4.1.4 - Production, costs and revenue

1/87

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

88 Terms

What is production?

- The process by which inputs are combined, transformed, and turned into outputs.

- We can produce both goods and services

What is Productivity?

Output per unit of input per time period

What is labour productivity?

Output per worker

Why is it good to have good productivity?

- If you are more productive, you can produce the same quantity of output, but with less inputs required, so the average cost per unit is lowered

How can productivity be increased?

- Training workers

- Using more advanced machinery

What are potential reasons why the UK's productivity isn't growing?

Poor investment in new capital goods

- Low wages

- Employers hoarding workers

What is specialisation in division of labour?

- When each worker concentrates on a specific task in the production process

- Firms can then take advantage of increased efficiency and can lower their average costs of production

How was the idea of specialisation established?

- Adam Smith said by dividing the production of pins into 18 different tasks, the output would significantly increase, as it would allow each worker to specialise

What are the advantages of specialisation?

- Higher output and potentially higher quality

- There's more competition in the market which incentivises firms to lower their prices to get more people buying from them

- There's more opportunities for economies of scale, so market size increases

What are the disadvantages of specialisation?

- Work becomes repetitive, which could lower motivation of workers and eventually reduce productivity

- It could later result in structural unemployment, as workers would have been doing the same tasks for so long, so if their industry goes down, the workers may not have transferable skills

- By producing one type of good consistently, variety

What is specialisation in the production of certain goods?

- Countries can specialise in the production of certain goods

- For example, Norway is the world's largest oil producers. Country's that are unable to produce oil can trade with Norway to get the oil

What is comparative advantage?

- When a country can produce a good at a lower opportunity cost than another country

What is absolute advantage?

- When a country can produce more of a good than another country with the exact same inputs

What are fixed costs?

Indirect costs which do not vary with output, so firms must pay them regardless

What are examples of fixed costs?

- Rental costs

- Annual business rate

What are variable costs?

- Direct costs which do vary with output

- As production increases, total variable costs will rise

What are examples of variable costs?

- Raw materials - The more you produce, the more raw materials you need

= Wages of employees - The more you produce, the greater worker wages are

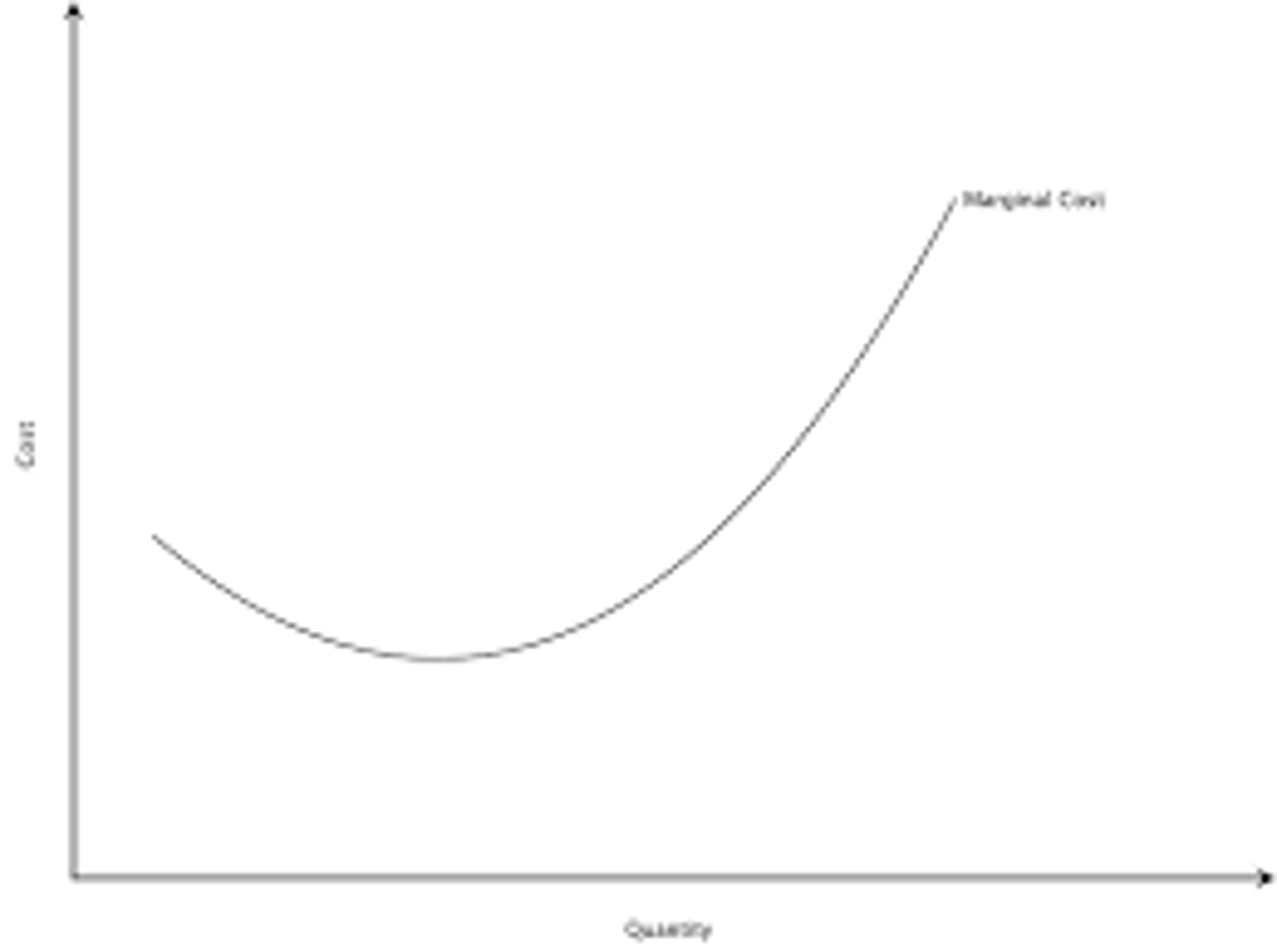

What are marginal costs?

- The cost of using an extra unit of output. They can be used to see if it's worth producing an extra unit

- Change in total cost/ change in quantity

What are average costs?

-How much it costs to produce each unit of output

- Average cost=total cost/output

What are total costs?

- Average cost x output

- Or total fixed costs+ total variable costs

What is the short run?

- The time period where at least one of the factors of production is fixed and cannot be varied

- The only way a firm can produce more in the short run is by adding more variable factors of production such as labour

What is the long run?

- The time period where no factors of production are fixed, so you can increase your production in an easier manner

Is the quantity of labour variable or fixed for firms?

Variable

Is the quantity of capital variable or fixed for firms?

Fixed

What does a total fixed cost diagram look like?

