HW - Topic 4: Departmental Cost Allocation

1/5

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

6 Terms

The direct method of departmental cost allocation is the simplest of the three methods because it:

Multiple Choice

Ignores the reciprocal flows.

Correct

Uses the service flows only to service departments.

Uses a sequence of steps to allocate service department costs.

Doesn’t require any calculations.

All of these answer choices are correct.

Ignores the reciprocal flows.

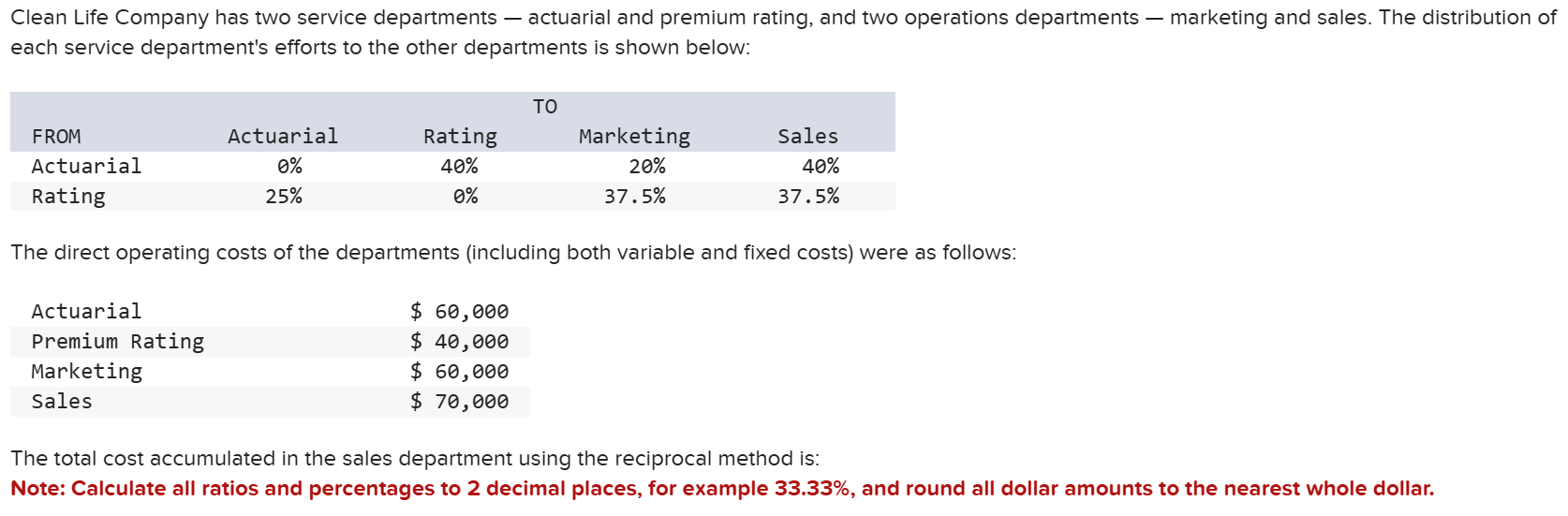

$102,222.

$122,402.

$127,778.

$142,471.

$150,050.

$127,778.

