Carina Foundations

1/64

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

65 Terms

is the situation in which available resources (factors of production) are finite but our wants/needs are infinite

what is the definition of scarcity?

- has a high price/value

- if the demand > supply

- if you can't find it (unavailable)

- the resources are allocated in certain ways (rational, lottery)

how do you know when something is scarce?

makes us make choices

what does scarcity make you do?

studies the behaviour of individual decision making in the economy (such as producers and consumers)

microeconomics definition

consumers (households) and firms (businesses)

what are the two main decision makers studied in microeconomics?

The study of the economy as a whole, is concerned with the aggregate or sum of behaviour

macroeconomics definition

Combination of many individual markets into one overall market

meaning of aggregate

using our scarce resources in the least wasteful way

what is one thing the study of economics is about?

refers to the long-term maintenance or viability of any particular activity of policies. and in economics refers to the ability of the present generation to satisfy its needs by the use of resources and non-renewable resources, without limiting the future-generations ability to satisfy their own needs

sustainability definition

land, labor, capital, entrepreneurship

what are the 4 factors of production?

all natural resources or ' gifts of nature'

what does the land factor entail?

the physical or mental effort that people contribute to the production process.

what does the labor factor entail?

the man-made FoP used to produce goods/services.

what does the capitol factor entail?

skill possessed by some people of creatively combining or organizing the other factors of production into a good/service.

what does the entrepreneur factor entail?

the income received for supplying factors of production

what are factor payments?

land gets you rent

what is the factor payment of land?

labor gets you wages

what is the factor payment of labor?

capitol gets you interest

what is the factor payment of capitol?

entrepreneurship gets you profit

what is the factor payment of entrepreneurship?

the value of the next best alternative that must be given up in order to obtain something else

opportunity cost definition

3

how many basic economics questions are there?

1. What to produce? - what goods/services are we going to produce?

what is the first basic economics question?

2. How to produce? - how are we going to use our resources to produce the goods/services we want/need?

what is the second basic economics question?

3. For whom to produce? - how are goods/services going to be distributed amongst the population?

what is the third basic economics question?

resources are owned privately and it's up to producers and consumers to make economic decisions

market method definition

resources are owned by the government who make the economic decisions

command method definition

free economy, mixed economy and command economy

what three types of economies are there?

an economy without government intervention and individuals own the factors of production. Businesses make goods/services to make profit

What is a free economy?

an economy where the factors of production are owned by the government and in which production, investment, prices, and incomes are determined centrally by a government.

what is a planned/command economy?

an economy mixed with free markets and government intervention. the government will pay for public goods, eg roads bridges and public services, eg firefighters and teachers

What is a mixed economy?

the government regulates production and ensures the welfare of labor workers

what is the purpose of government intervention in a mixed economy?

businesses meet society's needs when they seek their own self-interest

invisible hand in the free market

minimum price mean minimum wage

what does minimum price mean?