- It is a straight line. Costs do not vary with output

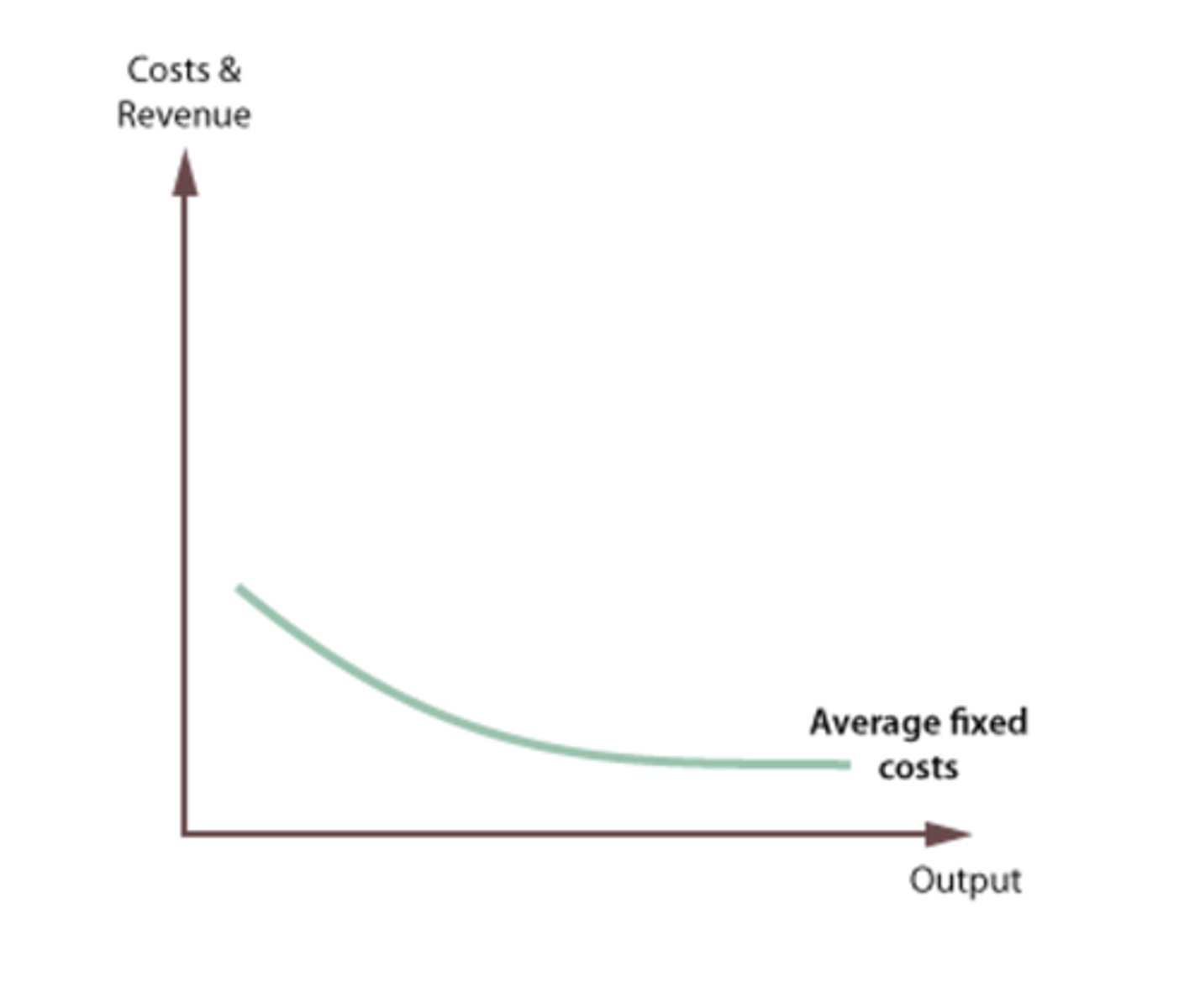

What does an average fixed cost diagram look like?

- As your increase your output, your costs fall

- This is because you divide a constant number by an ever increasing number

What does an average variable cost diagram look like?

- It is U-shaped because as you increase your output, your costs will fall up until the law of diminishing marginal returns kicks in, where costs will begin to rise again

- At this point, the wage cost of employing an extra worker is still the same, but each worker is less productive than the previous one

- Therefore, total variable costs rise faster than output and marginal output also rises

Average Total Cost (ATC)

- The same shape as the average variable cost curve but it is higher up

What is average variable cost?

Total cost of employing variable factors of production divided by output size

What is average fixed cost?

Total cost of producing fixed factors of production divided by output size

How is a firm's short run marginal cost curve derived from short run production theory?

- Short run marginal costs are determined by changes in variable costs of production, as fixed costs don't change with output

- If we assume labour is the only variable factor of production, variable costs must be wage costs. When all workers have the same hourly wage, total costs rise in exact proportion to the number of workers employed

- If a firm benefits from increasing marginal returns to labour, total variable costs of production rise at a slower rate than output

- Therefore, the marginal cost of producing one extra unit of output falls

- However, after this, law of diminishing returns kicks in and short run marginal costs rise as output increases, so the wage cost of employing an extra worker is the same, but each worker is less productive

- Therefore, total variable costs rise faster than output and short run marginal costs rise

How does marginal cost relate to average variable cost and average total cost?

- In the same way a firms short run marginal cost curve comes from the marginal returns of the variable factors of production, the firm's AVC curve comes from the average returns scale

- When increasing average returns are experienced with the labour force becoming more efficient and productive, the AVC per unit of output falls as output rises

