Understanding the Economy: Key Concepts and Analysis

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

28 Terms

What is the economy?

The economy refers to the system of production, distribution, and consumption of goods and services within a society.

What is the difference between needs and wants?

Needs are essential for survival (e.g., water), while wants are things we would like to have but can survive without.

What are the four factors of production?

Natural resources, human resources, capital resources, and entrepreneurship.

What are natural resources?

Natural resources are 'gifts of nature' such as air, water, minerals, and energy resources like coal and oil.

What do human resources refer to?

Human resources refer to the quantity and quality of the labor force, including both labor and enterprise.

What is capital in economics?

Capital refers to man-made resources, such as tools and machinery, that assist in the production of goods and services.

What is a cost-benefit analysis (CBA)?

CBA is a process that sums potential rewards from a situation or action and subtracts the total costs associated with taking that action.

What are the steps in conducting a cost-benefit analysis?

1. Understand your situation and identify your goals. 2. List all costs (financial and non-financial). 3. List all benefits. 4. Ensure benefits outweigh costs.

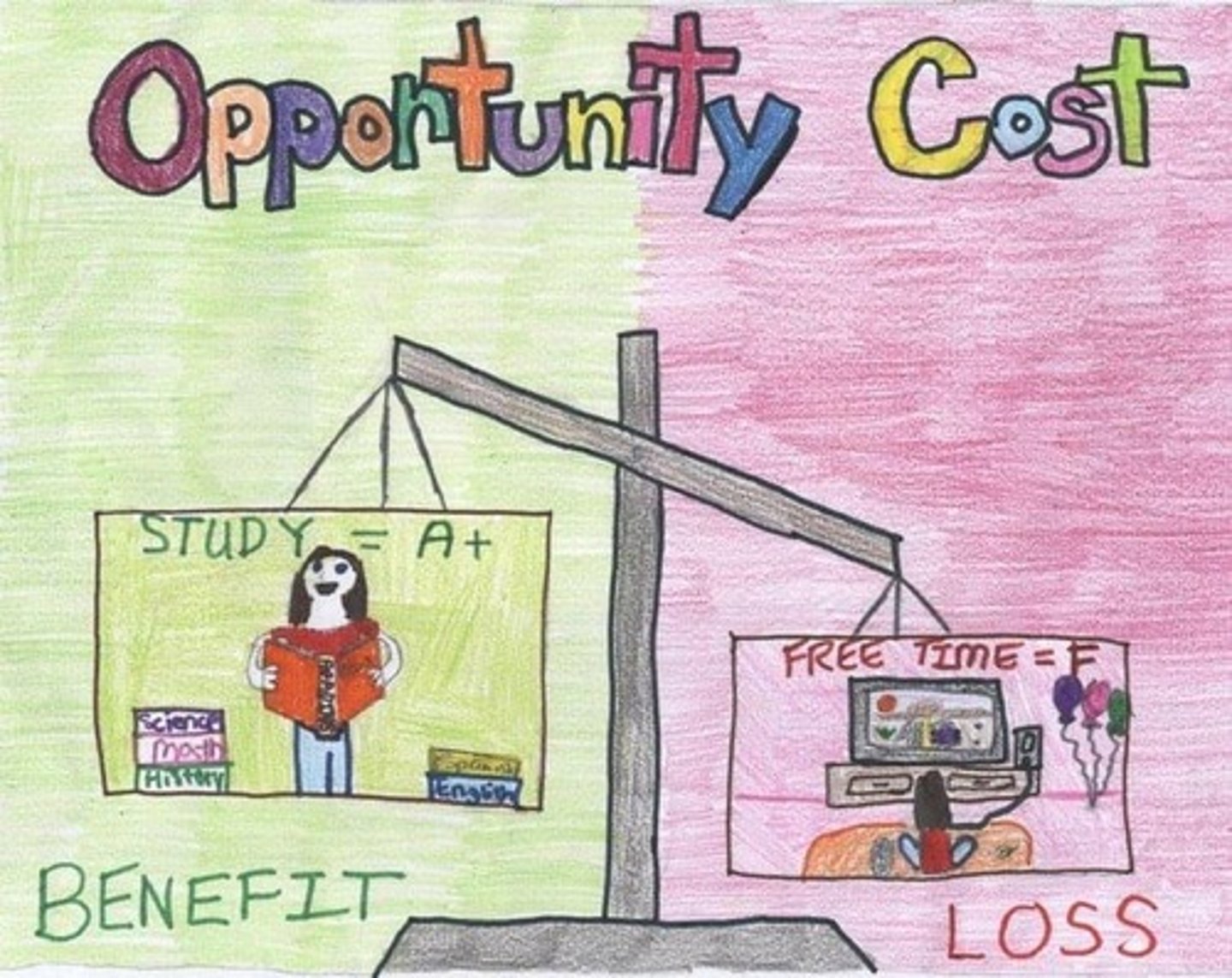

What is opportunity cost?