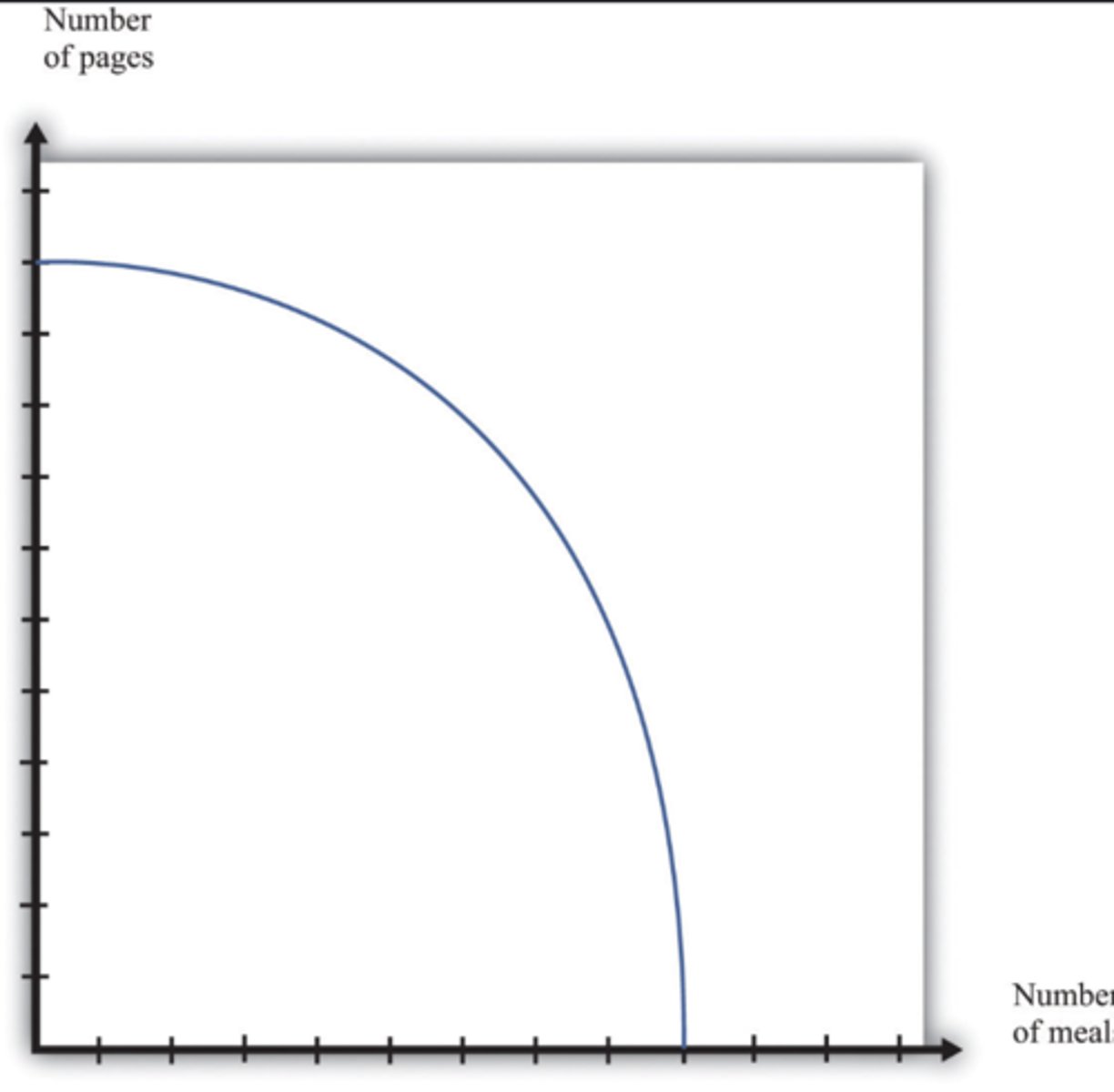

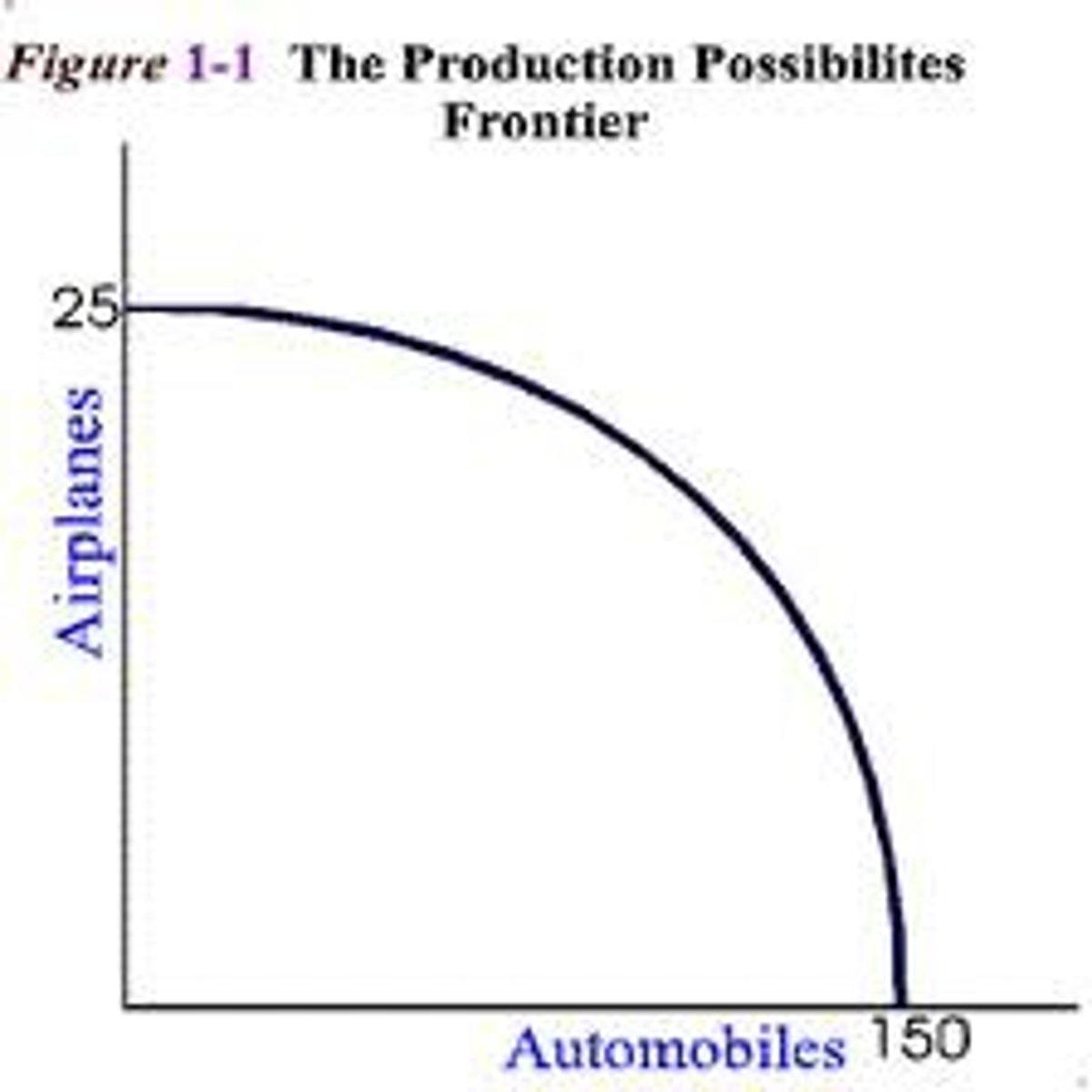

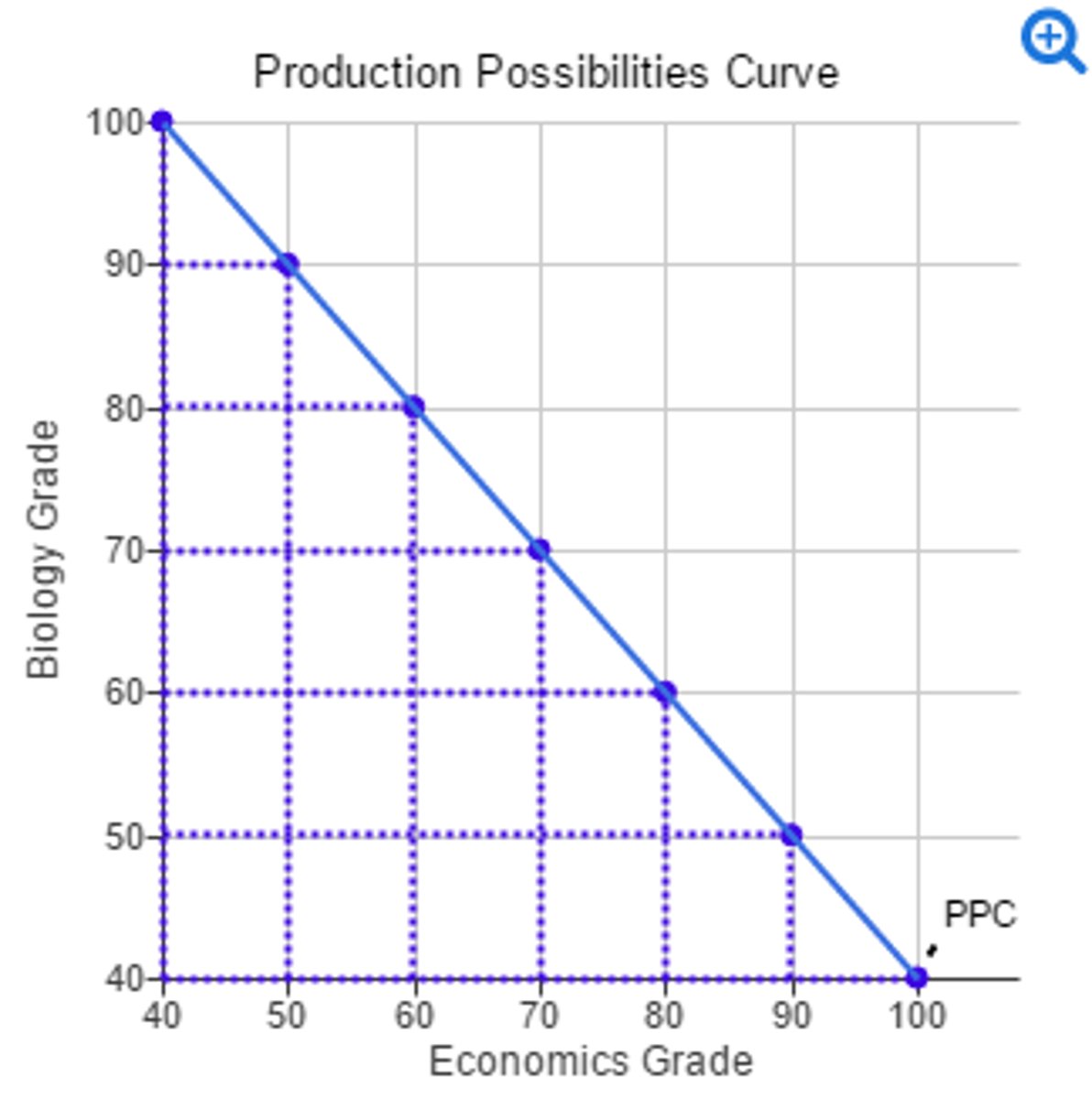