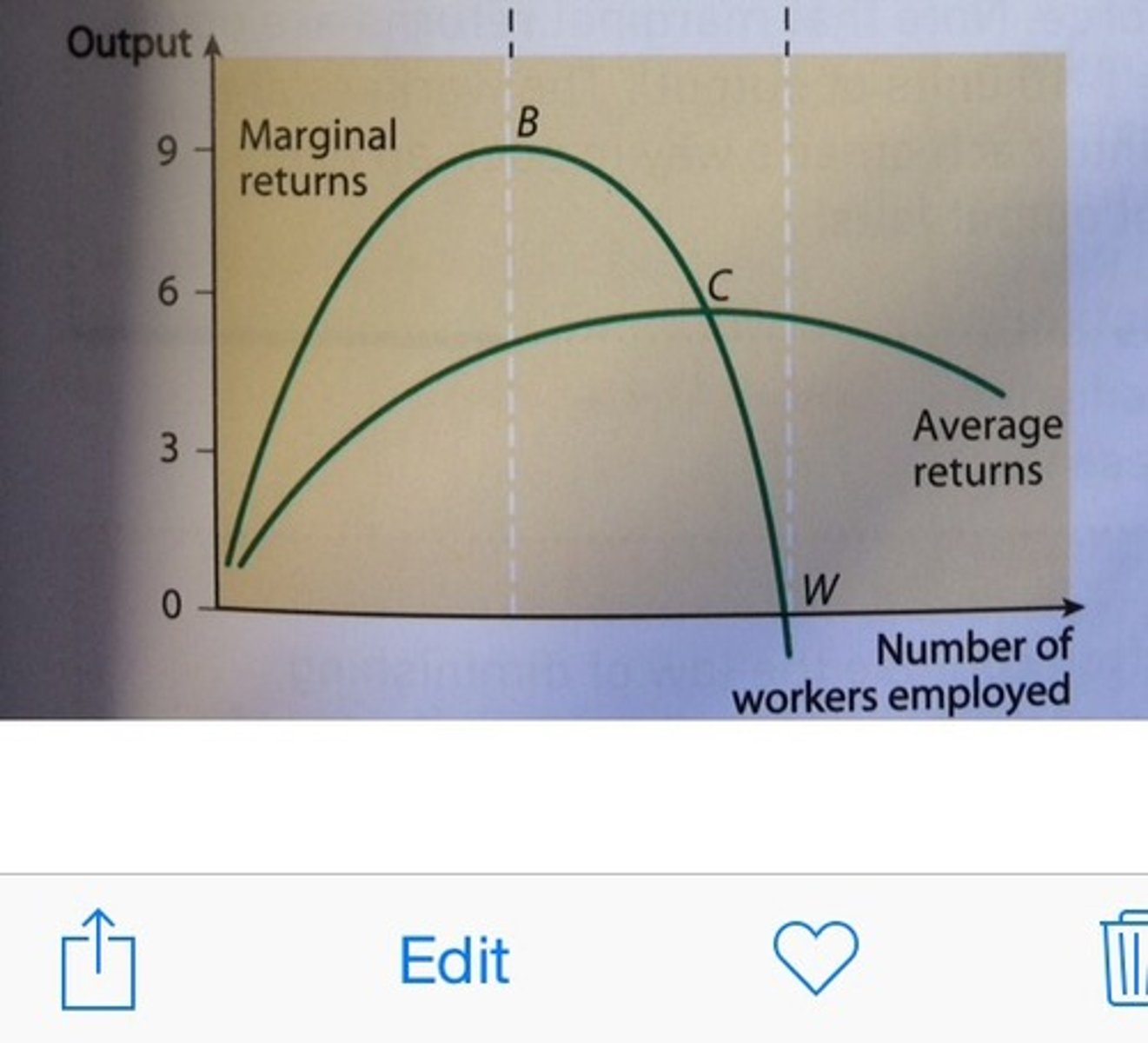

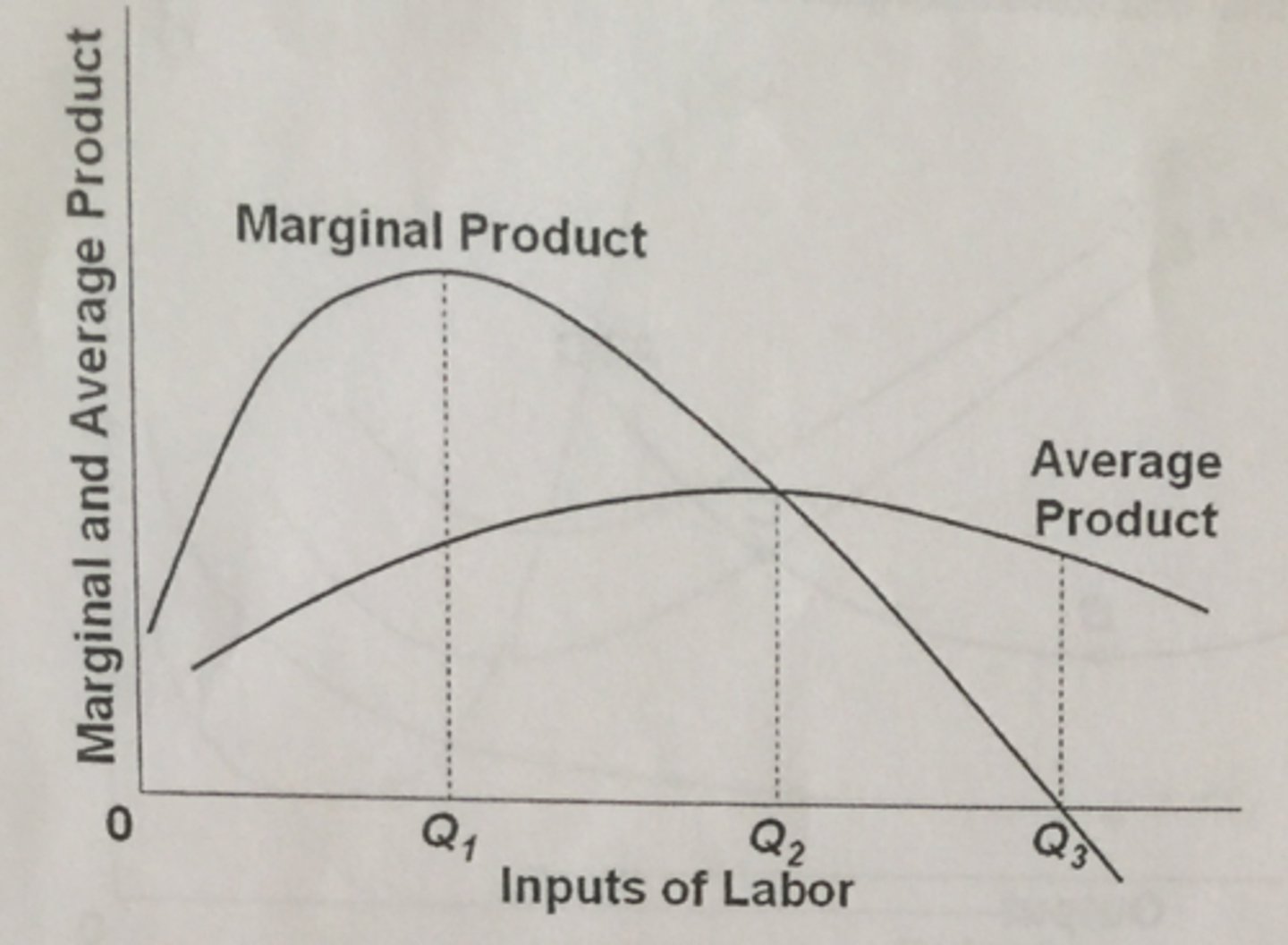

Marginal returns and average returns

- The marginal returns curve intersects the average returns curve at its highest point

What is a long run average cost curve?

