IB Economics: Introduction to Economics: UNIT ONE

1/104

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

105 Terms

How is economics characterized as?

Economics is a social science characterized by interdependence, which focuses on how people interact with each other to improve their economic wellbeing, influenced and enabled by their values and their natural surroundings.

Why is economics considered a social science?

Economics is regarded as a social science because it uses scientific methods to build theories that can help explain the behavior of individuals, groups and organization's. Economics attempts to explain economic behavior, which arises when scarce resources are exchanged

The economic world is ______ in nature and constantly subject to ____________.

Dynamic

Change

What are economic theories based off?

Economic theories are based on logic and empirical data, using models to represent and analyze this complex reality. Individual and collective motivations and behaviors are complex and diverse and their understanding entails the interaction of a variety of disciplines such as philosophy, politics, history and physiology.

What does economics decision-making impact?

Economic decision0 making impacts the relative economic-wellbeing of individuals and society.

What are the central problems of economics?

Scarcity and choice

What is the study of economics

Economics is the study of scarcity and its implications for the use of resources, production of goods and services, growth of production and welfare over time, and a great variety of other complex issues of vital concern to society.

What are the biggest problems that Economics face? And what do these problems force?

Scarcity and Choice are the biggest problems in economics. Which creates a forced opportunity cost to arise due to the allocation of limited resources in our world to satisfy our unlimited and competing wants. This challenges the sustainability and fair trade of resources as well as the question to make the best use of limited resources without wastage.

What are the two debates regarding the potential conflicts of economics?

The potential conflict between economic growth and equity

The potential conflict between free markets and government intervention

Why can can't economic growth continue to be based off finite resources?

Endless economic growth, based on the consumption of finite resources, cannot continue indefinitely as it is unsustainable. New economic models and social movements have challenged mainstream opinion about the purpose of growth and how the economy could be redesigned to support long-term prosperity. E.g. BCE

- TEST QUESTION

What is scarcity?

It is the situation in which available resources, or factors of production, are finite, whereas wants are infinite. It is the idea that resources are limited and unable to meet the unlimited human wants and needs.

What is Choice?

because resources are scarce, decisions must be made about which wants/needs are satisfied, and which are forgone.

What is Efficiency?

Making the best possible use of resources. Minimizing waste. It could refer to maximizing output while minimizing resource use. It could also refer to allocating resources to satisfy society's wants and needs ( rather than producing unwanted items).

What is equity?

Being fair and just. This is why we must study the distribution of income and wealth in economics

What is economic well-being?

Can refer to prosperity, economic satisfaction and security, and standards of living among the members of society. Quality of life indicators include health, education, social connections, environmental quality and personal security.

What is sustainability?

Managing resources so that the present generation is able to satisfy its needs without limiting the ability of future generations to satisfy theirs.

What is change?

This is an important concept as economics is dynamic- both in theory and in real-life events. This is why we must recognize a variety of economic ideas and monitor trends in economic outcomes.

What are stakeholders?

A stakeholder is a person, group or organization with a vested interest, or stake, in the decision-making and activities of a business, organization or project.

What is interdepence?

The idea that stakeholders in the economy interact with and rely on each other. This is because it is impossible to maintain our current standards of living in a self-sufficient manner.

What is intervention?

Government involvement and influences on the market. This is because while the free market offers many benefits, it also has its limitations

What is Microeconomics?

The study of economics that examines the behavior of individual decision-making units in the economy. This focuses on specific markets, industries or sectors.

What is macroeconomics?

The study of economics that examines the economy as a whole to obtain a broad overall picture of the economy. It analyses 'aggregates'. Which is the measure of the total economic activity for a nation state or a region.

What is monetary?

Relating to money or currency .The Monetary Economics Program studies the conduct and effects of monetary policy, including its impact on interest rates (price of burrowing money) and inflation (increase in cost of goods and service) , and the consequences of policy actions by central banks. It also considers macroeconomic forces that negatively influences on central bank decision-making.

What is monetary and non monetary in economics?

If it can be converted into cash easily and quickly, the asset is considered a monetary asset.

What is GDP?

GDP ( Gross Domestic Product) measures the monetary value of final goods and services that is, those that are bought by the final user—produced in a country in a given period of time

What does aggregate in economics mean?

An aggregate is a composite value measuring the result of economic activity. The main aggregate is GDP.

Explain the social nature of economics:

Economics is a social science because it deals with human society and behavior, and particularly those aspects concerned with how people organize their activities and how they behave to satisfy their needs and wants. It is a social science because its approach to studying human society is based on the scientific method.

Social economics is primarily concerned with the interplay between social processes and economic activity within a society. Social economics may attempt to explain how a particular social group or socioeconomic class behaves within a society, including their actions as consumers.

Distinguish between Microeconomics and Macroeconomics?

The study of economics breaks down the economic world into two levels. One of these is like looking at the economic world through a microscope, while the other is like looking at it through a telescope.

The micro level, called microeconomics, examines the behaviour of individual decision-making units in the economy. The two main groups of decisionmakers we study are consumers (or households) and firms (or businesses). Microeconomics is concerned with how these decision-makers behave, how they make choices, what are the consequences of their decisions and how their interactions in markets determine prices.

The macro level, called macroeconomics, examines the economy as a whole to obtain a broad or overall picture of the economy. Macroeconomics uses aggregates, which are wholes or collections of many individual units, such as the sum of consumer behaviors and the sum of firm behaviors, and total income and output of the entire economy, as well as total employment and the overall price level.

Explain what scarcity is?

Scarcity, refers to the idea that resources are insufficient to satisfy unlimited human needs and wants. In fact, it is said that if there were no scarcity, there would be no social science of economics. This is because economics is the study of how our scarce or limited resources can best be used in order to satisfy the unlimited needs and wants of human beings

Explain what choice is?

Choice In a very important sense, economics is the study of choice. Since resources are scarce, it is not possible for all human needs and wants to be satisfied. This means that choices must be made about what will be produced and what will be foregone (not produced and therefore sacrificed). Economics studies how different decision-makers make choices between competing alternative options, and analyses the present and future consequences of their choices.

What are factors of production?

Resources that ae fundamental, building blocks for the economy, used to prouduce goods and services. There are four main categories: Land, labor, capital, and entrepreneurship.

Explain what equity is?