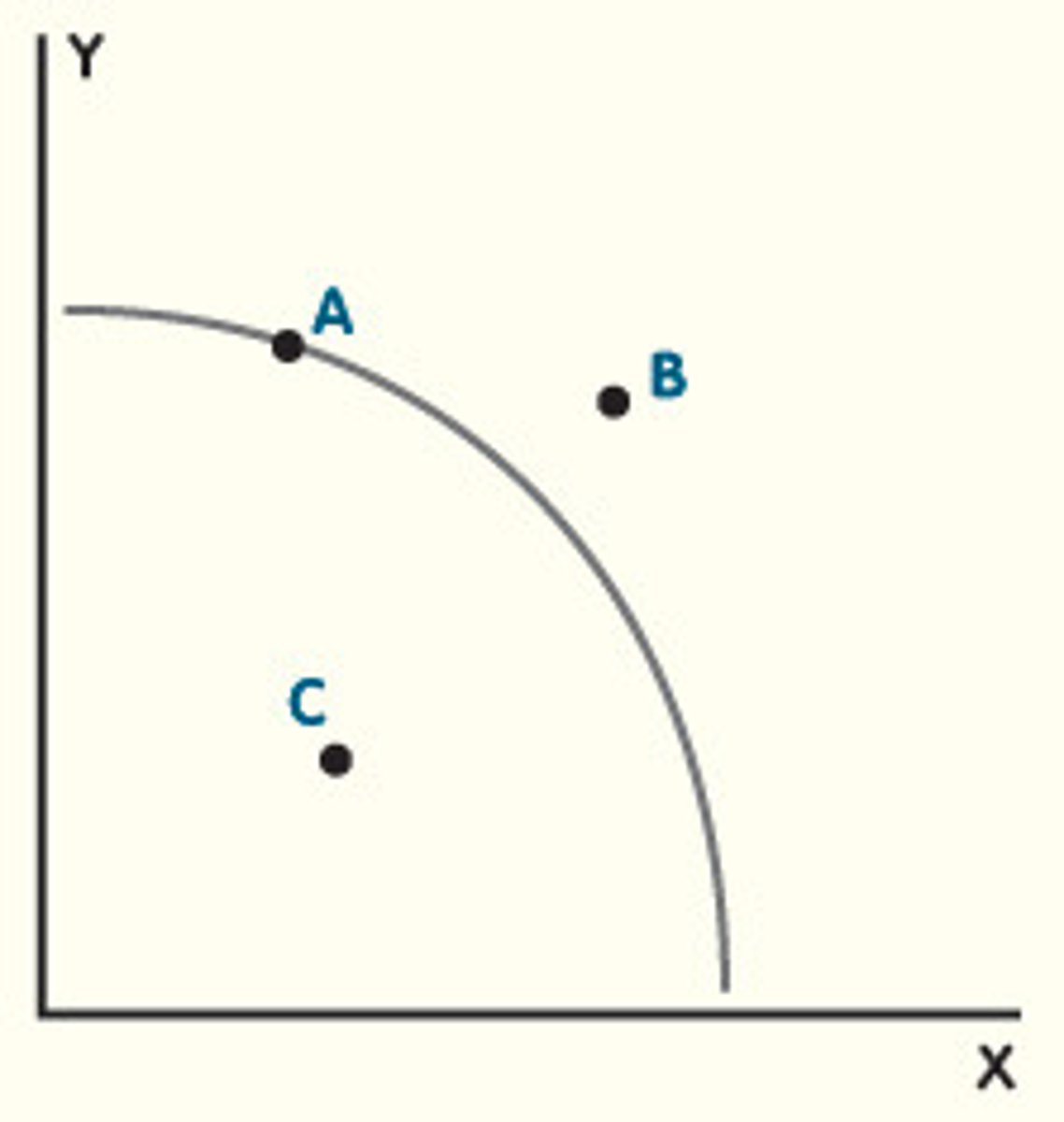

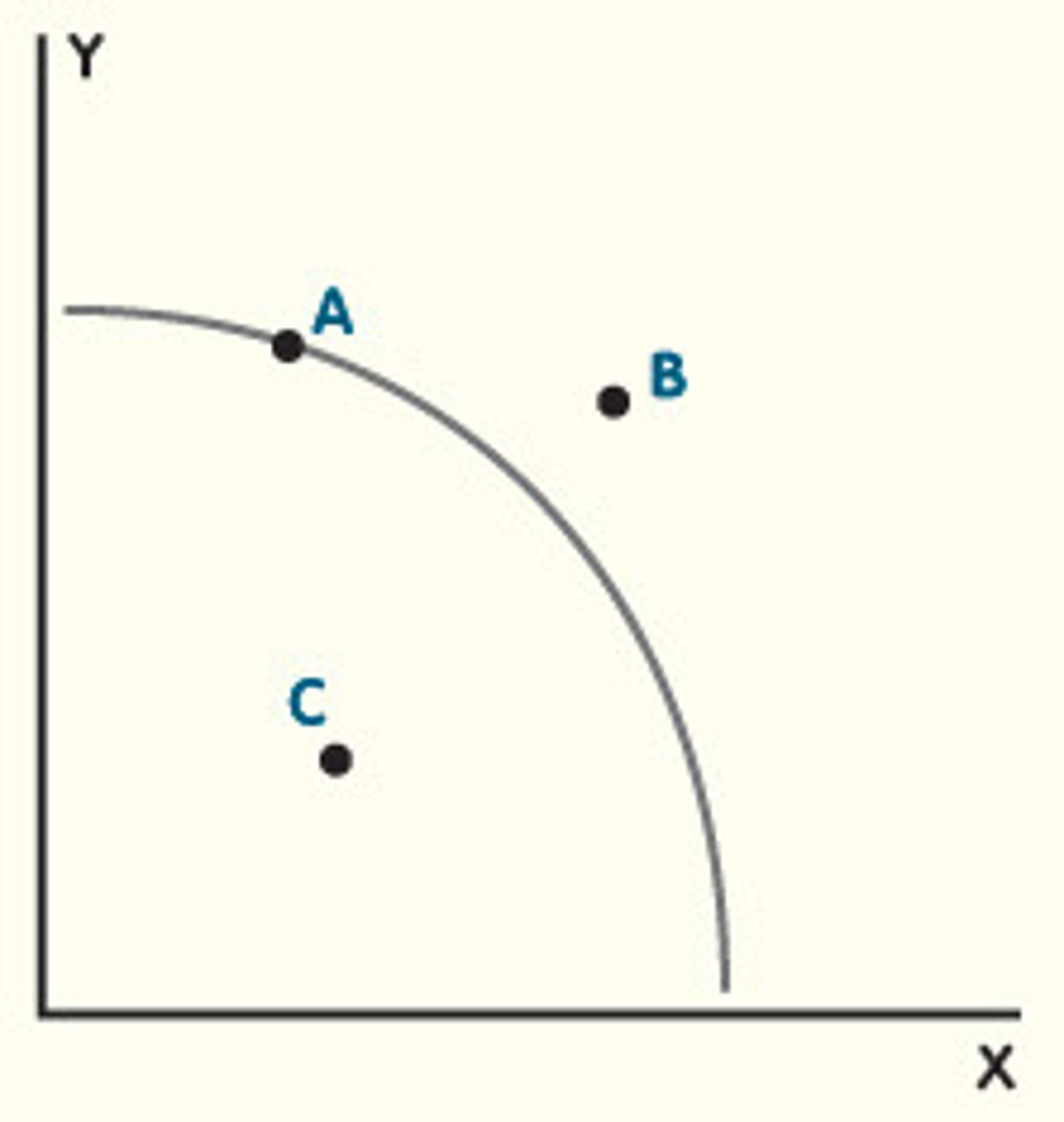

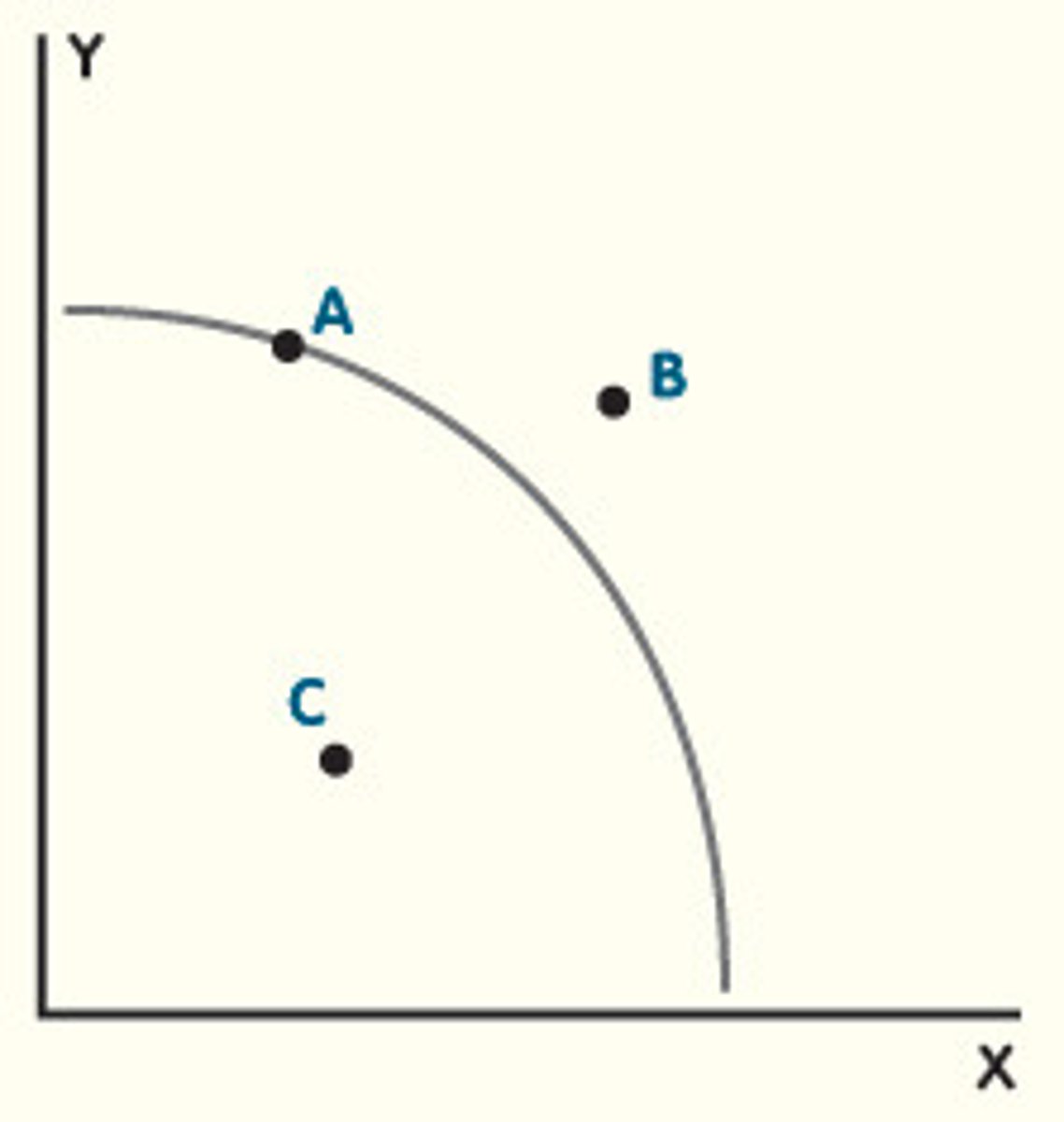

represents all combinations of the maximum amounts of two goods that can be produced by an economy, given its resources and technology, when there is full employment of resources and efficiency in production.

