Week 3 comm1100

1/92

Earn XP

Description and Tags

model

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

93 Terms

Managers make decisions about..

what prices to set

who to buy from

who to employ

how to operate

Elements of all decisions (aooc)

agency - ability to make independent choices

options - different alternatives

outcomes - expected result of each option

context - circumstances and constraints affecting the decision

How is business decision-making different to individual decision-making?

Business decisions affect a larger number of stakeholders, such as employees, customers, and shareholders, whereas individual decisions usually affect fewer people.

Who are stakeholders? What is a ‘stake’?

those who can affect or be affected by an organisation’s decisions, policies, or practices

A stake = claim on, or investment in, an organisation, which brings exposure to riskmay be past, present or future (future generation environmental impacts, inheritors) oriented

Who are the shareholders/owners of the firm?

large investors like superannuation funds/banks - need increasing share prices to report profits for their own investors - looking for long-term growth

day traders/ short-term share traders = short-term increases

small shareholders - like you?

founders - more emotional connection, long-term prosperity to hand company over to future generations

employees - long-term growth, job security

executives - short-term highest share price to exercise their options

therefore, some may want long vs short-term share price growth

Core stakeholders? (7)

shareholders/owners

employees

customers

suppliers

local communities (grant social licence to operate - build facilities, use public resources like infrastructure, roads, educated workforce, etc.)

societies

regulators/governments

Why are governments important stakeholders?

develop laws

can apply sanctions

raise taxes

Business decision-making questions

who are the core stakeholders in this situation?

what are their rights?

what are their interests?

What do they value?

their motivations?

who is harmed/benefited by this decision?

eg: customers value products/services that improve their lives, suppliers value fairness + transparency, employees - fair wages, meaningful work, job security

What are the 4 sources of expertise ?

the economist, the lawyer, the CR expert, and the management consultant

The economist

They help managers understand

markets

give context

- how various stakeholders enable/ constrain business activity (buying, selling, producing products/services), which helps managers understand how much agency they have in the decision-making process and what are the important options

- how business activity impacts other stakeholders, which helps inform normative (moral) decision making

The lawyer

Managers don’t need to be lawyers; they only need to know when legal advice from lawyer is needed

types of laws: competition law, human rights law, contract law, intellectual property law, consumer protection law, employment law, tax law, etc

limitation: A decision may be legal but still unethical

Corporate Responsibility expert

Ensuring business decisions respect the rights of stakeholders and consider ethical and environmental responsibilities.

Management Consultant

Integrates different perspectives to solve complex business problems.

Cost-Benefit Principle

Choose an action only if its benefits are greater than/equal to its costs

If MB ≥ MC

Scarcity

Limited resources

Economic Surplus? With trade, both buyer/seller…

Economic Surplus = Benefits - Costs

your gain after making a decision

With trade, both buyer/seller gain economic surplus

Opportunity Cost

The next best alternative that must be given up when making a choice.

Sunk Cost

A cost that has already been incurred and cannot be recovered (don’t consider when making decision)

Why Is a Business in Business?

Benefits > Opportunity Costs

Why is understanding the law important for business decision-making?

determines what businesses can, cannot, and must do. (constrain/enable)

Influences managers' available options

breaking law can result in penalties/legal consequences

4 Core Legal Concepts that impact business decision making (COAL)

Control (law controls business activity, even playing field for ethical and non-ethical businesses (so businesses can’t take advantage of another business))

Liability (Legal responsibility for harm, losses, or obligations)

torts law (breaching individual rights), company law (companies are seperate legal entities), consumer law

Ownership

Agreement

Why does liability matter

Managers must consider:

Potential legal claims

Financial costs

Risks of business activities

Liability creates costs that must be included in decision-making.

Ownership

Ownership gives legal rights over property.

