Multiple linear Regression

1/63

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

64 Terms

The Regression process

Check if dependant variable is continuous

Estimate the model

Analyse residuals

Check is the assumptions are verified

examine the goodness of fit model

Is the overall fit significant

Is the model the best

5 assumptions of multiple linear regression

Linearity

homoskedacity

Independance of errors

Normality of residuals

No collinearity

Scatterplot matrix

Helps to better understand the model

Scatter plot of residual against dependant variable

detect outliers

Scatter plot of residual against dependant variable

confirm outliers and look for broken assumptions

normal q-q plot

Compare the distribution of the residuals to a normal distribution

Partial regression coefficient

Coefficient that describes the effect of a one-unit change in the independent variable on the dependent variable, holding all other independent variables constant.

If a regression model is estimated using all five independent variables

any prediction of the dependent variable must also include all five variables

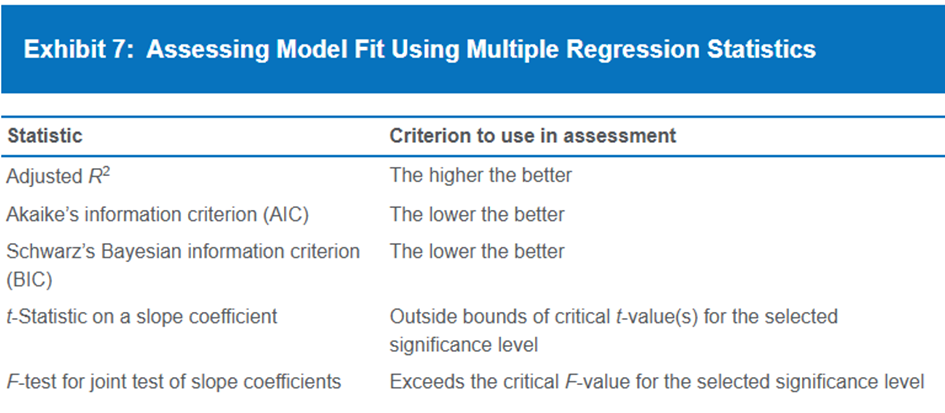

R²

Sum of square regression / Sum of square total

Evolution of R² When you add variables

R² can not decrease

Problems with R²

R² Do not say wether coefficient are statistically significant

R² do not say anything about biases

R² do not say if the model is a good fit

Overfitting

model is too complex, meaning there may be too many independent variables relative to the number of observations in the sample

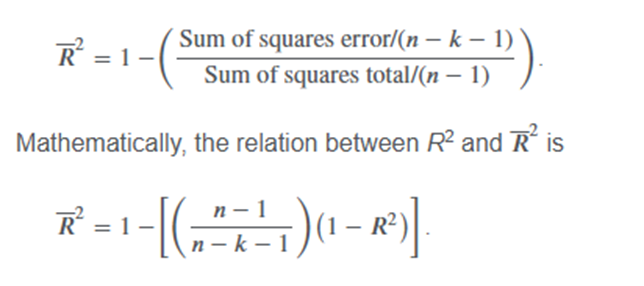

Adjusted R²

What does it mean if adjusted R² increase or decrease

new coefficient t stat is superior / inferior to 1

Who is bigger R² or adjusted R²

R²

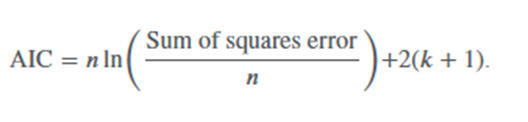

AIC

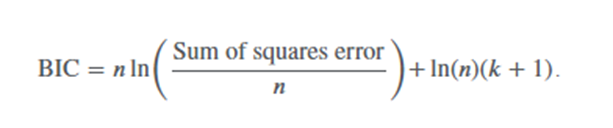

BIC

BIC impose a greater penalty on more complex model

When do you use AIC or BIC

AIC is for prediction

BIC is for testing fit

Nested model

Models in which one regression model has a subset of the independent variables of another regression model.

