Looks like no one added any tags here yet for you.

net realizable value

expected selling price/ value of an item - the cost of making the sale

loss is recorded when the damage

Merchandise Inventory

Merchandise Inventory includes costs to bring an item to a salable condition and location

Inventory Costs

includes invoice cost - any discounts + any other costs

expense recognition principle

the expense recognition principle says inv. costs are expensed as cogs when inventory is sold.

Specific Identification

Methods to assign costs to inventory + costs to inv. + cogs

i. specific identification

ii. first-in, first-out: FIFO

iii. last-in, first-out LIFO

iv. weighted average

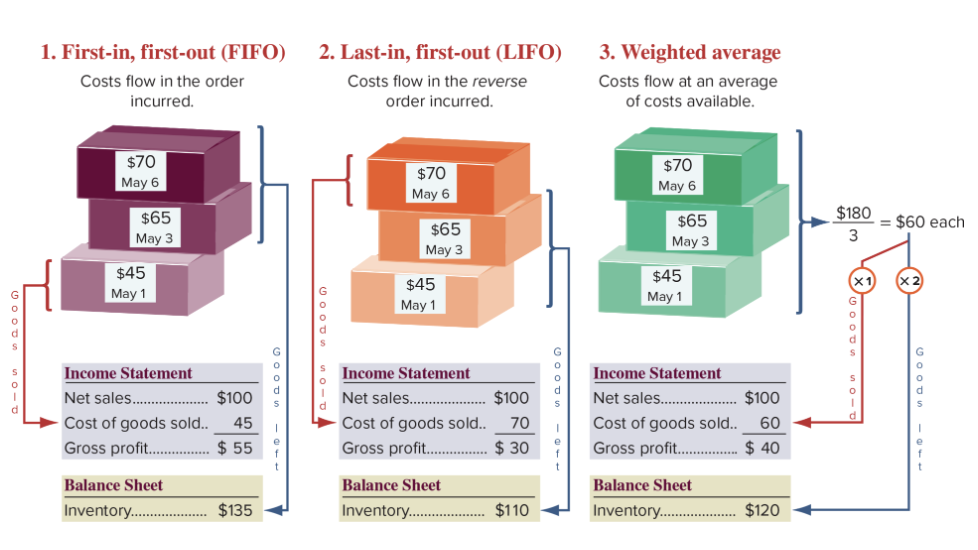

first-in, first-out FIFO

FIFO assumes costs flow in order incurred

earliest units acquired are charged to COGS

leaves out costs from the most recent purchases in ending inventory.

cogs and ending are the same for periodic and perpetual

ADVANTAGES:

inventory on the balance sheet approximated its current costs

follows the actual flow of goods for most businesses

last-in, first-out LIFO

assumes costs flow in the reverse order incurred

ADVANTAGES:

cogs on the income statement approximated its current costs

matches current costs with revenues

Weighted Average

Weighted Average assumes cost flow at an average of the costs available.

WA = cost of goods available for sale (at each sale)/

number of units available for sale

Specific Identification

method for assigning cost to inventory when the purchase of each item in inventoyr is identified and used to compute the COGS and/ or costs of inventory

Rising Costs

When purchasing costs regularly RISE, the following occurs:

FIFO

reports the lowest cost of goods sold - yielding the HIGHEST gross profit & net income

inventory on the balance sheet approximated its current costs

follows the actual flow of goods for most businesses

LIFO

reports the highest cost of goods sold - yielding the LOWEST gross profit & net income

Weighted Average

average yields results between FIFO & LIFO

falling costs

When purchasing costs regularly DECLINE, the following occurs:

FIFO

reports the highest cost of goods sold - yielding the LOWEST gross profit & net income

LIFO

reports the lowest cost of goods sold - yielding the HIGHEST gross profit & net income

