IB Economics - 2.1 - 2.4

1/49

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

50 Terms

Market

A place where buyers and sellers meet and exchange different goods and services.

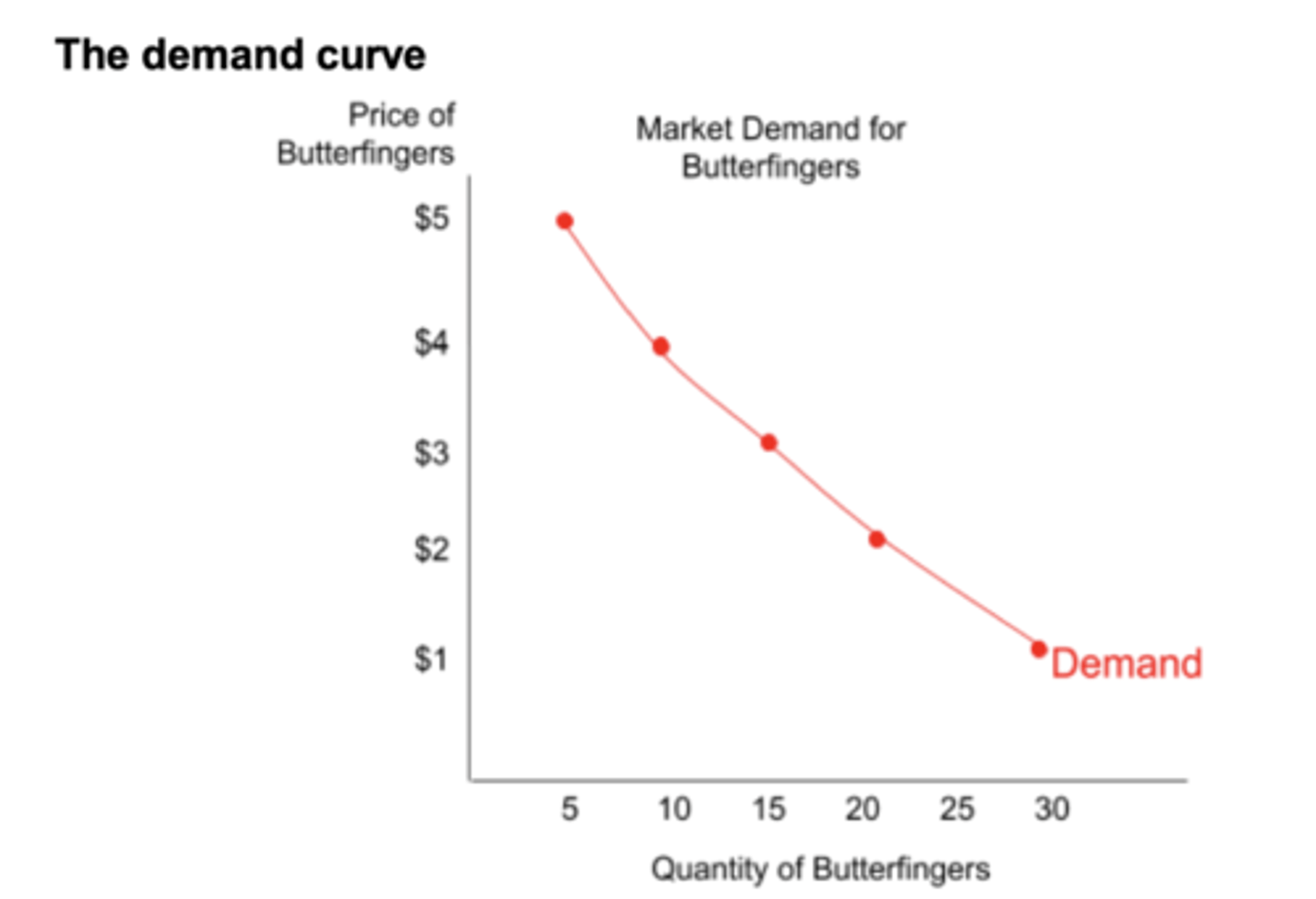

Demand

The willingness and ability of an individual to buy goods and services at different price levels.

Law Of Demand

The quantity demanded of a good or service is inversely proportional to its price, ceteris paribus.

Market Demand

The sum total of all the individual demands of the consumers in the market.

Demand Curve

A graph that shows the inverse relationship between QD and price.

