y axis - price

marginal benefit and marginal cost

MB>MC - good

MB=MC - acceptable

(both above are rational choices)

MB<MC - no good

why would someone pay to much to get so less benefits

What is equilibrium

When demand is equal to supply

No resource is wasted

Supply thing (give the law and definition)

Law of supply

Supply go up

Price go up

(Positive slope)

how much good/service is the supplier willing to supply at a given price

Movement vs Shift

Movement - price change, demand/supply change)

Shift- the price doesn't change, supply/demand change

(affected by non price factors)

Shifts usually affect the other (eg shift in supply, movement in demand)

Example of movement

Discounts, sales

List what affects demand (non price factors)

Income

Price of substitute/complement change

Changing tastes/preferences

Changes in expectations about future

Changes in composition of the population

Inferior product?

Income go down

Demand go up

goods that ppl only buy when they are poor

Elasticity??

Basically how “flexible" a price can be adjusted where ppl can still buy the product

how responsive the people are to the price

Inelastic is not flexible price

Supply shift determinents

Natural and social factors

natural conditions

Input prices (raw materials)

Numbers of sellers

technology

government policies

expectations on future prices

what is elastic, and what is not

elastic - >1

unit elastic - = 1

inelastic - <1

Price floor and ceiling

they are price controls set by the government

price ceiling is at the bottom - maximum price something can be charged

(eg necessities, so people can afford them)

(price ceilings forces shortages)

price floor at the top- minimum price something can be charged

eg cigarettes so people wont buy them

Opportunity cost

the value of the forgone alternative action or decision

what is Scarcity

unlimited human want, and limited resource

“when human wants for goods and services exceed the available supply”

Elasticity formulas (3)

ELASTICITY OF INCOME

Yield (returns to you) -Y

+Ve normal prod. -ve inferior prod

ELASTICITY OF DEMAND/SUPPLY

Price of product - P

+Ve supply -ve demand

ELASTICITY OF CROSSPRICE PRODUCT

Price of another product - X

+Ve substitute -ve complementary

Fixed cost vs marginal cost vs variable cost vs average cost

Fixed cost - cost that doesnt change with the amount produced- rental fee

variable cost - scales with amount produced- Raw materials (?)

factors of production and how they are paid

selling labour - wages

capital :

selling skill- salary

selling machines - interest

selling land - rent

selling entrepreneurial (skills?) - profit

positive vs normative economics

positive - focus on description , explanation, quantification

OBJECTIVE facts, no opinions involved, no judgement

Normative

SUBJECTIVE judgment, value based, ethical considerations etc.

production possibilities frontier

a graphical model illustrating the maximum combinations of two goods or services an economy can produce with its available resources and technology

on the line - optimum

inside the line - not using the resources to its potential

outside the line - not possible or achievable (cuz scarcity and limited resources)

the law of increasing cost

it explains the concave shape of the PPF

cuz if more goods are produced, the opportunity cost for an additional unit increases

firms main objective?

Decrease cost

shortage vs surplus

shortage - too many demand

fix by increasing price to lower the demand

surplus = too many supply

fix by decreasing price to increase the demand

and by fixing them, they return to equilibrium

complementary and substitute goods’

complementary - they go tgt

when good A demand up, the complementary product does the same

positive relationship

substitute - they “replace” the product

when good A demand up, the substitute demand goes down

inverse relationship

what is ceteris paribus

“with other conditions remaining the same, other things being equal”

demand assumptions

constant income (of the buyers)

constant prices of relative goods

unchanging preferences

constant number of buyers

all are normal goods

ceteris paribus

Demand? (law and definition)

LAw of demand

price go up, demand go down

price go down, demand go up

definition

the amount people are willing to buy

Shifting thing (what decreases and increases)

Quantity increase, price decreases - shifts right

Quantity decrease, price increase - shift left

The 4 types of economic structures (?)

Monopoly

oligopoly

monopolistic competition

(the middle 2 = imperfect competition)

perfect competition

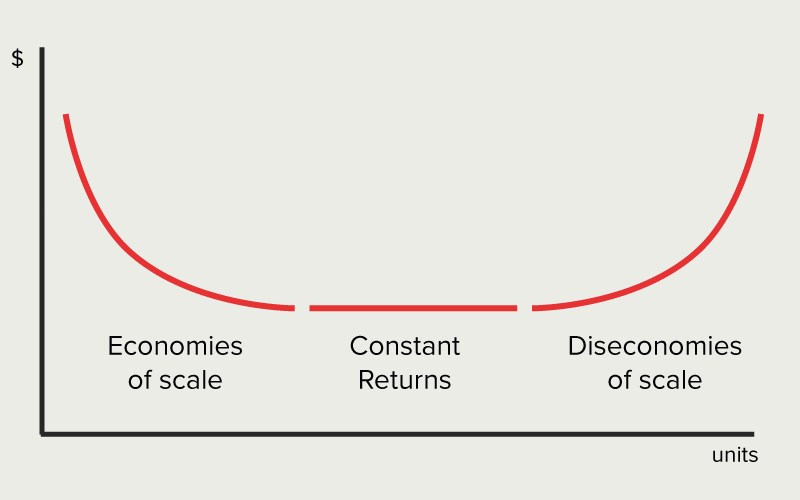

Total cost, total average cost thing

Economies of scale

Economies of scale = increasing returns (average cost gets lower)

constant returns =

Diseconomies of scale = decreasing returns ( average cost becomes higher again)

average cost go up cuz need to afford more machines, hire more ppl to cover the demand to produce more.

total revenue = ?