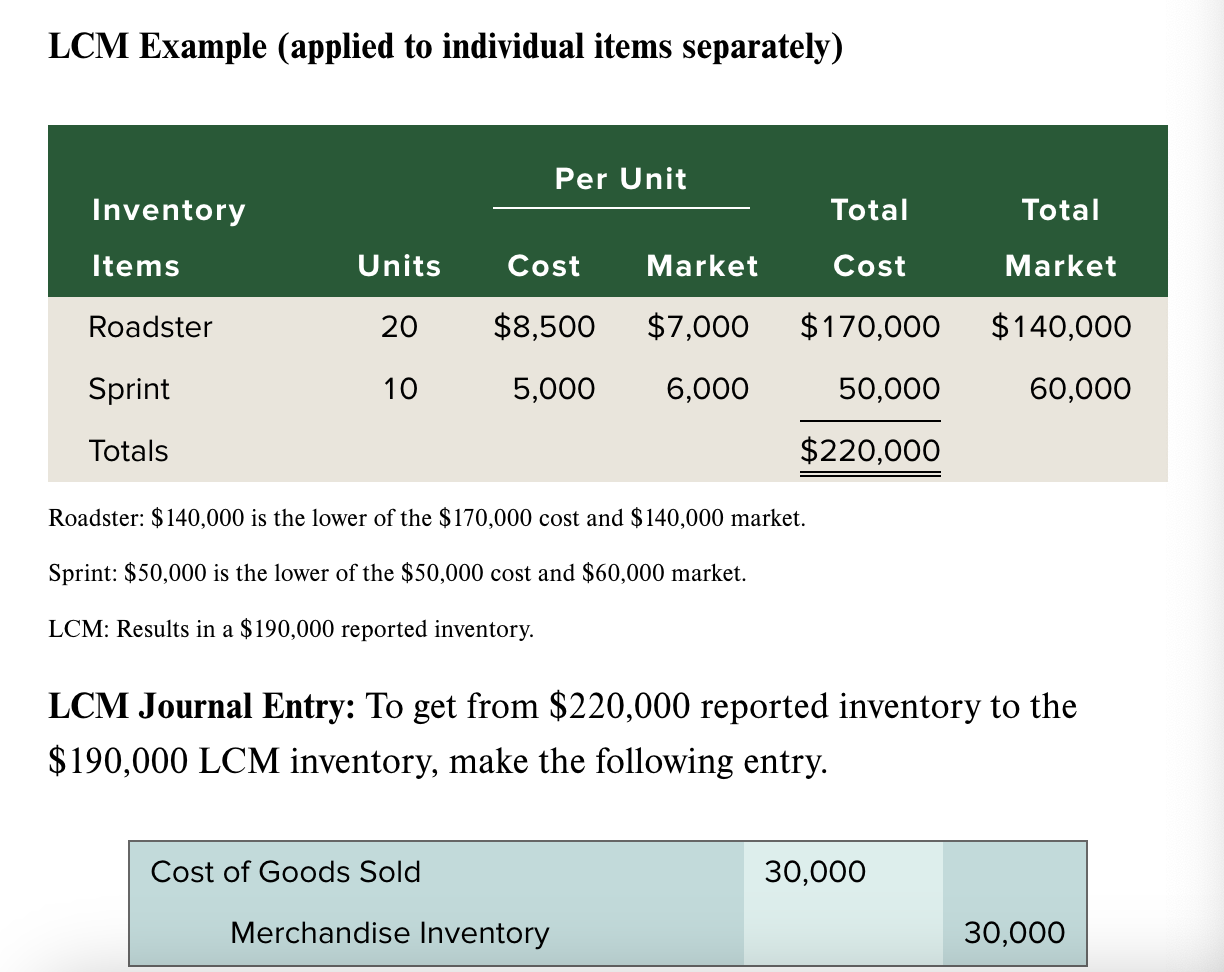

Lower of Cost/ Market (LCM)

required method to report inventory at market replacement cost when that market cost is lower than recorded costs