Property includes:

Physical Property

Buildings

Equipment

Land

Intangible Property

Intellectual Property (IP)

Shares

Agreement

business agreement = contract

agreement = mutual understanding

contract = legally enforceable agreement

Corporate Responsibility

focuses on how business decisions help/harm all stakeholders

different stakeholders value different things

company’s commitment to operating as a responsible and sustainable business

Types of Stakeholders

Organisational Stakeholders (people directly invovled)

Managers

Employees

Investors/shareholders

Market Stakeholders (involved in the exchange of goods and services)

Customers

Suppliers

Competitors

Societal Stakeholders (broader business impacts)

Government and regulators

Communities

Environment (eg: wildlife) + environment groups (gov/non-gov)

Future generations

Normative vs instrumental approach

Normative → What is the ethical/moral thing to do? - human rights, justice and fairness

Instrumental considerations → What helps achieve business goals? - financial performance, profit, competitive advantage, regulatory compliance

Good business decisions often require both. Just normative - not practical, just instrumental - neglect ethical principles

4 dimensions of an organisation’s impact (SEEP)

Economic (eg: creating jobs, increasing local income)

Social (employee wellbeing, diversity and includsion)

Political (lobbying govs, influencing regulations)

Environmental (carbon emissions, waste)

Ripple Effect and Managerial Agency

Managers have agency over many of the positive and negative impacts their organisations create.

Managers can:

Increase positive impacts

Reduce negative impacts

Change how business activities are conducted

According to Edward Freeman’s Stakeholder Theory…

Any individual or group affected by the organisation’s decisions

Models

simplified representation of reality.

Regulation

Rule created to enforce law

Shareholder vs Stakeholder centric business view

Shareholder view: managers work on behalf of shareholders

Stakeholder: managers have to consider rights and interests of stakeholders

Why corporate responsibility?

Consumers want to spend their money on products and services that they believe in and that follow ethical practices that meet their own beliefs

James has a ticket for a football match in Sydney for which he paid $45. On the day of the game he takes the train to Sydney Olympic Park, which costs him $3. When he arrives, he realises that the game is taking place in Moore Park instead. He can take a taxi for $50 and arrive just in time for the match. Otherwise, he will miss it. Suppose James values watching the match at $70. Should he take the taxi or go home?

match ticket ($45) and the train ticket cost ($3) are a sunk cost

The marginal benefit of going to the football match (value to James of seeing the match = $70) is greater than the marginal cost of going to the match (the cab fare = $50).

net benefit here is $20

If James, goes home, his marginal benefit is 0,

Therefore, James should take the taxi to the football match.

By thinking at the margin (and especially ignoring his sunk cost), this is the best decision: A net benefit of 20 is better than a net benefit of 0.

Economic models contain:

characters, motivations, a setting and a plot.

Agents

Preferences

Constraints → limits (time, money, resources)

Environments

choices/interactions (The choices agents make given their: Preferences & Constraints)

These are the model's assumptions.

Economic model benefits

Economic models help predict:

How people behave

How businesses behave

How markets operate

Pitfalls/limitations of using a model

Pitfall: ❌ Using a model without checking its assumptions.

Example:

Following a GPS/map without considering road closures, traffic, or terrain.

Limitations

Ignore many real-world factors.

Can lead to poor decisions if assumptions don't match reality

How to use economic models properly

Understand the assumptions.

Check whether they fit the situation

Consider important factors the model leaves out.

Why do markets exist? What economic principles explain why markets exist?

Because people and businesses benefit from specialising and trading rather than producing everything themselves. The cost-benefit principle and the opportunity cost principle.

Why don't people produce everything they need themselves?

Because specialising and trading often allows goods and services to be produced at a lower opportunity cost.

What is absolute advantage?

The ability to perform an activity using fewer resources than someone else.

an agent can produce a good using fewer resources than another agent, or they can produce more goods for the same resources

Does having an absolute advantage determine who should specialise?

No. Comparative advantage determines specialisation.

What is comparative advantage? What determines comparative advantage?

