Fin 316 Class 12

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

18 Terms

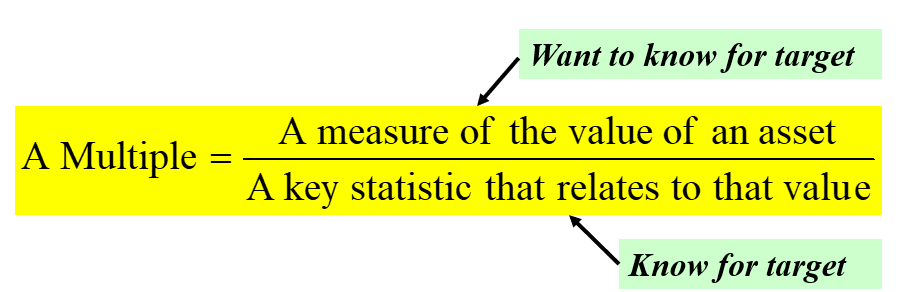

Multiples method for valuing a company

1.Select comparable assets/firms (“comps”).

2.Choose and calculate appropriate multiples for these comps; average the multiples across the comps.

3.Assume these averages hold for the company of interest and apply them to get EV.

4.Take the resulting EV and get the stock price.

Step 1 of the multiples method

Select comparable assets/firms (“comps”).

We want firms with similar risk, growth, and cash flow characteristics.

Practically, this usually means firms in the same industry, selling the same products.

How many? It’s a tradeoff. More reduces the impact of outliers, but as you add more they may not be as comparable. 3-5 is pretty good. Can vary a lot.

Step 2 of the multiples method

For a bag of marbles

Price of bag/# marbles

Price of bag/weight

For a house

House price/sq foot

House price/bedroom

Common finance multiples:

EV/EBITDA

EV/Sales

EV/ [some industry specific measure]

EV/subscribers for cable TV firms

EV/”eyeballs” for internet firms

EV/oil reserves for oil companies

Stock price/Earnings per share (P/E)

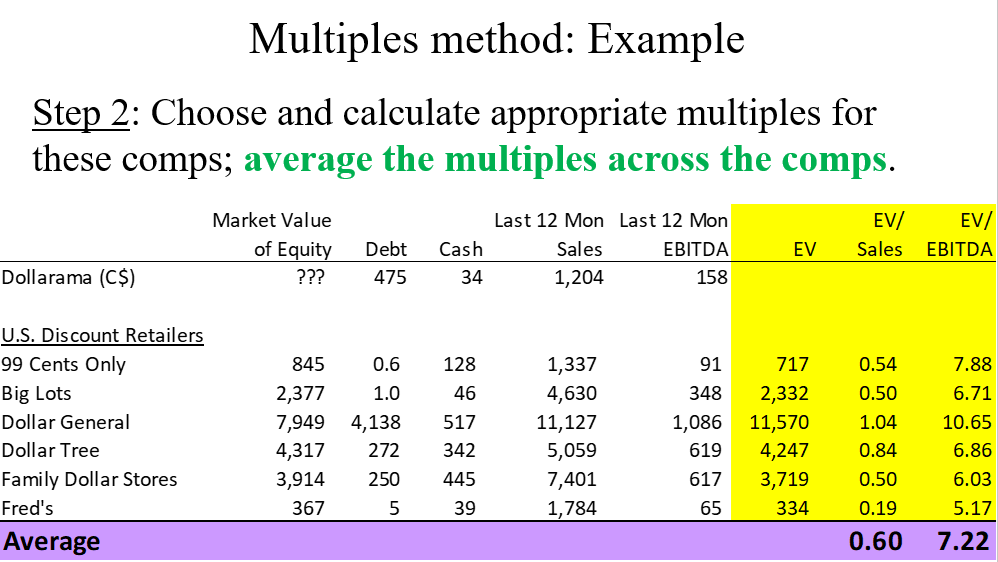

Choose and calculate appropriate multiples for these comps; average the multiples across the comps.