…. adjustment required when market value of inventory is lower than its cost

(‘market’ in the term LCM is replacement cost for LIFO, but net realizable value)

LCM Journal Entry:

cost of goods sold #

merchandise inv. #

COST OF GOODS SOLD

beg. inventory + net purchases - ending inventory = COGS

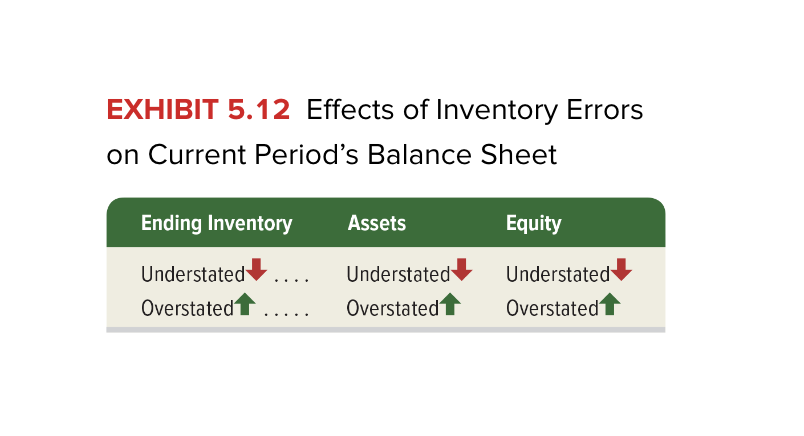

effects of inventory errors

Balance Sheet

inventory turnover

shows how many times a business sells its inventory in a period

Inventory Turnover = COGS/ average inventory

low ratio shows the company has more inventory than it needs/ struggles to sell inventory

high ratio shows inventory might be too low

preferable

days sales in inventory

day sales in inventory = ending inventory/ cogs (365)

Periodic Inventory System

merchandise inventory account is updated at the end of each period to reflect purchases and sales

Retail Inventory Method

method for estimating ending inventory based on the ratio of the amount of goods for sale at cost to the amount of goods for sale at retail

STEP I:

i. goods available for sale at retail - net sales at retail = ending inv. @ retail

STEP II:

i. goods available for sale at cost - net sales at retail = cost-to-retail ratio

STEP III:

i. ending inv. at retail x cost-to-retail ratio = ESTIMATED ENDING INV AT COST

Gross Profit of Inventory Estimation

STEP I:

i. net sales at retail (x) 1.0 - gross profit ratio = est. cogs

STEP II:

i. goods available for sale at cost (-) estimated cogs = estimated ending inventory at costs

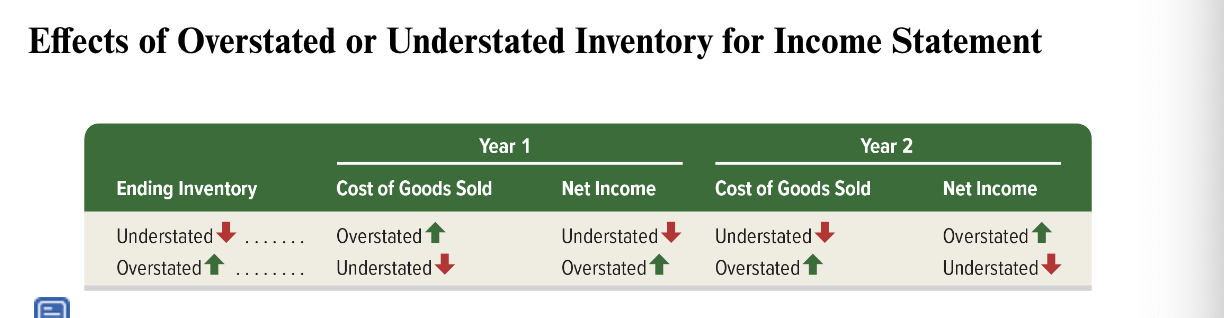

Effects of Overstated/ Understated Inventory for Income Statement

refer to image