Ch. 5: Elasticity

1/21

Earn XP

Description and Tags

Flashcards for Chapter 5 of Principles of Economics by Gregory Mankiw

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

Elasticity

a measure of the responsiveness of quantity demanded or quantity supplied to a change in one of its determinants

Price elasticity of demand

a measure of how much the quantity demanded of a good responds to a change in price of that good, computed as the percent change in quantity divided by the percent change in price.

Q: How does availability of close substitutes affect price elasticity?

A: The availability of close substitutes makes demand for a good more elastic, as consumers can easily switch to alternatives when the price changes.

ex) if the price of butter increases while the price of margarine remains fixed, the quantity demanded for butter will decrease as consumers switch to margarine.

Necessities vs. Luxuries

Necessities are more inelastic, while luxuries are more elastic. Necessities are goods that are essential for survival and have less sensitivity to price changes, whereas luxuries are non-essential items that consumers can forgo, making their demand more sensitive to price fluctuations.

Q: How does the definition of a market affect its elasticity?

A: A broader market definition has fewer substitutes, which makes demand less elastic. A more narrow market definition has more substitutes and more elastic demand.

ex) demand for food is very inelastic because it has few substitutes, while demand for vanilla ice cream is elastic because it has many substitutes (frozen yogurt, chocolate ice cream, etc.)

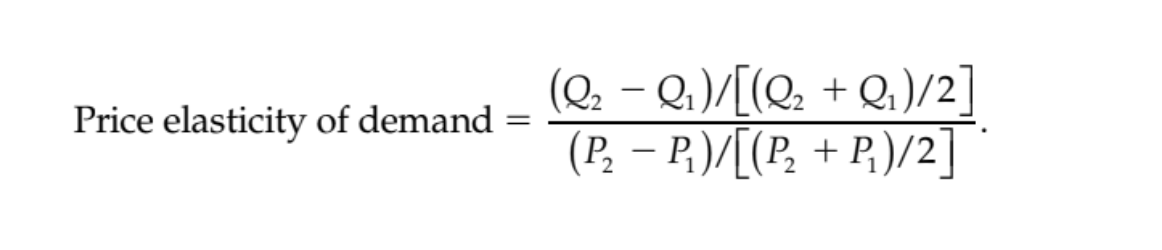

Price elasticity of demand (midpoint method)

Q: When is demand elastic?

A: Demand is elastic when the price elasticity of demand is greater than one, indicating that a change in price leads to a proportionally larger change in quantity demanded.

PED > 1

Q: When is demand inelastic?

A: Demand is inelastic when the price elasticity of demand is less than one, indicating that a change in price leads to a proportionally smaller change in quantity demanded.

PED < 1

Q: What is unit elastic demand?

A: Unit elastic demand is when the price elasticity of demand is equal to one, meaning that a change in price results in a proportional change in quantity demanded.

PED = 1

Total revenue

The amount paid by buyers and recieved by sellers of a good. Can be computed as the product of the price per unit and the quantity sold, or P X Q.

Q) What happens to revenue if you increase the price of an elastic good?

An increase in price causes total revenue to decrease when demand is elastic because the extra revenue from selling units at a higher price is more than offset by the loss of revenue from selling fewer units.

Q) What happens to revenue if you increase the price of an inelastic good?

An increase in price causes total revenue to increase when demand is inelastic because the extra revenue from selling units at a higher price more than offsets the loss of revenue from selling fewer units.

Unit elastic

A price elasticity equal to exactly one, total revenue remains constant when the price changes

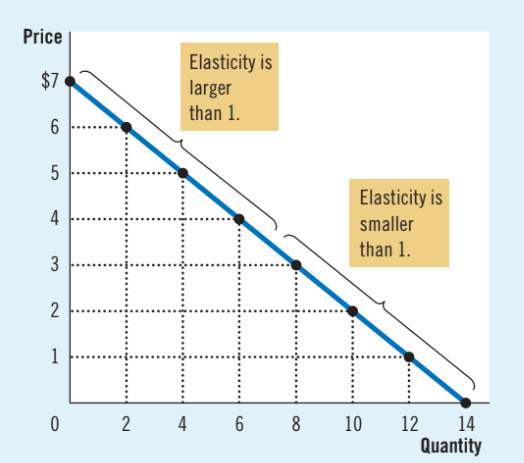

Elasticity of a linear demand curve

At points with a low price and high quantity, the demand curve is inelastic. At points with a high price and low quantity, the demand curve is inelastic

Q: Why is the elasticity of a linear demand curve not constant?

A: The slope is the ratio of the change between two variables, whereas the elasticity of demand is the ratio of the percent change in two variables.

Income elasticity of demand

A measure of how much the quantity demanded of a good responds to a change in the consumer’s income.

Elasticity of normal vs. inferior goods

The elasticity of normal goods is positive, the elasticity if inferior goods are negative.

Engel’s Law

As a family’s income rises, the percent of its income spent on food declines, indicating an income elasticity less than one. By contrast, luxuries such as jewelry and recreational goods tend to have large income elasticities because consumers feel that they can do without these goods altogether if their income is too low.

Cross-price elasticity of demand

Measures how the quantity demanded of one good responds to a change in price of another good

Cross-price elasticity of substitutes vs. compliments

The cross-price elasticity of substitutes is positive (price and quantity demanded move in the same direction), and the cross-price elasticity of complements is negative (price and quantity demanded move in opposite directions)

Price elasticity of supply

Measures how much quantity supplied responds to a change in price.

Price elasticity long run vs. short run

Supply is usually more elastic in the long run than in the short run.