What is a PPC (Production Possibilities Curve)?

all factors of production are being used to their maximum

what does it mean when all resources are being fully employed?

resources are not being wasted and output i being produced with the least amount of resources possible

what does it mean when all resources are being efficiently used?

Constant and increasing

what are two types of PPCs that represent opportunity cost?

increasing opportunity cost

1. what does this PPC represent?

constant opportunity cost

2. what does this PPC represent?

an economy will not be able to produce outside the PPC, there is no availability of the factors of production to produce the output

what does scarcity mean in terms of a PPC?

scarce resources mean that countries need to make choices about the goods/services or combination of goods/services they want to produce.

Choice definition (in terms of scarcity)

any choice between choosing more or less of a good/service means there will be an opportunity cost for that choice.

opportunity cost - refer to choices

fully efficient use of resources and no unemployment

what does point A on the PPC graph represent?

scarcity as the point is inadmissible - market is unable to produce the good/service given its resources

what does point B on the PPC graph represent?

inefficient use of resources and unemployment

what does point C on the PPC graph represent?

the increase in the quantity of output produced in an economy over a period of time

economic growth definition

caused by reduction in unemployment and increases in efficiency in production

Actual growth definition

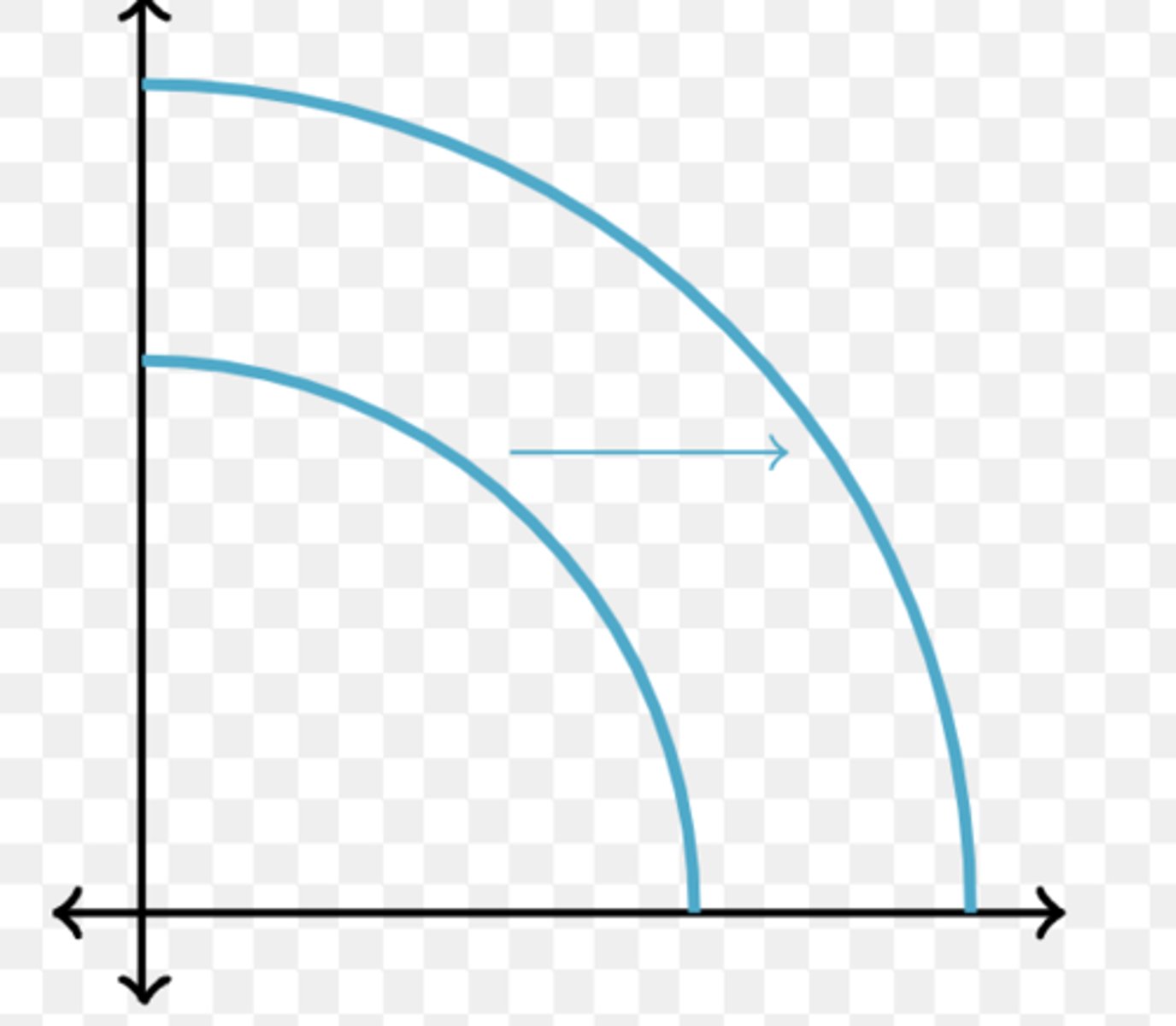

caused by an increase in the quality or quantity of resources (factors of production)