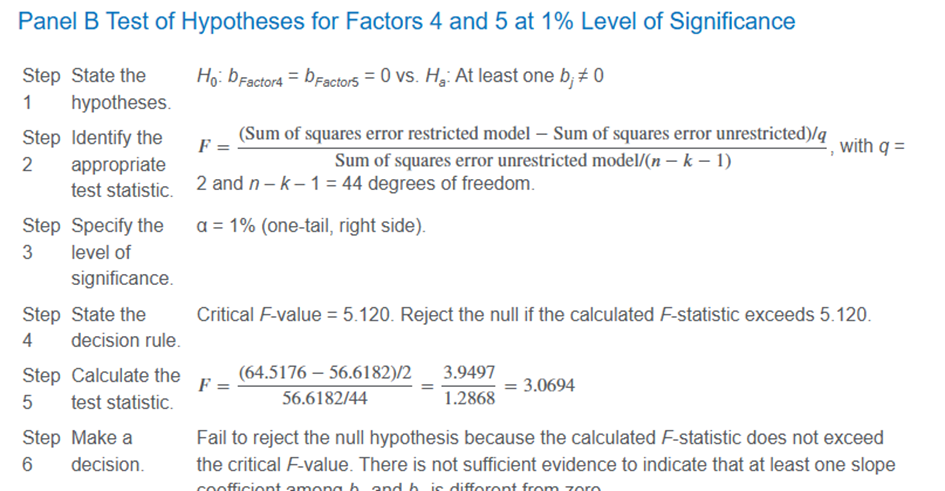

F stat for restricted model

Summary Model Fit

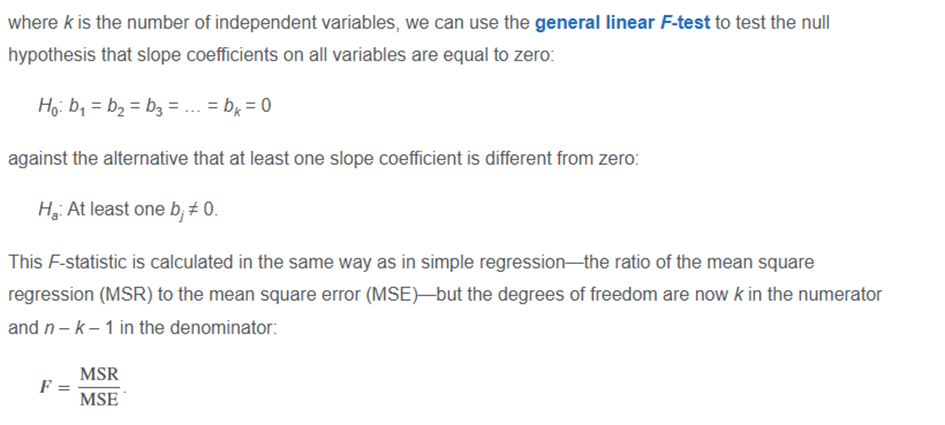

general linear F test

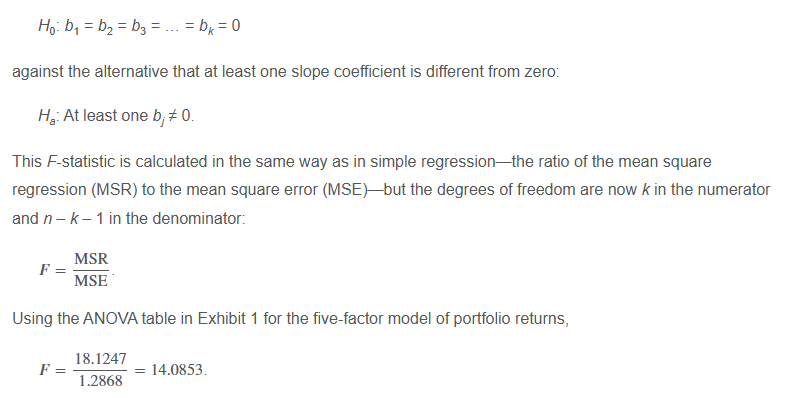

R2 and adjusted R2 are not generally suitable for testing the significance of the model’s fit; for this, we explore the ANOVA further, calculating the F-statistic and other goodness-of-fit metrics.

ok

Principles of model specification

Grounded in economic reasoning

Parsimonious

Perform on other samples

Model should adapt to non linearity

Model should satisfy regression assumptions

Failures in regressions

Omitted variables

Innapropriate form of variables

Inaproprate variable scaling

Innapropriate data pooling

Heteroskedacity

Variance of residuals differs across observation

Interpretation of Breusch Pagan test

the null hypothesis is that there is not heteroskedacity. This is a one tail risght side test.

What model should you use if there is heteroskedacity

Robust standards errors

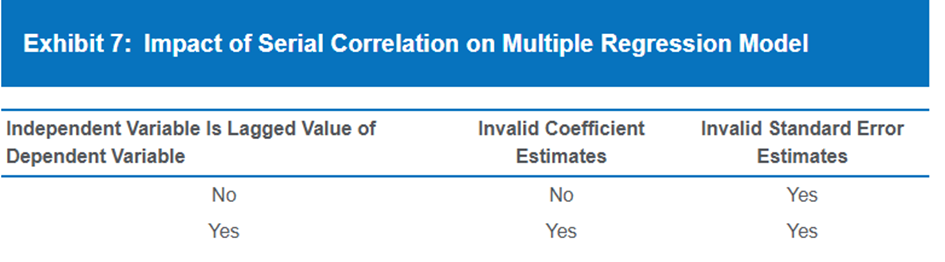

Serial Correlation

Often found in time series. Residual are correlated

Impact of Serial Correlation on Multiple regression model

First order serial correlation

The correlation is about the adjacent residuals

VIF interpretation

VIF > 5 so investigate

VIF > 10 serious multicolinearity

How you correct multicollinearity

Exclude variables

Using a different proxy

Increasing the sample size

high leverage point

An observation of an independent variable that has an extreme value and is potentially influential.

An outlier

An observation that has an extreme value of the dependent variable and is potentially influential.

How to identify ouliers and high leverage points

Scatterplot

Leverage

A value between 0 & 1 to identify how far is the high leverage point (1 being the highest)

How to detect high leverage point

Higher than 3 x (K+1/N)

Method to identify outliers

Studentised residuals

degree of freedom for studentised residuals

n-k-2

Conclusion of studentised resiudals

if studentised residuals are higher than Critical value then it is an outlier

Number of dummy variable for N categories

N-1

Qualitative dependant Variables

logistic regression

The log of the probability of an occurrence of an event or characteristic divided by the probability of the event or characteristic not occurring.

Model used to estimate coefficient in logisitic regression

Maximum likelyhood ratio

error distribution for logistic regression

the distribution’s shape is similar to the normal distribution but with fatter tails.

how to assess logistic model fit

Likelyhood ratio test

LR = −2 × (Log-likelihood restricted model − Log-likelihood unrestricted model)

Interpratting log likelyhood test

log-likelihood metric is always negative, so higher values (closer to 0) indicate a better-fitting model.

General linear F test