1.1 Nature of economics

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

Utility

The usefulness/enjoyment a consumer can get from a good/service.

Assumptions

Generalisations about behaviour, choices, and likely outcomes based on observations in the real world.

Ceteris paribus

The assumption that other things are being held equal or constant, so nothing else changes.

Inability to make scientific experiments

Scientific experiments involve controlled conditions + manipulation of variables.

However, economics observes human behaviour influenced by numerous variables, making experiments uncontrollable.

so models are devised by using real life scenarios + making assumptions.

Demand theory: Observe human behaviour→form hypothesis of how consumers spend→make predictions from hypothesis→use evidence to test predictions.

Scarcity

Resources are in limited supply.

The economic problem

How to allocate scarce resources (FoP) given unlimited wants.

This forces choices to be made:

WHAT to produce, HOW to produce, FOR WHOM to produce for.

Renewable resource

Resources, such as fish stocks or forests, which can be exploited over and over again bc they have the potential to renew themselves. e.g hydropower, wind, biomass

Non-renewable resource

Resources such as coal or oil, which once exploited, can't be replaced. e.g. coal, petroleum, natural gas, uranium(nuclear)

Sustainable resource

Renewable resource which is being economically exploited in such a way that it will not diminish or run out.

Opportunity cost

The cost of the next best alternative foregone (given up) when a choice is made.

How is opportunity cost important to economic agents(producers, consumers, government)?

The government might have to choose between spending more on the NHS and spending more on education.

Positive statement

Factual statements/theories that can be proved true or false through evidence.

inflation has increased by 11% in the last 12 months

the quantity of meat produced has increased since 1990.

Normative statement

Statements that involves judgement and opinion.

the government should increase the minimum wage

the unemployment rate should decrease

What do the factors of production describe?

What are they?

What are the rewards?

The resources/ inputs used in the production of goods or services to make an economic profit.

1. Land: The natural resources, such as water, forests, oil, used in the production of a product.

-the incentive is rent

2. Labour: The effort and skills of people who work to produce goods + services.

-the incentive is wages

3. Capital: Man made factories, machinery + other physical assets used to produce goods/services.

-the incentive is interest (through borrowing capital)