Equity is the idea of being fair and just. In economics, the ideas of equity and inequity are usually identified with equality and inequality, and are used mostly in connection with equality in the distribution of income, wealth and human opportunity. In all economic systems, these kinds of inequities or inequalities are present both within and between societies, and are significant issues, as many people cannot meet their basic needs and lack opportunities.

Explain economic well-being?

Economic well-being refers to the levels of prosperity, economic satisfaction and standards of living among the members of a society. Examples include: Security with respect to wealth and income, The ability to pursue one's goal and The ability to have a satisfactory quality of life.

Explain sustainability?

In economics, it is most commonly used to refer to the ability of the present generation to satisfy its needs by the use of resources, and especially non-renewable resources, without limiting future generations' ability to satisfy their own needs. The problem arises because the present generation at any moment in time engages in many economic activities of production and consumption that too often destroy or degrade (lower the quality of) the environment and non-renewable resources. The result of such activities is that future generations will be penalized. Therefore the issue is how to develop methods of production and patterns of consumption that will not result in such environmental and resource destruction and degradation.

Explain Change?

You will often be asked to analyze and evaluate this kind of change in a large variety of contexts

Economists very often study change between one situation and another situation that has been caused by a change in one or more variables. Regarding the study of real-world phenomena, the world is characterized by continuous change in economic events such as institution and technology.

Explain what interdependence is?

Interdependence refers to the idea that economic decision-makers interact with and depend on each other. Interdependence arises from the fact that no one is self-sufficient, requiring ever-increasing degrees of interactions and interdependence. Consumers, workers, firms, governments and all other individuals or groups of individuals depend on one another for the achievement of their economic goals. With increasing globalization (which refers to the interactions and integration of economies world-wide), interdependence increases. Economists must therefore take into consideration both intended and unintended consequences of economic decisions and events when there is a high degree of interdependence.

Explain what intervention is?

Intervention typically refers to government intervention, meaning that the government becomes involved with the workings of markets. While markets offer numerous advantages as a way to achieve important economic objectives, it is generally recognized that markets on their own often cannot achieve important societal goals, such as the goals of equity, sustainability, economic well-being or efficiency. Government's intervene in order to correct for the market's deficiencies.

Explain what efficiency is?

Efficiency refers to making the best possible use of scarce resources to avoid resource waste. In view of the scarcity of resources, it is important to use these in ways that ensure they are not wasted. In part, efficiency means using the fewest possible resources to produce goods and services. But, in addition, it requires that scarce resources are used to produce the goods and services that mostly satisfy society's needs and wants. This is known as allocative efficiency, used as a benchmark or standard to determine the appropriateness of economic actions from the point of view of minimizing resource waste.

TEST QUESTION

What are the advantages and disadvantages of free markets versus government intervention.

Distinguish between the free marker versus the government intervention.

Explain the unlimited human needs and wants to be met by limited resources?

Resources are the inputs used to produce goods and services wanted by people, and for this reason are also known as factors of production. They include things like human labor, machines and factories, and 'gifts of nature' like agricultural land and metals inside the earth. Factors of production do not exist in unlimited abundance: they are scarce, or limited and insufficient in relation to the unlimited uses that people have for them. Scarcity arises whenever there is not enough of something in relation to the need for it. For example, we could say that food is scarce in poor countries. Scarcity is important in describing a situation of insufficient factors of production, because this in turn leads to insufficient goods and services.

What do economists do?

Economists study the world from a social perspective, with the objective of determining what is in society's best interests.

Why does scarcity force choices to be made?

The conflict between unlimited wants and scarce resources has an important consequence. Since people cannot have everything they want, they must make choices. The classic example of a choice forced on society by resource scarcity is that of 'guns or butter', or more realistically the choice between producing defense goods (guns, weapons, tanks) or food: more defense goods mean less food, while more food means fewer defense goods. Societies must choose how much of each they want to have.

Explain scarcity and sustainability?

Economic activities in many (if not most) countries are often achieved at the expense of the natural environment and natural resources. Economic growth, which involves increases in the amount of goods and services produced, very often results in increased air and water pollution, and the destruction or depletion of forests, wildlife and the ozone layer, among many other natural resources. Increasing awareness of this issue has given rise to the concept of sustainable development. It is clear that the problem of sustainability arises because resources are scarce. If they were not scarce, it would not matter at all how fast we used them or destroyed them as there would be plenty more.

When someone is not put into good use what are they called?

Unemployed.

Explain Land?

Land consists of all natural resources, including all agricultural and non-agricultural land, as well as everything that is under or above the land, such as minerals, oil reserves, underground water, forests, rivers and lakes. Natural resources are also called 'gifts of nature'.

Explain Labor?

Labor includes the physical and mental effort that people contribute to the production of goods and services. The efforts of a teacher, a construction worker, an economist, a doctor, a taxi driver or a plumber all contribute to producing goods and services, and are all examples of labor.

Explain Captial?

Capital, also known as physical capital, is a manmade factor of production (it is itself produced) used to produce goods and services. Examples of physical capital include machinery, tools and factories. Physical capital is also referred to as a capital good or investment good. It consists of man-made inputs that provide a stream of future benefits in the form of the ability to produce greater quantities of output.

Explain Entreperneruship?

Entrepreneurship (management) is a skill involving the ability to innovate by developing new ways of doing things, to take business risks and to seek new opportunities for opening and running a business. Entrepreneurship organizes the other three factors of production and takes on the risks of success or failure of a business.

EXAM QUESTION:

Where does the factors of production play in choice?

Factors of production are finite = scarcity = choice

What is the cost of choice?

The concept of opportunity cost, or the value of the next best alternative that must be sacrificed to obtain something else, is central to the economic perspective of the world, and results from the scarcity that forces choices to be made. For example, Every time we choose to do something, we give up something else we could have done instead. For example, your decision to read this book now means you have given up a different activity, such as sleeping. Opportunity cost in this case rises from the fact that time is limited or scarce; if it were endless, you would never have to sacrifice any activity in order to do something else.

What are free goods and an economic good?

A free good is any good that is not scarce, and therefore has a zero opportunity cost. Since it is not limited by scarcity, it includes anything that can be obtained without sacrificing something else. An economic good is any good that is scarce, either because it is a naturally occurring scarce resource (such as oil, gold, coal, forests, lakes), or because it is produced by scarce resources. All economic goods have an opportunity cost greater than zero. For example, arable land in America before European colonizers arrived was a free good because it was so abundant; as the colonizers grew in numbers it became increasingly scarce and therefore an economic good

What are the steps towards the basic economic question?

