A Level Topic 4 - Production Costs and Revenues

1/45

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

46 Terms

Decreasing returns to scale

When output increases by a smaller proportion than the increase in inputs

Diseconomies of scale

When long run average costs rise as output increases.

Increasing returns to scale

When output increases by a larger proportion than the increase in inputs

Internal Economies of Scale

Firms taking action to reduce unit costs, Purchasing, Financial, Managerial, Marketing and Risk Bearing Economies

External Economies of Scale

Cost savings that are outside of the control of the firm e.g. Location of suppliers, infrastructure, skills of the workforce in the area

Labour Productivity

Measure of effectiveness of workers calculated as Total Output / Avg No of Workers

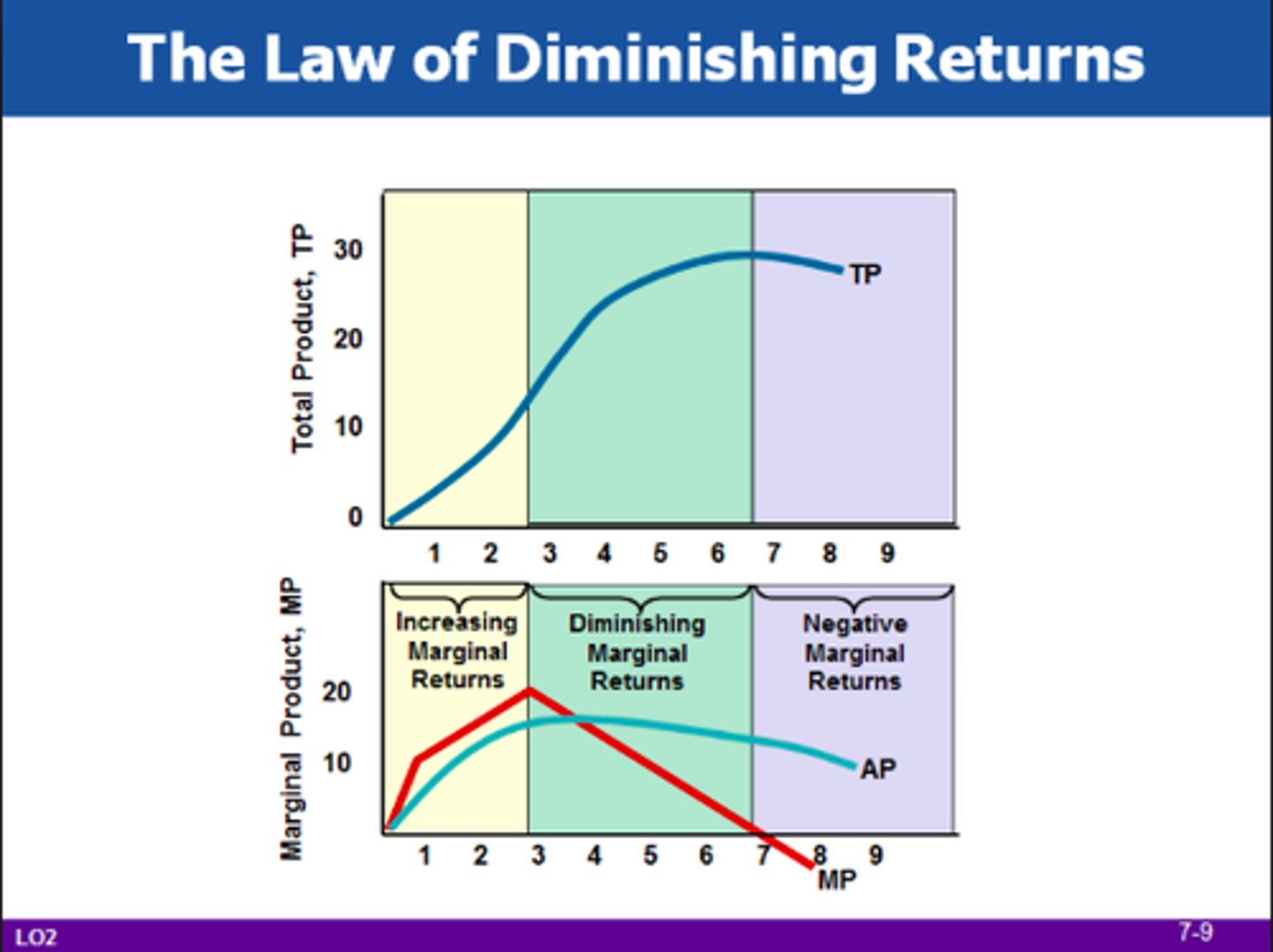

Law of diminishing returns

When variable factors are added to fixed factors eventually the return per variable factor increase with fall

Long run

Time period in which none of the factors of production are fixed so any can be increased

Long Run Average Cost

Total cost per unit of output over a long period of time

Mechanisation

When a firm changes from being more labour intensive to more capital intensive

Minimum efficient scale MES

The lowest level of output at which average costs are minimised. Creates a barrier of entry for other firms entering the market.

Normal profit

Total revenue is equal to total costs, the minimum amount needed to keep a firm operating in an industry

Production

Turning raw materials into finished or semi finished output

Productivity

Measure of effectiveness, how well does the firm use its resources to turn inputs into outputs Total Output/Total Inputs

Short run

Time period in which at least one of the factors of production are fixed and cannot be increased or decreased

