ECN 104

0.0(0)

0.0(0)

Card Sorting

1/143

Earn XP

Study Analytics

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

144 Terms

1

New cards

Scarcity

We can’t have everything because everything is limited money, time and energy

2

New cards

Oppourtunity Cost

The cost of the best alternative given up

(Give up/Get)

(Give up/Get)

3

New cards

Smart choice (Voluntary Trade)

The value of what you get must be greater than the value of what you give up

4

New cards

Absolute Advantage

The ability to produce a product/service at a lower absolute cost than another producer

No basis for trade

No basis for trade

5

New cards

Comparative Advantage

The ability to produce a product/service at a lower Oppourtunity cost than another producer (more efficiently)

Basis for trade

Basis for trade

6

New cards

Trades

Make induviduals better off when each specializes in producing a product/service with comparative advantage

7

New cards

Production Possibility Frontier

A graph that shows the maximum combinations of products/services that can be produced with existing inputs

8

New cards

Points Above the PPF

Not attainable and not efficient

9

New cards

Points Under the PPF

Attainable but not efficient (all resources are not being used)

10

New cards

Points on The PPF

Attainable and efficient (all resources are being used)

11

New cards

Economic Model (Circular Flow Model)

Consists of 3 players-Consumers, producers and the government who interact in 2 markets-Input and Output

In input markets, households are sellers, businesses are buyers

In output markets, households are buyers, businesses are sellers

In input markets, households are sellers, businesses are buyers

In output markets, households are buyers, businesses are sellers

12

New cards

Inputs

Productive resources-labour, natural resources, capital equipment and entrepreneurial ability used to produce products and services

13

New cards

Marginal

‘’Additional” benefits from the next choice

Marginal Benefits= Δ Total benefit/ Δ Total quantity

Marginal Benefits= Δ Total benefit/ Δ Total quantity

14

New cards

Marginal Opportunity Cost

‘’Additional” Oppourtunity costs from the next choice

Marginal Opportunity cost= Δ Opportunity cost/ Δ Total quantity

Marginal Opportunity cost= Δ Opportunity cost/ Δ Total quantity

15

New cards

Implicit Cost

Opportunity costs of investing your own money/time

16

New cards

When marginal benefit is larger than marginal opportunity cost (MB>MOC)

Consume or produce more (wanted)

17

New cards

When marginal opportunity cost is larger than marginal benefit (MB

Consume or produce less (not wanted)

18

New cards

When Marginal benefit equals marginal oppourtunity cost (MB=MOC)

Indifference-consume or produce more (wanted)

19

New cards

The Law of Demand

If the price of a product/service rises, quantity demanded decreases (all other factors remaining the same)

20

New cards

Quantity demanded

The amount you actually plan to buy at a given price

21

New cards

Market demand

The sum of demands of all induviduals willing/able to buy a particular product/service

22

New cards

Demand curve

Illustrates the relationship between price and quantity demanded (all other factors remaining the same)

23

New cards

To read a demand curve

Read over and down

24

New cards

To read a marginal benefit curve

Read up and over

25

New cards

Change in Quantity Demanded

An increase in quantity demanded is a movement down the demand curve

A decrease in quantity demanded is a movement up along the demand curve

A decrease in quantity demanded is a movement up along the demand curve

26

New cards

Increase in demand

Increase in consumers willingness/ability to pay-rightwards shift of the demand curve

27

New cards

Decrease in demand

Decrease in consumers willingness/ability to pay-leftward shift of the demand curve

28

New cards

Substitutes

Prouducts/Service used in -lace of each other to satisfy the same want

29

New cards

Complements

Products/Services used together to satisfy the same want

30

New cards

Substitutes and Demand

As the price for one substitute increases, the demand for the other substitute will increase

As the price for one substitute decreases, the demand for the other substitute will decrease

As the demand for one substitute increases, the demand for the other substitute will decrease

As the demand for one substitute decreases, the demand for the other substitute will increase

As the price for one substitute decreases, the demand for the other substitute will decrease

As the demand for one substitute increases, the demand for the other substitute will decrease

As the demand for one substitute decreases, the demand for the other substitute will increase