Suppose we chose EV/EBITDA and EV/Sales.

For each comp, find/calculate EV, EBITDA, Sales.

Now you can calculate EV/EBITDA, EV/Sales.

Lastly, average them across the comps.

In step 2, what is the one common finance multiple that does NOT work?

EV/Net income

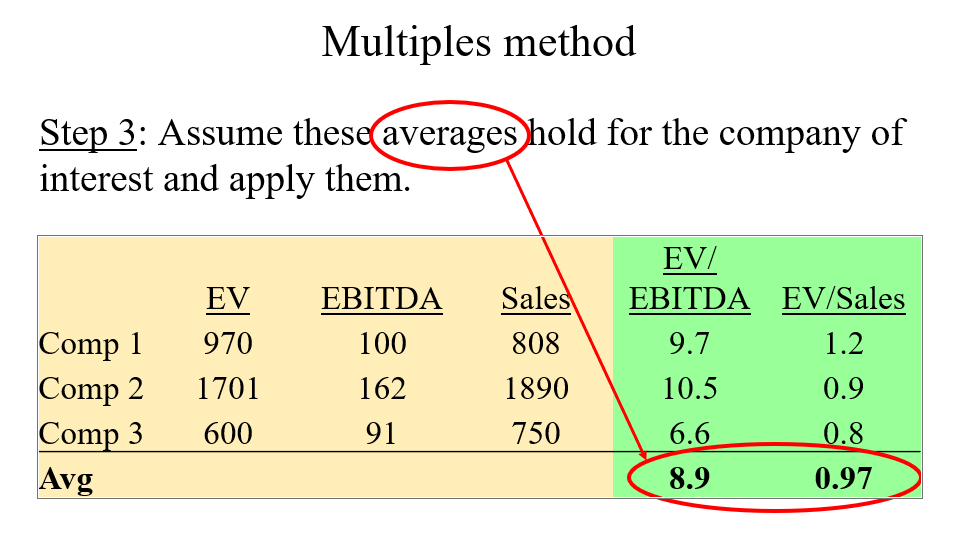

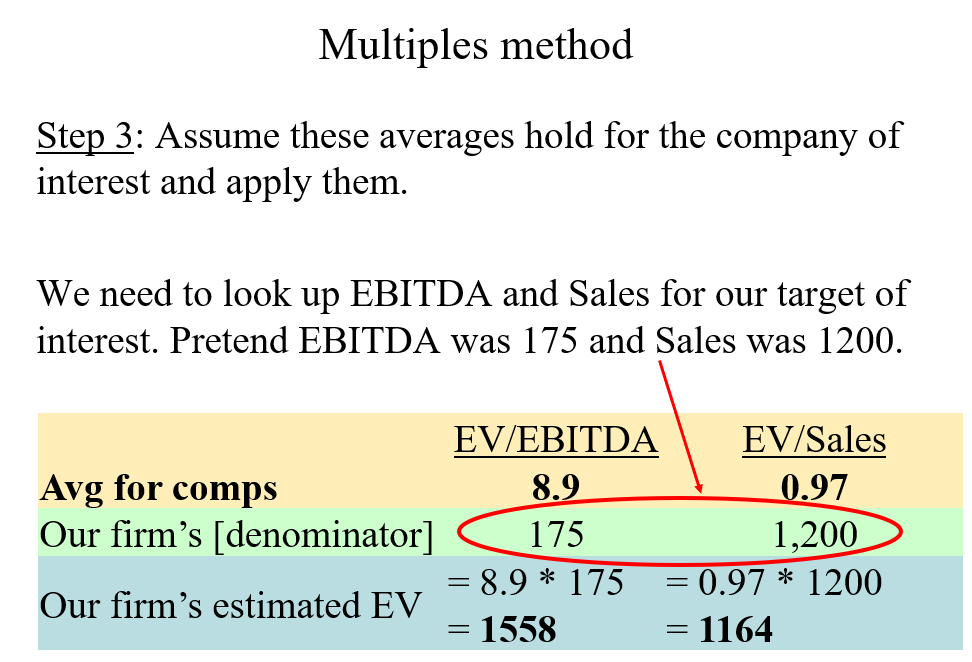

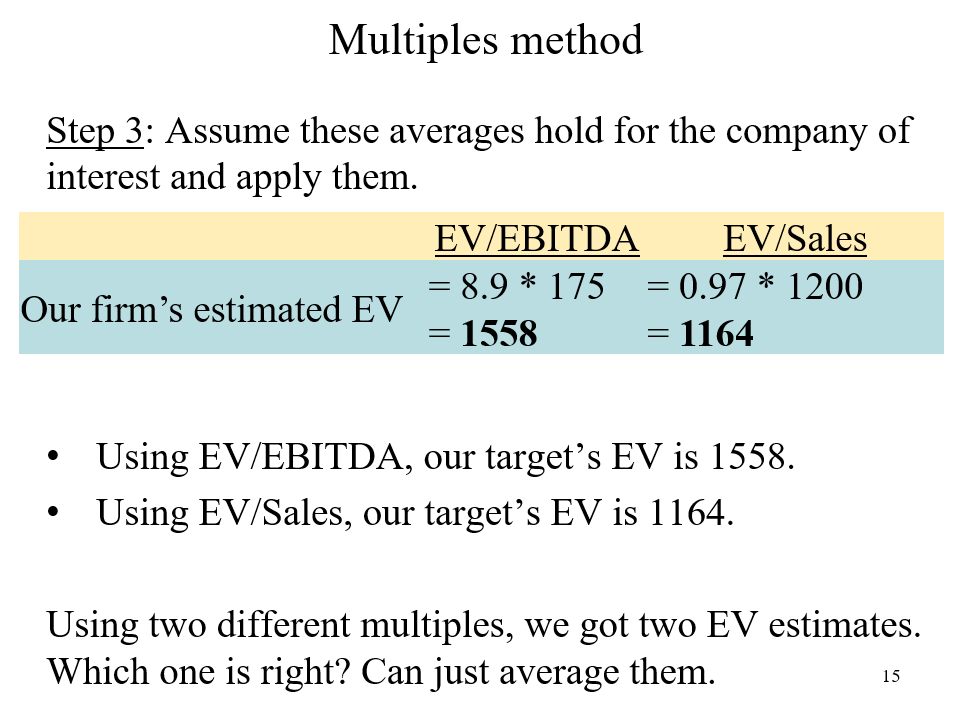