An economy has to allocate its resources and choose from different potential bundles of goods (What to produce), select from different techniques of production (How to produce), and decide in the end, who will consume the goods (For whom to produce

What are the means of answering the economic question?

1. Market versus government intervention

2. Economic systems: free market economy, planned economy and mixed economy

What is the meaning of government intervention in the market?

In the market method, resources are owned by private individuals or groups of individuals, and it is mainly consumers and firms (or businesses) who make economic decisions by responding to prices that are determined in markets. In the command method, resources (land and capital in particular) are owned by the government, which makes economic decisions by commands. In the last 40 or so years, there has been a trend around the world for economies to rely more and more on the market and less on commands. When the government makes decisions that affect the economy, this is

known as government intervention, because the government intervenes (or interferes) in the workings of markets. Examples of government intervention include provision of public education and public health care.

Whatever the reasons for and types of government intervention in the market, government intervention changes the allocation of resources (and distribution of output and income) from what markets would have achieved working on their own.

What is the common debate on market versus government intervention?

Whereas practically everyone agrees that some government intervention in markets is necessary, economists disagree widely over how much governments should intervene and how they should intervene. There are two broad schools of thought on this issue. One focuses on the positive aspects of markets, while the other focuses on the imperfections of markets.

According to the first perspective, economists argue that in spite of imperfections, markets are able to work reasonably well on their own, and can produce outcomes that generally promote society's well-being. Government intervention changes this allocation of resources, and often

worsens it, giving rise to resource waste. Therefore, while some minimum government intervention may be needed in certain situations, this should not be very extensive.

According to the second school of thought, markets have the potential to work well, but in the real world their imperfections may be so important that they make government intervention necessary for their correction. The purpose of government

intervention, therefore, is to help markets work better and arrive at a better pattern of resource allocation and distribution of income and output.

What are the three ideal types of economies to answer the basic economic question?

The market and command methods to answer the basic economic questions discussed above can be thought of as two 'ideal types' of economies: a free market economy based on the market approach and a planned economy based on the command approach. As we also discussed above, real-world economies combine markets and commands in many different ways, resulting in mixed economies.

The ideal-type free market and planned economies are distinguished from

each other on the basis of three criteria. What are they?

Resource ownership: public or private sector

Economic decision-making

Rationing systems

Distinguish between the free market and the government intervention based on the three criteria's?

In the free market economy households and firms (the private sector) are the main owners of resources, as well as the economic decision-makers who make buying and selling decisions, and who are linked together in product and resource markets. Product and resource markets determine prices of goods, services and resources, which act as the basis of price rationing.

The planned economy is characterized by the absence of markets or the limited operation of markets. As the owner of resources and economic decision-maker, the government makes all allocation and distribution decisions through non-price rationing. This is called a planned economy because the government authority makes detailed plans of all economic

activities, on the basis of which it directs and coordinates economic decisions through commands. There remain very few countries in the world that are still highly centrally planned; these include North Korea and, to a lesser extent, Cuba. Most other countries have begun to introduce major reforms intended to strengthen the role of markets.

Mixed economy: That is, most economic activity is market-based based rather than centralized, and price rationing is more common than non-price rationing. In mixed market economies, public or private sector ownership and decision-making often go together. For example, privately owned firms usually make decisions about what and how they will produce and sell,

while the government makes decisions about economic activities that fall under its ownership (such as public health services, public road systems, public parks, defense facilities and many others).

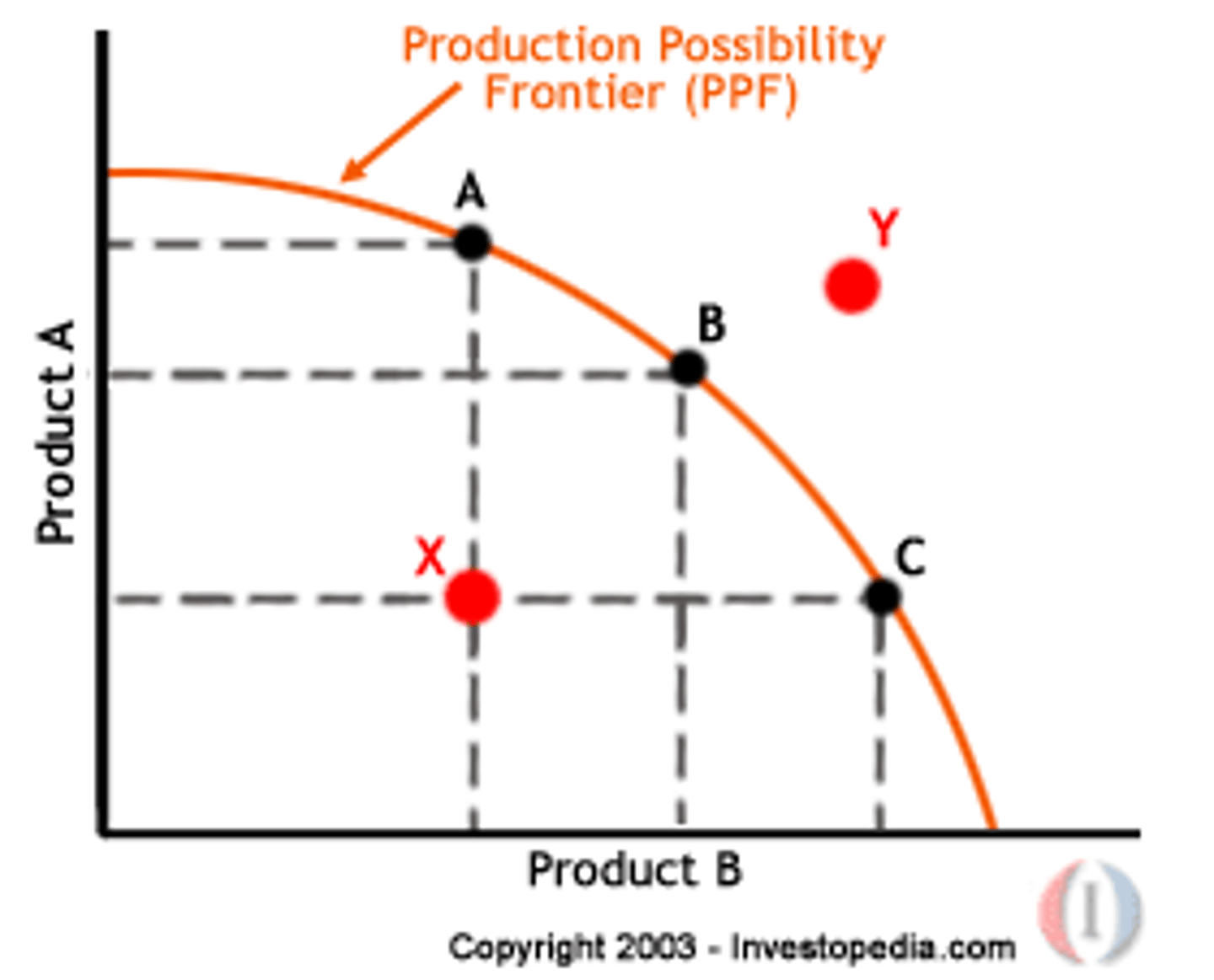

What is the production possibilities curve model?

