chapter 6 - chargeable gains

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

18 Terms

chargeable disposal

sale or gift of asset, eg:

sale/gifts of assets or part of assets

loss or destruction of asset (if money is received from insurance, money is disposal proceeds)

occurs on the date of the contract or when the date of a conditional contract becomes unconditional

exempt disposals

disposal w no chargeable gain or loss, includes:

transfers on death

gifts to charities

chargeable asset

all assets are chargeable (unless exempt)

exempt assets

motor vehicles for private use

UK gov stocks

qualifying corporate bonds (company loan stock)

wasting chattels (race horses)

premium bonds

investments held in an ISA

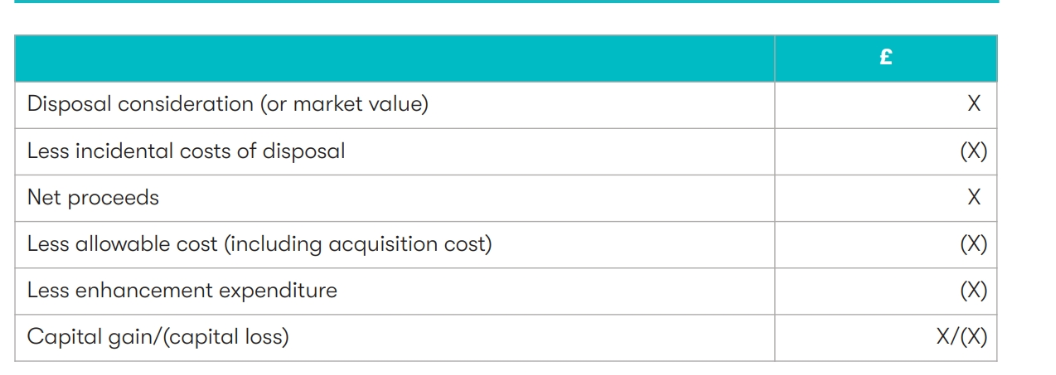

basic capital gains computation

disposal consideration is deemed to take place at market value when the disposal is:

a gift

made for consideration that cant be valued

made to a connected person (if taxpayer buys at a bad bargain, then actual proceeds is used)

costs:

incidental costs (costs of selling asset (eg advertising, estate agents, legal costs, valuation fees)

allowable costs: original purchase price of asset & costs incurred of purchasing asset

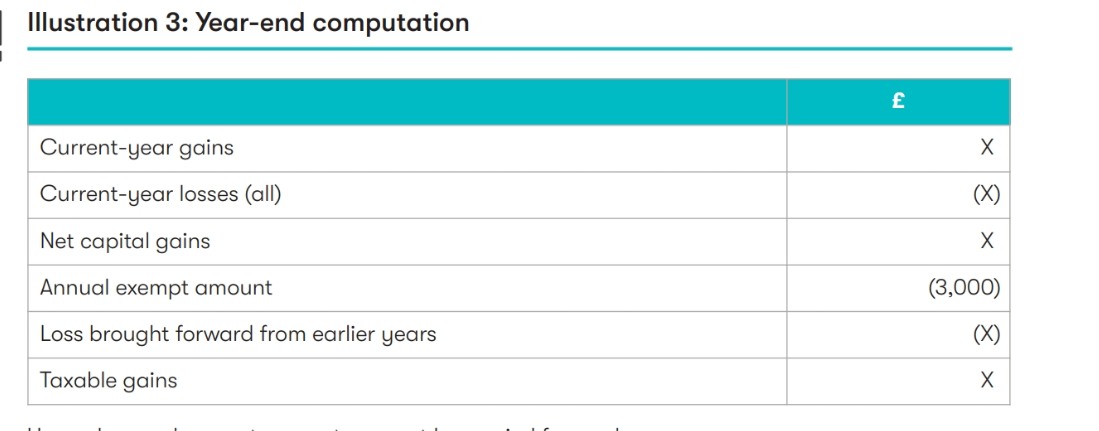

year end computation

annual exempt amount

amount of capital gains a taxpayer may realise in a tax year before capital gains tax is deducted

3,000

losses

offset against current year gains

excess is carried forward and deducted AFTER future year annual exempt amount has been deducted

when is CGT payable

31 January

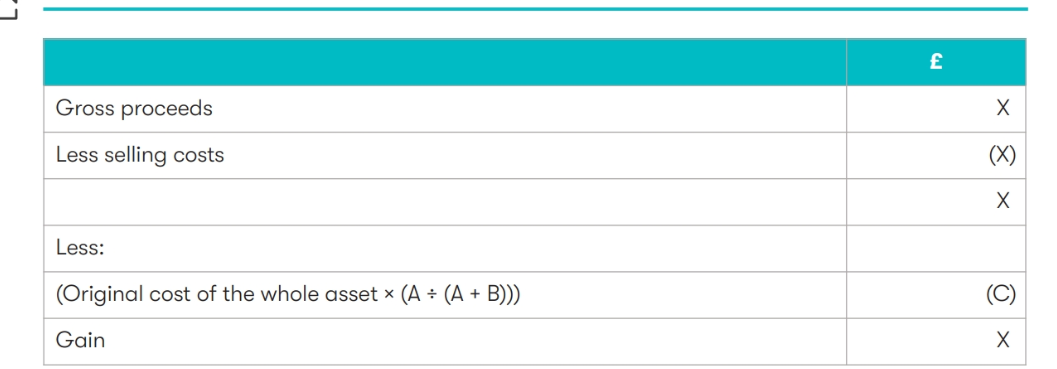

part disposal

must determine the cost of the part of the asset that was disposed by:

