CFA L1 Fixed Income: Curve-based and Empirical Duration

1/8

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

9 Terms

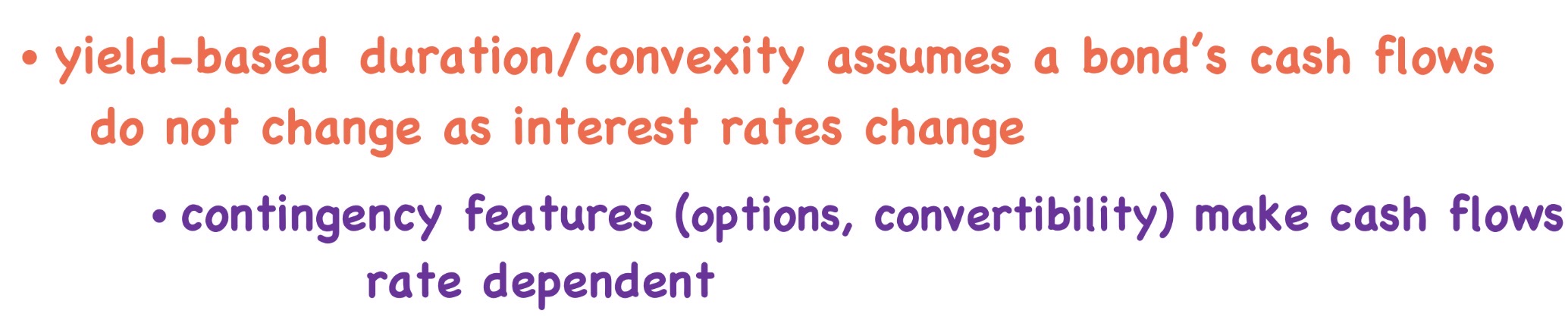

How do contingency factors (options, convertibility) impact cash flows?

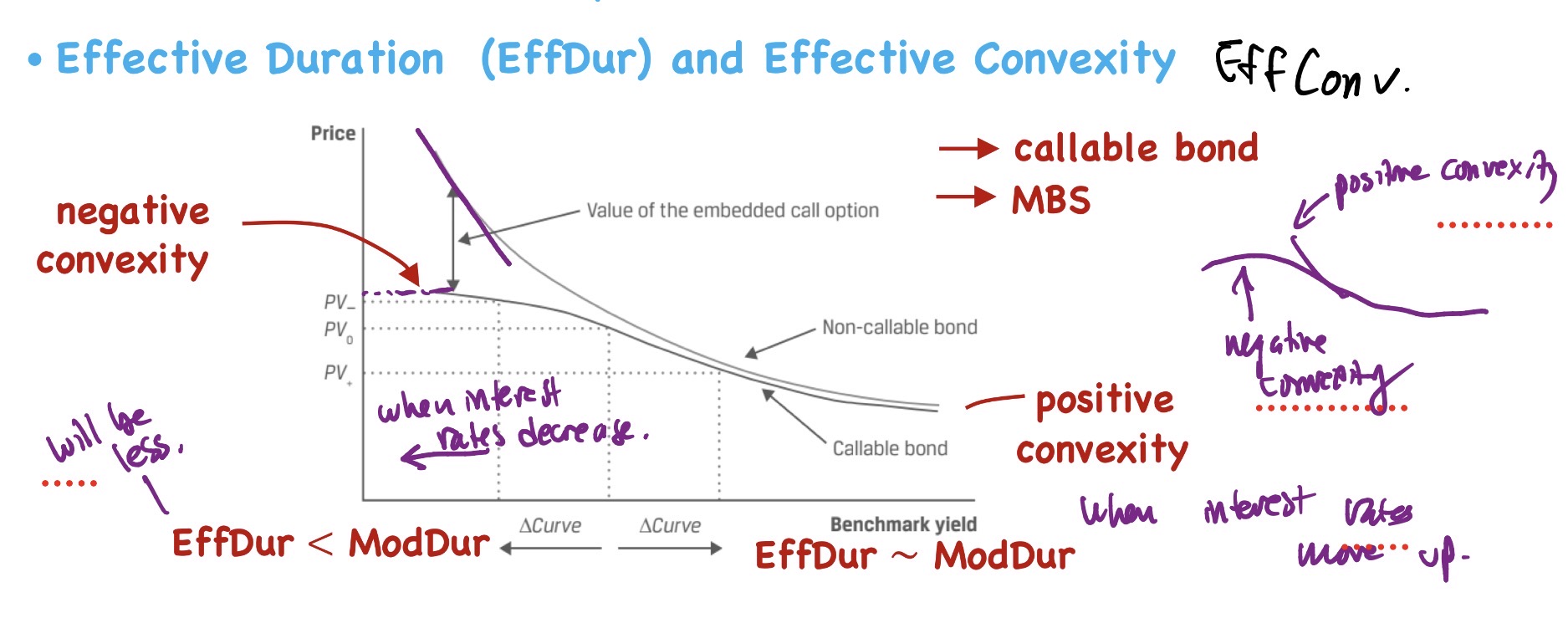

For callable bonds, as interest rates get higher, are the Effective duration or the Modified duration higher? What if interest rates are lower?