- Long run total cost divided by output. It's the same shape as the average variable cost curve but it's because of the economies of scale and not the diminishing law of marginal utility

- As you increase levels of production, your unit cost decreases, which is economies of scale

- Overtime, you may get to a stage where you produce so much that you begin to suffer from diseconomies of scale and costs increase, which could be due to comunication problems as a firm begins to get too big

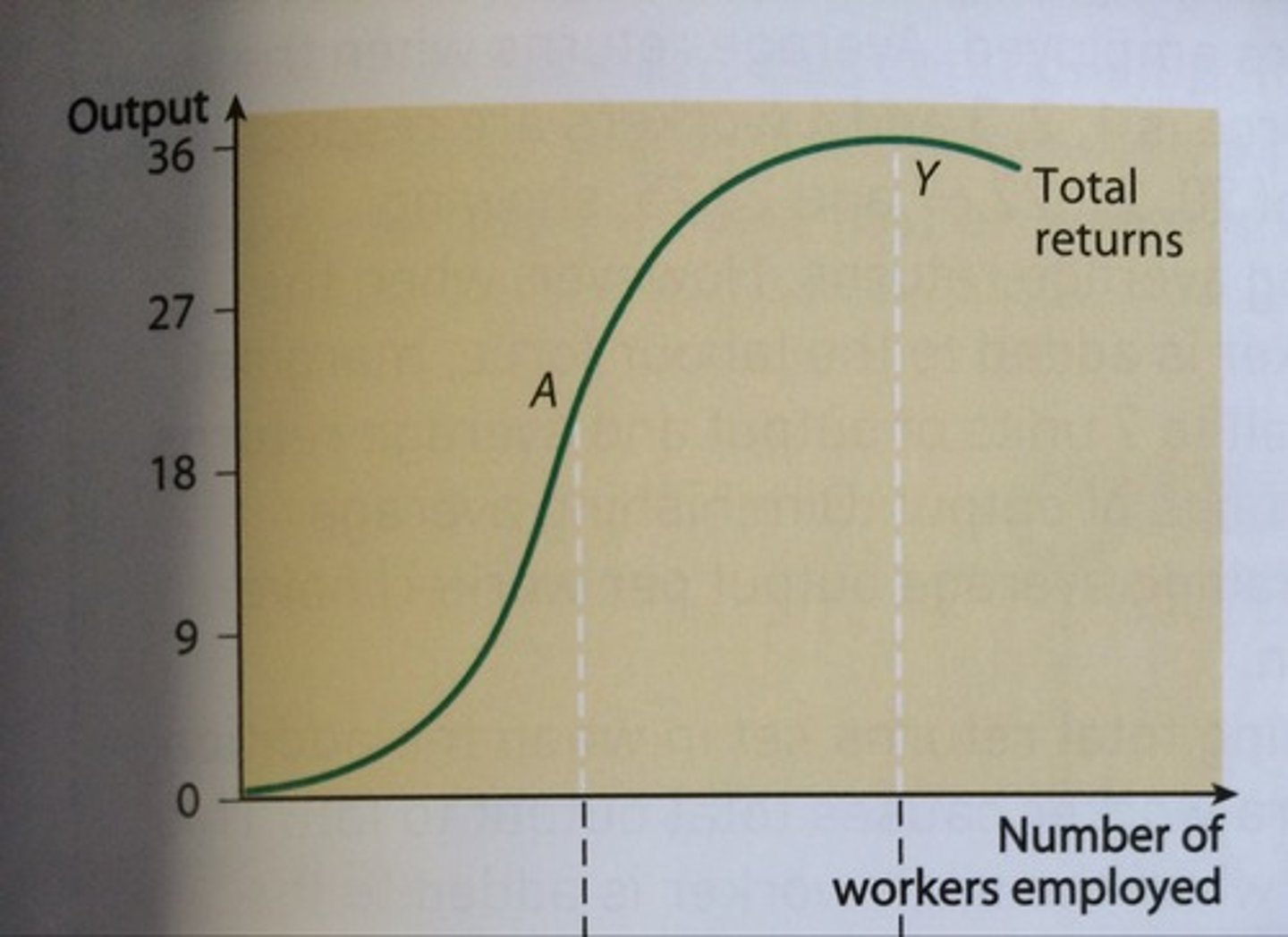

What is the Law of Diminishing Returns?

- When variable factors of production are added to fixed factors of production, total and marginal product will rise initially but then fall

What is Total product?

Total output produced by a number of units of factors over a period of time

Average product x quantity of workers

What is Marginal Product?

Extra unit derived per extra unit of input

Change in total product/ change in quantity of workers

What is Average product?

Total Product / quantity of workers

What is the law of diminishing returns?

- As you keep adding variable factors of production to fixed factors of production, output will initially increase until the fixed factors of production get used up, which is where output will begin to fall

How are Marginal and Average Returns affected by diminishing returns?

- Output initially rises as labour productivity increases

- This happens due to specialisation and an under utilisation of fixed factors of production

- For specialisation, as we employ workers, they can learn from the previous workers to produce at a faster rate. For the under utilisation, there is enough work space for the workers

- However, eventually, marginal product and labour productivity fall as we employ more workers

- Fixed factors of production become a constraint as there isn't enough space to match the increase in workers

How is Total Returns affected by diminishing returns?

-At the beginning, the shape of the total revenue curve increases, where the labour force benefits from increasing marginal returns

- However, after this, law of diminishing marginal returns kicks in, and the total returns continues to rise, as more workers are combined with capital, however, it rises at a slower rate than previously

- After this, the total returns falls, as workers begin to get in the way of each other to the point where marginal returns becomes negative

What is the relationship between marginal returns and average returns

- When marginal> average, average rises

- When marginal< average, average falls

- When marginal=average, average stays constant

What is Returns to scale?

The rate by which output changes if the scale of the factors of production are changed

What is an increase in returns to scale?

- When the inputs through factors of production are increased, output increases by a greater rate

- E.g, if inputs double, output quadruples

What is a constant returns to scale?

- When the scale of the factors of production employed increases, output increases at the same rate

- If input doubles, output also doubles

What is a decrease in returns to scale

When the scale of the factors of production increases, output increases by a smaller rate

- When input quadruples, output doubles

What are the inputs?

- Factors of production

How does returns to scale work?

- Initially, as inputs through factors of production are increased, outputs are increased by a greater extent, so costs are lowered. This is increasing returns to scale, and the firm experiences economies of scale

- Eventually, the firm will reach the MES (Minimum efficient scale) lowest level of output required to exploit economies of scale. A firm should stop increasing output here

- Next, they will experience a constant returns to scale, where, there are no changes to costs

- However, after this, a firm experiences a decrease in returns to scale, where as inputs increase by a certain extent, output increases at a smaller rate. This is a diseconomies of scale

What is Economies of scale?