Opportunity cost is the value of the second best alternative that is forgone when a choice is made.

What characterizes a traditional or subsistence economy?

Producers are self-sufficient, producing enough to survive without aiming for profit, and money is not used.

Give an example of a traditional economy.

The Oribu tribe in the Brazilian Jungle Forest, which practices self-sufficiency and shares resources.

What defines developing economies?

Economies that have shifted from subsistence agriculture to specialization of work and product, encouraging industrial growth.

What are emerging economies?

Emerging economies are those experiencing rapid change, urbanization, and high levels of economic growth.

What are modern economies?

Fully developed economies with access to a wide variety of goods and services, complex credit systems, and high wage earnings.

What is the role of specialists in a modern economy?

Specialists produce the goods and services needed and wanted by consumers, relying on each other in a market economy.

What are some costs to consider in economic decision-making?

Financial costs, time, disruption, ethics/morality, environmental impact, opportunity costs, and negative externalities.

What benefits should be considered in economic decision-making?

Increased wealth and earnings, overall satisfaction, future efficiency, environmental benefits, and ethical considerations.

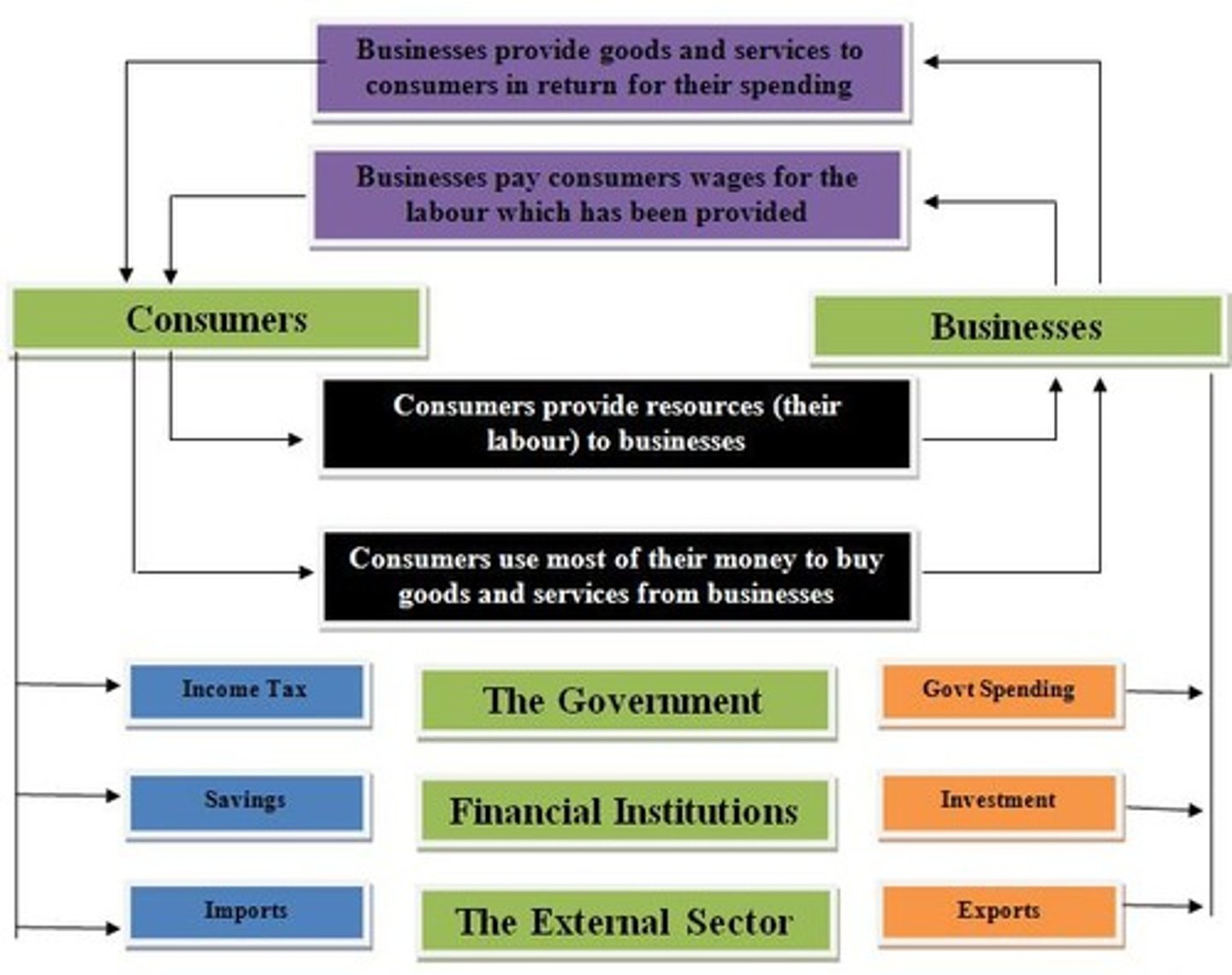

What is the significance of the circular flow matrix in economics?

