2.3 The Firm (Costs of Production)

1/59

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

60 Terms

Total revenue

Selling price multiplied by quantity sold

Profit

Occurs when selling price is greater than costs of production

Subnormal profit

Profit that is earned below normal profit; Average cost is greater than average revenue

Normal profit

The minimum amount of profit which the entrepreneur needs to earn in the short run to keep resources in their present use in the long run; Average cost is equal to average revenue

Supernormal/Abnormal/Economic profit

The profit earned in excess of normal profit; Average revenue is greater than average cost

The Short Run

A period of time during which at least one factor of production is fixed in supply

The Long Run

A period of time in which all of the factors of production can be varied in quantity

The Law of Diminishing Marginal Returns

If increasing quantities of a variable factor of production are added to a given quantity of a fixed factor of production, eventually a point will be reached where the addition to the total output begins to decline

Does the Law of Diminishing Marginal Returns apply in the short run or in the long run?

Only in the short run, as it is only in the short run that at least one input is fixed

What are the assumptions that underlie the Law of Diminishing Marginal Returns?

Technology remains constant, Constant quality, One fixed factor

Why must technology be constant for the LDMR to apply?

If a technological breakthrough occurs, and there are advancements in technology then the law begins again from the start

Why must quality be constant for the LDMR to apply?

The variable factors added to the fixed factor must be of the same quality so they have the exact same skill and education as the previous workers

Why must one factor be fixed for the LDMR to apply?

It only applies in the short run, so one factor will be fixed

Fixed Costs

Costs that do not change as output changes

Variable Costs

Costs that vary as output changes

Examples of Fixed Costs

Rent, Mortgage, Managerial Salary

Examples of Variable Costs

Raw materials, Wages, Utility Bills

A business will survive in the short run if they cover what kind of cost?

Variable Costs

Why can a business survive if they cover their variable costs?

Fixed costs may not have to be paid for a period of time, whereas variable costs are an immediate liability. A business will survive in the short run if their revenue can cover their variable costs as they can negotiate an extension on payment of their fixed costs, and any extra profit can go towards repayment.

Total Costs

Both fixed and variable costs added together; How expensive it is to produce a product when all factors are considered

Average Fixed Cost

Fixed costs divided by the number of units produced

Average Cost

The total of average fixed and average variable costs

Marginal Cost

The additional cost to produce one extra unit of a good

Explicit Costs

The monetary costs a firm pays for inputs. They require a cash outlay by the firm.

Example of Explicit Costs

Rent, Wages

Example of Implicit Costs

The owner’s time and investment into the firm

Implicit Cost

Non-monetary costs that are often hard to quantify

Sunk Costs

Costs incurred by a firm that cannot be recovered if the firm ceases trading

Profit Maximisation

MR = MC

Marginal Revenue

The extra revenue generated from selling an extra unit of output

Average Revenue

The revenue per unit sold

Show the relationship between TC, FC and VC on a graph

TC = FC + VC

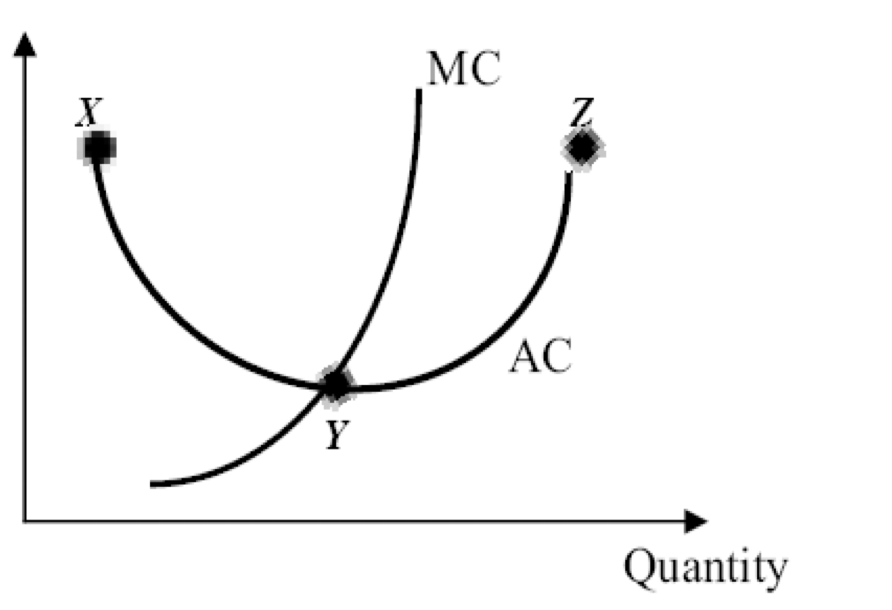

Show the relationship between MC and AC on a graph

Why does the SRAC curve slope downwards?