As output increases, long run average cost falls

What is Diseconomies of scale?

As output increases, long run average cost rises

Can firms suffer from diminishing returns in the long run?

- No as diminishing returns only occurs in the short run, and firms can increase their plant size in the long run to prevent it

- However, they can still suffer from diseconomies of scale

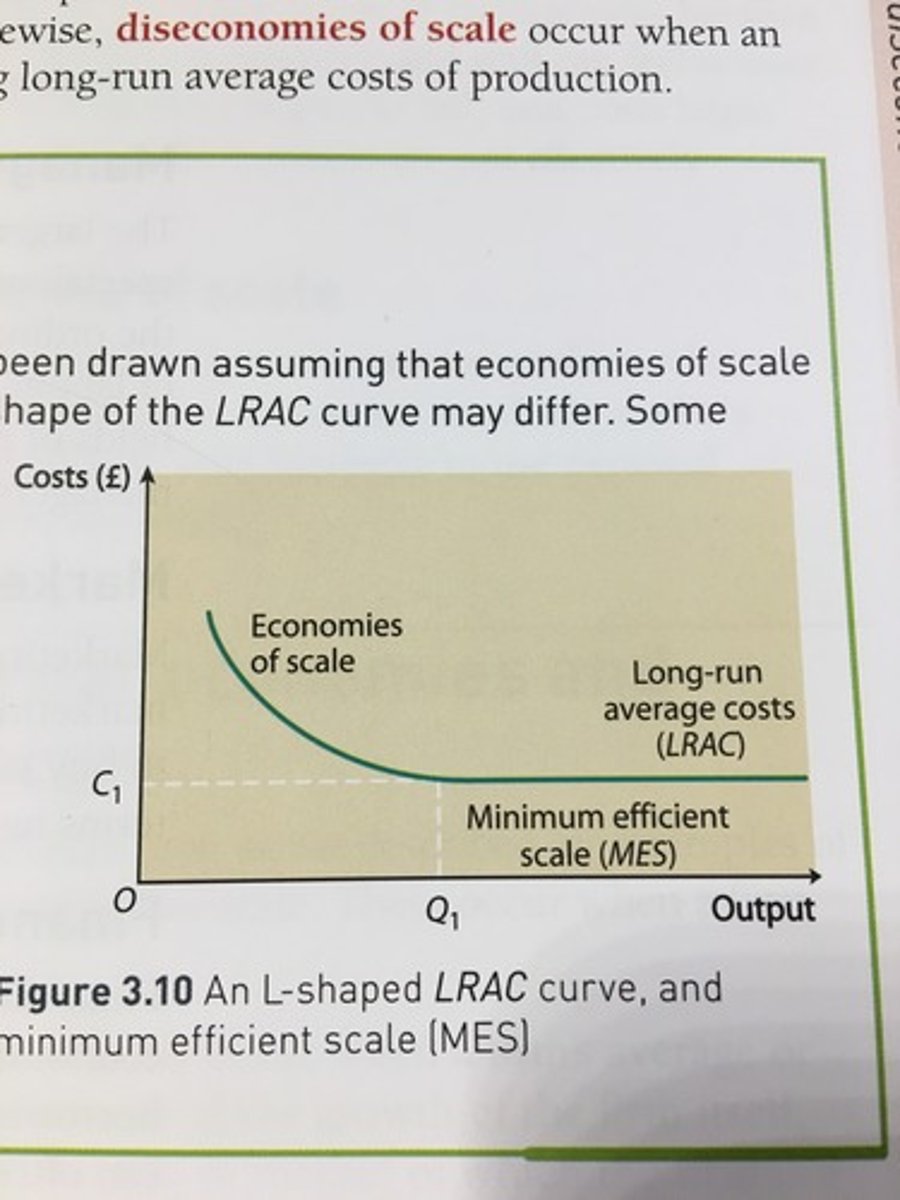

What is the L-shaped LRAC curve?

- It suggests that to begin with, as output increases, costs per unit falls due to the firm benefiting from economies of scale

- However, the curve stays constant instead of rising up again

- This is because even if there are diseconomies of scale such as if the marginal costs increase, they are cancelled out by economies of scale gained from technical or production factors

How does the minimum scale of production link to market structure?

- The MES relates to the lowest level of output needed to benefit from economies of scale, and no further economies of scale can be achieved beyond this.

- When MES is low, this allows a large number of firms to operate efficiently due to a low output needed, so there will be many firms

- However, if MES is high, this means economies of scale can only be achieved at a very high level of output, so only a few firms such as monopolies will enter the market

What does a horizontal LRAC curve mean

- There is a constant returns of scale, as there is just a straight line

What are examples of Economies of Scale?

- Risk bearing - Firms becoming richer means they can expand production to many different businesses which they can fall back on

- Managerial - Larger firms can specialise to employ specialist managers to help lower their average costs

- Technological - Larger firms can afford to invest in advanced and productive machinery to help lower their costs

- Purchasing - As a firm is growing in size, they can buy their raw materials in bulk, and as they buy more, they can negotiate unit discounts, so even though their costs increase, they increase at a slower rate than output

What are internal economies of scale?

- As a firm grows, costs are lowered

What are external economies of scale?

- As a firm's industry or market grows, costs are lowered

What are examples of external economies of scale?

- Cluster effect - When a large number of firms locate close to each other, the firms can benefit from each other

- Improvements in roads - Local roads may be improved, so transport costs for local industries will fall

What are examples of diseconomies of scale?

- Control - As a firm becomes larger, it becomes difficult to monitor how productive the workforce is

- Coordination - It's harder to coordinate with each worker when there are thousands of employees

- Communication - Workers may feel alienated and excluded as the firm begins to grow, which could lead to a fall in productivity as they lose motivation