4. Enterprise: Risk takers who innovate + produce goods + services to make a profit

-the incentive is profit

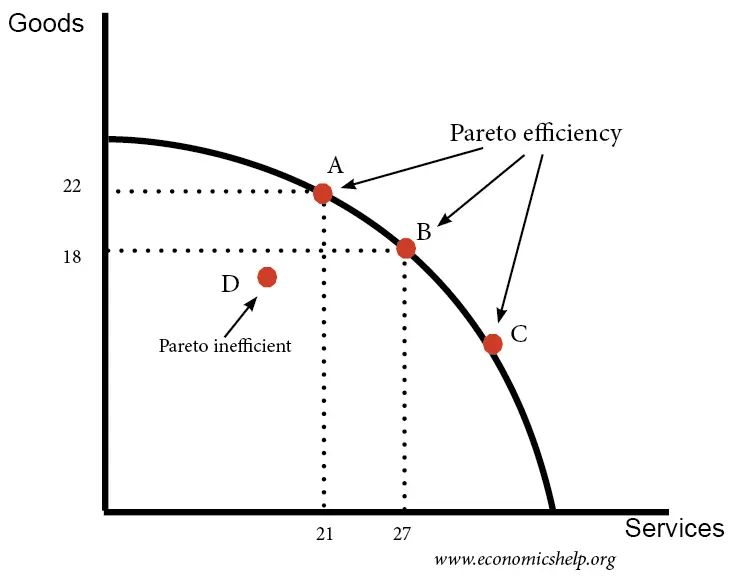

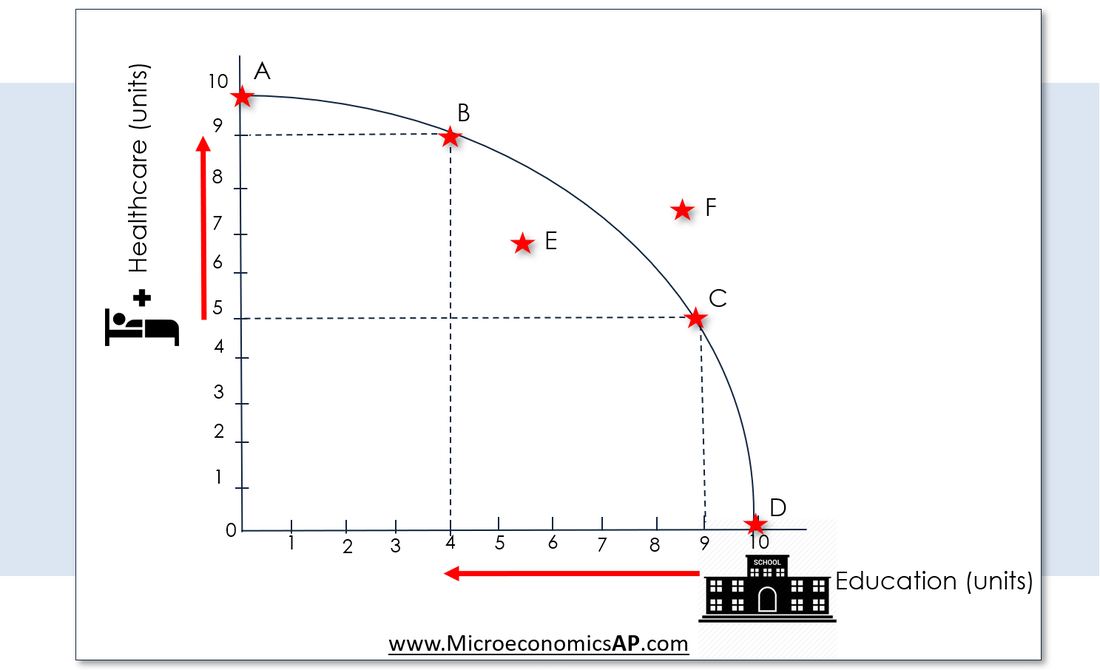

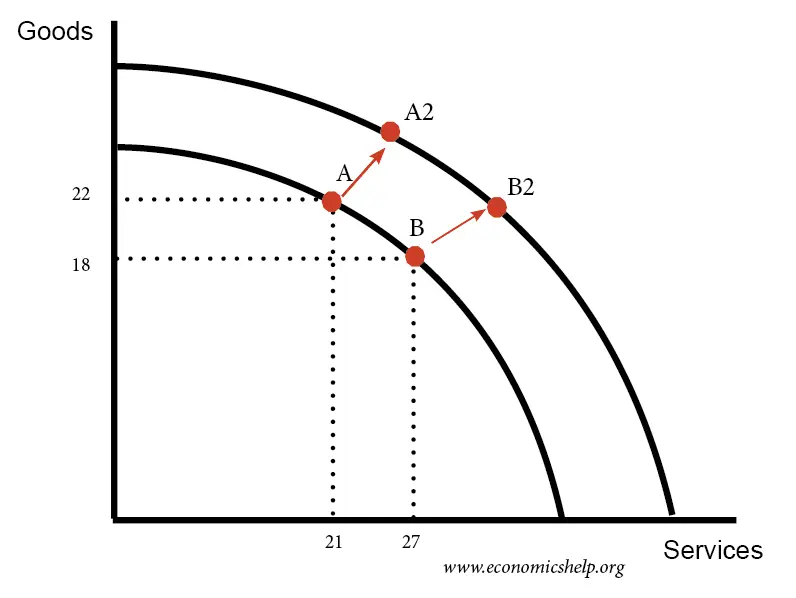

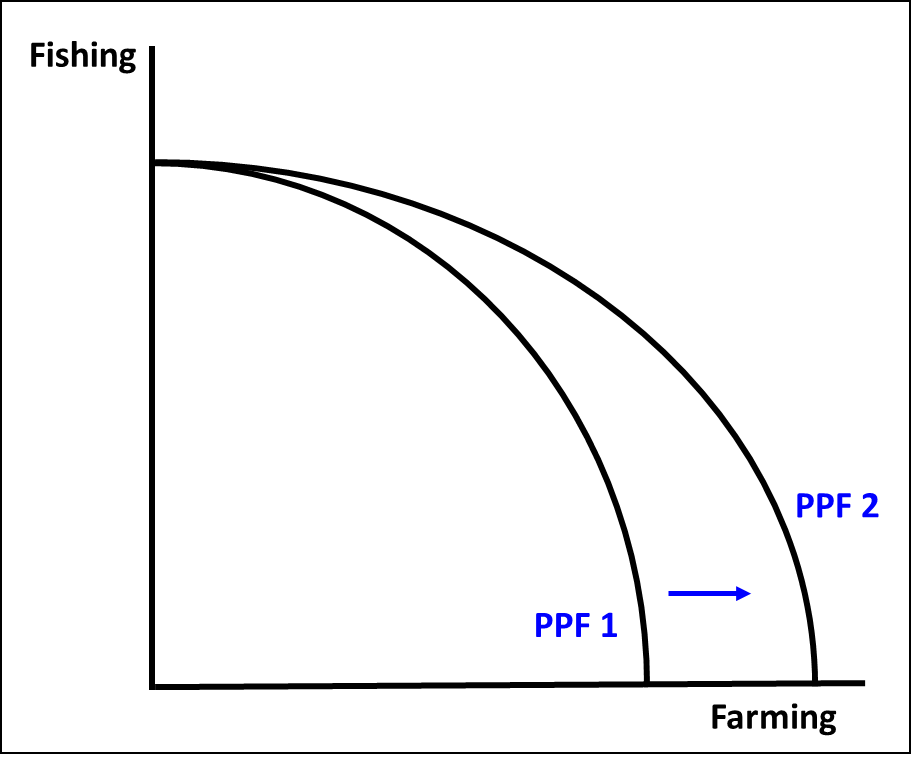

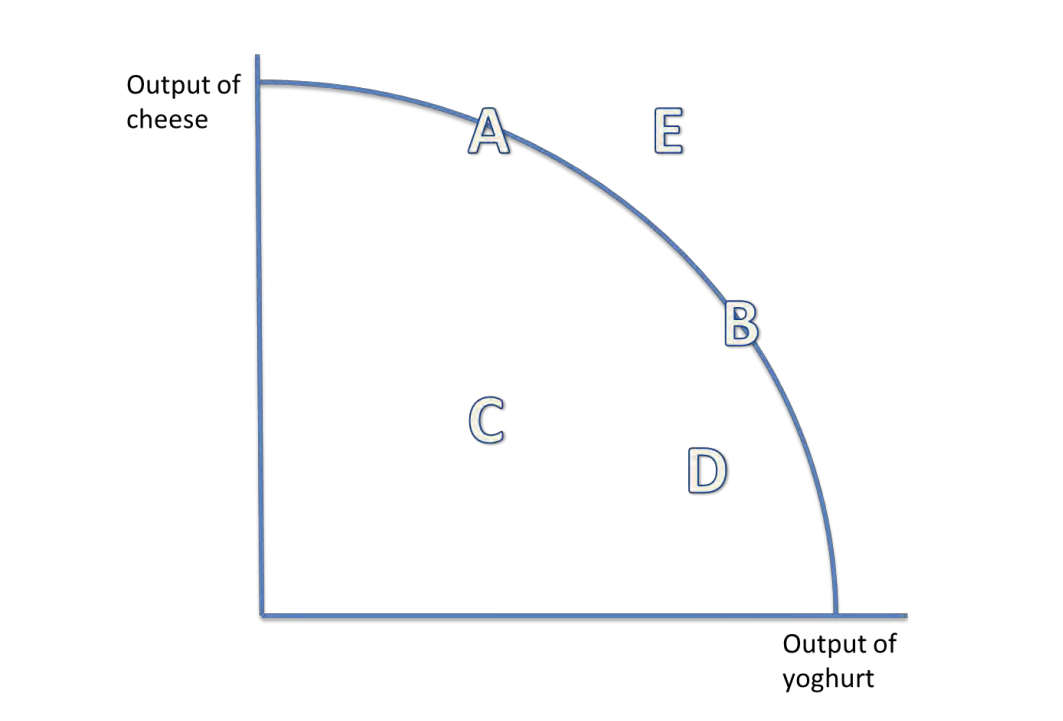

Production possibility frontiers(PPF's)

The maximum possible production of two goods or services with a given level of factors of production.

Opportunity cost on PPF

The opportunity cost of producing 6 more of services from (21 to 27) is 4 goods. This means the economy more specialised in producing services than goods(lower opportunity cost).

Efficiency on PPF

Productively efficient: ABCD where we are maximising use of factors of production.

-E is productively inefficient.

Allocatively efficient: Can’t know consumer demand from a PPF, so we can’t tell allocative efficiency. But if society only wanted healthcare, A is allocatively efficient. If society only wanted education, D is allocatively efficient.

Pareto efficiency: Nobody can be made better off without making somebody else worse off. ABCD is Pareto efficient as increasing production of one variable will decrease the production in the other.

What can cause the PPF curve to shift outwards?(economic growth + production increasing)

Increasing quantity + quality of factors of production. e.g. increase labour (quantity), increase productivity of labour using training (quality), ↑ technological advancement(quality).

What causes a movement in the PPF curve? (production increasing in farming)

Increase in quality+quantity of FoP that favours one variable instead of the other one. e.g. increase in land available for farming.

What does each letter describe? (obtainable production)

A+B: Attainable + most efficient combinations of output on the PPF.

C+D: Attainable but inefficient as resources (FoP) aren’t used to their full productive potential.

E: Unattainable with the current resources (FoP).

Law of diminishing returns

the more factors of production you employ at the next unit, the less you get of a return than the previous unit.