Fixed costs spread over larger output: AC is high when quantity produces is small as the fixed costs are spread over a small output, as units produced increases the unit cost falls

Specialisation: Existing workers become more efficient resulting in lower unit costs due to less mistakes

Why does the AC curve slope upwards?

Law of Diminishing Marginal Returns: After the optimum point AC tends to rise as the LDMR begins to

What is the relationship between MC and AC?

When MC is less than AC then AC is falling

When MC is greater than AC then AC is rising

When MC is equal to AC it is the lowest/optimum point

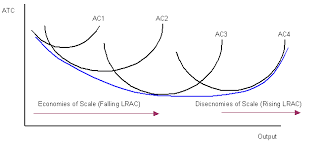

What is the relationship between SRAC and LRAC

Firms always operate in the short run, so the long run is a series of short run average cost curves

As the firm expands it will have different factory sizes and hence different SRAC curves

It will always wish to produce at the lowest point on the SRAC curve

We end up with a hollow U-shaped LRAC curve like above

Economies of Scale

The forces at work which result in a reduction in the LRAC of production as the firm increases its size of operation

Internal Economies of Scale

Forces at work within a firm that cause the average costs of that firm to decline as the firm expands

Labour Economies

A job can be separated into components, workers can become more skilled, efficient and thus specialised, increasing output per worker

Purchasing Economies

Large firms may be able to avail of discounts when purchasing raw materials, lower supply costs when buying in bulk

Financial Economies

Larger firms may have access to a greater range of finance options and may be able to borrow at lower rates of interest

Managerial Economies

Large firms can attract the best managers which can motivate and then inspire staff, they can reduce inefficiencies and thus the average cost of production

Technical Economies

Larger firms can afford the most advanced technology which increases efficiency and reduces production costs

External Economies of Scale

Forces outside a firm that cause the average costs of all firms to decline as the industry expands

Better infrastructure

As roads and communications improve then all firms will benefit from shorter delivery times, better communication and less fuel usage

Support from Public Bodies

Some public bodies help particular industries by providing grants and subsidies which reduces the unit cost of production

Development of separate R & D units

As the industry becomes very large, R&D agencies may set up to provide facilities for individual firms

Diseconomies of Scale

Forces at work which result in an increase in the LRAC of production as the firm expands

Internal Diseconomies of scale

Forces within a firm that cause the average costs of that firm to increase as the firm expands

Managerial Diseconomies

The bigger the firm, the harder it is to manage. The directors may not know all the necessary information which can result in communication problems

Interest of workers

Workers may feel like a cog in the wheel of production, they may lose motivation and mistakes increase which makes them less efficient and increases cost per unit

Unproductive staff

The firm must hire solicitors, accountants and other employees who do not directly contribute to producing goods and thus increase the average cost of producing a product

External Diseconomies of Scale

Forces at work outside a firm that cause the average cost of all firms to increase as the industry expands

Increased Demand for Labour

Skilled labour becomes very short in supply causing wages to rise, and firms may be forced to employ less skilled workers, costs will increase

Greater need for infrastructure

Greater demands are made on the economy’s infrastructure, the current state may be inadequate. Traffic congestion leads to increased delivery time which increases the cost of distributing the product

How can the government improve the competitiveness of small firms?

Reduce the minimum wage: Employers could get cheaper labour and reduce costs, they could negotiate to lower PAYE and limit pay rises.

Reduce utility charges: Reducing costs for electricity, gas, postage and waste charges would reduce the costs of production.

Develop infrastructure: Improvement of roads and broadband would make it easier for small businesses to operate effectively.

Why do small firms survive in the Irish Economy?

Small size of market: The restricted size may not facilitate the operation of large-scale business, like in a rural area.

Personal services: Consumers may desire personal attention and a small firm will be the only type to provide this.

Consumer loyalty: A small firm may have built up a reputation over the years in the provision of goods and services and consumers may be loyal.

Economic advantages of falling production costs for the Irish economy:

Increased Competitiveness: With lower costs, prices may fall for Irish goods and exports may become cheaper.

Lower Prices: Inflation may fall and this could entice consumers to purchase more goods.

Increased employment: With rising demand, businesses may increase demand for labour.

What objectives might a firm have other than profit maximisation?

To become a takeover target: some firms build a business that may not generate profit, and have specific assets valuable to other firms, causing them to be bought out to eliminate competition.

To satisfy a sufficient level of profit: Increasing output involves financial risks that entrepreneurs aren’t willing to put in, so they will just build a business to a normal level of profit.

To alleviate a social/environmental problem: Social enterprises build businesses to provide a solution to a particular problem rather than pursue profits.