Tax Lecture 7

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

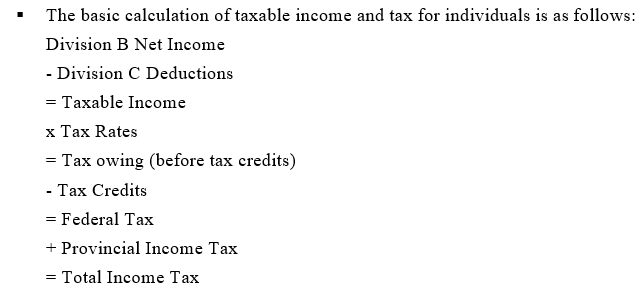

Overview of computation of taxable income and tax for and individaul

Stock Option Deduction

Deduction of 50%

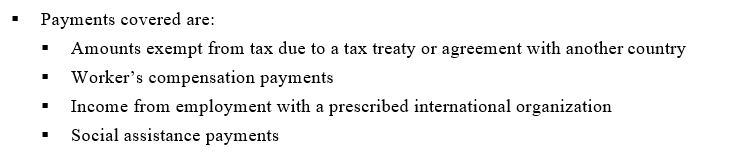

Deduction for payments not taxed but taken into net income consideration

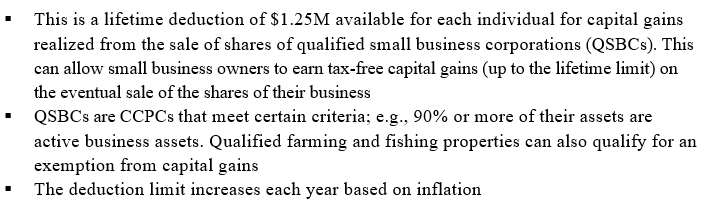

Capital Gains Exemption

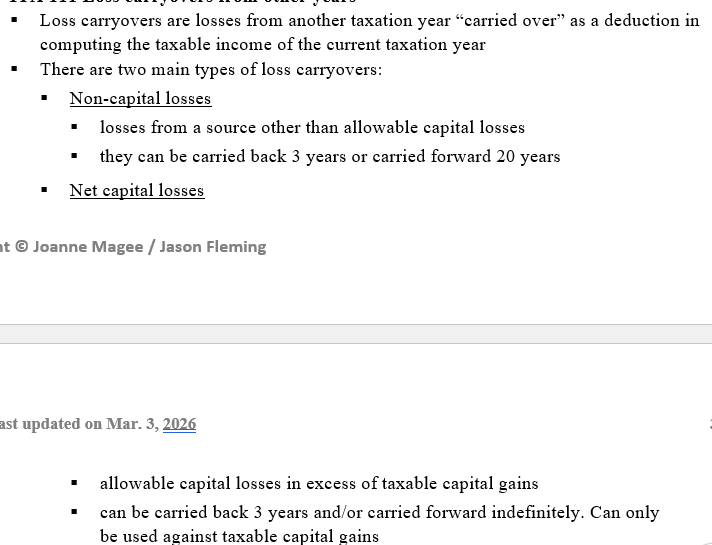

Loss Carryovers from others years(With examples)