The production possibilities curve (or frontier) represents all combinations of the maximum amounts of two goods that can be produced by an economy, given its resources and technology, when there is full employment of resources and efficiency in production. All points on the curve are known as

production possibilities.

What must the economy have, in order to produce the greatest possible output?

All resources must be fully employed. This means that all resources are being fully used. If there were unemployment of some resources, in which case they would be sitting unused, the economy would not be producing the maximum it can produce.

All resources must be used efficiently. Specifically, there must be efficient resource use. The term 'efficiency' in a general sense means that resources are being used in the best possible way to avoid waste.

What are the features of the model?- Define all these features

Opportunity cost

Scarcity

Choice

Unemployment of resources

Efficiency

Actual growth and growth in production possibilities

The production possibilities model is very useful for illustrating the concepts of scarcity, choice and opportunity cost: How so?

Because of scarcity, the economy cannot produce outside its PPC. With its fixed quantity and quality of resources and technology, the economy cannot move to any point outside the PPC, such as point G because it does not have enough resources (i.e. there is resource scarcity).

Because of scarcity, the economy must make a choice about what particular combination of goods will be produced. Assuming it could achieve full employment and efficiency, it must decide at which particular point on the PPC it should produce.

Because of scarcity, choices involve opportunity costs. If the economy were at any point on the curve, it would be impossible to increase the quantity produced of one good without decreasing the quantity produced of the other good. In other words, when an economy increases its production

of one good, there must be a sacrifice of some quantity of the other good.This sacrifice is the opportunity cost.

What is economic growth?

Economic growth refers to increases in the quantity of output produced in an economy over a period of time.

What is the difference between actual growth and growth in production possibilities?

It is important to distinguish between actual growth, which involves a movement from one point inside the PPC to another point closer to the PPC, and growth in production possibilities involving an outward shift of the PPC. Actual growth is caused by reduction in unemployment and increases in efficiency in production. Growth in production possibilities is caused by

increases in the quantity of resources, improvements in the quality of resources and technological improvements.

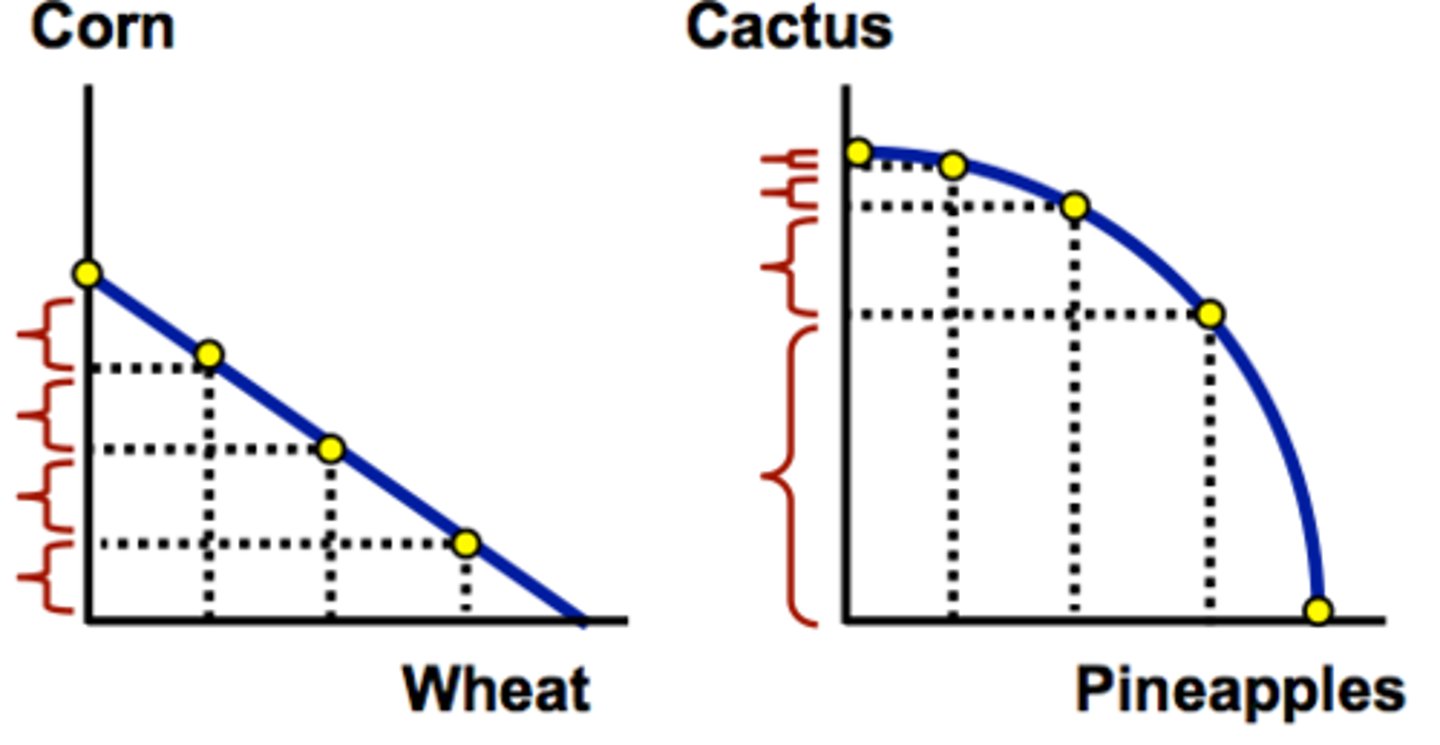

Distinguish between increasing versus constant opportunity cost?