growth in production possibilities definition

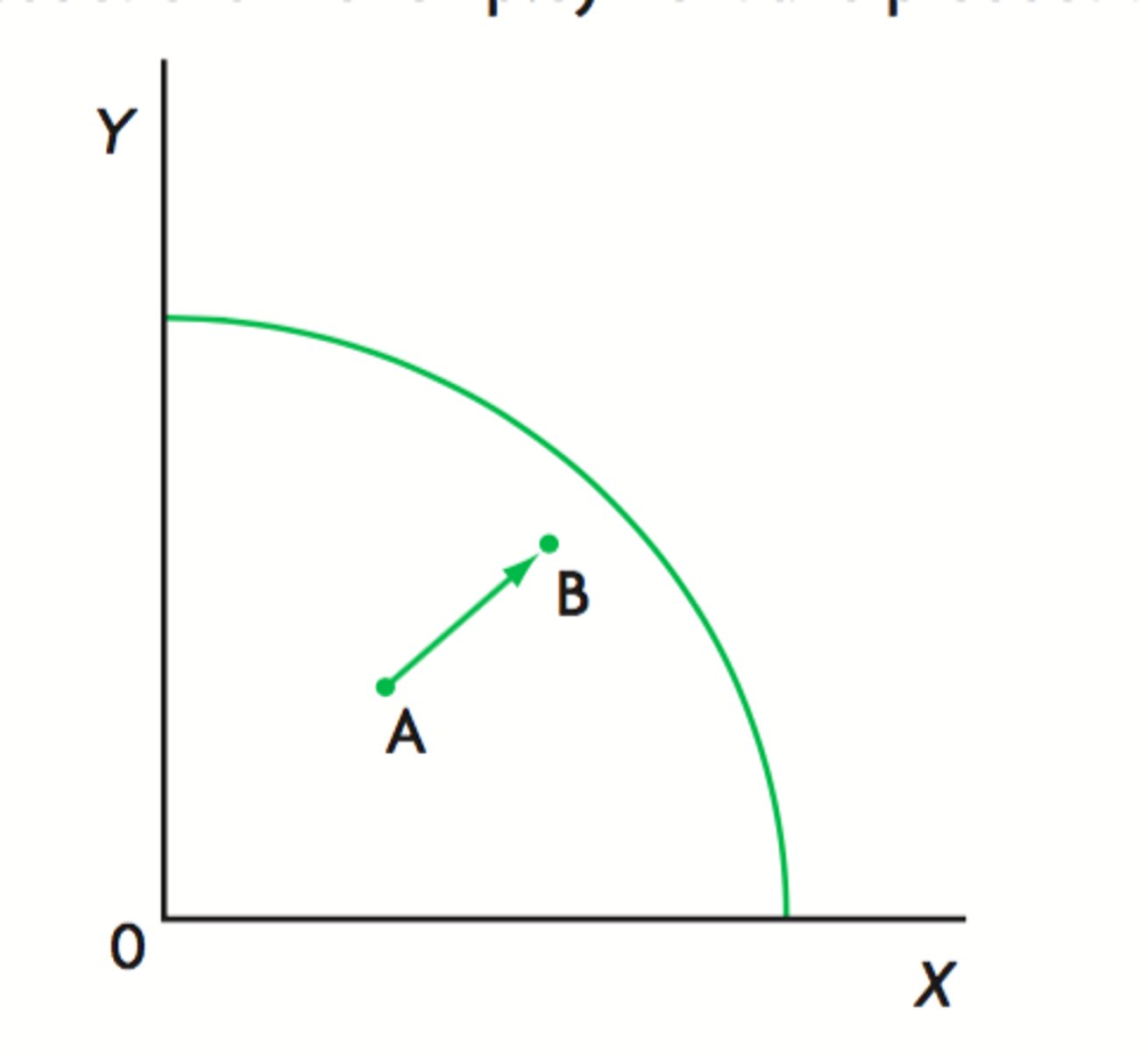

increase in actual growth

1. what is this image an example of?

economic growth, increase in production possibilities

2. what is this image an example of?