The ability to perform an activity at a lower opportunity cost than someone else. Opportunity cost.

an agent has a comparative advantage when they can perform a task at a lower opportunity cost relative to another agent.

What is the key difference between absolute and comparative advantage?

Absolute advantage compares resources used; comparative advantage compares opportunity costs.

Which advantage explains why trade and specialisation occur?

Comparative advantage.

What is opportunity cost? Why is opportunity cost important when deciding what to produce?

The next best alternative forgone. Because resources should be allocated to activities with the lowest opportunity cost.

Following the core principles that we have introduced, a business should produce something if … (2)

The benefits to the business outweigh the costs, and

The manager recognises that the costs include all opportunity costs (and no sunk costs), not just the money spent to produce and sell the good.

What is demand?

The willingness and ability of consumers to purchase goods and services.

What is the supply and demand model?

A simple economic model used to explain how markets determine prices and quantities.

What is the cost-benefit principle?

Choose an action if its benefits are greater than or equal to its costs.

What is the marginal principle? (Marginal Benefit?, Marginal Cost?, consumer decision rule?)

Quantity decisions should be made incrementally (one extra unit at a time).

Compare:

Marginal Benefit (MB) = extra benefit from one more unit

Marginal Cost (MC) = extra cost from one more unit

Consumer Decision Rule:

Do more if MB > MC

Stop when MB = MC

Example

Studying one more hour:

MB: Better understanding, higher grades

MC: Lost leisure time, fatigue

Keep studying until the extra benefit equals the extra cost.

Why is the marginal principle useful?

It turns "how many?" decisions into a series of simpler "either/or" decisions.

Assumptions of the Consumer Demand Model

Consumers are price takers

Cannot influence market prices.

Must accept the market price.

Consumers follow economic principles

Cost-benefit principle

Opportunity cost principle

Marginal principle

Reservation price

maximum amount a buyer is willing to pay

minimum a seller is willing to accept

informed by opportunity costs

E.g., spending $4 on a coffee means foregoing $4 worth of the next best thing you could have bought

How is market demand calculated?

By adding together individual consumers' demands.

What does a demand curve show?

The relationship between price and quantity demanded.

6 factors that shift the market demand curve?

Income

Preferences

Prices of related goods

Expectations

Congestion and network effects (choices made by others, congestion - too many ppl)

The type and number of buyers

(but not a change in price. (This is a movement along the demand curve.)

Mnemonic: "I Prefer Pizza Every Cold Tuesday"

I = Income

Prefer = Preferences

Pizza = Prices of related goods

Every = Expectations

Cold = Congestion & network effects

Tuesday = Type & number of buyers

What causes a movement along the demand curve?