31

New cards

Complements and Demand

As the price for one complement increases, the demand for the other complement will decrease

As the price for one complement decreases, the demand for the other complement will increase

As the demand for one complement increases, the demand for the other complement will increase

As the demand for one complement decreases, the demand for the other complement will decrease

As the price for one complement decreases, the demand for the other complement will increase

As the demand for one complement increases, the demand for the other complement will increase

As the demand for one complement decreases, the demand for the other complement will decrease

32

New cards

Normal Goods

Products/services you buy more of when your income

33

New cards

Inferior Goods

Products/Services you buy less of when your income increases

34

New cards

Normal goods and Demand

As income increases, demand increases

As income decreases, demand decreases

As income decreases, demand decreases

35

New cards

Inferior Goods and Demand

As income increases, demand decreases

As income decreases, demand increases

As income decreases, demand increases

36

New cards

Future Prices and Demand

As the expected future price increases, the demand today increases

As the expected future price decreases, demand today decreases

As the expected future price decreases, demand today decreases

37

New cards

Marginal Cost

Additional opportunity cost of increasing quantity supplied

Marginal Cost= Δ Total cost/ Δ Quantity

Marginal Cost= Δ Total cost/ Δ Quantity

38

New cards

Marginal Cost for Supply

Marginal cost is the opportunity cost of time

Marginal cost increases as your quantity supplied increase

Marginal benefit is measured in ($)

Marginal cost increases as your quantity supplied increase

Marginal benefit is measured in ($)

39

New cards

Marginal Benefit for Demand

Marginal benefit is the satisfaction you get

Marginal benefit decreases as your quantity demanded increases

Marginal cost is measured in ($)

Marginal benefit decreases as your quantity demanded increases

Marginal cost is measured in ($)

40

New cards

Supply

Businesses willingness to produce a particular product/service because price covers all opportunity costs

41

New cards

Quantity Supplied

The quantity you actually plan to supply at a given price

42

New cards

Market Supply

Sum of supplies of all business willing to produce a particular product/service

43

New cards

Law of Supply

If the price of a product/service increases, quantity supplied increases

44

New cards

Supply curve

Illustrates the relationship between price/quantity supplied (other things remaining the same)

45

New cards

Change in Quantity

An increase in quantity supplied is a movement up along a supply curve

A decrease in quantity supplied is a movement down along a supply curves

A decrease in quantity supplied is a movement down along a supply curves

46

New cards

Change in Supply

An Increase in supply is a rightwards shift of the supply curve

A decrease in supply is a leftwards shift of the supply curve

A decrease in supply is a leftwards shift of the supply curve

47

New cards

Future Price and Supply

As the expected future price increases, supply now decreases

As the expected future price decreases, supply now increases

As the expected future price decreases, supply now increases

48

New cards

Input Price and Supply

As the price of an input increases, the supply decreases

As the price of an input decreases, the supply increases

As the price of an input decreases, the supply increases

49

New cards

Market

The interactions between buyers and sellers

50

New cards

Shortage (excess demand)

When quantity demanded exceeds quantity supplied

Shortages create pressure for prices to rise

Rising prices provide signals to business to increase quantity supplied and for consumers to decrease quantity demanded, elimating the shortage

Shortages create pressure for prices to rise

Rising prices provide signals to business to increase quantity supplied and for consumers to decrease quantity demanded, elimating the shortage

51

New cards

Frustrated Buyers

Market price too low

52

New cards

Frustrated Sellers

Market price too high

53

New cards

Surplus (excess supply)

Where quantity supplied exceeds quantity demanded

Surpluses create pressure for prices to fall

Falling prices provide signals to business to decrease quantity supplied and for consumers to increase quantity demanded, eliminating the surplus

Surpluses create pressure for prices to fall

Falling prices provide signals to business to decrease quantity supplied and for consumers to increase quantity demanded, eliminating the surplus

54

New cards

Market Clearing Price

The price that equalizes quantity demanded and quantity supplied

55

New cards

Equilibrium Price

The price that balances forces of competition and cooperation, there is no tendency for change

