Lvl2: Economics

1/38

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

39 Terms

covered interest rate parity

Ff/d = Sf/d × [1 + if(actual/360)]/[1 + id(Actual/360)]

The domestic currency will trade at a forward premium (Ff/d > Sf/d) if, and only if, the foreign risk-free interest rate exceeds the domestic risk-free interest rate (if > id).

![<p><span>F<sub>f/d</sub> = S<sub>f/d</sub> × [1 + i<sub>f</sub>(actual/360)]/[1 + i<sub>d</sub>(Actual/360)]</span></p><p>The domestic currency will trade at a forward premium (<em>F<sub>f</sub></em><sub>/</sub><em><sub>d</sub> > S<sub>f</sub></em><sub>/</sub><em><sub>d</sub></em>) if, and only if, the foreign risk-free interest rate exceeds the domestic risk-free interest rate (<em>i<sub>f</sub></em> > <em>i<sub>d</sub></em>).</p>](https://assets.knowt.com/user-attachments/9dafa96a-d481-48e3-92fa-553d4ee45547.png)

uncovered interest rate parity

change in spot rate over the investment horizon should, on average, equal the differential in interest rates between the two countries

country with the higher interest rate or money market yield will see its currency depreciate

evidence that uncovered interest rate parity works better over very long-term horizons

forward rate parity - covered rate parity + uncovered rate parity

forward exchange rate will be an unbiased predictor of the future spot exchange rate

relies on risk neutral speculators

forward exchange rates are typically poor predictors of future spot exchange rates in the short run. Over the longer term, uncovered interest rate parity and forward rate parity have more empirical support.

purchasing power parity (PPP)

law of one price - identical goods should trade at the same price across countries

over shorter horizons nominal exchange rate movements may appear random, over longer time horizons nominal exchange rates tend to gravitate toward their long-run PPP equilibrium values.

absolute PPP

Pf = (Sf/d)(Pd)

equilibrium exchange rate between two countries is determined entirely by the ratio of their national price levels

relative PPP

percentage change in the spot exchange rate (%ΔSf/d) will be completely determined by the difference between the foreign and domestic inflation rates (πf − πd)

currency of the high-inflation country should depreciate relative to the currency of the low-inflation country.

Fisher effect

foreign–domestic nominal yield spread is determined solely by the foreign–domestic expected inflation differential

assume that currency risk is the same throughout the world

emerging country’s investors will require a risk premium for holding the currency

real interest rate parity

The real yield spread between the domestic and foreign countries (rf − rd) will be zero, and the level of real interest rates in the domestic country will be identical to the level of real interest rates in the foreign country

carry trade

taking long positions in high-yield currencies and short positions in low-yield currencies

during periods of low volatility, carry trades tend to generate positive returns, but they are prone to significant crash risk in turbulent times

fat tail with negative skew

Assume uncovered interest rate parity does not hold

The Flow Supply/Demand Channel

if a country sold more goods and services than it purchased then the demand for its currency should rise > exert upward pressure on the value of the surplus nation’s currency > currencies appreciate over time

limited pass-through effects of exchange rate changes on traded goods prices

The Portfolio Balance Channel

Countries with trade deficits will finance their trade with increased borrowing > increase their dollar holdings

The Debt Sustainability Channel

If a country runs a large and persistent current account deficit > experience an untenable rise in debt owed to foreign investors > investors expect a major depreciation of the deficit country’s currency

Mundell–Fleming Model

expansionary monetary policy affects growth, in part, by reducing interest rates and thereby increasing investment and consumption spending > induce capital to flow to higher-yielding markets, putting downward pressure on the domestic currency > more responsive capital flows are to interest rate differentials, the greater the depreciation of the currency

Expansionary fiscal policy > upward pressure on interest rates because larger budget deficits must be financed > attract capital from lower-yielding markets, putting upward pressure on the domestic currency > appreciate substantially

Monetary Models of Exchange Rate Determination

Output is fixed and monetary policy affects exchange rates primarily through the price level and the rate of inflation

X percent rise in the domestic money supply will produce an X percent rise in the domestic price level > proportional decrease in the domestic currency’s value - PPP

Portfolio Balance Approach

assumed to hold a diversified portfolio of domestic and foreign assets, including bonds

government budget deficit leads to a steady increase in the supply of domestic bonds outstanding > investors expect to be compensated with (1) higher interest rates (2) immediate depreciation of the currency

in the long run, governments that run large budget deficits on a sustained basis could eventually see their currencies decline in value

currency crisis

capital markets have been liberalized to allow the free flow of capital

large inflows of foreign capital

preceded by (and often coincide with) banking crises

fixed or partially fixed exchange rates are more susceptible

Foreign exchange reserves tend to decline precipitously

currency has risen substantially relative to its historical mean

ratio of exports to imports deteriorates

Inflation tends to be significantly higher

Factors limiting growth

Low rates of saving and investment

Poorly developed financial markets

Weak, or even corrupt, legal systems and failure to enforce laws

Lack of property rights and political instability

Poor public education and health services

Tax and regulatory policies discouraging entrepreneurship

Restrictions on international trade and flows of capital

Return on equity

E(Re) = dividend yield + expected repricing + inflation rate + real economic growth – change in shares outstanding

= dy + Δ(P/E) + i + g – ΔS

Earnings growth per share is the primary channel through which economic growth can impact equity returns.