Basic Personal Credit

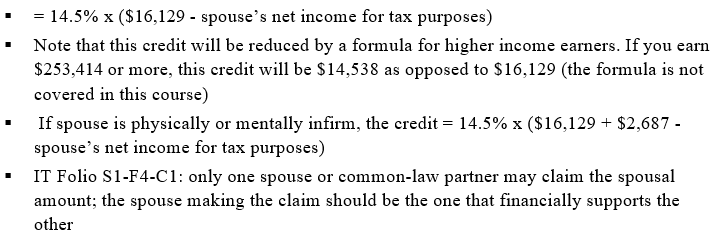

Spousal Credit

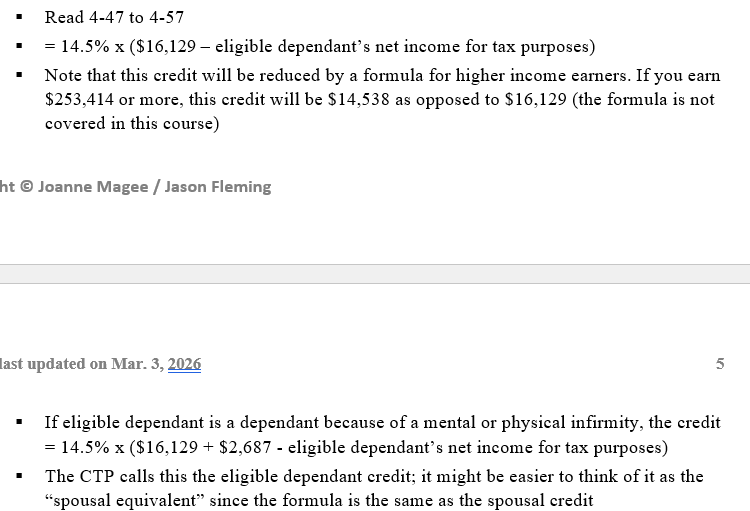

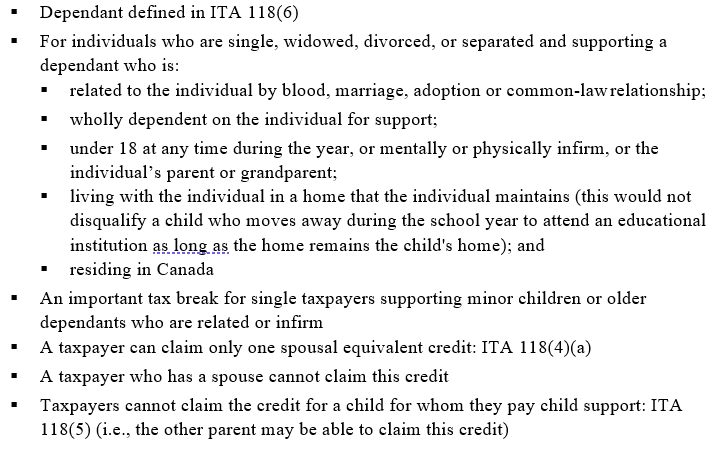

Individuals Supporting an Eligible Dependant

Define an Dependent

Explain The eligible dependent and spousal equivlaent credit relationship and canada caregiver tax credit

to do

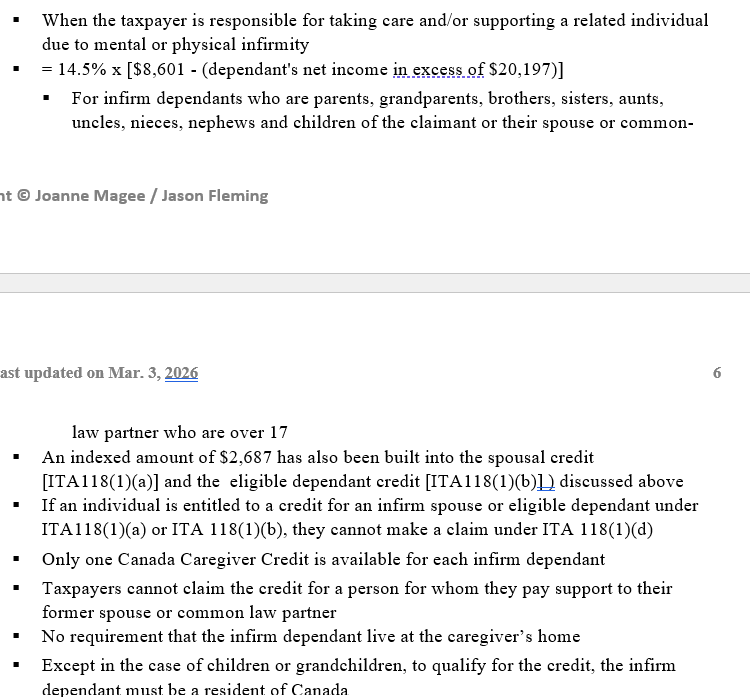

Canada Caregiver Amount for Child

Canada Caregiver Tax Credit

Canada Caregiver credit - Additional amount

When the credit for an infirm spouse [ITA118(1)(a)] or infirm eligible dependant [ITA118(1)(b)], is less than the Canada Caregiver amount