56

New cards

Effect of Demand on Quantity Supplied

As demand increases, equilibrium price increases and quantity supplied increases

As demand decreases, equilibrium price decreases and quantity supplied decreases

As demand decreases, equilibrium price decreases and quantity supplied decreases

57

New cards

Effect of Supply on Quantity Demanded

As supply increases, the equilibrium price decreases and quantity demanded increases

As supply decreases, the equilibrium price increases and quantity demanded decreases

As supply decreases, the equilibrium price increases and quantity demanded decreases

58

New cards

Increase in both demand and supply

Quantity increases

Price is ambiguous

Price is ambiguous

59

New cards

Decrease in both demand and supply

Quantity decreases

Price is ambiguous

Price is ambiguous

60

New cards

Increase in demand and decrease in supply

Price increases

Quantity is ambiguous

Quantity is ambiguous

61

New cards

Increase in supply and decrease in demand

Price decreases

Quantity is ambiguous

Quantity is ambiguous

62

New cards

Consumer Surplus

The difference between the amount a consumer is willing and able to pay and the price actually paid-the area under the marginal benefit curve but above market price

CS=(Willing-Actual)xQunantity

CS=(Willing-Actual)xQunantity

63

New cards

Producer Surplus

The difference between the amount a producer is willing to accept and the price actually received-the area below market price but above the marginal cost curve

PS=(Equilibrium price-marginal cost)

PS=(Equilibrium price-marginal cost)

64

New cards

Efficient Market Outcome

Consumers only buy products/services where marginal benefit is greater than price

Products and services are produced at the lowest cost-prices just cover all opportunity costs of production

Marginal benefit=Marginal cost

Total surplus is at a maximum

Products and services are produced at the lowest cost-prices just cover all opportunity costs of production

Marginal benefit=Marginal cost

Total surplus is at a maximum

65

New cards

Deadweight Loss

Decrease in total surplus compared to an economically efficient outcome

Deadweight Loss= loss of CS+loss of PS

Deadweight Loss= loss of CS+loss of PS

66

New cards

Elasticity (price elasticity of demand)