change in price

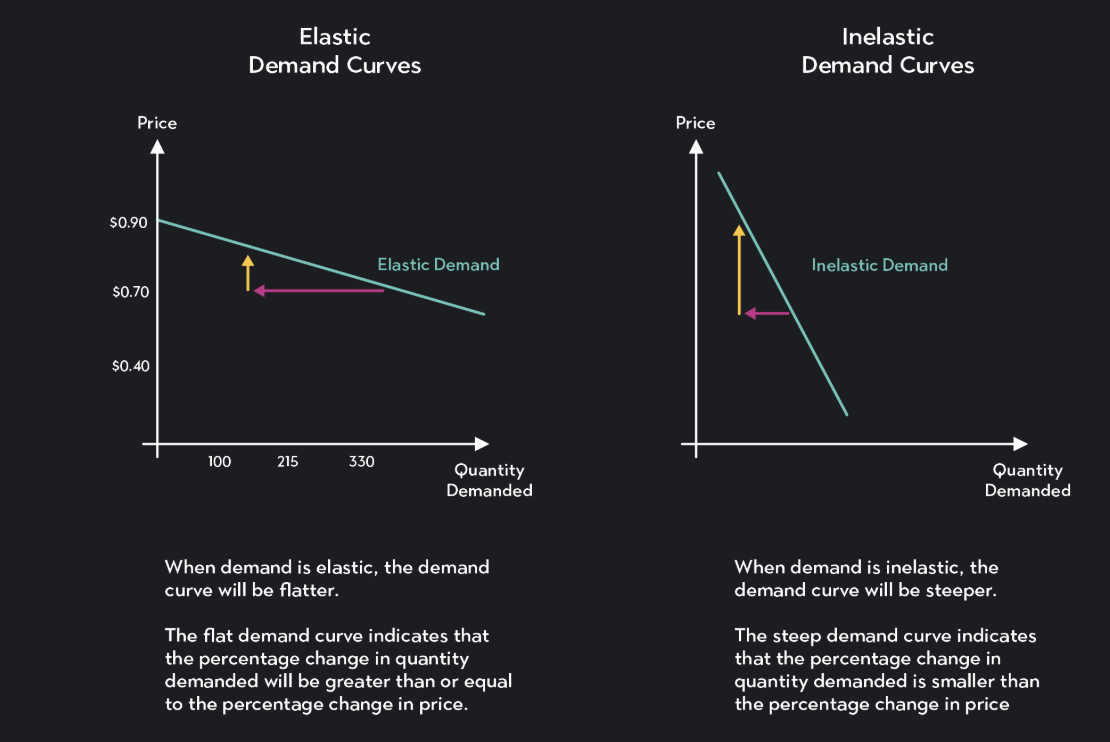

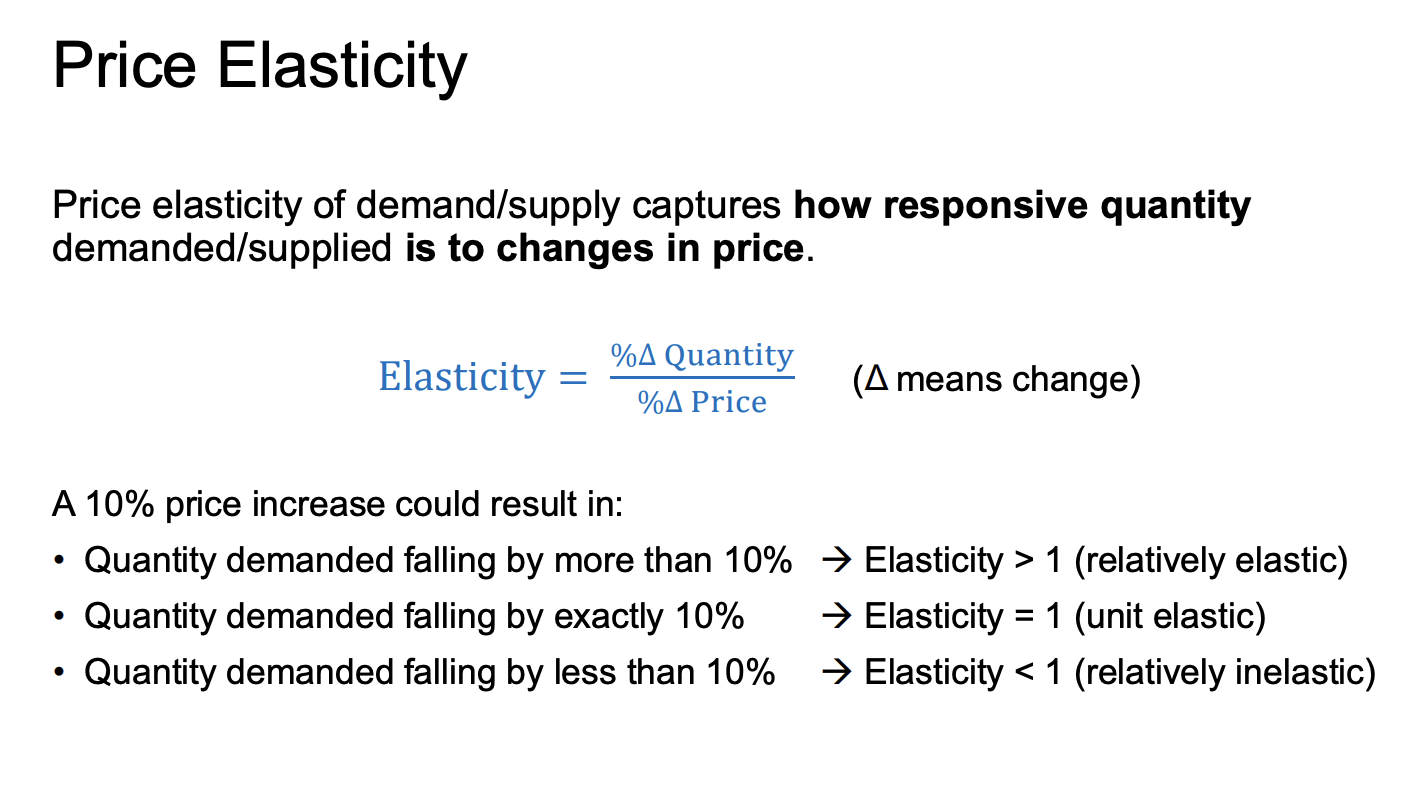

What is price elasticity of demand (PED)?

A measure of how responsive quantity demanded is to a change in price.

If a small price increase causes a large drop in quantity demanded, demand is?

Elastic. (flat demand curve)

Example of an elastic good? Example of an inelastic good?

Luxury goods or products with many substitutes.

Necessities such as basic medicines.

If a large price increase causes only a small drop in quantity demanded, demand is?

Inelastic (steep demand curve)

law of demand / supply

demand

as the price of a good or service increases, consumer demand for that quantity falls. Conversely, as the price decreases, the quantity demanded rises

supply

an increase in the price of a good or service leads to an increase in the quantity supplied by producers

What causes the price elasticity of demand to increase? (5)

availability of substitutes

more competing products

Happens for specific brands rather than broad categories (can easily switch apple brand)

For things that are not necessities

When it is easier for consumers search for better prices or alternatives

When there’s more time to adjust

When is it perfect competition?

Firms sell homogeneous (identical) goods.

Firms are price takers.

What does it mean for firms to be price takers?

Firms must accept the market price.

Charging a higher price causes customers to buy from competitors.

Firms have no market power (cannot raise prices without losing sales)

Why are firms in perfectly competitive markets price takers (no influence over price)?

Because they are small relative to the market and sell identical products.

What is market power?

The ability to raise prices without losing all customers.

Why don't competitive firms have market power?