Multiple Choice

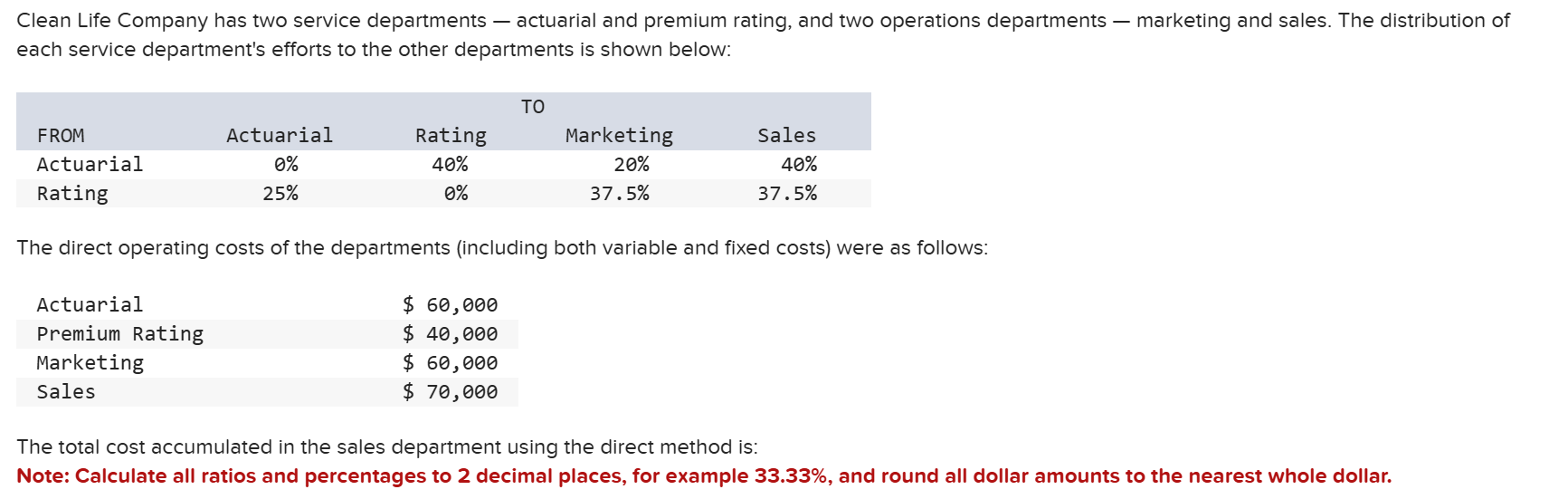

$100,000.

$109,000.

$126,000.

$130,000.

$135,000.

$130,000.

The departmental approach of cost allocation recognizes that the typical manufacturing operation involves which type(s) of departments?

Multiple Choice

Service departments and production departments.

Correct

Production departments and assembly departments.

Joint product departments and separable departments.

Cost pools and cost objects.

Support departments and other service departments.

Service departments and production departments.

The mathematical technique that underlies the reciprocal cost allocation method is:

Multiple Choice

Regression analysis.

Simultaneous equations.

Correct

Analysis of variances.

Complex algebraic functions.

Multiple correlation.

Simultaneous equations.

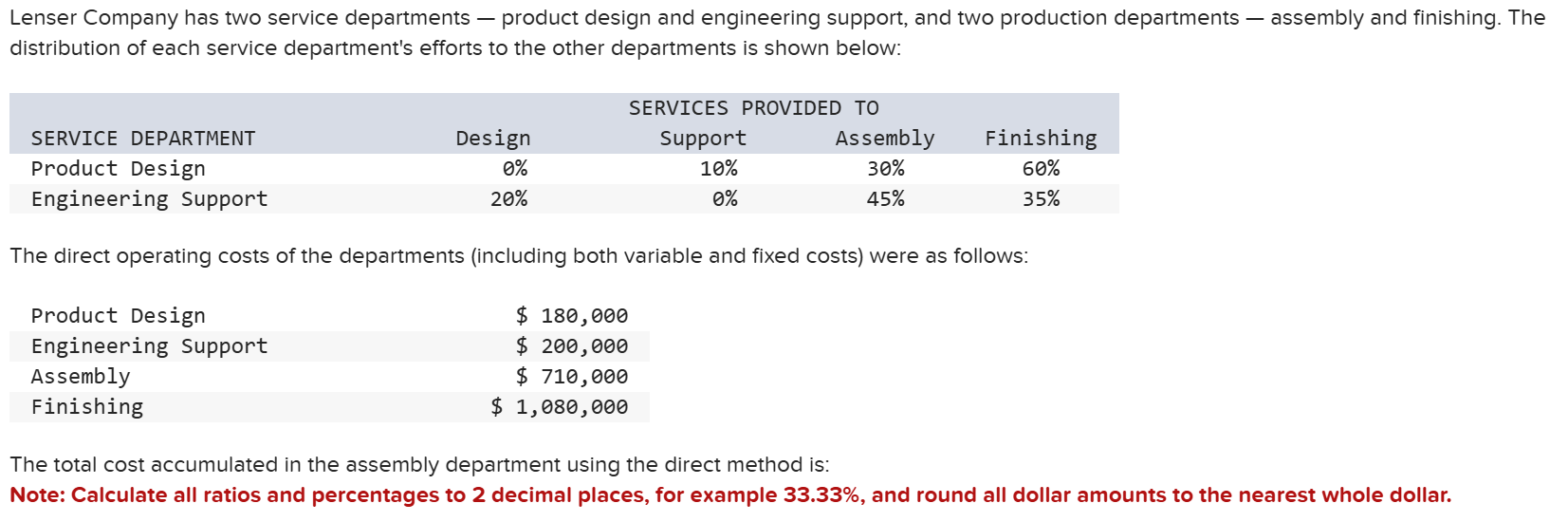

Multiple Choice

$1,287,500.

$2,170,000.

$882,500.

$842,500.

$889,166.

$882,500.