m= % change in quantity demanded/ % change in price

67

New cards

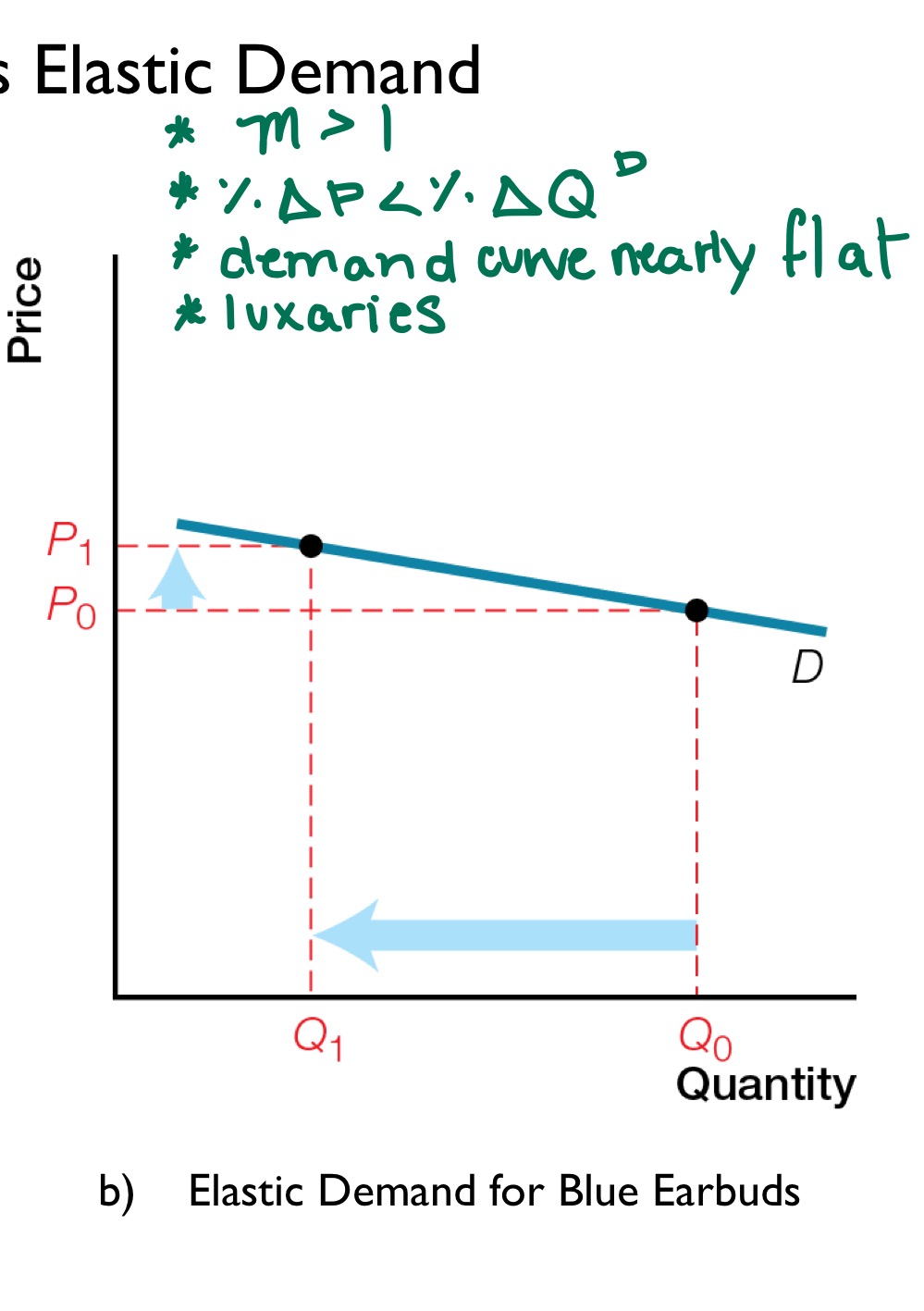

Elastic Demand

Large response in quantity demanded when prices increase

Where m>1 (larger than 1)

Demand curve is nearly flat

Usually for Luxury items Thant are not necessary to buy perfectly inelastic\

Where m>1 (larger than 1)

