Introduction to Microeconomics Vocab Lists 2 & 3

1/29

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

30 Terms

Labor

effort that goes into work

Capital

money, assets, and resources that help produce value and wealth

Oligopoly

when a small group of companies dominate an industry, which limits competition

monopoly

one producer dominates an industry

Supply

the amount of the good available for producers to sell

Demand

desire, willingness, and ability to buy a good/service at various prices

Incentives

a chance of reward or punishment that motivates someone to act in favor of their goal

Scarcity

limited quantity of resources and unlimited wants

Trade-offs

alternative choices you let go of when you decide to do something

Opportunity Cost

the second-best choice you let go of when you make a decision

Invisible Hand

A concept created by Adam Smith saying that producers will be guided to produce what the public wants

Perfect Competition

A market structure in which sellers & buyers exchange an equal/homogeneous good and no individual can influence the market price

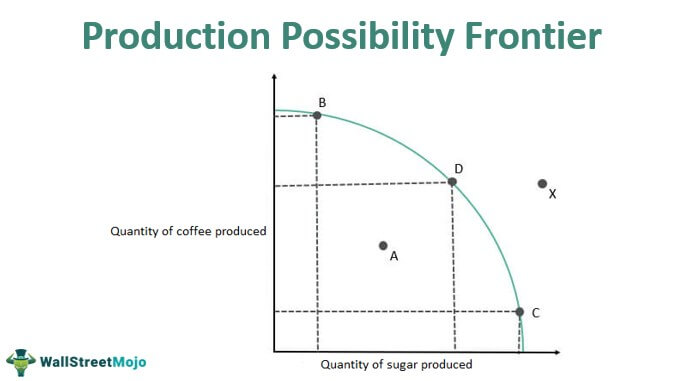

Production possibilities frontier

A graph showing the maximum possible combinations of two goods/services that an economy can produce

Entrepreneurship

the process of designing, launching, and managing a new business

Diminishing Marginal Utility

the satisfaction you get from consuming one good/service lessens the more units you consume

Demand curve

A graph representing the relationship between the price of a good/service and the quantity consumers are willing to buy

Equilibrium

when supply and demand are balanced

Law of demand

as price increases, demand decreases & vise versa

Law of supply

as price increases, supply increases

Price ceiling

the maximum legal price for a good/service imposed by the government (or other authority)

Price floor

the minimum legal price for a good/service imposed by the government (or other authority)

Shortage

A temporary situation in which there is less supply than there is demand

Supply Curve

A graph representing the relationship between the price of a good/service & the quantity producers are willing to sell

Surplus

when quantity supplied exceeds quantity demanded and the actual price of a good is higher than the equilibrium

Elasticity

the change in price & its effect on other economic factors (such as demand, supply, incentive, etc.)

Normal Good

A product/service for which demand increases as a consumers income rises & demand decreases as a consumers income falls

Inferior Good

A product/service for which demand decreases as a consumers income rises & demand increases as a consumers income falls

Externality

when a cost or benefit caused by a certain party involved in the production of a good/service doesn’t affect that same party.

Complements

goods/services that are consumed together, where a decrease in price for one leads to an increase in demand for the other

Price Elasticity of demand

A measure of how quantity demanded changes in response to a change in its price