Marginal

At the next unit

Capital goods

Goods which can be used to produce consumer goods. e.g. machinery

Consumer goods

Goods which can't be used to produce other goods. e.g clothing

Consumer durables: Products that provide a steady flow of satisfaction/ utility over their working life e.g. washing machine, smartphone

Consumer non-durables: Products used up in the act of consumption e.g. drinking a coffee, turning on heating

Consumer services: e.g. a haircut, ticket to a show

Specialisation

The concentration on production on a narrow range of goods and services.

Division of labour

Breaking down the production process into separate tasks upon specialisation.

Pros +cons of specialisation + division of labour in organising production

PROS

Lower costs: Workers more skilled in particular tasks, higher productivity+efficiency, lower cost of training, lower cost of production, passed onto consumers.

EoS: resources efficiently produced, produce larger quantities, more revenue, reach EoS

CONS

Lower productivity: workers find repetitive tasks monotonous, job dissatisfaction, become unproductive.

Occupation immobility: tech may advance, job done by machines + becomes automated, workers lose jobs. Workers are so highly skilled in one job, difficult to transfer skill to another job

Pros +cons of specialisation + division of labour in trade

PROS

Comparative advantage: focus on producing a single good/ service + export to other countries where they have CA, higher efficiency

Living standards: trade allows for wider variety of goods + higher economic growth, enhancing satisfaction + CS, allocative efficiency.

CONS

Income inequality: certain industries benefit + some lose out to specialised foreign industries

Vulnerable to external shocks: reliance on trade exposes it to more risks of shocks, shutting down production, lose greatly.

Function of money

a medium of exchange

Can be widely accepted for payments of debt/ goods.

a measure of value

Measure relative values of different good/ services. e.g. jewellery is considered more valuable than a table because of the relative price, measured by money.

a store of value

Money has to hold its value to be used for payment. It can be kept for a long time without expiring.

a method of deferred payment

Money allows for debts to be created. People can therefore pay for things without having money in the present, and can pay for it later. This relies on money storing its value.

Production vs productivity

What are they measured by?

Production: a measure of the value of the output of goods + services

measured by national GDP or an index of production in a specific industry such as car manufacturing

Productivity: a measure of the efficiency of factors of production

measured by output per person employed/ output per person hour

Free market economy e.g. Singapore, Hong Kong

Based on supply and demand where prices are set freely between consumers + sellers, without intervention from the government.

-economists Adam Smith and Friedrich Hayek are associated with free markets.

FEATURES

Private ownership

Profit maximising- this increases competition

More freedom of choice

Role of government in allocating resources is low

High variety+quality of goods + services- to meet consumer demands + make profit.

Merit goods underproduced + demerit goods overproduced

Income inequality- income can’t be redistributed, no pension schemes.

Command economy e.g. Cuba, North Korea

The government controls all major aspects of the economy + economic production, including FoP.

-economist Karl marx is associated with command economies.

FEATURES

Public ownership

Maximise social welfare

Low freedom of choice

Role of government is high

Low variety+quality of goods/ services- No incentive for gov. to meet demands.

Merit + demerit goods- At social optimum

Income equality- progressive taxes, pension schemes

Mixed economy e.g. UK, France, Germany

This is an economy where both the free-market mechanism + gov. planning allocate resources in the country.

-gov. control is usually 40-60%.

FEATURES

Total efficiency is maximised

Role of gov. is limited to where intervention is necessary.

Pros + cons of free market economies

PROS

Promotes competition: Firms keep costs low + pass this onto consumers (low prices), consumer surplus is high, quality of goods are high due to more reinvestment. Meets consumer demands.

Job creation + economic growth: quantity at max level due to competition, profit max + efficient allocation of resources→labour is a derived demand→more jobs. Higher quantity being produced→more GDP→more growth.

-no gov. to ensure full employment

CONS

Market failure: Not guaranteed to get allocative efficiency or high competition e.g. monopolies + oligopolies- can destroy benefit of low prices. Make many assumptions in determining pros of free markets. Assume good information- consumers don’t make rational decisions when there is imperfect information. Overconsume demerit goods + underconsume merit goods.

Income inequality: Although price is efficient, they may not be fair, may exclude consumers like those who can’t afford efficient prices. e.g. if the good is a necessity, some can’t access it.

Pros + cons of command economies

PROS

Less income inequality: Gov. implements progressive taxes to redistribute income, provides pensions on elderly, etc, to ensure everyone has access to basic necessities (social welfare max).

Social welfare maximised: No monopolies to exploit consumers through higher prices. More efficient outcomes (gov allocates resources- healthcare, education, basic goods).

CONS

Lack of competition: Profit max is not the motive. This leads to less innovation + product development. Prices are not kept at its lowest. Reduces quality of goods/ services.

Shortages/ surpluses: No price mechanism to ration surpluses + deal with shortages. Inefficient allocation- resources aren’t sufficiently distributed.