Explanations for the law of demand

The income effect

The substitution effect

The law of marginal utility

The Income Effect

If the price decreases, the proportion of income it occupies in the consumer's income decreases. This increases the consumer's purchasing power, increasing their QD. (and vice versa)

The substitution effect

As the price of a good decreases, consumers switch from other substitute goods to this good because its price is comparatively lower. (and vice versa)

The law of diminishing marginal utility

As we consume additional units of something, the satisfaction (utility) we derive for each additional (marginal) unit grows smaller (diminishes). Therefore, consumers are only willing to buy more of a good when its price falls.

Movement VS Shift in the Demand Curve

Movements along the demand curve are caused due to changes in prices.

Shifts in the demand curve are caused due to non-price determinants.

Determinants of Demand (6)

- Tastes and Preferences of Consumers: A change in consumers’ tastes and preferences will cause demand for a good to either increase (if it is more preferred) or decrease (if it is less preferred)

- Other related goods' prices: Prices of substitute and complementary Goods

- Expectations of future prices: If consumers expect that prices in the future will rise, demand today will fall and vice versa.

- Incomes: The higher the disposable income of a consumer, the higher their demand for certain goods.

- Size of the market: An increase in the number of consumers will increase the demand for a good and vice versa.

- Special Circumstances: Changes in weather, natural disasters, wars, pandemics, etc.

Supply

The willingness and ability of producers to produce goods and services at different price levels.

Market Supply

The sum of all the individual suppliers of a market.

Law of Supply

The quantity supplied of a good or service is directly proportional to its price, ceteris paribus.

Supply Curve

A graph that shows the direct relationship between QS and price.

Vertical Supply Curve

Indicates that even if the price increases, QS cannot increase, as:

- There is no time to produce more of it in the short term (e.g. theatre seats)

- It is no longer produced (e.g. ancient artefacts)

Non-Price Determinants of Supply (7 (TFAR))

- Subsidies: Reduce the CoP and increase the supply.

- Taxes: Increase the CoP and decrease the supply

- Technology: New technologies can make supply more efficient

- Other related goods' prices

- Resource Costs

- Expectations of Producers: If firms expect prices to rise, they will increase the production beforehand and vice versa.

- Size of the market: If the number of firms in the market increases, supply increases and vice versa.

Other related goods' prices

If another good that a firm could produce rises in price, firms will produce more of it and less of what they used to produce, decreasing supply.

If substitutes in production get cheaper, firms will increase production of the now more profitable good, increasing supply.

(e.g. A firm produces milk and curd. If the price of curd increases, they will allocate more resources to increase the supply of curd and thus earn more profit. The supply of milk will decrease.)

Explanations of the law of supply

The law of diminishing marginal returns

Increasing marginal costs and the firm's supply curve

Short Run

A time period during which at least one FoP input is fixed. (e.g. a firm can hire more labour and buy more machines, but stay in the same factory. Since land is fixed, the firm is operating in the short run)

Long Run

A time period during which all FoP inputs are variable.

(e.g. a firm can hire more labour and buy more machines and shift to a different factory. Since all the FoP inputs have been changed, the firm is operating in the long run)