Constant costs imply that all resources are of equal quality and that they are all equally suited to the production of both commodities. Increasing opportunity costs mean that for each additional unit of G produced, ever-increasing amounts of D must be given up.

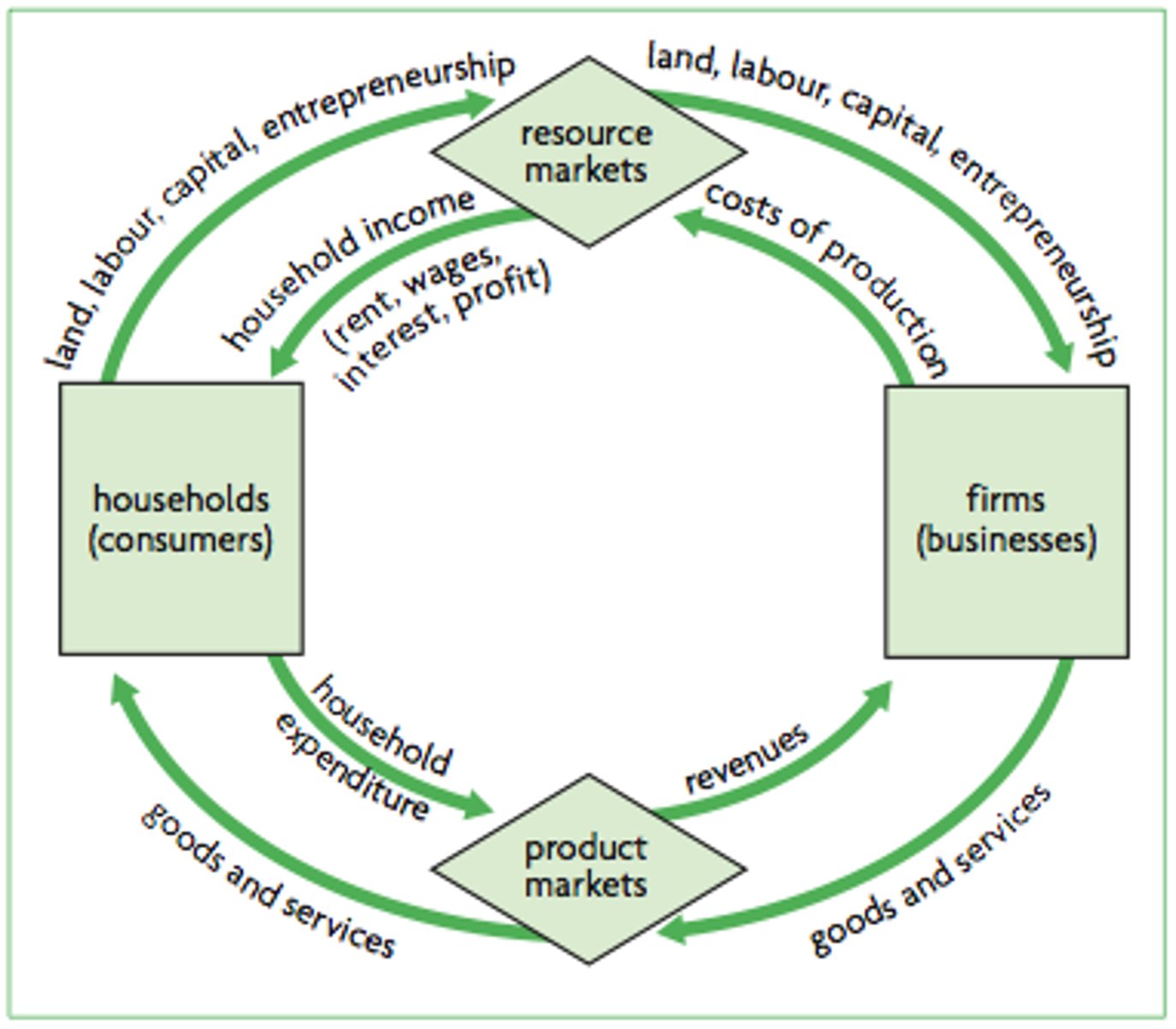

What is the circular flow of income model?

The circular flow of income model is a simple model that illustrates some economic concepts and relationships that will help us understand the overall economy. This model demonstrates an important principle: the income flow involving the money that goes from firms to households is equal to the expenditure flow from households to firms, which is the money that households spend to buy things from firms. In other words, the household incomes coming from the sale of all the factors of production equals the expenditures by households on goods and services. The circular flow of income shows that in any given time period (say a year), the value of output produced in an economy is equal to the total income generated in producing that output, which is equal to the

expenditures made to purchase that output.

Analyze the circular flow of income model?

Households are owners of the four factors of production: land, labor, capital and entrepreneurship. Firms buy the factors of production in resource markets and use them to produce goods and services. They then sell the goods and services to consumers in product markets. We therefore see a flow in the

clockwise direction of factors of production from households to firms, and of goods and services from firms to households.

In the counterclockwise direction, there is a flow of money used as payment in sales and purchases. When households sell their factors of production to firms, they receive payments taking the form of rent (for land), wages (for labor), interest (for capital) and profit (for entrepreneurship). These payments are the income of households. The payments that households make to buy goods and services are household expenditures (or consumer spending). The payments that firms make to buy factors of production represent their costs of production, and

the payments they receive by selling goods and services are their revenues. All payment flows, known as money flows, are shown in Figure 1.4