government payments to businesses or households designed to meet a specific objective

transfer payment definition

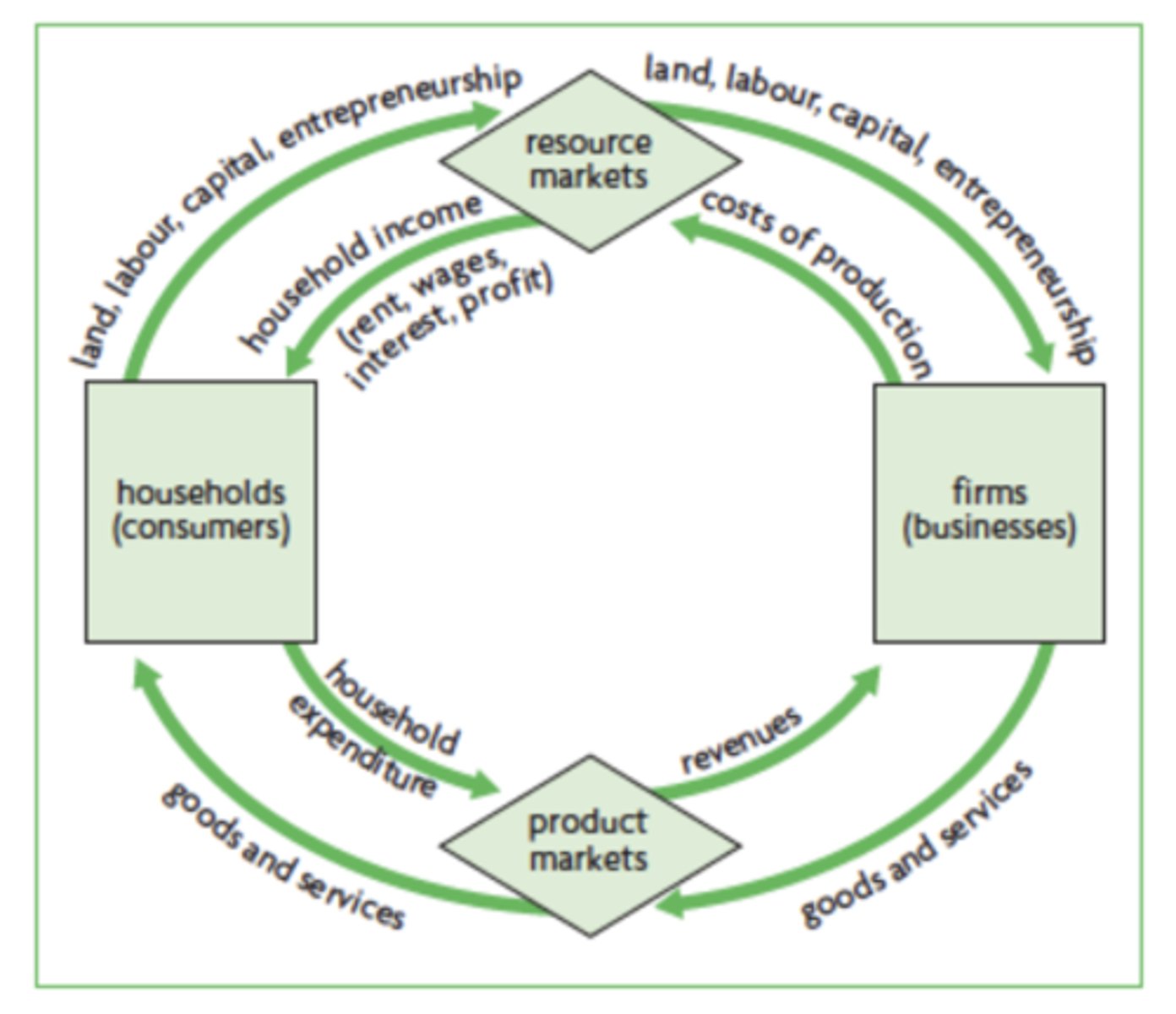

shows that in any given time period the value of output produced in an economy is equal to the total income generated in producing that output, which is equal to the expenditures made to purchase that output.

Circular flow of income

because everything works in a cycle

how can households & firms be buyers and sellers simultaneously?

withdrawals from the economy and come in the form of savings, taxes, and imports.

leakages definition

investments into the economy and come in the form of investments, government spending, and exports.

injections definition

economic growth is when there are less leaks and more injections into the economy

economic growth in terms of leaks and injections

firms get more money

what happens to the size of the economy when injections are bigger than leaks?

not enough resources, economy becomes unstable and firms get no money

what happens to the size of the economy when leaks are bigger than injections?

buyers of goods and services

sellers of factors of production (resources)

what are households sellers and buyers of?

buyers of factors of production (resources)

sellers of goods and services

what are firms sellers and buyers of?

they get revenue

when households use factor payments to spend on expenditures (to obtain goods and services), what do firms get?

the study of economics based on the scientific method used to arrive at knowledge about the economic world which includes descriptions, models, hypotheses, theories and laws. - they can describe, explain or predict

positive economics definition

forms the basis of judgements about what economic goals and economic policies ought to be. It is based on value judgements, because it identifies important economic problems that should be addressed and prescribes what should be done to solve them.

normative economics definition

are any kind of arrangement where buyers and sellers of goods services, or resources are linked together to carry out an exchange

markets definition

Competitive markets involve numerous sellers and buyers acting independently, allowing no single seller to control product prices. Price is determined by supply and demand forces and the interaction of many sellers and buyers.

competitive markets definition