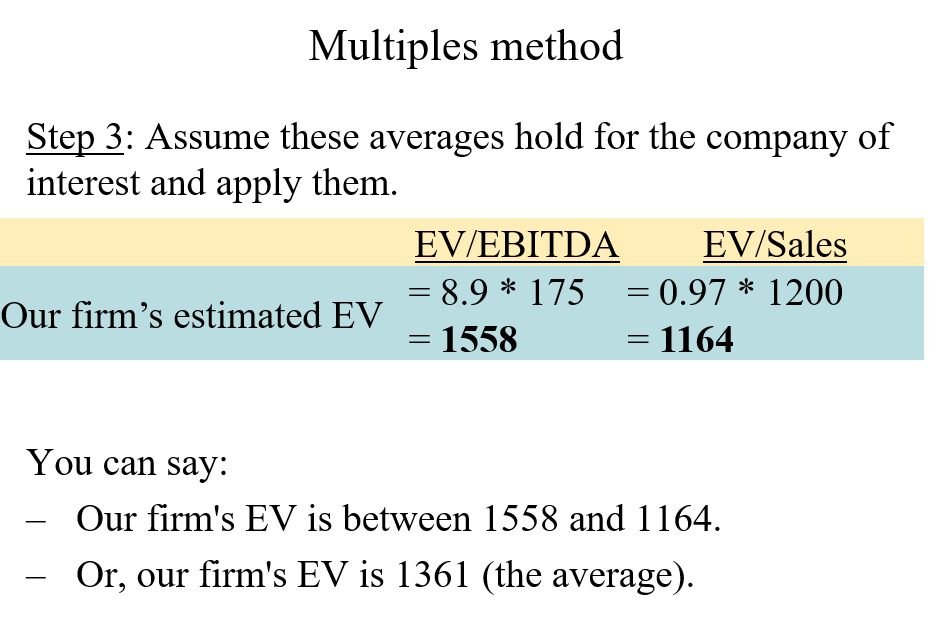

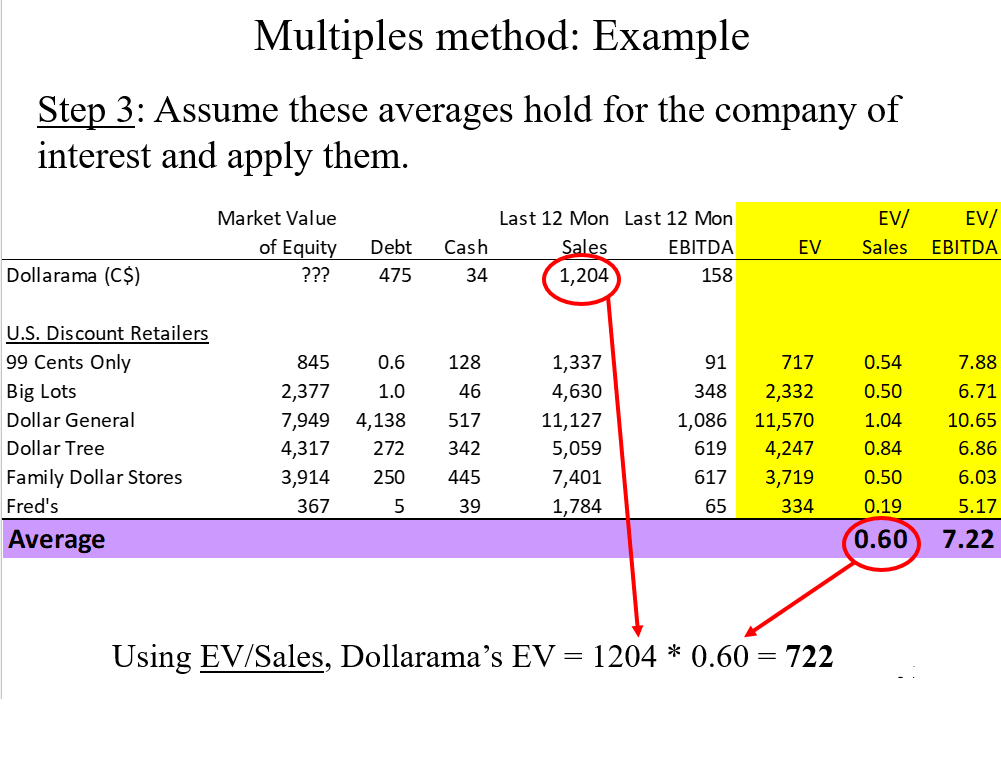

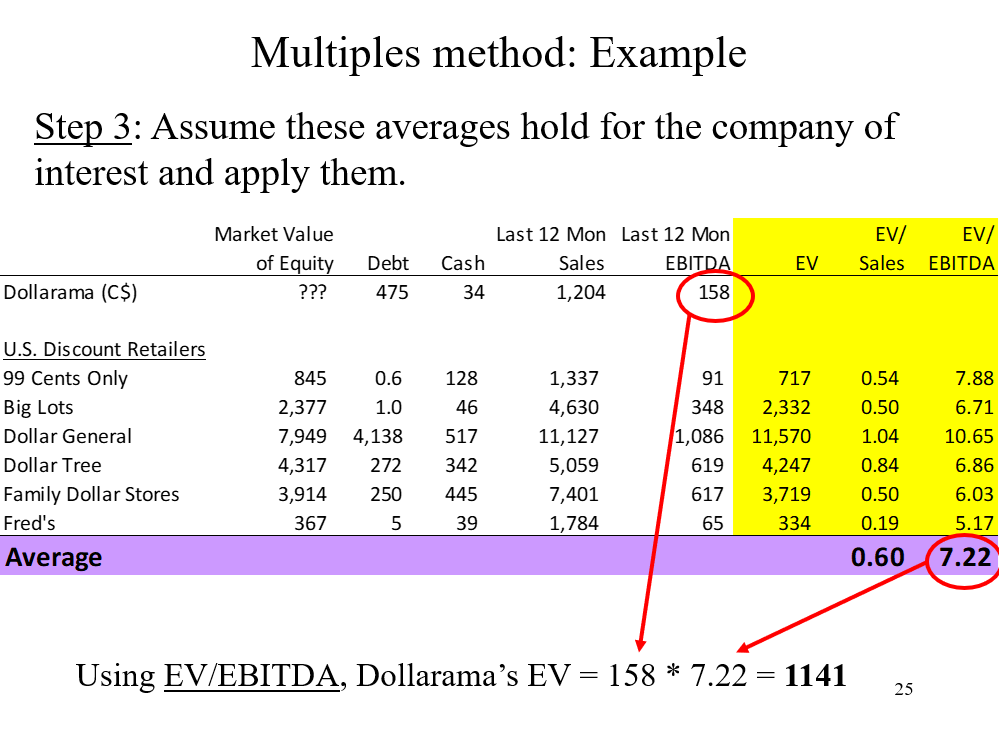

Step 3 of Multiples method

Step 3: Assume these averages hold for the company of interest and apply them.

Step 4 of the Multiples method

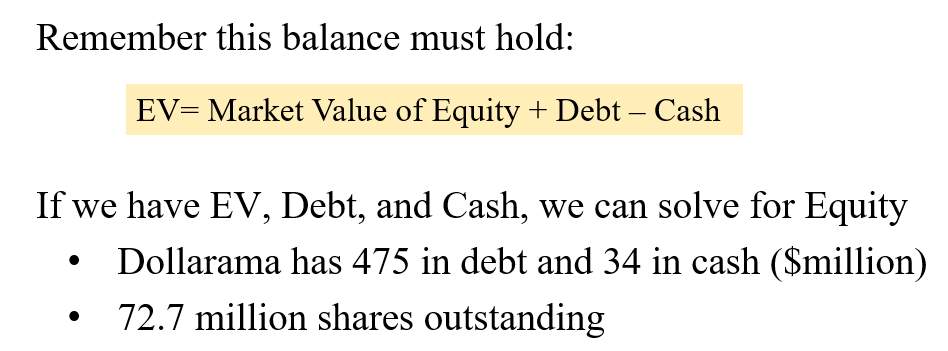

Step 4: Take the resulting EV and get the stock price.

This step is identical to the ending of the FCF method for stock.