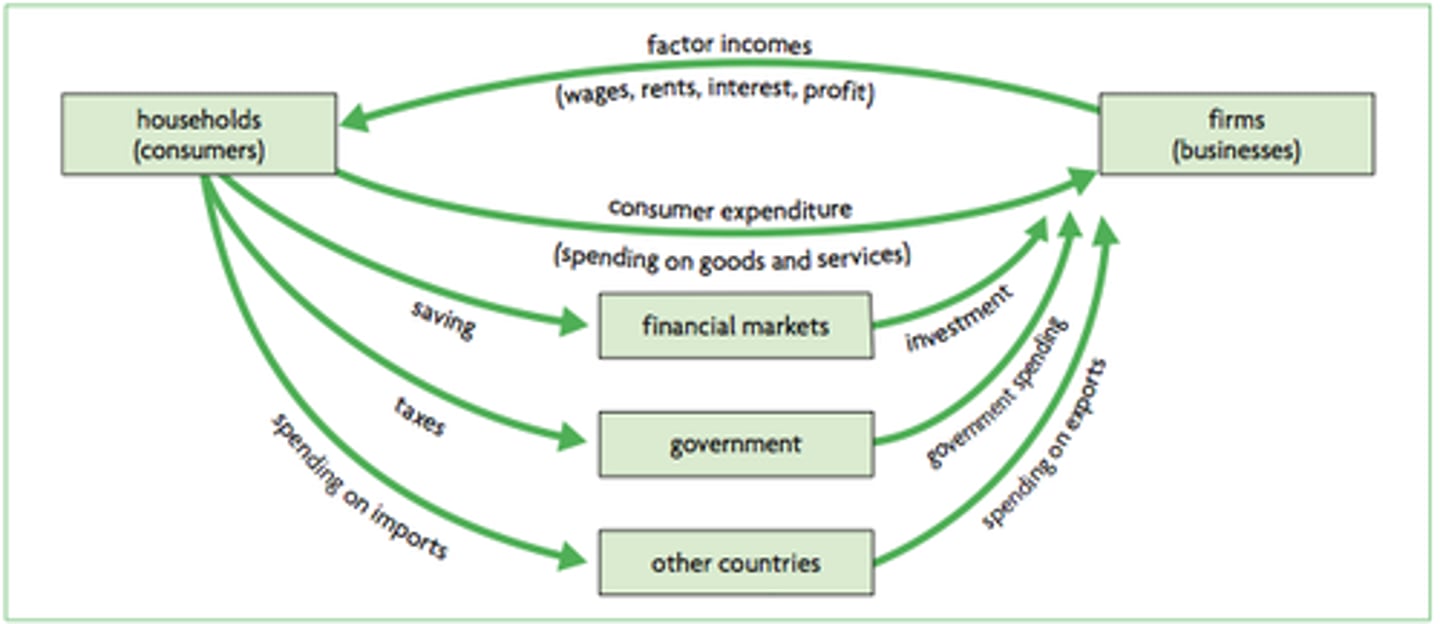

What are the type of leakages and injections?

Leakages and injections are paired together so that what leaks out of the flow can come back in as an injection.

LEAKAGES:

saving

taxes

imports

Saving and investment

INJECTIONS:

investment

government spending

exports

How do leakages and injections work in a circular flow of income model?

When households save part of their income, this represents a leakage from the circular flow of income because it is income that is not spent to buy goods and services. Households place their savings in financial markets (bank accounts, purchases of stocks and bonds, etc.). Firms obtain funds from financial markets (through borrowing, issuing stocks and bonds, etc.) to finance investment, or the production of capital goods. These funds therefore flow back into the injections investment

government spending exports expenditure flow as injections.

What is positive economics?

Positive economics is concerned with objective statements of how a market or an economy works. These positive economic statements are based on empirical evidence and tend to be statements of fact. They can be proven to be true or false. Positive statements are used to describe, explain or predict economic events by use of hypotheses, theories and models.

Examples of positive economic statements include:

The unemployment rate in India has fallen from 8% to 7.3% in the past twelve months

Increasing the minimum wage last year in the UK resulted in improvements to wage inequality

Prices in the EU have risen dramatically, partly due to the 20% increase in the price of oil

What are normative economics?

Normative economics focuses on value judgements

These judgements are built around opinions and beliefs as to what the best economic policies or solutions may be

Examples of normative economic statements include:

Every economy should aim to provide free healthcare for its citizens

Corporation taxes in an economy should be higher than personal income taxes

EXAM TIP:

In short answer questions, should you wish to provide an example of a positive or normative statement ensure that normative statements have the word 'should' in them. Positive statements usually include data that is hard to challenge.

What is the use of logic in the role of positive economics?

When analyzing markets, a range of assumptions are made about the rationality of economic agents ( people) involved in the transactions all to try to describe, explain or make predictions about economic events. Example: Producers are assumed to act rationally. They do this by selling goods/services in a way that maximizes their profits

What does rational mean?

Means that economic agents are able to consider the outcome of their choices and recognize the net benefits of each one