Total revenue = price x quantity

Profit = total revenue - total cost

Marginal cost

Cost needed to produce ONE MORE UNIT

it gets higher and higher at some point

Diseconomies of scale

Dimishing marginal returns or somethiNG>

Why can't the demand curve be vertical? (Firms charging as high they like

1) income is fixed

2) we will actively seek substitutes

Shut down vs exit

Shutdown

Shutting down a production line, but keeping labour, land and entrepreneurial skills. Basically making another product

Exit

quit everything basically. Selling all resources

Dead weight loss

An area of the graph that is a lose lose situation because it is inside the ppf which means it is underutilized. This only happens in pure monopoly (factt check this)

Monopoly power (?)

Influencing prices

Influencing output

Pricing strategies to prevent or stuffle competition

May not pursue profit maximization - encourage unwanted entrants to the market

Sometimes seen as a case of market failure

Monopolistic characteristics

Large number of firms in the industry

Small price band

May have some element of control over price due to differentiate their product in some way from their rivals - products are therefore close but not perfect , substitutes

Entry and exit from the industry is relatively easy -few barriers to entry and exit

Consumer and producer knowledge imperfect

Price maker and price takers

Price maker set prices, usually the dominating firm does it

Price takers take the price from price makers

Perfect competition caharcteristics

Horizontal demand line

Large number of firms

Products are homogenous - Consumer has no reason to express a preference for any firm

Freedom of entry and exit into and out of industry

Firms are price takers

Each producer supplies a very small proportion of total industry output

Consumers and producers have perfect knowledge about the makert

Predatory pricing

Big firms try to prevent smaller firms from entering by lowering the price (cuz they are price makers) to below their competitors cost.

Oligopoly

Price may be relatively stable across the industry - kinked demand curve (a combo of inelastic and elastic)

Potential of collusion

Behaviour of firms affected by what they believe their rivals might do - interdependence of firms

Goods could be homogeneous or highly differentiated

Branding and brand loyalty may be a poten source

Game theory

kinked demand curve

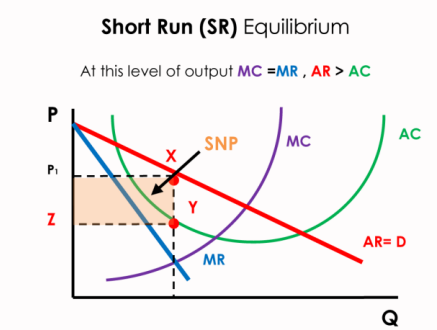

WTH is a supernormal profit ???

Supernormal Profit = Total Revenue - Total Cost

The orange area

the profit a firm earns above and beyond the normal profit, calculated by subtracting both explicit and implicit costs from total revenue. (then why is it called super normal profit??)

Supernormal profit is the excess profit a business makes after covering all its costs, including the minimum amount needed to keep the business running (normal profit). It's calculated by subtracting all total costs (both explicit and implicit) from total revenue. In simple terms, it's the "extra" profit earned above what is just necessary to stay in business. “

often temporary

Imperfect competition

number of independent firms in

Aim of firm is to maximise profits industry

Product differentiation exists.

The products are not homogenous and competitive advertising occurs

Free entry/exit of firms to/from the market

Knowledge is widespread each competitors know what the other is earning

Many buyers of the goods produced in the industry

Concentration ratio

an economic metric that measures the dominance of a few firms in a market by summing the market shares of the largest firms, typically expressed as a percentage.

shows market structure

CR4- Concentration ratio of 4 companies

CR8 - 8 companies , measures market

Long run vs short run

In short run

in long run, many short runs make it up (?) variable cost (uhhh)

Law of diminishing returns

When MPL is more than 0, MPL declines as more labour is hired. (or any marginal product like land, capital)

when MP at maximum and MC at minimum.

Accounting profit vs economic profit

Accounting - minus explicit ONLY

Economic - minus explicit and implicit (oppurtunity cost)

relationship between MC and MP

The relationship is inverse ,both of them slope upwards, but MC gets steeper and steeper while MP gets flatter and flatter.

Why is 1 season a short run?

Short run - at least one fixed input ( factors of production) (capital, labour, land , entrepreneurial skills)

Cuz you fix one to see which is the most efficient (observe what is most optimum)

MIDPOINT FORMULA!!!!

Economics of scale

When minimum points of all possible SRATC (short run average total cost ) become lower as quantity of output

The kinked demand curve - where it appears and what it is

Appears in oligopoly

it has both inelastic and elastic properties (?)

elastic cause drop in price

inelastic causes raised price for revenue

what does macroeconomics examines?

examines Performance and behavior affected by :

government policies

central banks (federal reserve in ‘murican books) financial institutions

Actions of other economies (other countries)

aggregate economics units and phenomena

What are the ceaseless activities?

Activieties that keep happening

recession

inflation

economic growth

unemployment

2 types of GDP

Nominal

real

3 causes of inflation

3 types of unemploment

Frictional quit a job to get another (short term)

Structural (long) (fired!!) - cuz your skills are no longer required (change in industry, technological advancement )

Cyclical - due to recessions

whats NRU

Natural something unemployment

tools of monetary policy

fiscal policy

Constant returns of scale?

The flat part of the long run graph

Diseconomies of scale

definition of inelastic

Inelastic means that a 1% change in the price of a good or service has less than a 1% change in the quantity demanded or supplied.

GDP (definitiions)

gross domestic produce

Market value of all the final goods and services produced within a countries borders in a given period

only final goods (intermediate goods are excluded to prevent double counting)

only legal goods

What is CPI

How to calculate inflation rate from CPI