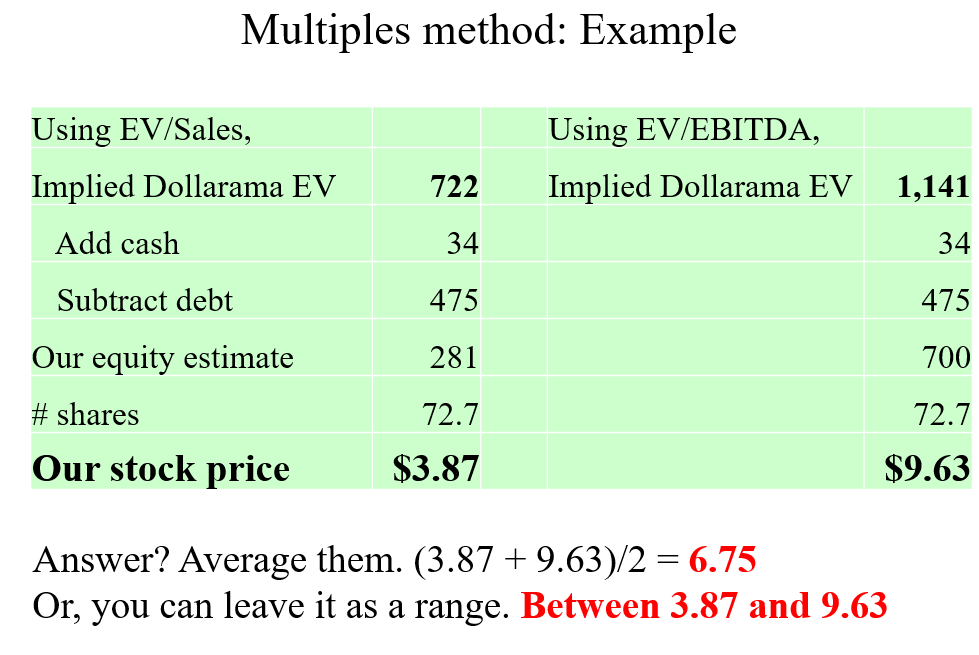

Take the average 1361 EV we just got, minus the debt, add the cash. This gives us Market Value of Equity. And then divide by # shares. Done.