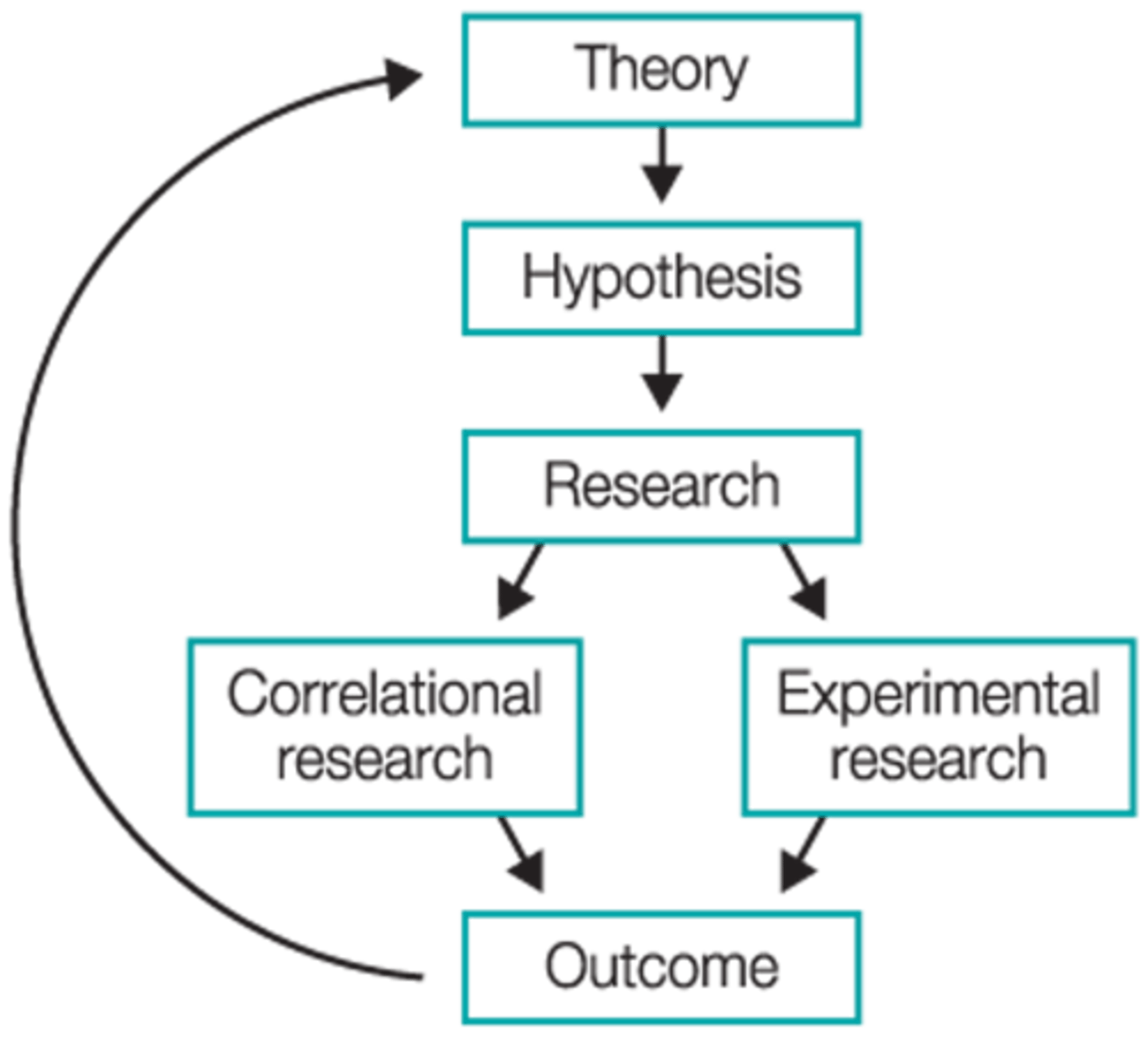

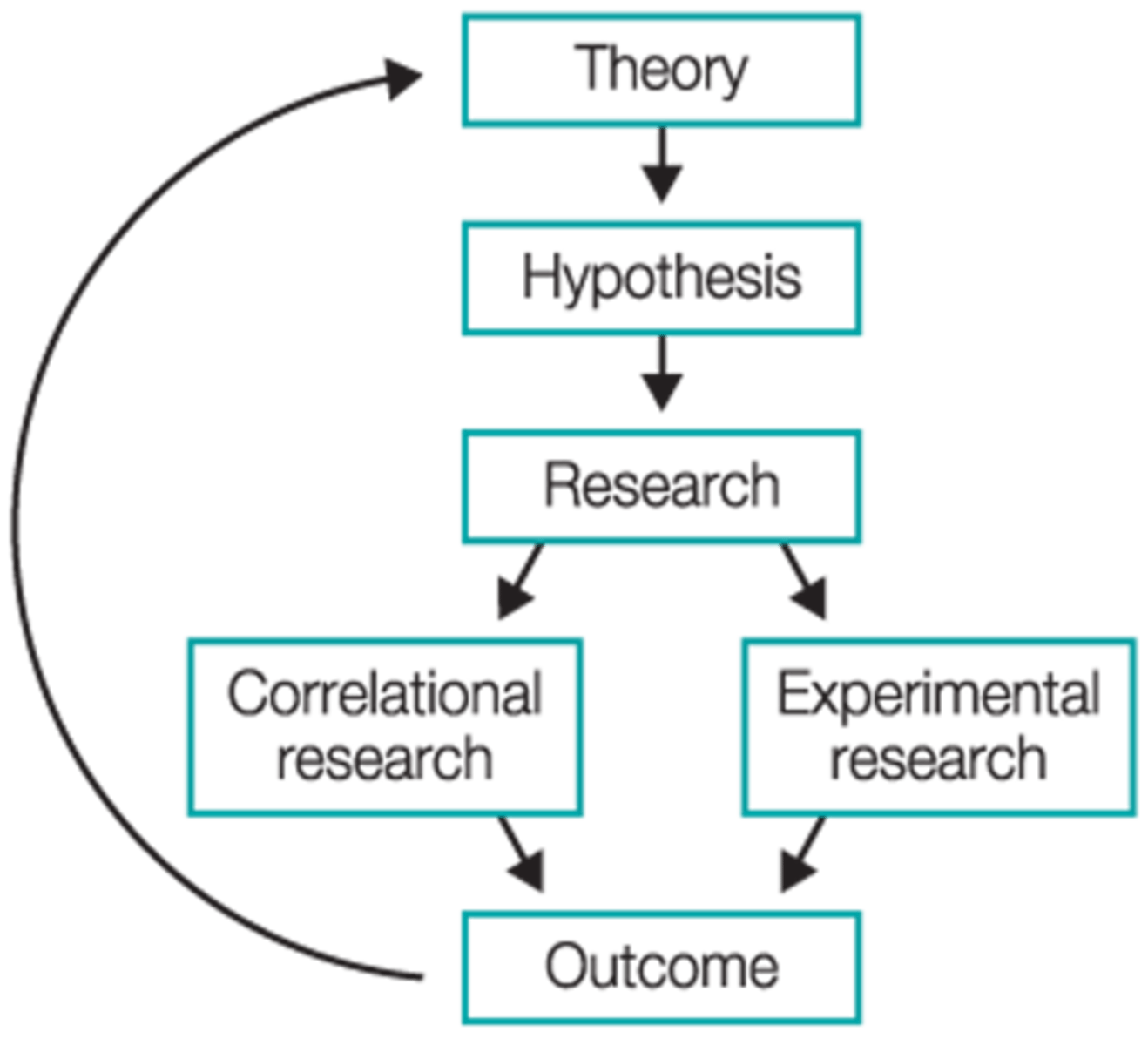

Why can Economics not have scientific experiments?

The social sciences use a variation of the scientific method of research which is called the social scientific method

There is an inability to make scientific experiments the results of which can be proven time and time again This is due to the complexity of human nature and the significant number of social interactions that are taking place in any economy at any given point in time.

Explain how social scientific method uses empirical research to gather data?

We have seen that a hypothesis is an educated guess about a cause-and- effect relationship in a single event ( Hypothesis) . A theory is a general explanation of a set of interrelated events, usually (though not always) based on several hypotheses that have been tested successfully ( Empirical Evidence). Economic models are developed by economists once a hypothesis has been repeatedly proven or rejected in different circumstances. (Report Conclusion).

What is empirical evidence?

The social scientific method uses empirical research to gather data. Empirical research is collected through observations, surveys, opinion polls etc. The results of the same hypothesis can vary significantly when conducted by different researchers at different time periods and between different places and cultures. Empirical evidence is information that researchers generate to help uncover answers to questions that can have significant implications for our society.

What is a refutation?

Refutation is the act of a statement or theory being proved to be wrong by the empirical evidence. Refutation helps to determine if an economic statement is positive.

What is the ceteris paribus assumption?