Demand curve is nearly flat

Usually for Luxury items Thant are not necessary to buy perfectly inelastic\

68

New cards

Inelastic Demand

Small response to quantity demanded when prices increase

Where 0

Where 0

69

New cards

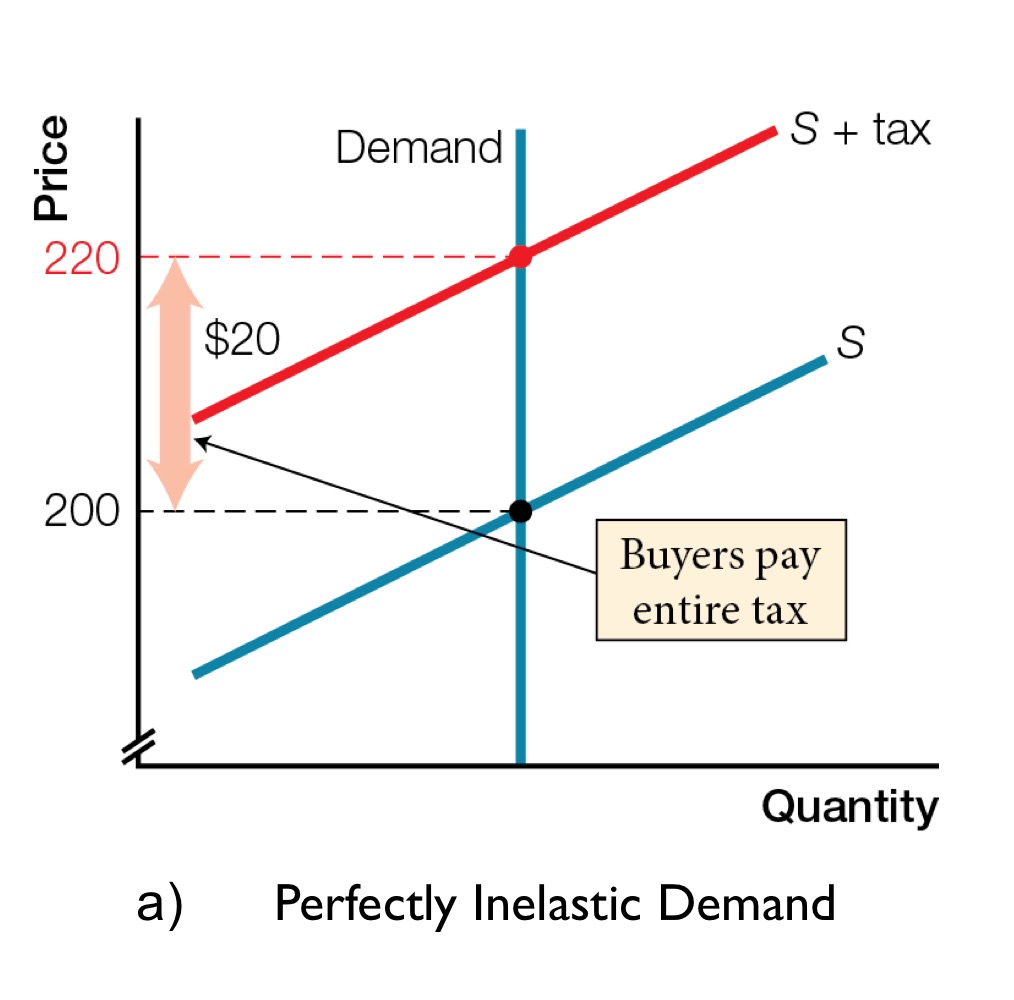

Perfectly Inelastic Demand

Quantity demanded does not respond to change in price

Where m=0

Demand curve is vertical

Completely unresponsive to price changes

Where m=0

Demand curve is vertical

Completely unresponsive to price changes

70

New cards

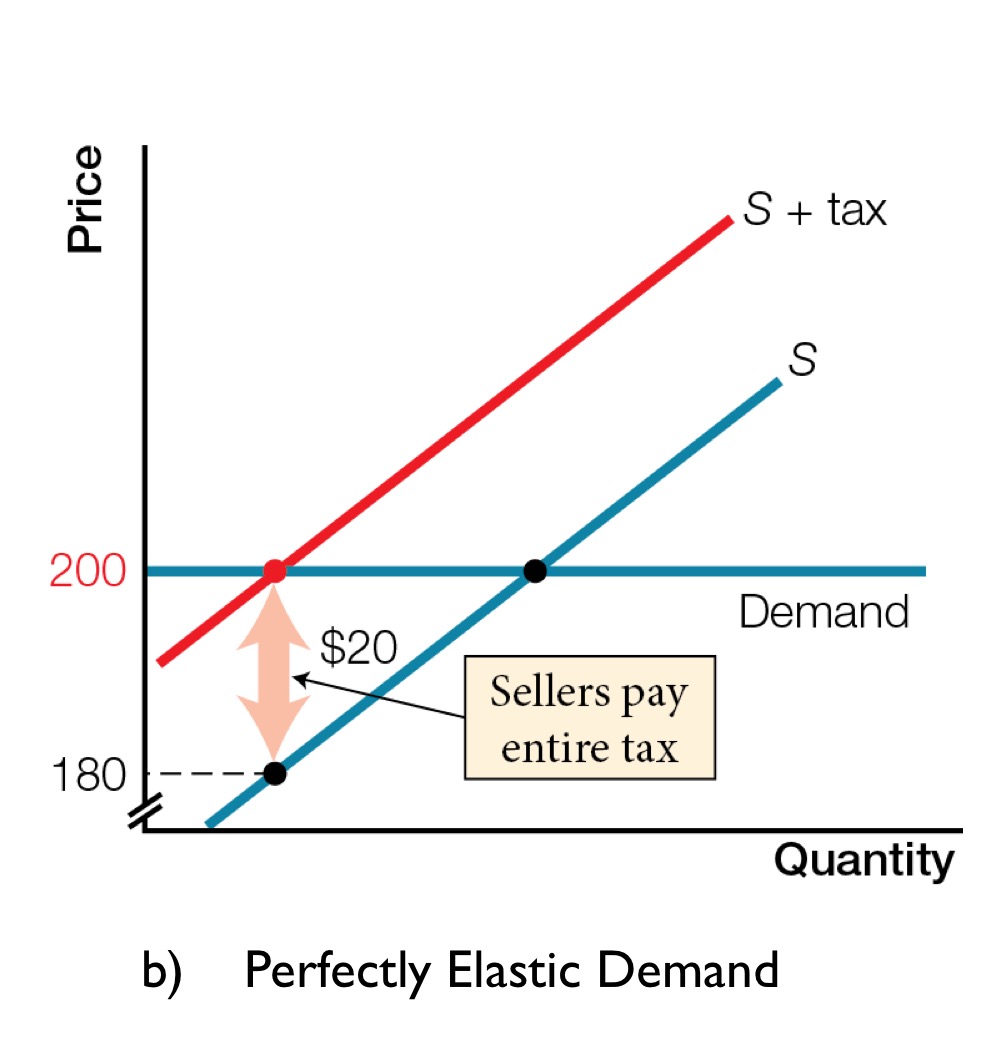

Perfectly Elastic Demand

Quantity demanded has infinite response to change in price

Where m=infinity

Demand curve is horizontal

Completely responsive to price changes

Where m=infinity

Demand curve is horizontal

Completely responsive to price changes

71

New cards

Influences on Elasticity

Available substitutes-more substitutes mean more elastic demand

Time to adjust-longer time to adjust means more elastic demand

Proportion of Income Spent-greater proportion of income spent on a product/service means more elastic demand

Time to adjust-longer time to adjust means more elastic demand

Proportion of Income Spent-greater proportion of income spent on a product/service means more elastic demand

72

New cards

Total Revenue (TR)