Because customers can easily switch to identical products sold by competitors.

What is the only decision a competitive firm can make (if not the price)?

how much to produce. They do this using marginal principle, produce another unit as long as the marginal benefit is greater than the marginal cost

diminishing marginal product

as more units of a single input are added to production, the additional output or benefit gained from each additional unit will eventually decrease

Market supply

Sum of total supply of all individual firms in the market

What happens when price increases/decreases in supply curve?

Quantity supplied increases/decreases

What causes a shift in the supply curve?

A change in a factor other than the product's own price.

(production costs, technology, market size, government policies, natural disaster)

What causes a movement along the supply curve?

A change in the product's own price

What is price elasticity of supply?

A measure of how responsive the quantity supplied is to a change in price.

What is short vs long run analysis for supply curve?

short - where firms decide how much to produce (but cannot easily enter/exit), assuming the number of firms in the market is fixed.

long - Free entry and exit of firms.

Firms can enter profitable markets and leave unprofitable ones.

Why are entry and exit decisions considered long-run decisions?

Because they often require significant planning and investment.

Variable vs Fixed costs?

Variable Costs that change when output changes.

Examples: labour, raw materials.

they matter in short-run because they affect marginal cost

Fixed

Costs that do not change with the quantity produced.

Examples: rent, managers' salaries, insurance

don’t affect marginal cost

Average costs

When would an incumbent firm want to leave the market?