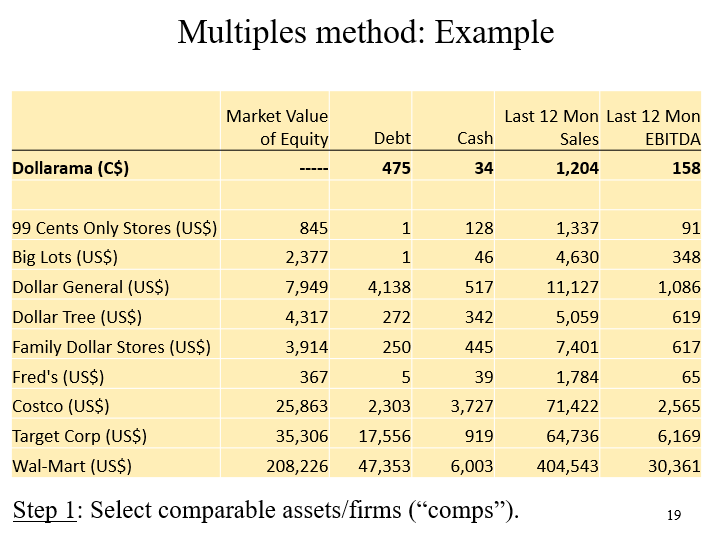

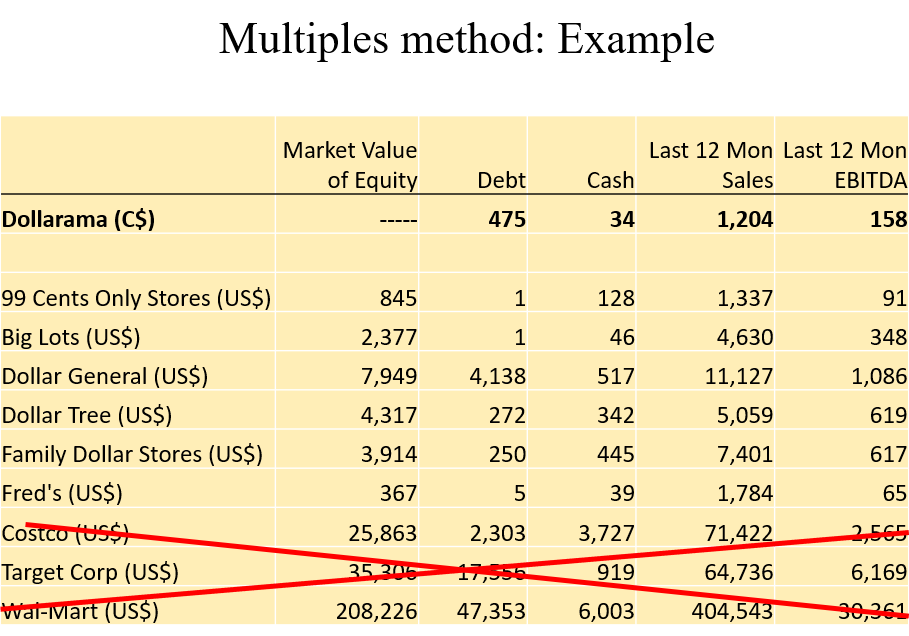

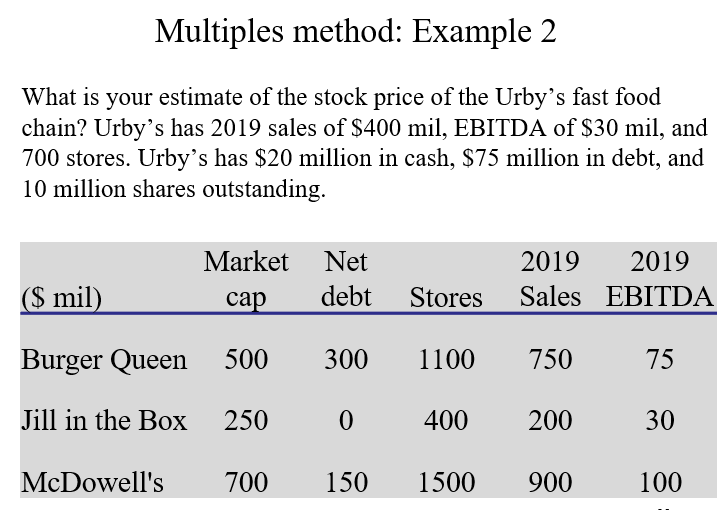

What would be step 1 using this data?

Step 1: Select comparable assets/firms (“comps”).

We will keep only the ones that seem more similar to Dollarama. Some judgement here, no single right answer.