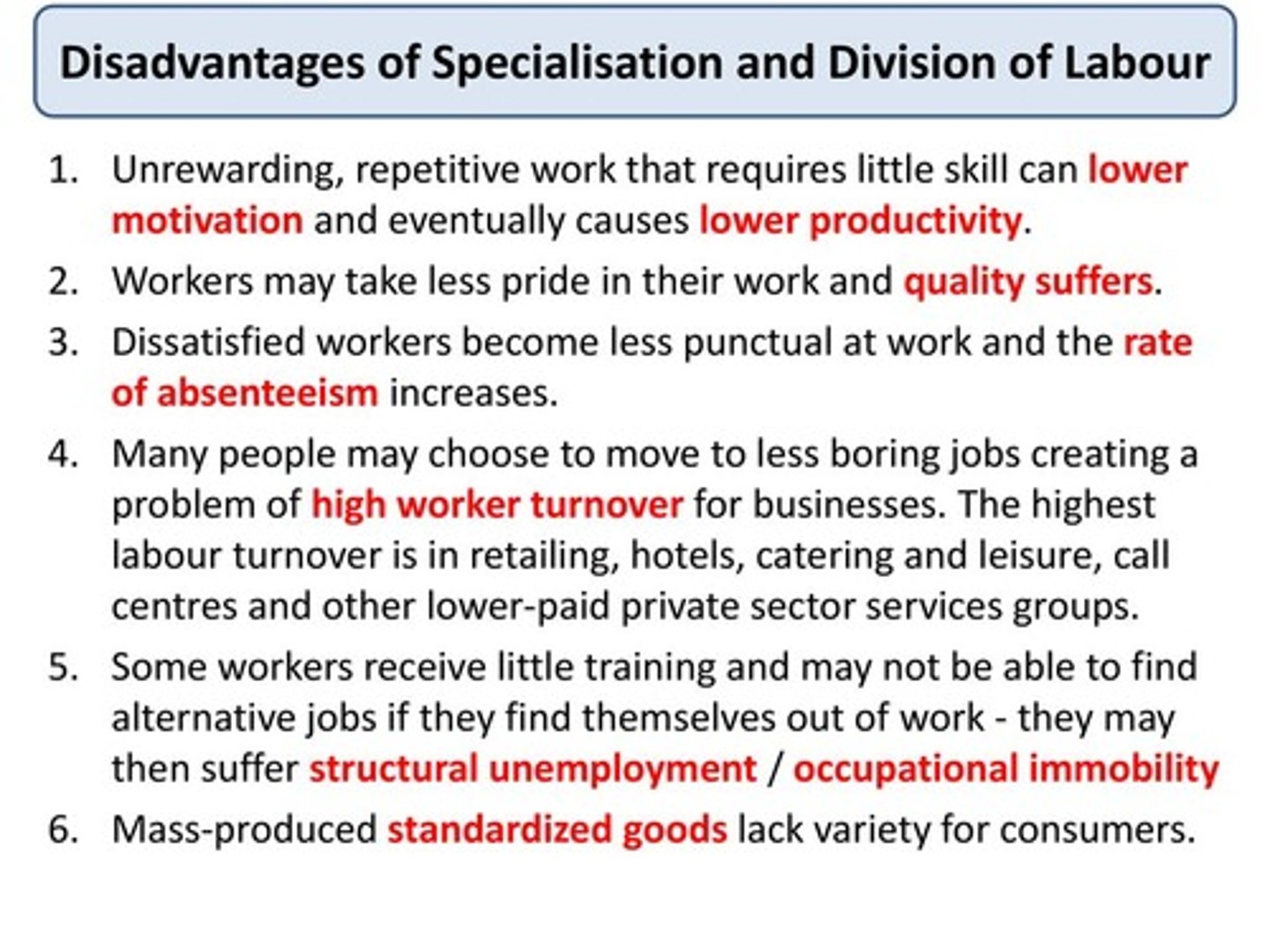

Specialisation

When an individual/firm or country focuses on performing one task or producing a specific product

Sunk Cost

Unrecoverable expenditure associated with entering a market

Supernormal/Abnormal Profit

Any level of profit over and above normal profit

Technical Economy of Scale

Increasing capacity through the introduction or better technology or more efficient machinery

X Inefficiency

When a firm does not have the incentive to control costs and therefore the average costs of production are higher than necessary