When its total revenue doesn’t cover all of its costs, including opportunity costs

When would a firm want to enter a market?

When expected revenues exceed total cost of production and opportunity costs

the five factors shift the market supply curve are

Input prices

Productivity and technology

Prices of related outputs

Expectations

The type and number of sellers

. . . but not a change in price. (This is a movement along the supply curve.)

IPPETS

(pronounced: "I-pets")

I = Input prices

P = Productivity & technology

P = Prices of related outputs

E = Expectations

T = Type & number of sellers

Second, the price elasticity of supply reflects the flexibility of firms to increase or decrease the quantity supplied. It is larger… when … for firms…

For firms that store inventories

(They can immediately release stock when prices rise.Example:

Apple has 10,000 iPhones in a warehouse.

Price rises.

They can instantly supply more.

➡ More responsive → More elastic._

When inputs are easily available

For firms with extra capacity

When firms can easily enter and exit the market

When there’s more time to adjust

In the long run, firms will enter the market if… firms will exit the market if..

Firms will enter the market if the market is price is greater than their average cost.

Firms will exit the market if the market price is less than their average cost.

What is market equilibrium?

The point where quantity demanded equals quantity supplied.

What is a surplus?

A situation where quantity supplied exceeds quantity demanded.

What does it mean prices are determined at the margin?

the price of a good or service is dictated by the value of the last unit produced or consumed, not its total value.

Prices ultimately settle at the point where the marginal benefit to the buyer equals the marginal cost of the producer.

Hiring: A business will hire workers as long as the revenue generated by the last worker hired (marginal revenue product) is greater than or equal to the wage paid.

Why do we trade

agents can have an absolute advantage in both activities, they cannot have the comparative advantage in both activities.

Agents can specialise in the activities in which they have a comparative advantage and engage in mutually beneficial trades to meet their consumption goals.

Trade expands consumption bundles beyond what is possible through self sufficiency

Trade allows people and businesses to specialise according to their comparative advantage, increasing total production and enabling everyone to consume more than they could on their own.

How to know if something is elastic or not?

Price elasticity of demand depends on…

depends on how easy it is to find an alternative (substitute) to the good whose price just went up.

Time horizon - Do you need the thing tomorrow or can you shop around?

Short run:You still need to drive to work.

Demand barely changes.

Demand is inelastic.

Long run:

You buy a more fuel-efficient car.

Move closer to work.

Use public transport.

Demand becomes more elastic.

Rule

More time → More elastic demand

Availability of substitutes - Are there things that are just as good that you can buy instead?

Definition of good (how narrowly/broadly is product is defined)- Did the price rise affect only something specific or a broad category? (Specific products → More elastic, Broad categories → More inelastic)

Income share - How much do you care about/notice this price increase?

Easy Memory Table

Factor | More Elastic When... |

|---|---|

Time Horizon | More time to adjust |

Substitutes | Many alternatives exist |

Definition of Good | Product is narrowly defined |

Income Share | Product takes a large share of income |

Quick Memory Aid: TADI

T = Time horizon

A = Availability of substitutes

D = Definition of good

I = Income share

Price elasticity of supply depends on…

depends on how easy it is to make/sell more of the good when the price goes up.

• Time horizon - Is the price rise sudden or did you anticipate it well?

More time → More elastic supply (more time to supply and cater to demand)

• Availability of raw materials - Do you have a bunch of raw materials lying around, or do you need to source more before you can increase production?

Inputs easy to obtain → More elastic supply

Inventories - Do you already have a bunch of finished goods lying around that you can sell, or do you need to make more first?

More inventory → More elastic supply

• Excess capacity - Are you using your inputs to the max already, or can you use them more rather than needing to source more?

More spare capacity → More elastic supply

Easy Memory Aid: TIRE

T = Time horizon

I = Inventories

R = Raw materials

E = Excess capacity

The more TIRE a firm has, the more elastic supply becomes.