Entitled to an additional amount of credit base that would bring the credit up to the amount of the regular caregiver amount

Age Credit

Seniors who are 65 or older at the end of the year are eligible. Can transfer unutilized credit to spouse.

Pension Credit

= 14.5% x first $2,000 of "pension income" = $290 maximum (not indexed)

If age 65 or older at year-end and have “eligible pension income” (i.e., employer RPP payments, RRSP annuity payments, RRIF payments)

“pension income” excludes: OAS, CPP, Quebec Pension Plan (QPP), lump sum withdrawals from an RRSP, and certain other amounts [ITA 118(8)]

If under age 65, the credit is limited to “qualified pension income”, which is basically employer RPP (registered pension plan) payments according to ITA 118(7)

Can transfer unutilized credit to spouse [ITA 118.8]

Canada Employment Tax Credit

§ Must have Canadian employment income

§ = 14.5% x lesser of

§ $1,471; and

§ net employment income (calculated without any employee expenses allowed under section 8 of the Act)

Adoption Expenses Credit

Can only be claimed in the year when adoption is finalized (the expenses can be incurred over several years) to a maximum of $19,580 per adoption

= 14.5% x the eligible adoption expenses (up to the maximum of $19,580) = $2,839 maximum

If child adopted by couple, credit can be shared (usually the higher-income spouse will claim the credit)

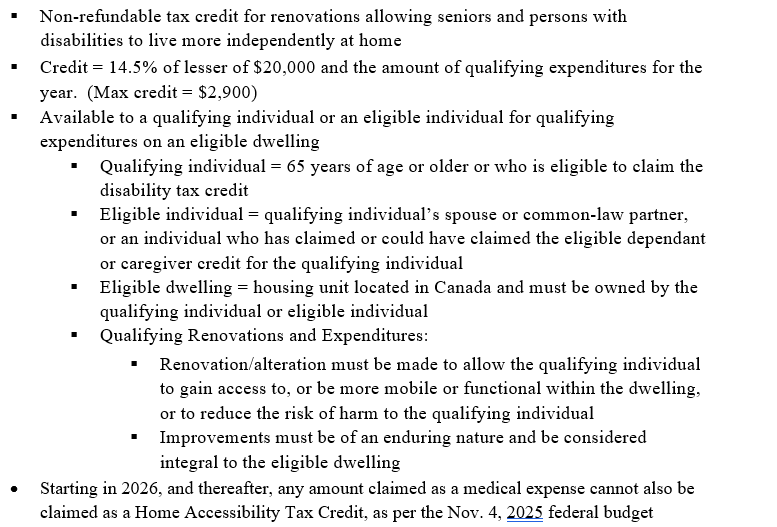

Home Accessibility Tax Credit

Medical Expenses Credit (do the inclass example)

Credit for taxpayer who pays the eligible expenses (or the taxpayer’s spouse)

Can claim expenses paid for any 12-month period ending in the year

Disability Credit

A person qualifying for this credit can transfer any unutilized credit to a spouse or supporting person who could have claimed the person as eligible dependant credit, caregiver tax credit, or a disabled dependant over 17

Tuition Credit

all mandatory ancillary fees imposed on all students and

allows up to $250 ancillary fees not imposed on all full-time or all part-time students

the cost of examination fees paid in order to obtain professional status recognized by federal or provincial statute (e.g., CPA final examination fees)

entrance exam fees paid in order to begin study in a profession or field are not eligible

