EC3333 Midterm Formulas

1/48

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

49 Terms

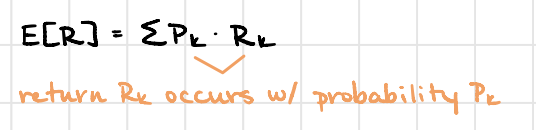

expected return

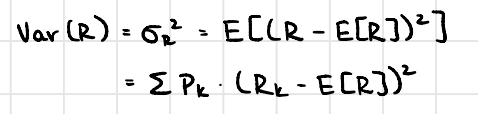

variance

variance estimate

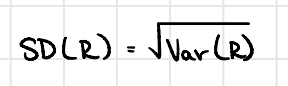

standard deviation

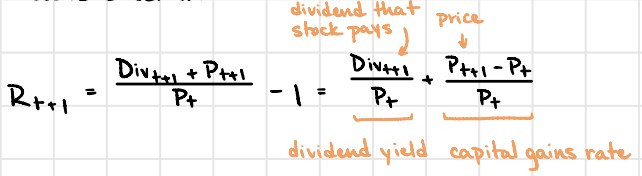

realized return

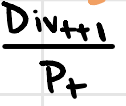

dividend yield

annual realized return

average annual return

compound annual return

standard error

95% confidence interval

expected portfolio return - risky only

covariance

covariance estimate

correlation

portfolio variance (2-asset)

portfolio variance (n-asset)

portfolio variance using each asset’s cov with the portfolio

portfolio volatility

minimum variance portfolio weights

minimize variance w.r.t weight s.t weights add to 1

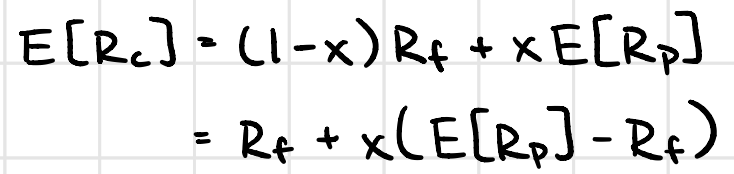

expected portfolio return - complete

complete portfolio volatility

capital allocation line

Sharpe ratio

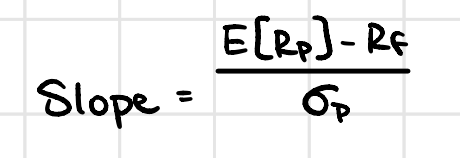

slope of CAL

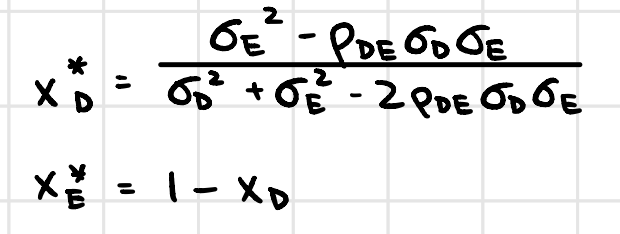

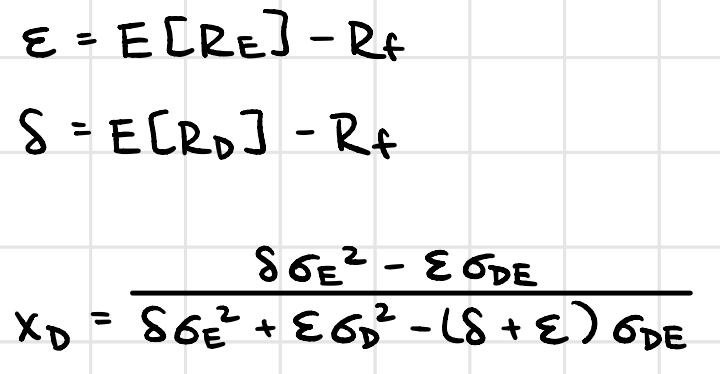

optimal risky portfolio weights

maximize Sharpe ratio s.t. we are on the efficient frontier

required return

beta - individual stock

correlation using sharpe ratios of i and P

assumes P is efficient —> Sharpe ratio is maximized, E[Ri] = ri

![<p>assumes P is efficient —> Sharpe ratio is maximized, E[Ri] = ri</p>](https://knowt-user-attachments.s3.amazonaws.com/aa6c1293-0b4d-489c-9ad4-0816464cea0c.png)

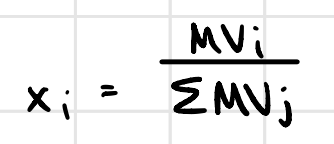

market cap

value-weighted portfolio

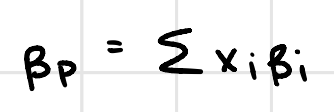

beta - portfolio

SML

alpha

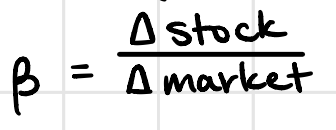

beta with stock changes vs. market portfolio changes

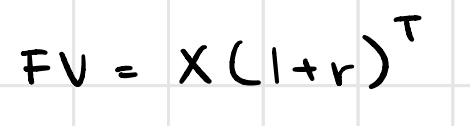

future value

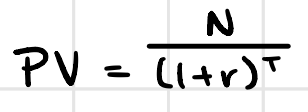

present value

EAR

APR

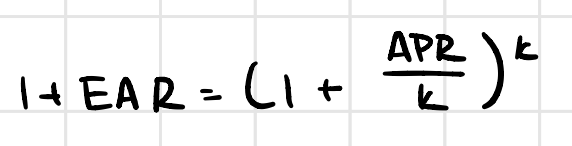

relating EAR and APR

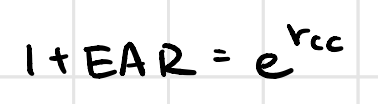

EAR with continuous compounding

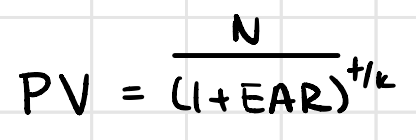

PV using EAR

fisher reltaion

rule of 72

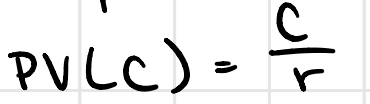

PV of perpetuity

PV of annuity

FV of annuity

NPV

PV of growing perpetuity

PV of growing annuity