Looks like no one added any tags here yet for you.

One Period Static model of liability

Check pic for more info

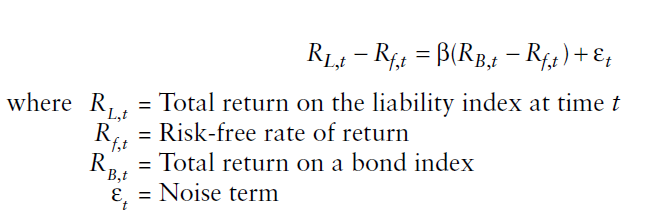

the \beta can be calculated as

Liability duration/approximate bond duration (Bond Index Duration)

Describe a series of unknown payment of pension fund

Mortality rates, where life expectancy may increase due to trends in lifestyle and/or healthcare

Future salary growth, where the actual salary growth is higher than expected or one-time benefit increases are applied

Employee demographics, where the demographics of the retired population differ from expected, e.g. a company may offer incentives for early retirement or is obligated to terminate a portion of the workforce

Two shortcomings to measure the tradeoff between risk and return using Sharpe ratio

First, the Sharpe ratio considers only the risk and return of assets and ignores the presence of the liability stream

A second shortcoming of the sharp ratio in the present context is that it’s really only a theoretically well-founded concept in one period model, and it doesn’t work well for multi period time being

What’s funding ratio

F_t = A_t/L_t

Formula will be provided for this chapter

Compare and contrast the managing of a defined benefit pension plan vs. a life insurance fund.

Differences

o Insurers are taxable

o Portfolio segmentation is a distinctive feature of life insurers

• Similarities:

o Both a long-term liabilities

o Both typically use an ALM approach to SAA

ALM considerations include yield, duration, convexity, key rate sensitivity, value at risk, and the effects of asset risk on capital requirements

o Both face contractual liabilities to insureds

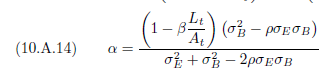

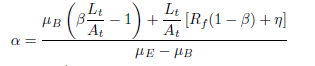

The surplus risk is minimized when an equity equals to

Minimum equity allocation needed for a fund to prevent the surplus from shrinking

Underfunded plans benefit more from higher equity allocations than do overfunded plans

Underfunded pension plans often benefit more from higher equity allocation because they need higher returns to closing funding gaps

Matching the duration of the bond portfolio to that of liabilities is important for all plans with underfunded plans benefiting the most

Global equity diversification is an attractive opportunity for overfunded plans, which can benefit from the highest sharp ratio of global equity. Unrefunded plans are better off investing domestically in order to benefit from the high correlation of liabilities with domestic assets

Fixed income diversification is not attractive for any of the plans studies. The effect of increase in sharpe ratio of assets from moving to global fixed income is more than offset by low correlation of liabilities with nondomestic bonds