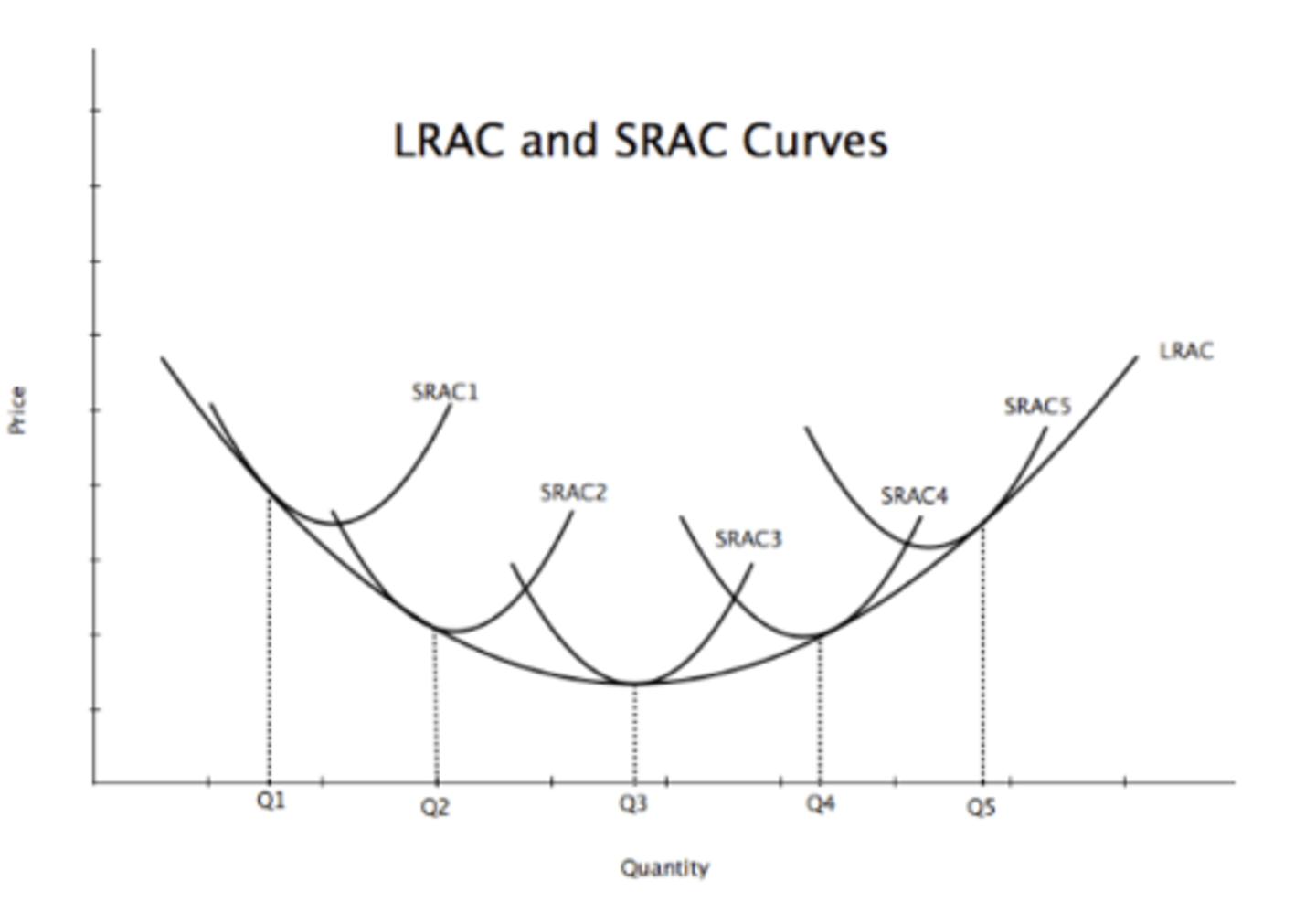

What is the relationship between long run average cost and short run average cost?

- In the long run, a firm can move from one short run cost to another, and each curve has a different scale of capacity fixed in the short run

- The LRAC curve shifts when there are external economies of scale

- The SRAC curve falls and then rises due to diminishing returns, but in the LRAC curve, costs change due to economies and diseconomies of scale

- If SRAC= LRAC, the firm can vary all factor inputs \

What is the optimum firm size?

- The size of the firm at the lowest point of the firm's LRAC curve, and this is productively efficient

What are the reasons for different shapes of the curves?

- There can be non-symmetrical shapes for the LRAC curve

- When the shape is like this, you can't identify a single optimum firm size

What is total revenue?

- The money a firm ends from selling the total output of a product

- Total revenue= price x quantity

What is average revenue?

- Total revenue/ quantity

- Average revenue just price and it's the firms demand curve, because as price increases, people are deterred from buying, so average revenue falls

What is marginal revenue?

