CFA L1 - Definitions and Formulas

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

13 Terms

Equilibrium Interest Rate

Required rate of return for a particular investment, in the sense that the market rate of return is the return that investors and savers require to get them to willingly lend their funds.

Real risk-free rate

theoretical rate on a single-period loan that contains no expectation of inflation and zero probability of default.

Time preference

the degree to which current consumption is preferred to equal future consumption. Represented by the real-risk free rate

Nominal risk free rate

Nominal risk-free rate = real risk free rate + expected inflation rate + default risk premium + liquidity risk premium + maturity premium

Default risk

This is the risk that a borrower will not make the promised payments in a timely manner.

Liquidity Risk

This is the risk of receiving less than fair value for an investment if it must be sold quickly for cash.

Maturity risk

the prices of longer-term bonds are more volatile than those of shorter-term bonds. Longer-maturity bonds have more maturity risk than shorter-term bonds and require a maturity risk premium.

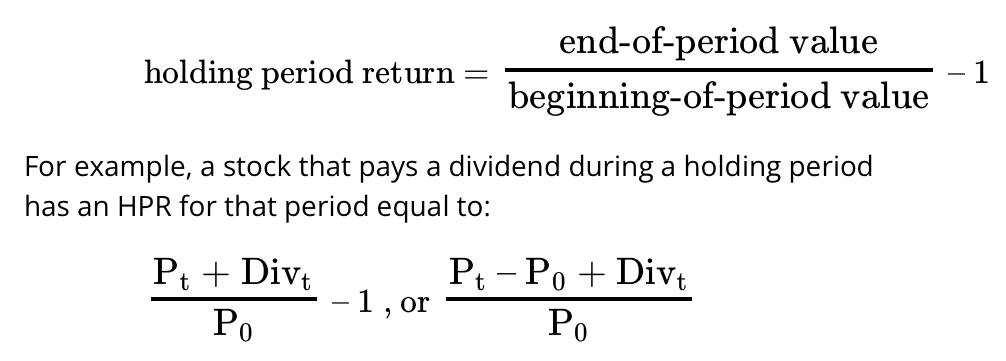

Holding period return (HPR)

the percentage increase in the value of an investment over a given period

Arithmetic mean return

the simple average of a series of periodic returns

Geometric mean return

a compound rate. When periodic rates of return vary from period to period, the geometric mean return will have a value less than the arithmetic mean return

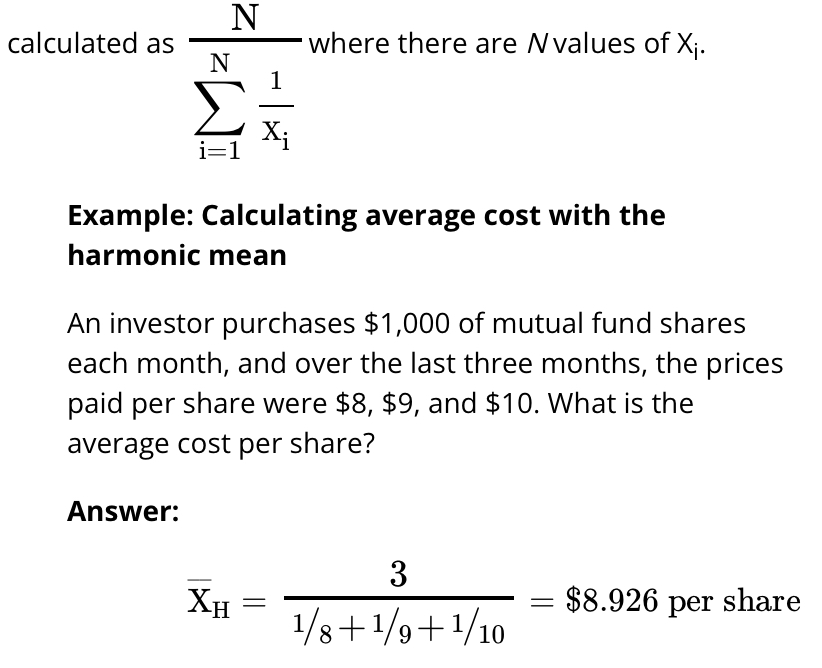

Harmonic mean

used for certain computations, such as the average cost of shares purchased over time

Money weighted return

applies the concept of the internal rate of return (IRR) to investment portfolios. An IRR is the interest rate at which a series of cash inflows and outflows sum to zero when discounted to their present value. That is, they have a net present value (NPV) of zero. defined as the IRR on a portfolio, taking into account all cash inflows and outflows. The beginning value of the account is an inflow, as are all deposits into the account. All withdrawals from the account are outflows, as is the ending value.

Time weighted rate of return

measures compound growth and is the rate at which $1 compounds over a specified performance horizon. Time-weighting is the process of averaging a set of values over time. The annual time-weighted return for an investment may be computed by performing the following steps:

Step 1: | Value the portfolio immediately preceding significant additions or withdrawals. Form subperiods over the evaluation period that correspond to the dates of deposits and withdrawals. |

Step 2: | Compute the holding period return (HPR) of the portfolio for each subperiod. |

Step 3: | Compute the product of (1 + HPR) for each subperiod to obtain a total return for the entire measurement period [i.e., (1 + HPR)1 × (1 + HPR)2 . . . (1 + HPR)n] – 1. If the total investment period is greater than one year, you must take the geometric mean of the measurement period return to find the annual time-weighted rate of return. |