Benefits of Specialisation

Drawbacks of Specilisation

Diagram - Diminishing marginal returns

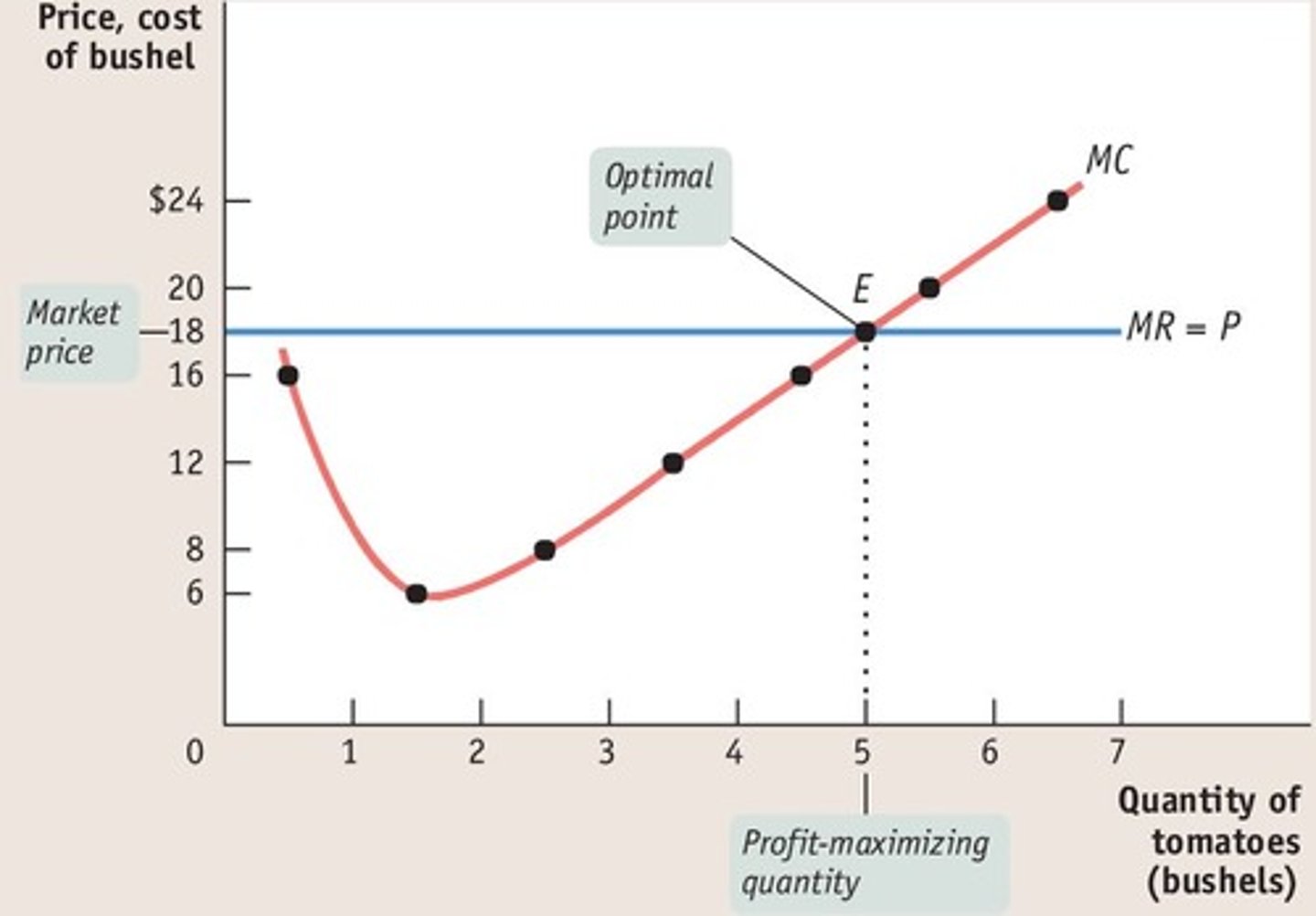

Marginal Cost

The cost of producing ONE additional unit of output

Draw the marginal cost curve

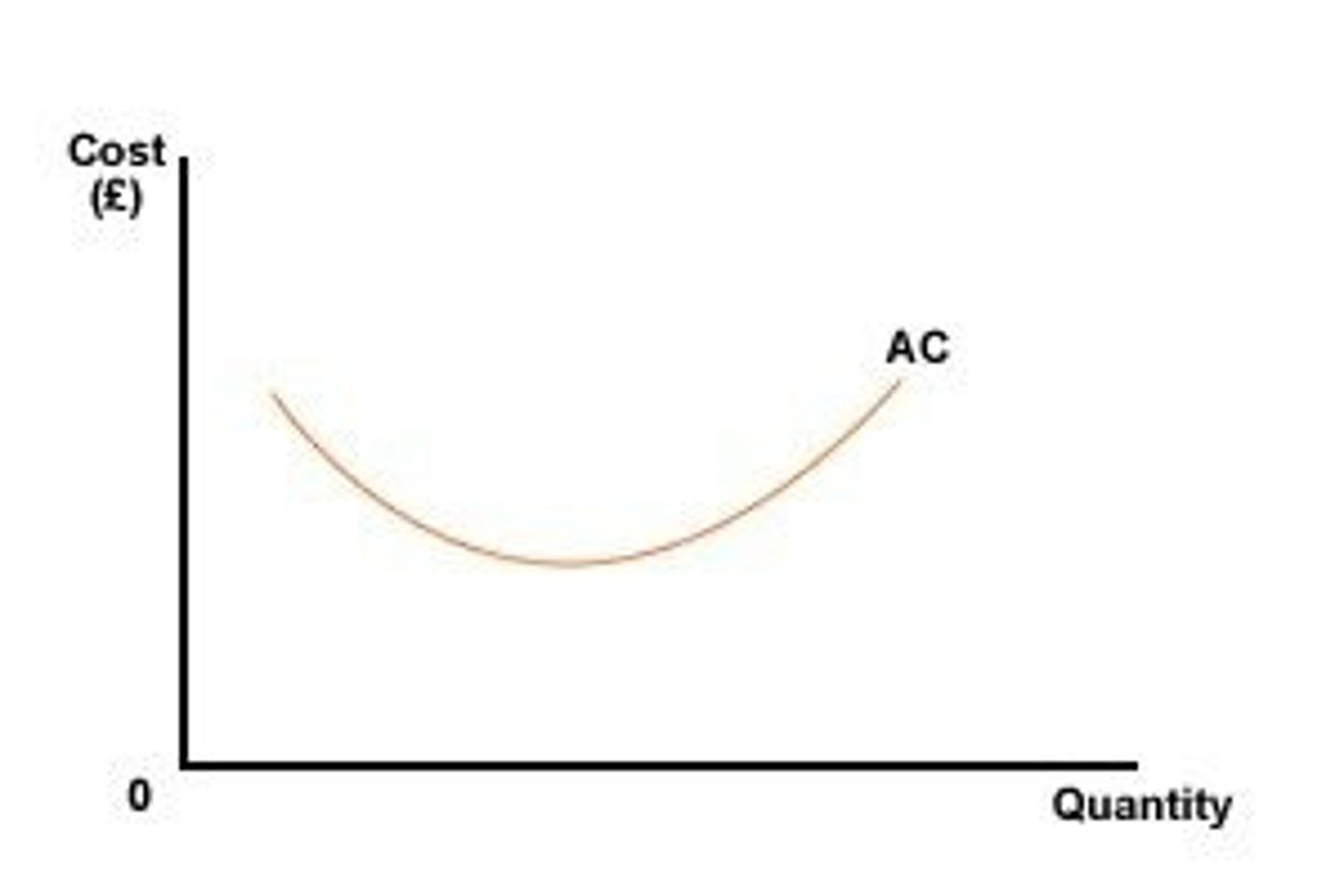

Draw the average cost curve

Marginal Revenue

Revenue recieved by the firm from selling the last unit of output.

Why is AR also the Demand Curve?

AR is average revenue, and the calculation for average revenue is Total Revenue / Quantity. Total Revenue = Price Quantity. Therefore AR = Price Quantity / Quantity => Price (as the Quantity is cancelled out). Hence AR = P, and D = P so we can say that D = AR.