Total product

Total quantity of output produced by a firm

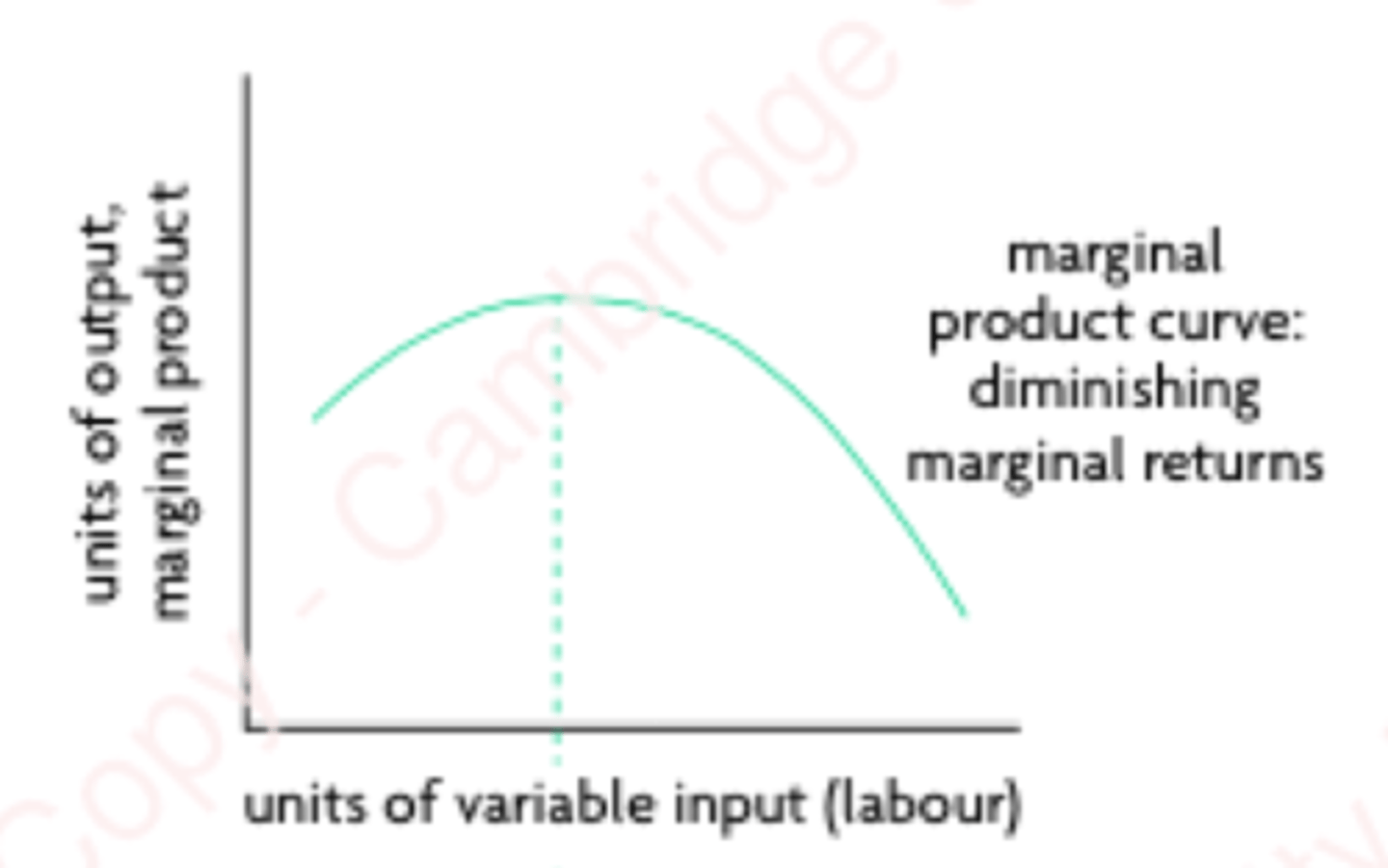

Marginal Product

The extra or additional product produced by one additional unit of variable input (usually labour).

Marginal Product Curve

Law of diminishing marginal returns

As more and more inputs of a variable input (such as labour) are added to one or more fixed inputs (such as land), the marginal product of the variable increases at first, but there comes a point where it begins to decrease. This relationship assumes that the fixed input(s) remain fixed and that the production technology is also fixed.