For putable bonds, as interest rates get higher, are the Effective duration or the Modified duration higher? What if interest rates are lower?

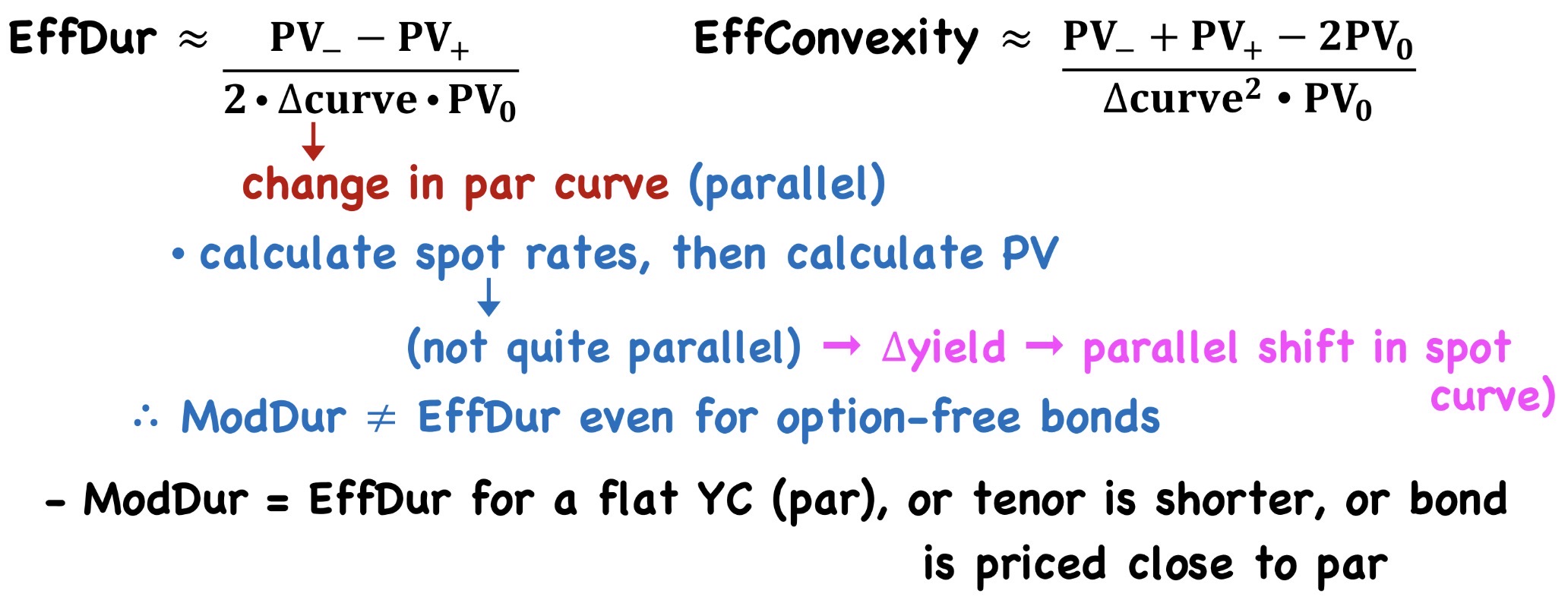

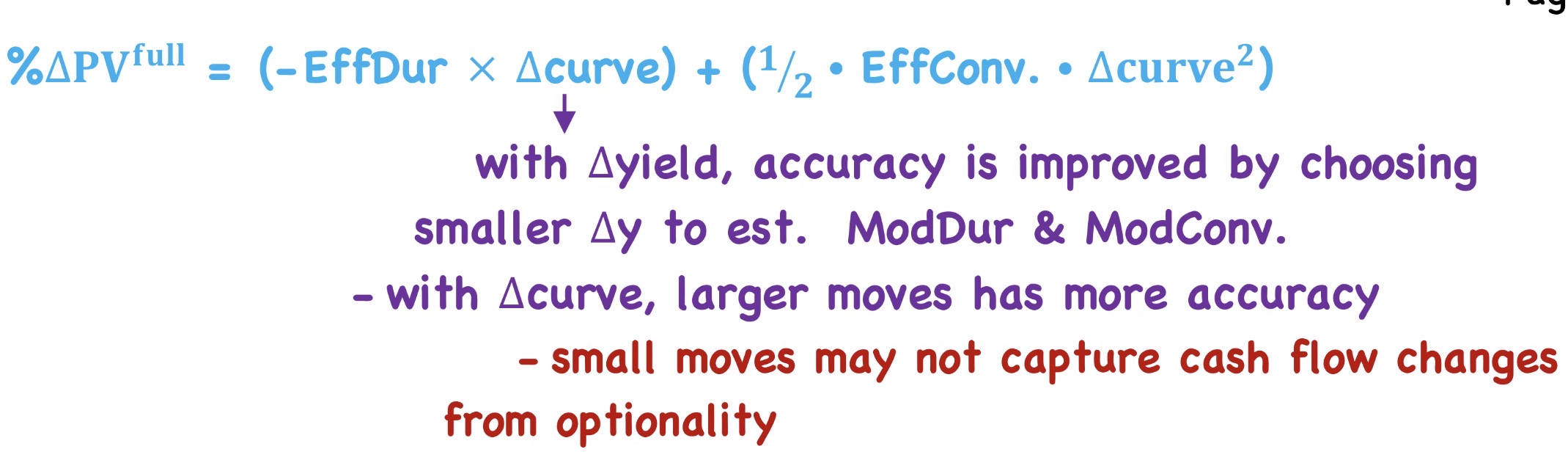

Effective duration and effective convexity formula (memorize!)

Percent price change of bond given effective duration and convexity (memorize!)