All money a business receives form sales

For businesses facing elastic demand (m>1), price cuts increase total revenue

For business facing Inelastic demand (m

For businesses facing elastic demand (m>1), price cuts increase total revenue

For business facing Inelastic demand (m

73

New cards

Elasticity of Supply

Measures by how much quantity supplied responds to a change in price

m= % change in quantity supplied/ % change in price

m= % change in quantity supplied/ % change in price

74

New cards

Inelastic Supply

Small response in quantity supplied when prices rise

Where m

Where m

75

New cards

Elastic Supply

Large response in quantity supplied when prices rise

Where m>1

Easy and inexpensive to increase production

Where m>1

Easy and inexpensive to increase production

76

New cards

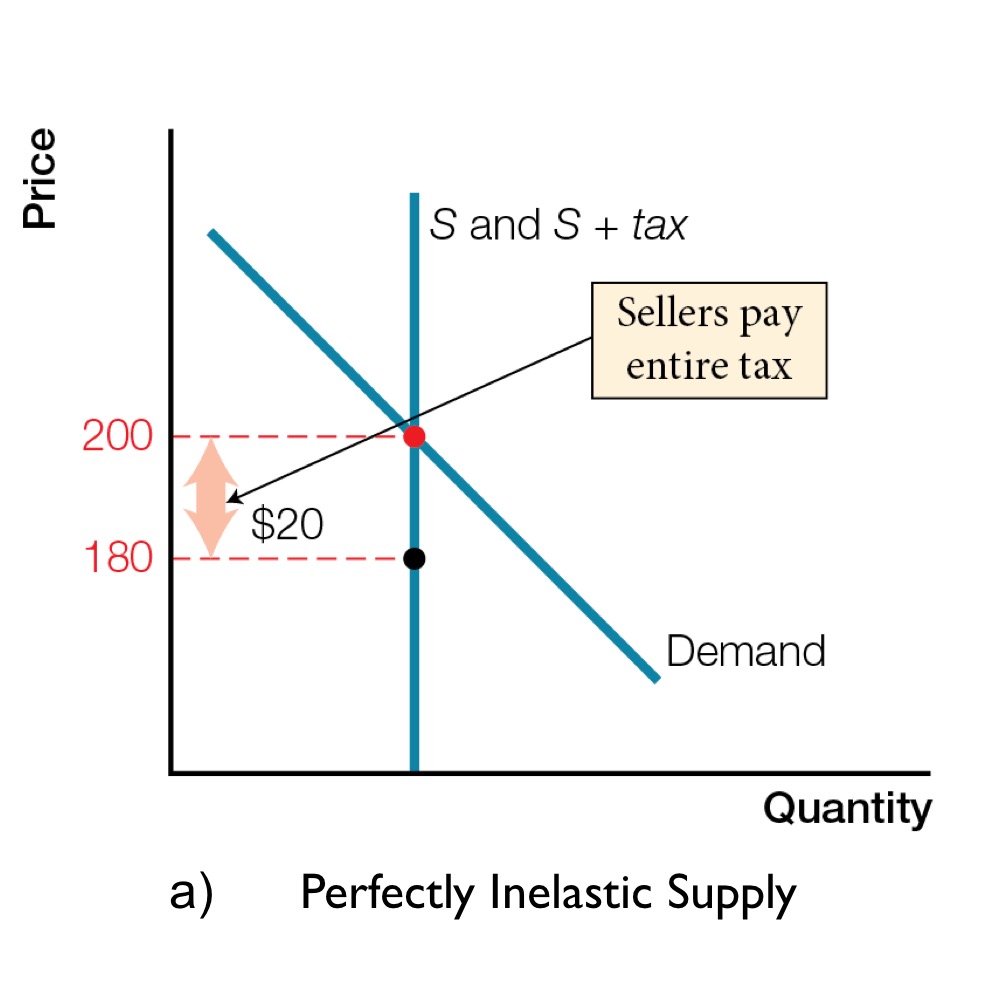

Perfectly Inelastic Supply

Quantity Supplied does not respond to change in price

Where m=0

Supply curve is vertical

Where m=0

Supply curve is vertical

77

New cards

Perfectly Elastic Supply

Quantity supplied has infinite response to change in price

Where m=infinity

Supply curve is horizontal

Where m=infinity

Supply curve is horizontal

78

New cards

Influences on Elasticity of supply

Availability of additional inputs-more available inputs men more elastic supply

Time production takes-less time means more elastic supply

Time production takes-less time means more elastic supply

79

New cards

Cross elasticity of demand

Measures responsiveness of the demand for a product/service to a change in price of a substitute/complement

m= % change in quantity demanded/ % change in price of substitute/complement

m= % change in quantity demanded/ % change in price of substitute/complement

80

New cards

Cross elasticity of Demand Substitutes

Cross elasticity of demand is a positive number for substitutes

The larger the number, the larger the change in demand, the larger the shift of the demand curve and the closer the products/services are to perfect substitutes

The larger the number, the larger the change in demand, the larger the shift of the demand curve and the closer the products/services are to perfect substitutes

81

New cards

Cross elasticity of demand complements

Cross elasticity of demand is a negative number for complements

The larger the number, the larger the change in demand, the larger the shift of the demand curve and the closer the products/services are to perfect complements

The larger the number, the larger the change in demand, the larger the shift of the demand curve and the closer the products/services are to perfect complements

82

New cards

Income elasticity of demand

Measures responsiveness of the demand for a product/service to a change in income

m= % change in quantity demanded/ % change in income

m= % change in quantity demanded/ % change in income

83

New cards

Income elasticity of demand for Normal goods

Positive for normal goods-increase in income increases demand for normal goods

84

New cards

Income elasticity of demand for Inferior goods

Negative for inferior goods-increase in income decreases demand for inferior goods

85

New cards

Income Inelastic Demand

% change in quantity is less than the % change in price

Where 0

Where 0

86

New cards

Income Elastic Demand

% change in quantity is greater than % change in price

Where m>1

Normal goods that are luxuries

Where m>1

Normal goods that are luxuries

87

New cards

Tax Incidnece

The division of a tax between buyers and sellers-depends on elasticities of demand and supply