COST * (A/ A+B)

A - market value (of part that was sold) before deducting incidental costs of disposal (basically disposal proceeds)

B - market value of part of asset that wasnt sold

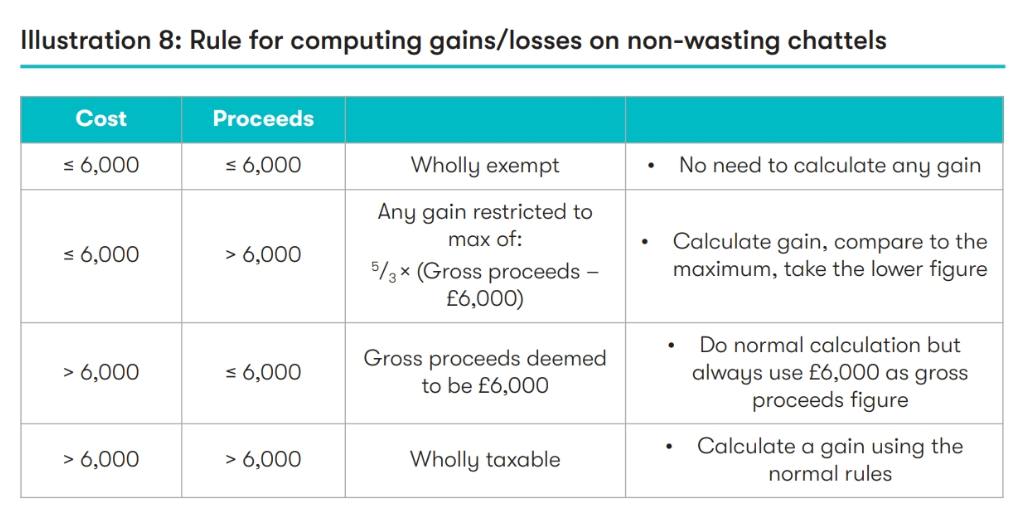

chattel

tangible moveable property

wasting chattel

chattel with an estimated remaining useful life of <50 years (eg race horse or greyhound)

exempt from CGT

rule for computing gains/ losses on non-wasting chattels

transfers to connected persons

if disposal is made to a connected person, the disposal is deemed at market value

allowable losses can only be offset against gains in current or future tax years from disposals to the SAME connected persons

and can only be set off if its still connected to the same person making the loss

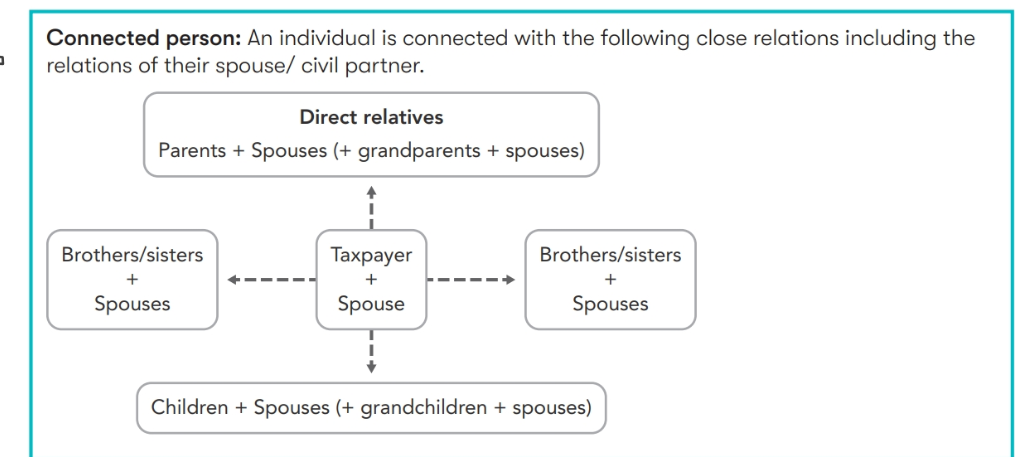

who are the connected persons

transfers between spouses / civil partners

taxed as two separate people.

losses of one individual cannot be offset against the others gains

disposals cannot have chargeable gains or allowable losses

the person who acquired the disposal (during transfer) takes the original cost at which the other individual bought it for

tax planning

consider:

delaying sale of an asset after end of tax year (gives you next years annual exempt amount + another yr to pay tax)

spouses may transfer assets at no gain no loss, so make sure the asset is sold by the partner who: pays tax at a lower rate, unused annual exemption and has capital losses