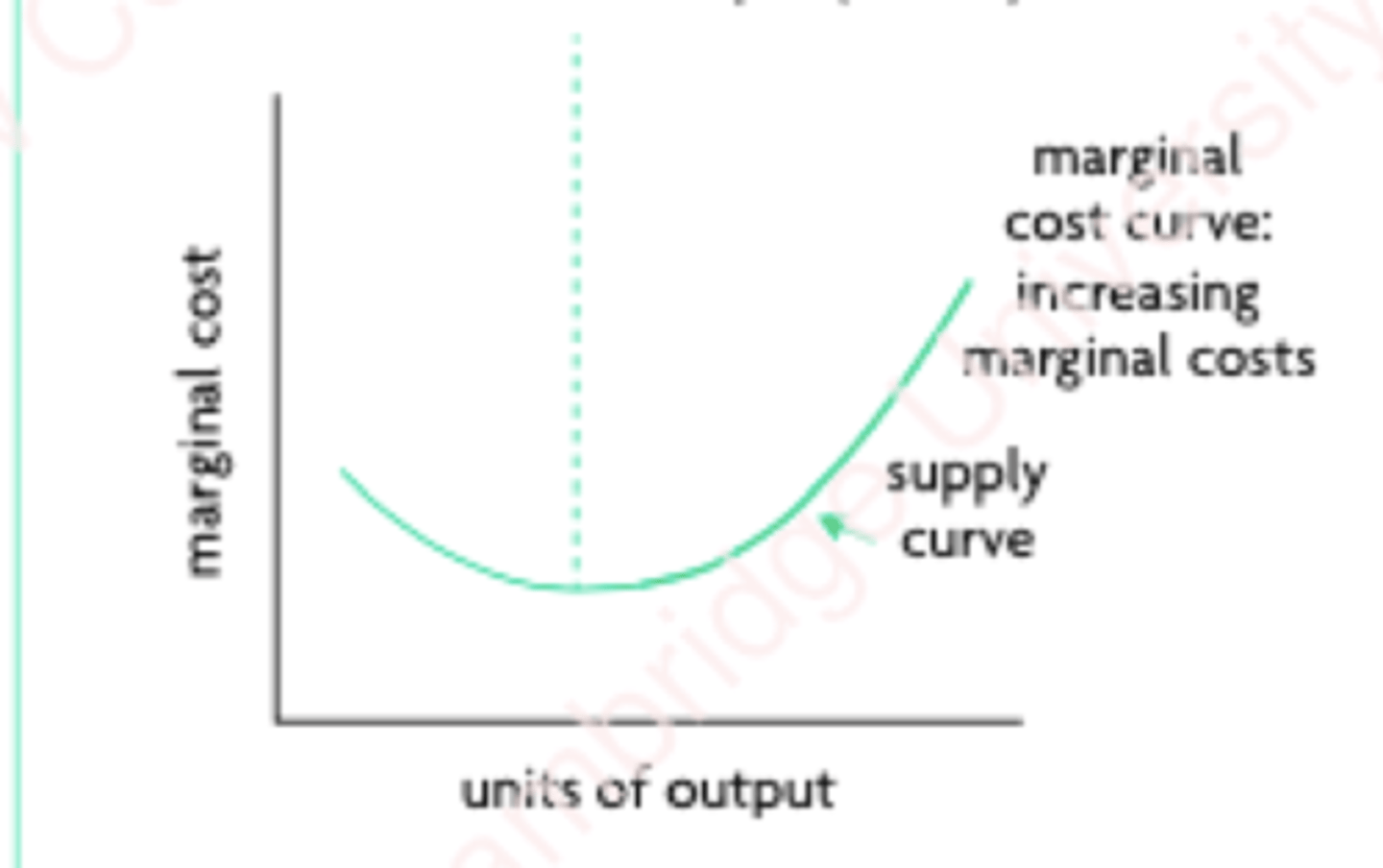

Marginal Cost

The extra or additional cost of producing one or more units of output.

It decreases at first and then increases.

How marginal costs are related to diminishing marginal returns

When marginal product increases, marginal cost decreases; when marginal product is maximum, marginal cost is minimum; and when marginal product falls, marginal cost increases.