ΔS dilution effect term

ΔS = nbb + rd

net buy backs + relative dynamism (small- and medium-sized entrepreneurial firms that are not traded publicly on the stock market)

Production Function

Y = AF(K,L),

Y= aggregate output in the economy

A = total factor productivity (TFP) - level of “technology”

K = stock of equipment and structures

L = quantity of labor

Cobb–Douglas production function

F(K,L) = KαL1−α

α determines the shares of output (factor shares) paid by companies to capital and labor

constant returns to scale - if all the inputs into the production process are increased by the same percentage, then output rises by that percentage

diminishing marginal productivity -

growth accounting equation

ΔY/Y = ΔA/A + αΔK/K + (1 − α)ΔL/L

growth in TFP as a residual

quantify the contribution of each factor

to measure potential output

labor productivity growth accounting equation

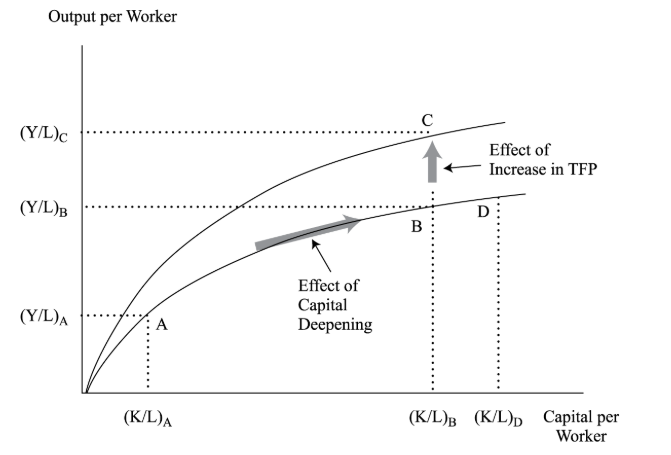

Labor productivity growth = capital deepening + TFP growth

Capital deepening

increase in the capital-to-labor ratio,

at point B, further additions to capital have relatively little impact

labor force participation rate

percentage of the working age population in the labor force

network externalities

The more people in the network, the greater the potential productivity gains

captured in TFP

Classical growth theory

population growth accelerates when the level of per capita income rises above the subsistence income

labor input faces diminishing marginal returns, the additional output produced by the growing workforce eventually declines to zero

population grows so much that labor productivity falls and per capita income returns back to the subsistence level

in the long run, the adoption of new technology results in a larger but not richer population

In reality

growth of per capita income increased, population growth slowed

technological progress more than offset the impact of diminishing marginal returns

Neoclassical Model

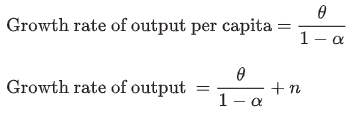

determine the long-run growth rate of output per capita and relate it to (a) the savings/investment rate, (b) the rate of technological change, and (c) population growth

steady state growth rate - neoclassical

θ denote the growth rate of TFP

n is the growth rate of the labor force

equilibrium output-to-capital ratio

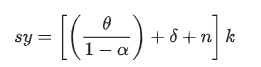

savings/investment equation

plant and equipment wearing out at rate δ,

deepen the physical capital stock at the rate θ/(1 − α)

capital for new workers entering the workforce at rate n,

capital-to-labor ratio (k)

Impact on the Steady State

Labor force growth (n) - increase > increases the slope of the required investment line > shifts the steady-state equilibrium to lower capital-to-labor and output per worker ratios

Depreciation rate (δ) - increases the slope of the required investment line > reduces the equilibrium capital-to-labor and output per worker ratios

Growth in TFP (θ) - same -

Conclusions from neoclasical

Capital Accumulation - level of output but not the LT growth rate - move to steady state

Capital Deepening vs. Technology - Rapid growth that is above the steady-state rate but slows LT - technological change or growth required because of diminishing marginal returns to capital

Convergence - growth rates of developing countries should exceed those of developed countries - convergence over time

Effect of Savings on Growth - initial impact temporarily raise the rate of growth - economy moves to a higher level of per capita output and productivity

endogenous growth theory

explaining technological progress rather than treating it as exogenous

self-sustaining growth - not steady state

no diminishing marginal returns to capital

increasing the saving rate permanently increases the rate of economic growth

no reason why the incomes of developed and developing countries should converge

endogenous growth rate of output per capita

∆ye/ye = ∆ke/ke = sc − δ − n

s = savings rate

Absolute convergence

developing countries, regardless of their particular characteristics, will eventually catch up with the developed countries and match them in per capita output + per capita income growth (not level) - neoclasical

Conditional convergence

conditional on the countries having the same saving rate, population growth rate, and production function

same level of per capita output as well as the same steady-state growth rate

club convergence

only rich and middle-income countries that are members of the club are converging to the income level of the world’s richest countries

appropriate institutional changes - otherwise non-convergence trap

open economies

neoclassical model, convergence should occur more quickly if economies are open and there is free trade

endogenous growth models predict that a more open trade policy will permanently raise the rate of economic growth