88

New cards

Tax Incidence of Perfectly Inelastic Demand

Buyers Pay all

89

New cards

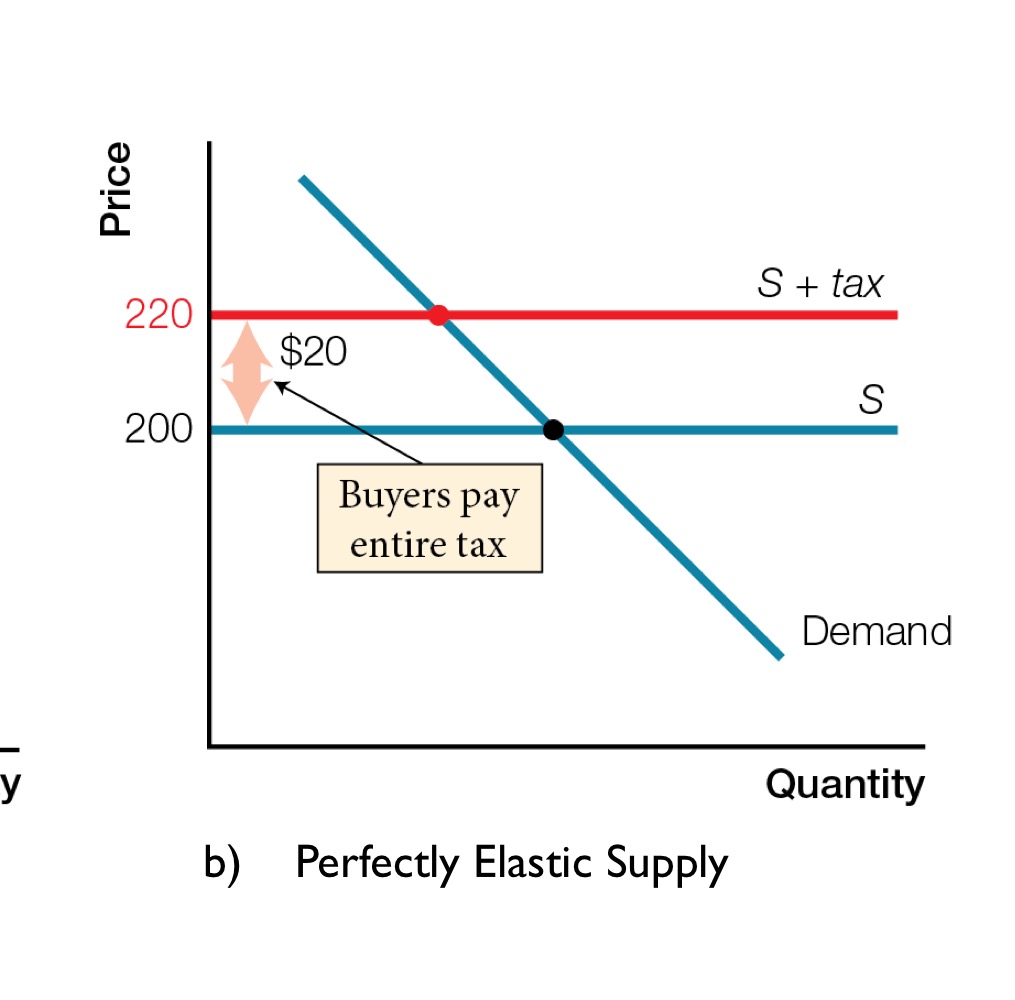

Tax incidence of perfectly elastic demand

Sellers pay all

90

New cards

Tax Incidence on more Inelastic demand

Buyers pay more

91

New cards

Tax incidence on more elastic demand

Sellers pay more

92

New cards

Tax incidence on perfectly Inelastic supply

Sellers pay all

93

New cards

Tax incidence on more Inelastic supply

Sellers pay more

94

New cards

Tax incidence on more elastic supply

Buyers pay more

95

New cards

Tax incidence on perfectly elastic supply

Buyers pay all

96

New cards

When price is fixed below market-clearing

Shortages develop-quantity demanded > quantity supplied

Consumers are frustrated

Consumers are frustrated

97

New cards

When price is fixed above market clearing

Surpluses develop-quantity supplied > quantity demanded

Businesses are frustrated

Businesses are frustrated

98

New cards

Governments can fix prices

But can’t force businesses/consumers to produce/buy at the fixed price

Businesses can reduce output or move resources elsewhere

Consumers can reduce purchases or buy something else

Businesses can reduce output or move resources elsewhere

Consumers can reduce purchases or buy something else

99

New cards

Price ceiling

Maximum price set by the government-making it illegal to charge a higher price

Ex.rent controls

Ex.rent controls

100

New cards

Robin Hood Principle

Take from the rich (landlords) and give to the poor (tenants)