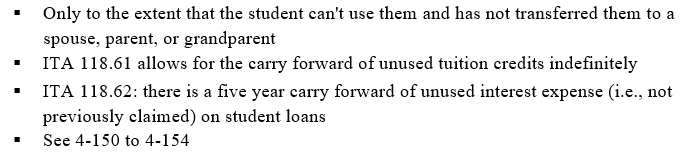

Carry Forward of Education-related Credits

§ ITA 118.9: can transfer to a parent or grandparent

§ ITA 118.8: can transfer to a spouse or common-law partner

§ ITA 118.81: the transfer amount is limited to the lesser of

§ the available credits and $5,000 (per year)

§ The transferred credit is then multiplied by 14.5% in 2025 (14% in 2026 and thereafter)

§ Taxpayers can only transfer these credits to the extent that they do not need them

EI & CPP (where is EI and CPP before credits (figure out)

Taxpayers earning employment income have EI & CPP premiums withheld from their pay (employers also pay a premium). The employee can claim tax credits = 14.5% of the EI & CPP premiums paid by them. The employer pays the same (i.e., matches) the CPP paid by the employee (and the employer deducts the amount that it pays)

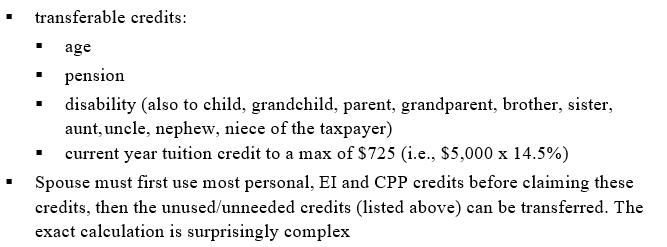

Transfer of Unused Credits to spouse

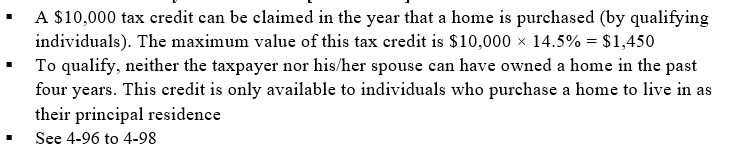

First Time Home Buyers Tax Credit

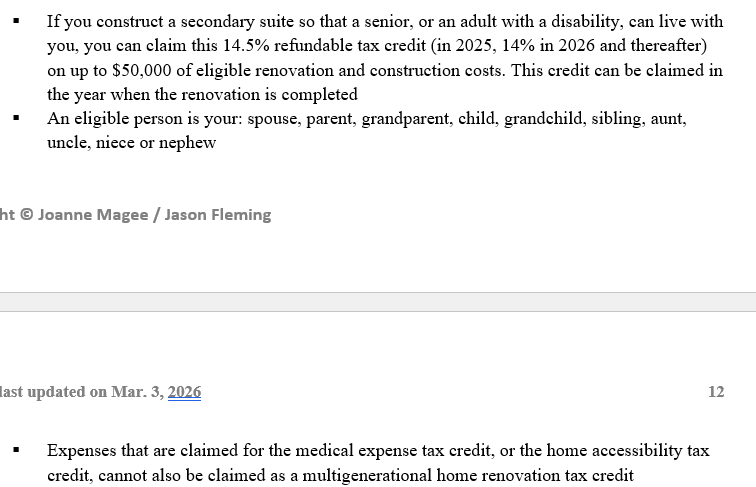

Multigenerational Home Renovation Tax Credit

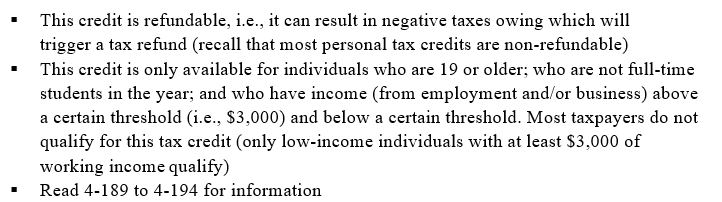

Canada Workers Benefit credit

List all refundable credits (search up)

Do problemm case