- The addition to total revenue from selling an extra unit of output

- Marginal revenue= change in total revenue/ change in quantity

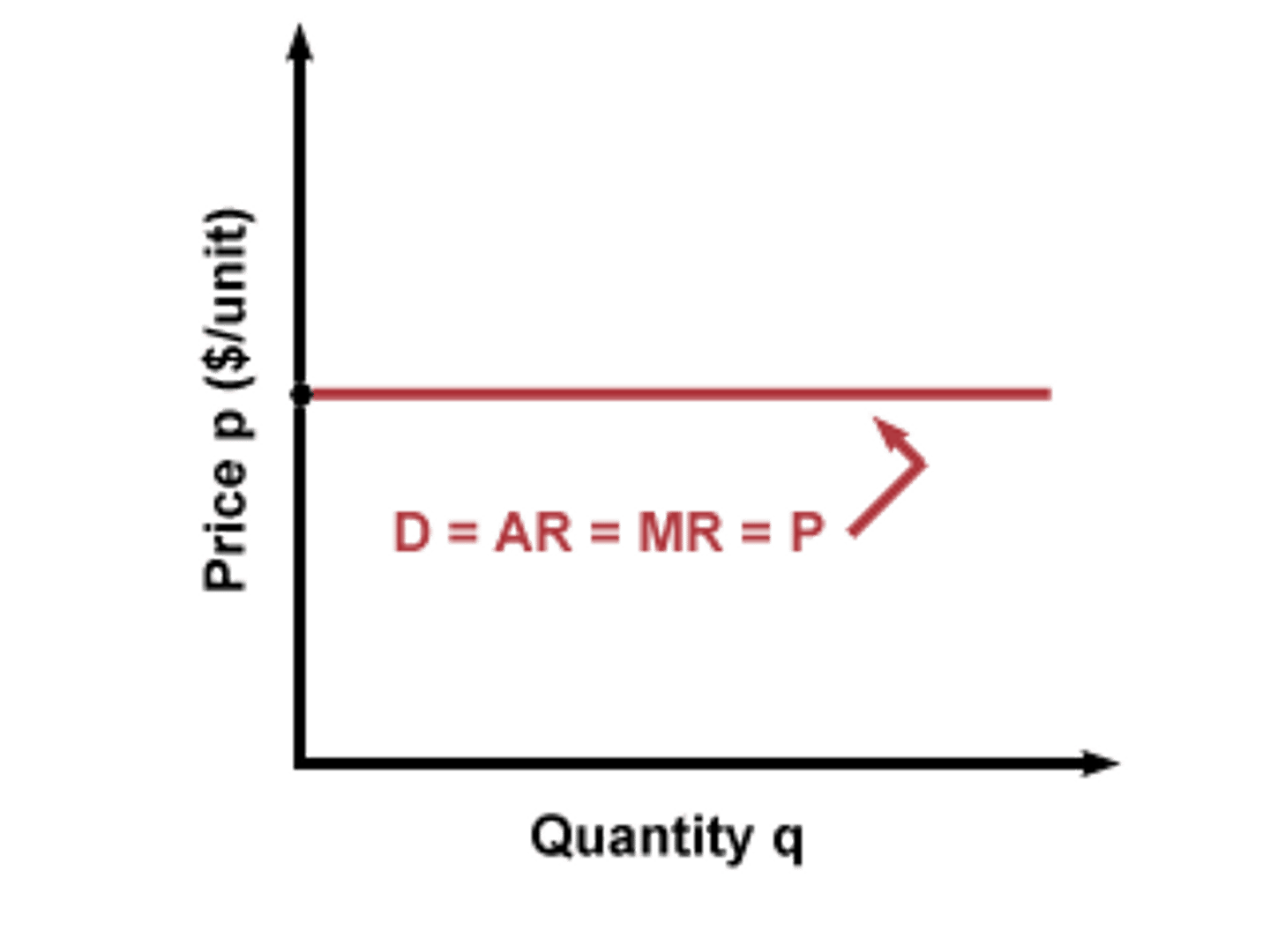

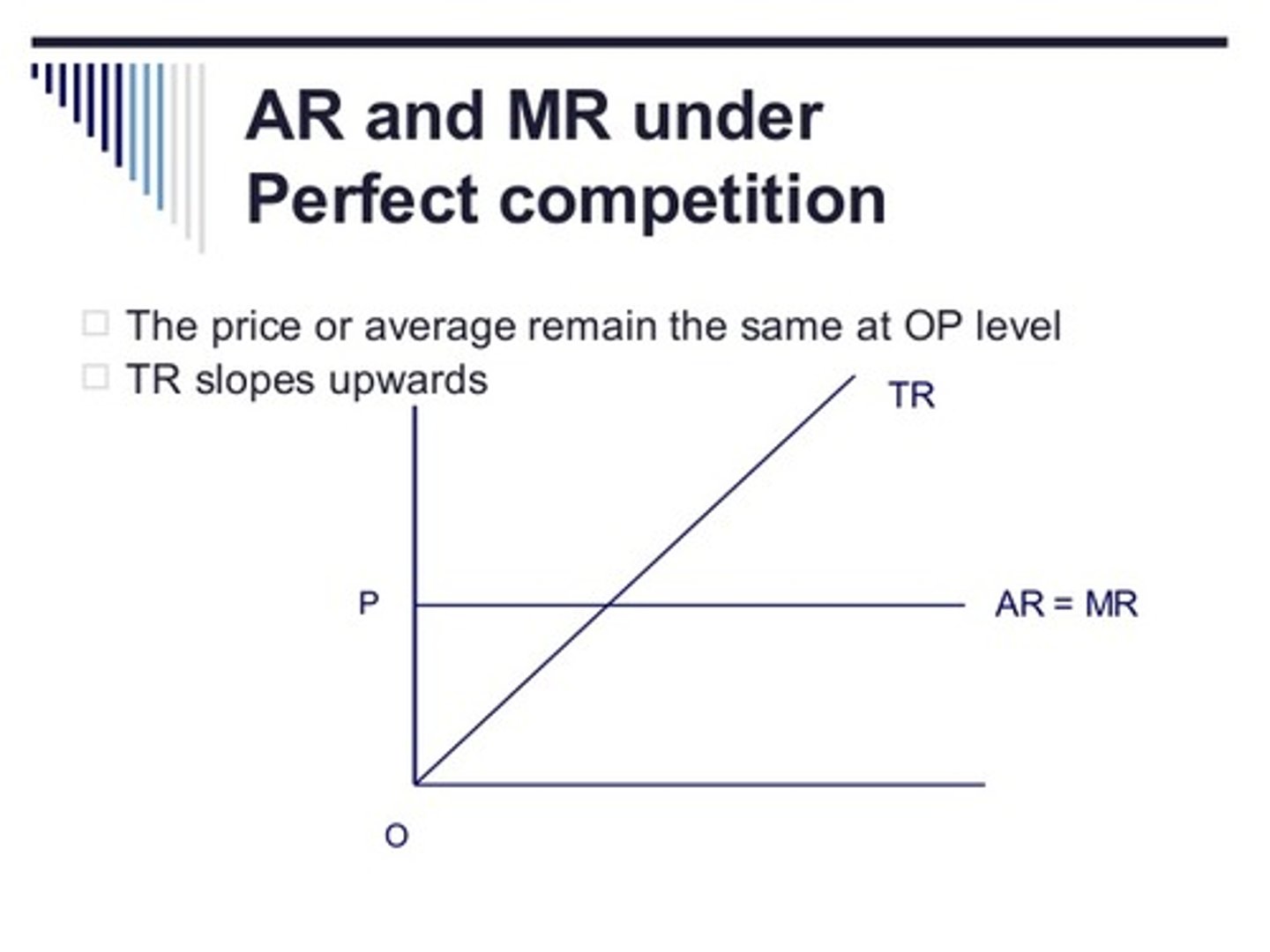

What is perfect competition?

- Involves a market structure with a large number of buyers and sellers

- They are the price takers as they don't have the ability to set their own prices, and they have no barriers to leave and enter the market. There is also perfect knowledge and information in the market

- Firms in perfect competition will always have to sell their units at the same price.

How are AR and MR in perfect competition?

- They are the same and they are both constant. - If you increase the price, less people will buy your product, but if you decrease the price, other firms will also lower their prices, so you won't make that much profit

How is TR in perfect competition?