Key rate duration definition

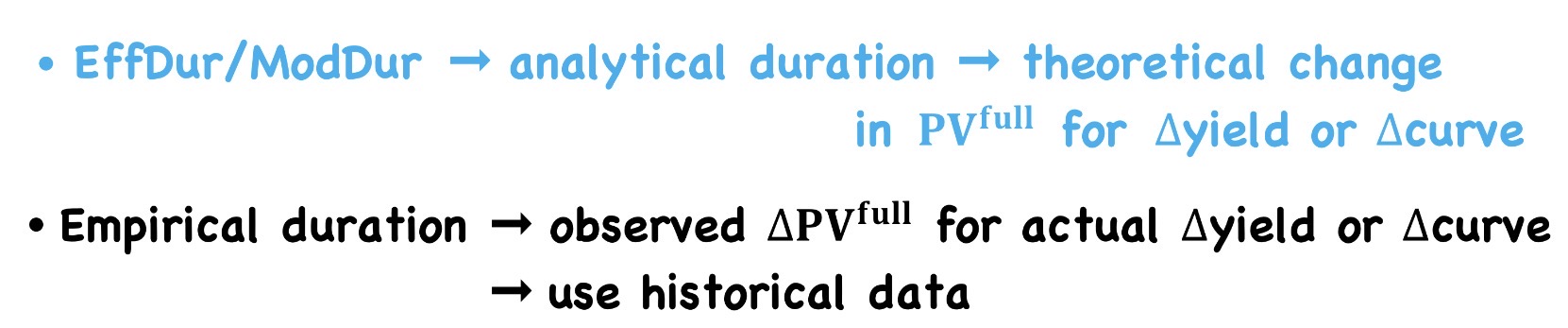

What is empirical duration and how is it different from effective duration and ModDur?

What is the empirical duration equal to for government bonds?

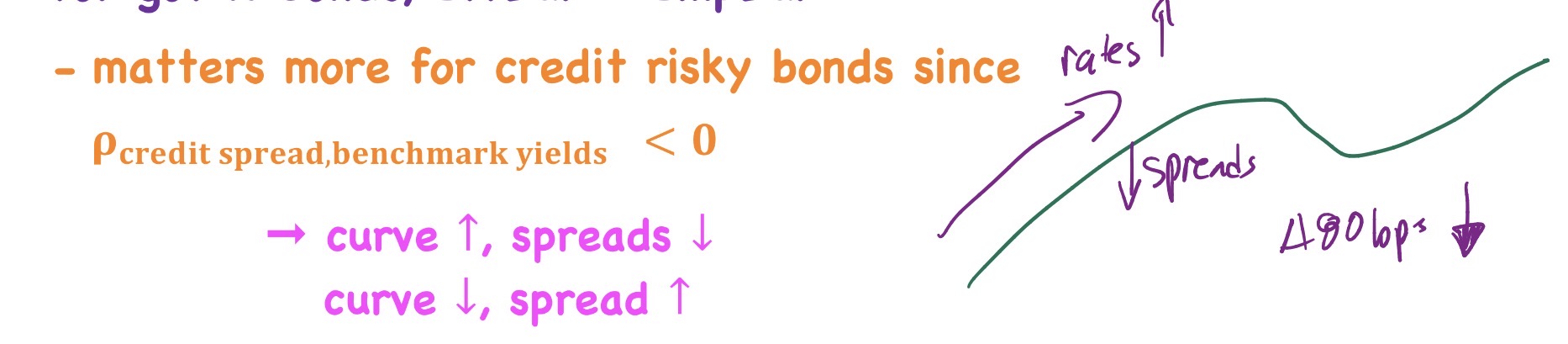

What is the relationship of curves and spreads for credit-risky bonds?