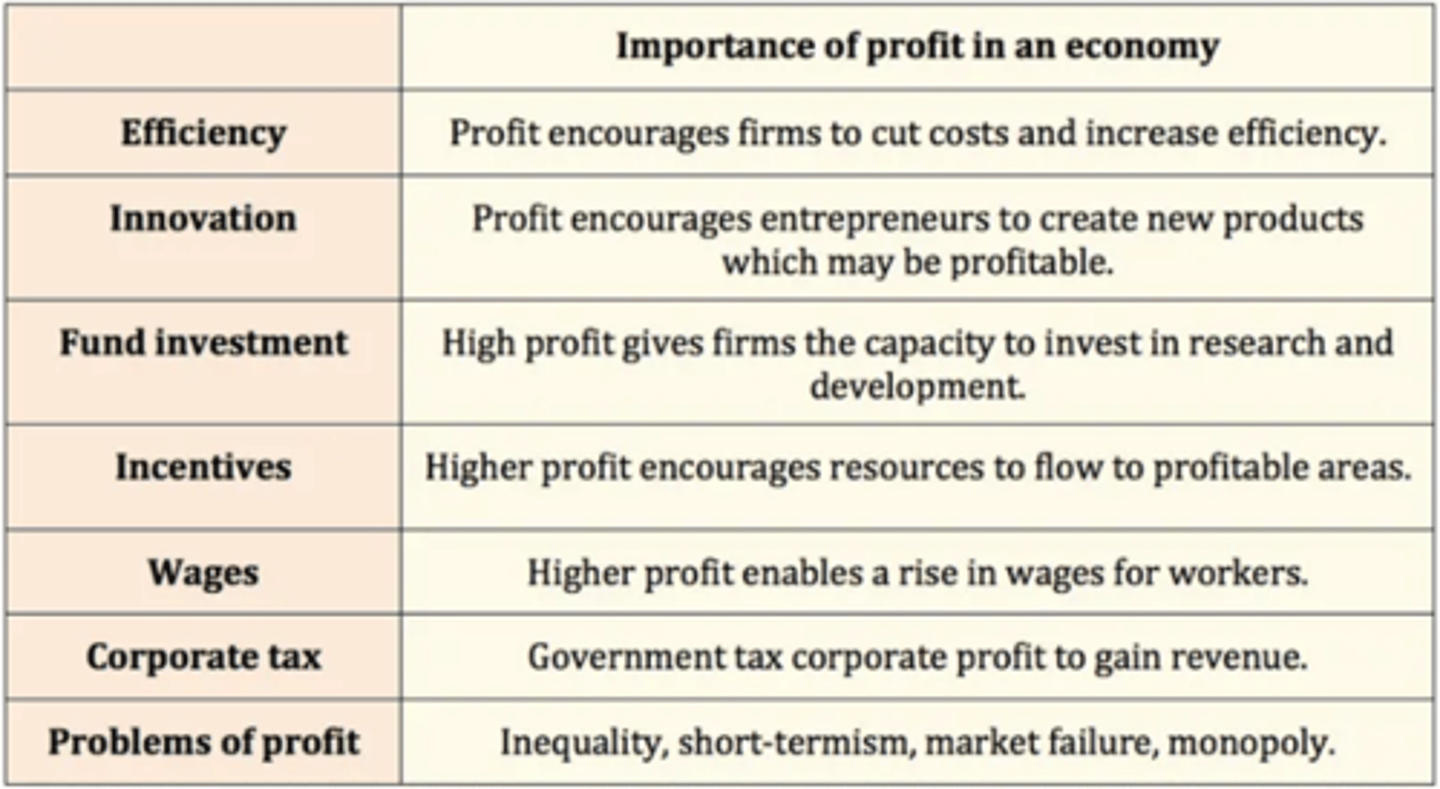

What is the role of profit - why is it important?

Invention

Invention is the discovery or development of a product or process by applying previous knowledge in new ways.

Innovation

Innovation is applying basic discoveries or inventions to produce a useful product or process and bringing it to the market

Technological Change

Technology lowers the cost of production and provides new products, it increases both productive and allocative efficiency for all firms. Technological change is the rate of developments in technology

Creative Destruction

the process of how capitalism leads to a constantly changing structure of the economy. Old industries and firms, which are no longer profitable, close down enabling the resources (capital and labour) to move into more productive processes

Economies of scope

When it is cheaper to make a range of products

Average Cost

The total production cost divided by the total output (cost per unit of output)

Average Revenue

Total revneue divided by total output (revenue per unit of output)

Division of labour

When production is split into smaller tasks and a worker performs one task

Economies of Scale

When long run average costs fall as output increases

Fixed Cost

Costs of production that do not vary with output produced e.g. rent, insurance,

Profit

Total revenue - total costs

Total Costs

Total Fixed Costs + Total Variable Costs

Total Revenue

Price of each good x the quantity sold. Total income recieved by the firm from its trading activities

Variable cost

Cost that increase or decrease as production levels increase or decrease. Directly related to output

Automation

Where parts of the production process are controlled by machines/robotics

Constant returns to scale

When output increases by an equal proportion to the increase in inputs

Types of disecnomies of scale

Communication Coordination Control