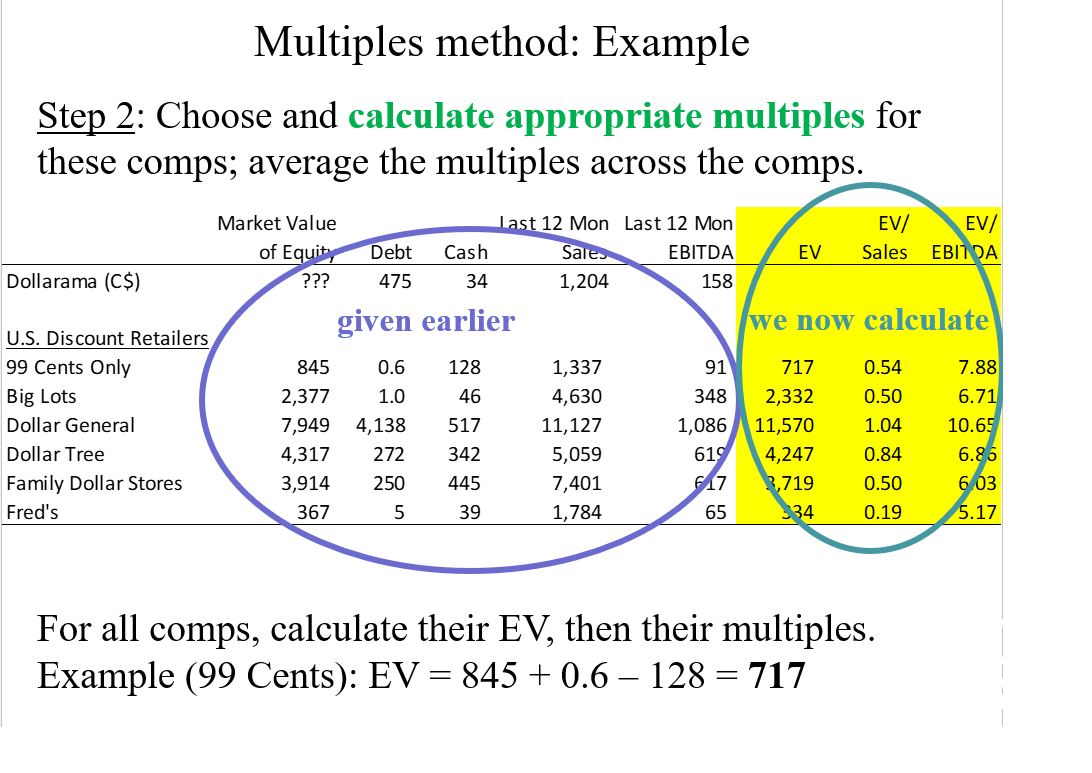

What is step 2 using this data?

Step 2: Choose and calculate appropriate multiples for these comps; average the multiples across the comps.

Let’s pick two common multiples:

EV/Sales

EV/EBITDA

What is step 3 using this data table?

Great! We’ve got two estimates for Dollarama’s EV.

What stock prices do these EVs imply?

Pros of a DCF Model

The process of doing a DCF helps you learn how the business operates (e.g. Do they have fat/thin, stable/volatile operating margins? Is the business capital intensive?)

Very amenable to sensitivity analysis, which uncovers the important value drivers.

Less affected by the current “mood of the market” i.e., panic or euphoria.

The projections can accommodate superior information.

DCF is fundamental value; PV of the cash flows received as an owner is a powerful idea.

Cons of a DCF Model

Garbage In, Garbage Out

Can be tweaked by a skilled practitioner to say just about anything. There are a lot of dials to turn, and if you turn them all in the same direction you can sway the value, even if none of the dials looks unreasonable on its own.

You’re forced to try to predict the future, which is, of course, impossible and maybe uncomfortable.

Pros of a Multiples Model

Reflects the current market, 1000s of participants. “What are people paying for comparable assets right now?”

Pretty easy (although surprisingly easy to screw up).

Don’t need to try and explicitly project the future or a WACC.

Relatively easy to explain to a non-finance person.

Cons of a Multiples Model

Garbage In, Garbage Out

Good comps can be hard to find.

Often difficult to know whether the target asset’s value should be more/less/equal to the mean of the comp set.

Can also be tweaked: pick comps that give you the answer you want.

It can’t detect when “market value” is wrong (e.g., a bubble).

What is step 1 in this process?

Step one has already been found, as there are no extreme outliers in this data table.

What is step 2 in this process?

Find the EV for all the firms, which the equation is a little different with Market Capacity instead of MVE.

EV=MC+Total Debt-cash

BQ=500+300=800

JITB=250+0=250

MDWS=700+150=850

Then find the EV/Sales

BQ=800/750=1.067

JITB=250/200=1.257

MDWS=850/900=.944

Then find the EV/EBITDA

BQ=800/75=10.67

JITB= 250/30=8.33

MDWS=850/100=8.5

Then, find the average of both.

Avev/sales=(1.067+1.257+.944)/3=1.087

Avev/Ebitda=(10.67+8.33+8.5)/3=9.167

What equals Enterprise value?

Net debt plus Equity value/MARKET CAPITALIZATION!!!

What is step 3 in this process?

Use the averages found in step 2, to find the EV’s of Urby’s

400 mil*1.087=434.8 million

30 mil*9.167=275.01 million

What is the fourth and final step in this process?

Subtract the debt from both EV’s and divide by shares to get stock price.

(275.01-55)/10=22

(434.88-55)/10=37.98