It illustrates how money and resources flow through the economy among households, businesses, and the government.

What is the importance of distinguishing between needs and wants in economics?

It helps understand consumer behavior and the allocation of resources.

How does religion and customs impact economies?

They can influence production methods, distribution practices, and consumption patterns.

What is a disadvantage of buying a car for Veronica?

Increased financial burden from loan repayments and maintenance costs.

What is an advantage of not buying a car for Veronica?

Savings on expenses related to car ownership, such as insurance and fuel.

What is a disadvantage of not buying a car for Veronica?

Limited mobility and reliance on others for transportation.

What is an advantage of buying a car for Veronica?

Increased independence and ability to work more shifts.

What is the role of opportunity costs in decision-making?

It helps evaluate the trade-offs involved in choosing one option over another.

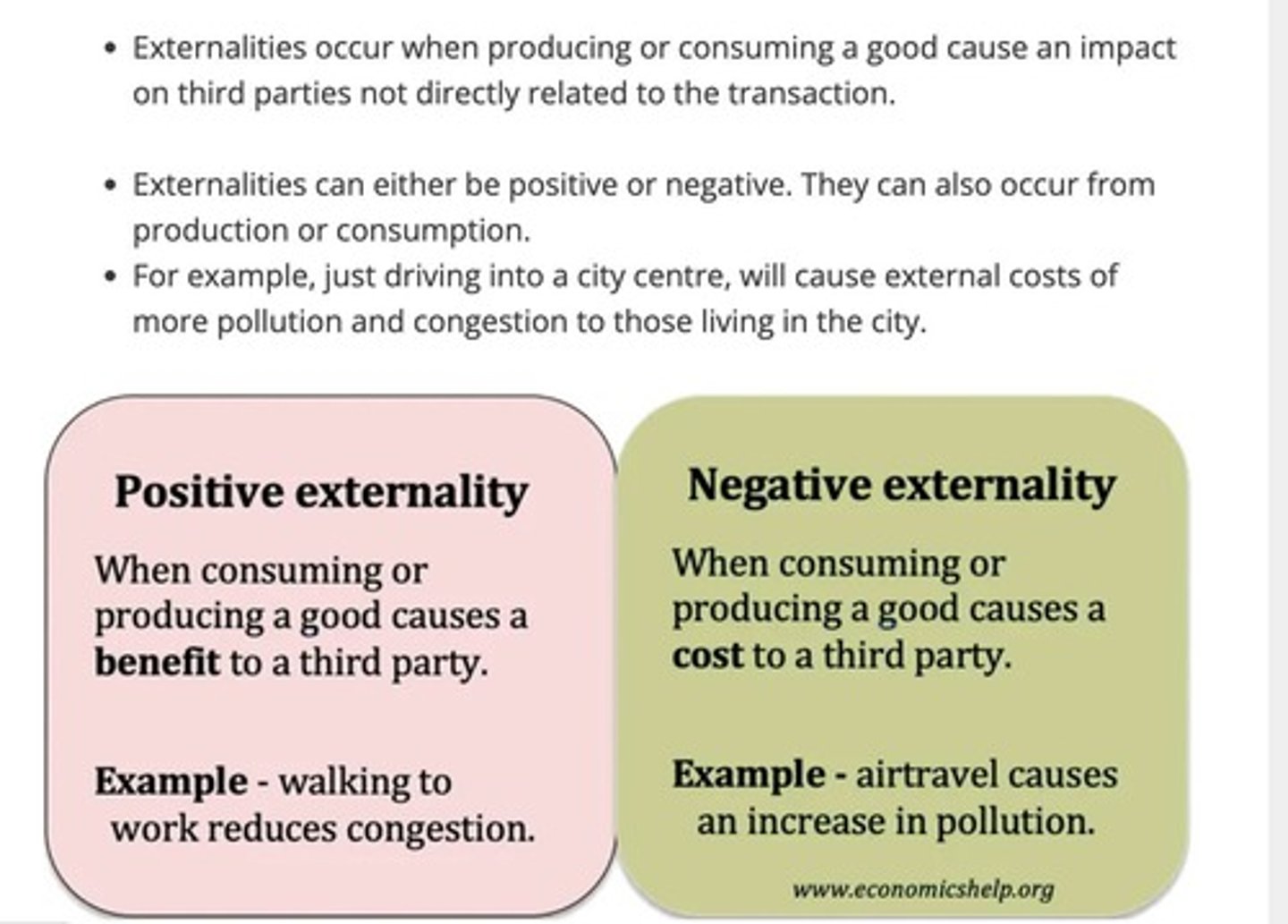

What are negative externalities?

Negative externalities are unintended adverse effects on third parties resulting from economic activities.

What is the impact of urbanization in emerging economies?

It leads to increased job opportunities, but can also result in overcrowding and strain on infrastructure.

What is the significance of custom and religious beliefs in traditional economies?

They influence production methods and distribution practices, often prioritizing community needs over profit.