- TR will be upward sloping, and increases by 1

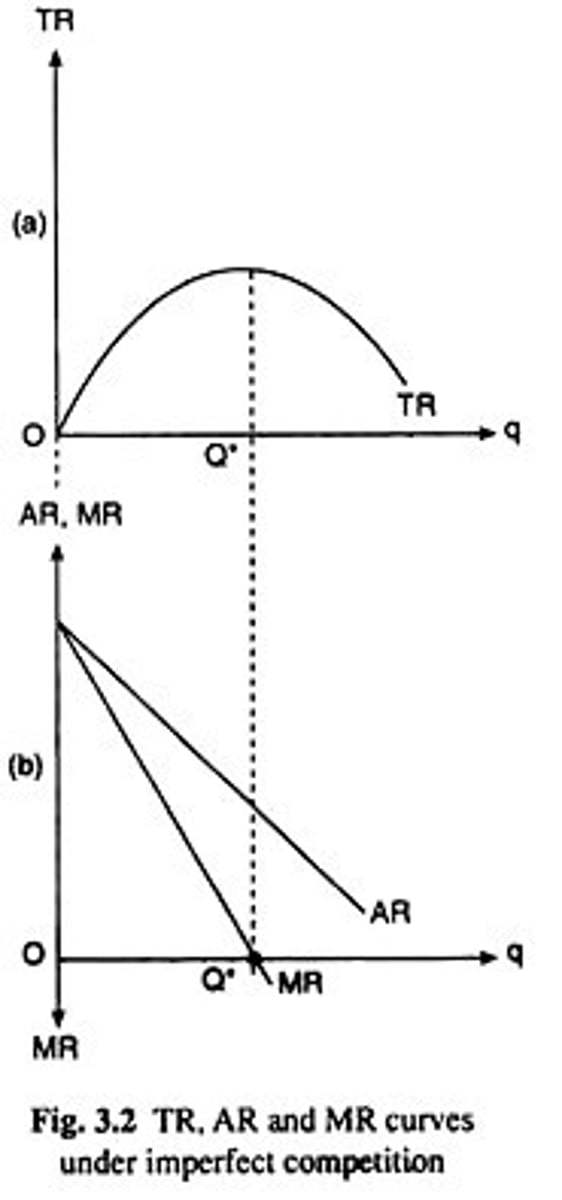

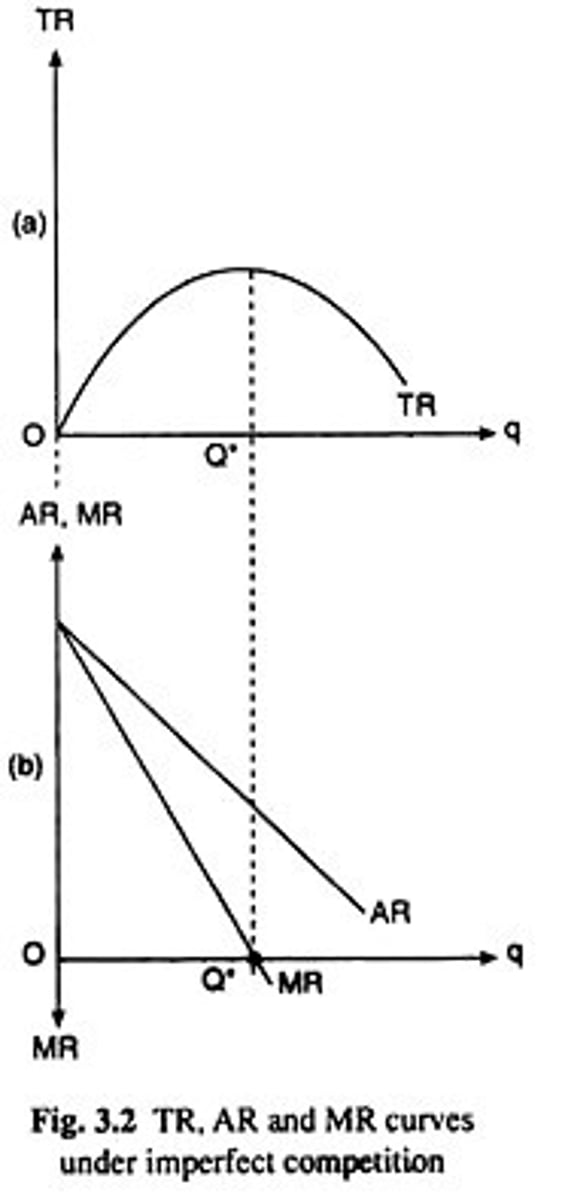

What is imperfect competition?

- Involves a market structure with few buyers and sellers

- The firms are the price makers as they have the ability to set their own prices, and there are high barriers to entry and exit

How are AR and MR in imperfect competition?

-In imperfect competition, average revenue and marginal revenue start high but then fall as quantity sold increase s

-AR is not equal to MR for any quantities greater than one.

-MR is twice as steep as AR, so it falls at a faster rate

How is TR in imperfect competition?

- TR rises, hits its peak when MR=0, and then falls

- This is because when MR=0, there is no more extra revenue to be gained, so TR is maximised

What are the functions of money?

- Medium of exchange

- Measure of value

- Method of delayed payment

Why is money a medium of exchange?

- Without money, transactions happened through bartering, where goods and services were traded with each other, but people didn't always get what they wanted

- Exchanges could only happen if there was a double coincidence of wants a party has what you want and you have what they want

Why is money a method of deferred payment?

- Money can allow for debts to be created, where people can pay for things without presently having money and they can pay it back later

Why is money a measure of value?

- Money is able to measure the relative values of goods and services, such as a piece of gold would be more valuable than a table

What is profit?

Total revenue - Total cost

What is normal profit?

- The minimum profit required to keep a firm in operation

- It covers the opportunity cost of investing funds into the firm and nowhere else

- This is where total revenue= total costs

What is supernormal profit?

- Profit above the normal level of profit

- These exceeds the value of the opportunity cost investing into the firm

- This is where total revenue> total costs

What is the role of profit in a market economy?

- Innovation - In a free market, profit is the reward entrepreneurs make when they take risks and invest. Entrepreneurs want to innovate so they can reduce their costs of production and improve the quantity and quality of their products, and this makes helps them maximise their profits

- Signals - Profits can also act as a signal to firms and consumers, as if there is a market where firms are making supernormal profits, new firms are more encouraged to enter it. This therefore increase the market supply and reduces the price

What is invention?

- Involves creating an entirely new product which didn't exist before

What is innovation?

- Involves improving or contributing to existing products

What is technology?

- Knowledge put to practical use to solve problems facing human societies

What is technological change?

- Describes the effect of invention, innovation and the spread of technology in the economy

What are the effects of technological change?

- Efficiency and productivity

- Development of new products and new markets can destroy existing markets

How can technological change improve efficiency and productivity?

- Improvements in efficiency and productivity can lower the costs of production which means quantity and quality of labour can improve

- For example, mobile phones have become cheaper to produce so more can be produced, while their quality has also improved

How can technological change lead to the development of new products?

- The development of DVDs blue rays and the rise of downloadable films has destroyed the market for VHS tapes

What is creative destruction?

- The belief put forward by Schumpeter which states as new firms become innovative and challenge existing firms, the more productive firms will then grow and the least productive firms are forced to leave the market

- This therefore expands the economy's productive potential

How can technological change influence the structure of the market?

- Monopolies don't have the incentives to be efficient as they have no competition, this means they are inefficient and their costs are higher than they should be

- Oligopolies have more incentives to innovate, as there as a small number of firms in the market and they try to get ahead of their competitors, so technological change is very fast