Due to the large number of variables that can influence any particular economic interaction in society, economists create models using the principle of ceteris paribus

Translated from Latin, ceteris paribus means 'all other variables remain constant'

It allows economists to simplify and explain causes and effects, even if the explanation is somewhat limited by the assumptions

E.g. There are many factors that affect the level of unemployment in an economy (interest rates, consumer confidence, firms' investment, government policies etc.). Using ceteris paribus, economists can simplify the economic model to analyse just two variables (e.g. unemployment and interest rates

EXAM TIP:

In your examinations, the essay questions test your ability to think critically. The command words for these questions are evaluate, discuss, or examine.

One way in which you can demonstrate critical thinking is to challenge the underlying assumptions of economic theory. The idea of rational decision making is one such assumption. Do consumers act rationally when they make impulse purchases? Do workers act rationally when they accept terrible working conditions for mediocre pay? Do governments actually maximise public welfare or do they implement policies that mainly benefit their core voter base?

Irrationality distorts markets and produces fundamentally different outcomes than what would be achieved if all economic agents acted rationally.

What are the value judgements in policy making?

Value judgements"] influence governments' choices with regards to the economic policies they choose to adopt and spend money on. A value judgement is often prescriptive, i.e. a normative view might be expressed that reveals certain attitudes or behaviours toward the world. All government economic policies are influenced by value judgements, which vary from person to person, resulting in fierce debate between competing political parties

The USA spends more money on imprisoning drug users than rehabilitating them

In the UK, the Government has recently increased its spending on rehabilitation

To say the UK approach is better would be a normative statement

To say that the UK government spends more per head on rehabilitation would be a positive statement

What is the meaning of equity?

Equity is concerned with economic fairness in the distribution of resources

Individuals and societies have different views on what is fair and this influences government policyE.g. Some countries believe it is fair for all of their citizens to be able to access healthcare, irrespective of their ability to pay, whereas other countries believe that 'no pay, no access' is fair

What is the meaning of equality?

Equality is concerned with everyone being equal and having equal recognitionEquality is often a normative concept. When are all people equal? When do people all have equal opportunities?Statistics on inequality would be considered to be positive economic statementsE.g. In 2018, women in the USA were paid 12% less than men in comparable jobs

Who was Adam Smith?

Adam Smith published his famous book on Economics in 1776: The Wealth of Nations. He is widely regarded as the father of Classical Economics. Written at the start of The Industrial Revolution, it captured his thoughts on how markets could be coordinated by demand and supply. This book was a natural response to the previous century of government intervention in markets in Europe during a period known as mercantilism

What is classical economics?

The belief that the economy can regulate itself without government intervention

What was laissez faire?

A philosophy which believes there should be no (or minimal) government intervention with regard to decisions about resource allocation and production

What was the Classical microeconomics (utility) idea?

The idea of utility as a concept challenged what classical economists believed about how a product should be priced

Previously, prices were a function of the costs of production involved. Now prices were seen as a function of the satisfaction gained in consumption

Producers should increase production for goods with high consumer utility

Utility theory assumes that consumers always act rationally (yet many purchasing decisions are based on emotion)

What was the concept of the margin idea?

Marginal utility is the additional utility (satisfaction) gained from the consumption of an additional product

The utility gained from consuming the first unit is usually higher than the utility gained from consuming the next unitE.g. A hungry consumer gains high utility from eating their first hamburger. They are still hungry and purchase a second hamburger but gain less satisfaction from eating it than they did from the first hamburger

To calculate total utility, the marginal utility of each unit consumed is added togetherThis means that total utility keeps increasing even while marginal utility is decreasing

What was the Classical Macroeconomics ( Soy's Law) idea?

Say's law of markets was developed in 1802 by the classical, laissez-faire economist Jean-Baptise Say

It can be summed up with the phrase 'supply creates its own demand'

By supplying goods to the market a producer generates income from sales which they can then use to purchase (demand) more products

This law implies that increasing national output in an economy is vital to income generation and thus governments should focus on generating production and be less concerned with consumption

What was Karl Marx's critic on classical economy?

Karl Marx, a German philosopher, identified that wealth seemed to come from worker exploitation (a natural function of profit maximization) and that inequality was deepening in societies. The exploitation was seen in low wages and poor working conditions. The owners of the factors of production (capitalists) generated the highest income (wages, interest, rent and profit). If all someone had to offer was labor, and wages were suppressed: then inequality was bound to increase.

Marx argued that capitalism would eventually lead workers to revolt and that periods of exploitation would be followed by revolutions. These revolutions would require government intervention to restore stability and equality. Governments would need to be involved in the allocation of resources (command economy) to prevent the pattern from repeating

What is command economy?

an economy in which production, investment, prices, and incomes are determined centrally by a government.

What was Keynes revolution?

Keynes believed that Governments needed to stimulate demand by increasing government spending

This would begin to increase the flow of income in the economy which would further stimulate demand which would help markets to function again

He developed the term and field of 'Macroeconomics' by explaining how aggregate demand is calculated

He argued that the use of Fiscal Policy was essential to stabilize an economy during periods of recession or depression, much more so than the use of Monetary Policy

What was Keynes's policy?

Fiscal policy was the use of government spending and taxation to influence the economy and achieve macroeconomic objectives.

What is aggregate demand?

Consumption + Investment + Government Spending + ( Exports - Imports)

What is the Monetary policy?

the adjustment of interest rates and the quantity of money to achieve the dual objective of price stability and full employment

What did monetarists believe?

Monetarism is an economic school of thought which emphasizes the use of Monetary Policy to influence an economy

Monetarists believe that poor monetary policy lead to the Great Depression

Monetarists believe that the use of fiscal policy leads to inflation as government spending increases aggregate demand

Who was the leading monetarist?

Milton Friedman was one of the leading Monetarists of the late 20th Century

His ideas influenced Ronald Reagan in the USA and Margaret Thatcher in the United Kingdom

Both Governments moved away from Keynesian economics

What happened in the New Classical Counter Revolution?

From the early 1980s there was a resurgence in the belief in classical economics and laissez-faire markets. Government spending reduced and the focus shifted to Supply-Side Policies. One prominent Supply-Side Policy that the USA and the UK embraced was the use of privatization

Wha is the supply-side policy?

These aims to improve the quantity/ quality of the factors of production thereby raising potential output.

What was privatization?

The transfer of ownership and control of firms/assists from the state ( public sector) to the private sector.