Marginal Cost Curve

Equilibrium Price

The price of a good at which QD = QS

Equilibrium Quantity

The quantity of output where in QD = QS

Surplus

When QS > QD

Shortage

When QS < QD

How to resolve a surplus

Decrease prices to increase QD

Decrease/Withhold supply to reduce QS

How to resolve a shortage

Increase prices to decrease QD

Increase production to increase QS

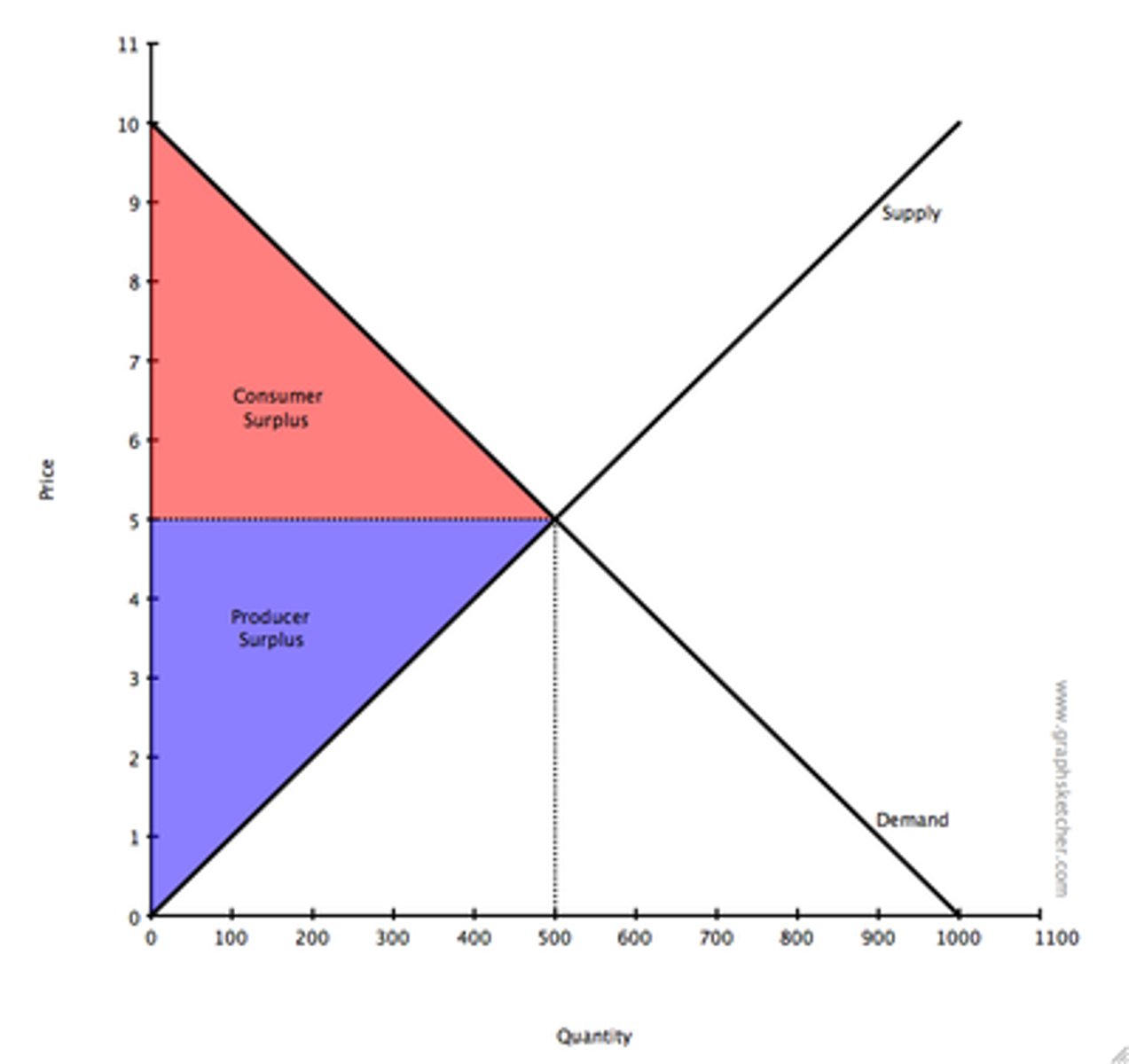

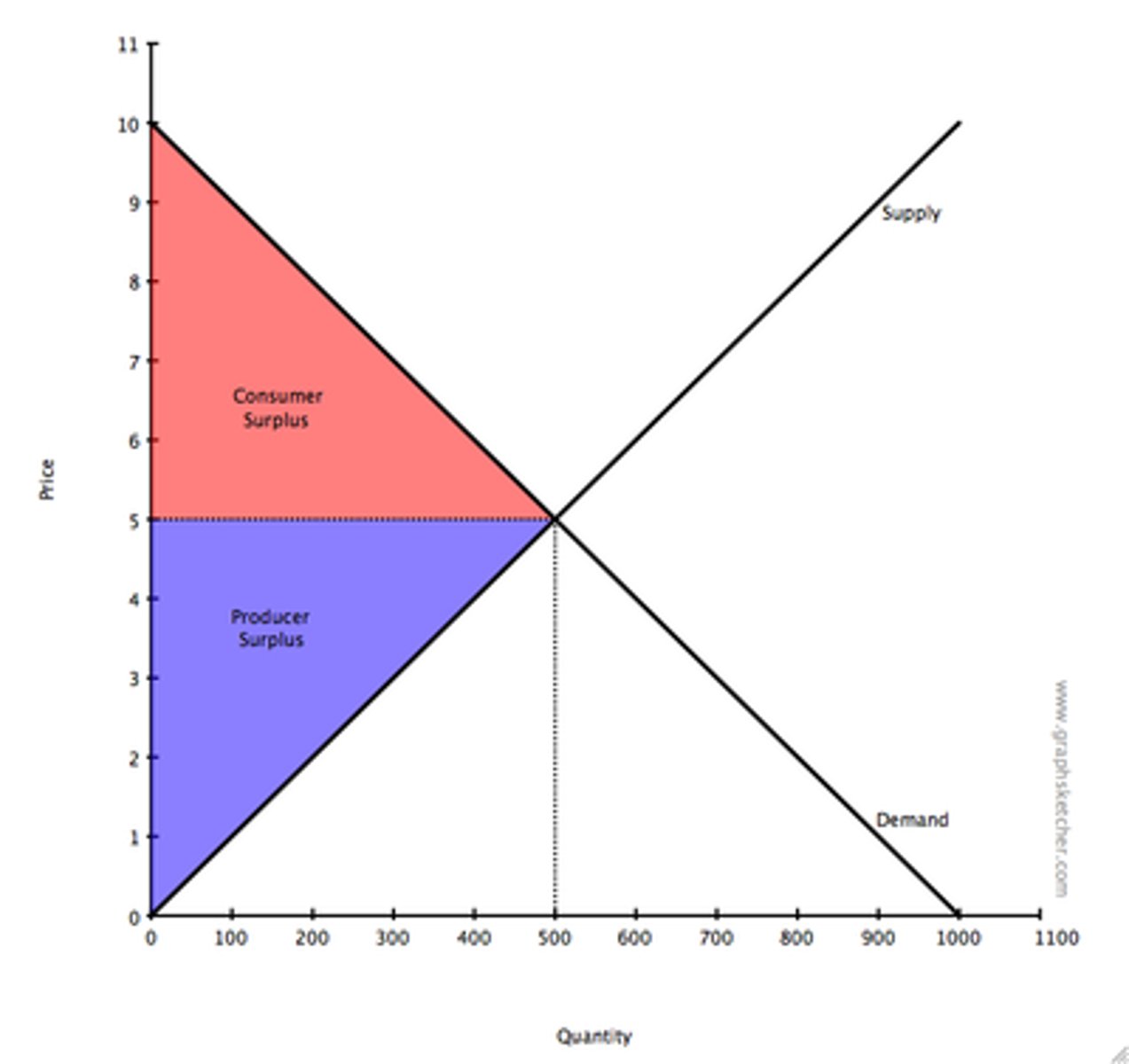

Consumer Surplus

The difference between the highest price a consumer is willing to pay for a good minus the actual price the consumer pays.

The upper triangle.

Producer Surplus

The difference between the lowest price a firm would be willing to accept for a good or service minus the price they actually receive.

The lower triangle.

Total surplus

Consumer surplus + Producer surplus

Allocative Efficiency

When a market maximizes consumer and producer surplus.

- The correct quantity is being produced

- Every unit produced is consumed

Marginal Social Benefit

Demand

The social benefit derived from the consumption of every additional unit of a good or service.

It decreases at higher levels of output because additional units of a good bring benefits to fewer and fewer people.

Marginal Social Cost

Supply

The social cost brought about by the production of an additional unit of a good or service.

Allocative Efficiency Formula

MSB = MSC

Deadweight Loss

Welfare loss due to price not being at equilibrium.

Rational economic decision making

Assumption that consumers will always try to maximise benefit and purchase for the lowest price whenever making purchasing decisions.

Assumptions of rational consumer choice

Consumer rationality: Preferences are certain and consistent.

Perfect Information: All possible information is available when making decisions

Utility maximisation: Maximising satisfaction

Limitations of the assumptions of rational behaviour

Biases:

- Anchoring to estimate the price of a product.

- Framing to present information differently

- Bounded Rationality: seeking a decision that will be good enough, rather than the best possible decision.

- Imperfect Information to not make optimal choices.

Behavioural Economics in Action

- Choice architecture

- Nudge theory

Nudge theory

A method designed to influence consumers' choices in a predictable way without offering financial incentives.

Choice Architecture

The design of environments in which people make choices by changing how options are presented.

Rational Producer Behavior

Profit Maximization

Alternative Business Objectives

- Corporate Social Responsibility - protecting the environment, supporting human rights and donating.

- Maximizing Market Share

- Growth Maximization

- Revenue Maximization

- Satisficing - achieving a satisfactory level of all objectives.