Microeconomics

1/114

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

115 Terms

Opportunity Cost

The value of the next best alternative

Marginal analysis

Comparing the benefits and costs of choosing a little more or a little less of a good

Law of diminishing marginal utility

As a person receives more of a good, the additional (or marginal) utility from each additional unit of the good declines

Sunk costs

costs that were incurred in the past and cannot be recovered, should not affect the current decision

Law of diminishing returns

As additional increments of resources are added to a certain purpose, the marginal benefit from those additional

increments will decline

Productive efficiency

when it is impossible to produce more of one good (or service) without decreasing the quantity produced of another good (or service)

Allocative efficiency

The particular mix of goods a society produces represents the combination that society most desires

comparative advantage

When a entity can produce a good at a lower opportunity cost than another entity.

budget constrain

all possible consumption combinations of goods that someone can afford, given the prices of goods, when all income is spent; the boundary of the opportunity set

opportunity set

all possible combinations of consumption that someone can afford given the prices of goods and the individual’s income

production possibilities frontier (PPF)

a diagram that shows the productively efficient combinations of two products that an economy can produce given the resources it has available

absolute advantage

producing a good over another entity using fewer resources to produce that good

Socialist Planned Economy

Allocation and ownership is planned by the government

Capitalism

Private allocation and ownership

Command Capitalism

allocation is planned by the government while ownership is private

Market Socialism

government planned ownership private allocation

Marginal analysis

examination of the associated costs and potential benefits of specific business activities or financial decisions

Incentives/disincentives

change the costs or benefits of a choice, therefore may alter the decision someone makes

demand

the relationship between price and the quantity demanded of a certain good or service (refers to the entire demand curve)

quantity demanded

The total number of units purchased at a price (refers to one point on a demand curve)

supply

the relationship between price and the quantity supplied of a certain good or service

law of supply

a higher price leads to a higher quantity supplied and a lower price leads to a lower quantity supplied

law of demand

a higher price leads to a lower quantity demanded and a lower price leads to a higher quantity demanded

equilibrium

The point where the supply curve (S) and the demand curve (D) cross

equilibrium price and quantity

the amount of the product consumers want to buy (quantity demanded) is equal to the amount producers want to sell (quantity supplied) at that price

surplus/excess supply

the quantity supplied exceeds the quantity demanded (all above equilibrium prices)

shortage/excess demand

at the existing price, the quantity demanded exceeds the quantity supplied

ceteris paribus

The assumption behind a demand curve or a supply curve is that no relevant economic factors, other than the product’s price, are changing

normal good

A product whose demand rises when income rises, and vice versa

inferior good

A product whose demand falls when income rises, and vice versa

substitute

good or service that can be used in place of another good or service

complements

the goods are often used together, because consumption of one good tends to enhance consumption of the other

shift in supply

a change in the quantity supplied at every price

Price controls

Laws that government enacts to regulate prices

price ceiling

keeps a price from rising above a certain level

price floor

keeps a price from falling below a certain level

consumer surplus

The amount that individuals would have been willing to pay, minus the amount that they actually paid

producer surplus

the amount that a seller is paid for a good minus the seller’s actual cost

social/total/economic surplus

the sum of consumer surplus and producer surplus

deadweight loss

The loss in social surplus that occurs when the economy produces at an inefficient quantity

Elasticity

an economics concept that measures responsiveness of one variable to changes in another variable

Price elasticity

the ratio between the percentage change in the quantity demanded (Qd) or supplied (Qs) and the corresponding percent change in price

price elasticity of demand

the percentage change in the quantity demanded of a good or service divided by the percentage change in the price

price elasticity of supply

the percentage change in quantity supplied divided by the percentage change in price

Zero elasticity/perfect inelasticity

the extreme case in which a percentage change in price, no matter how large, results in zero change in quantity

tax incidence

The analysis, or manner, of how the burden of a tax is divided between consumers and producers

cross-price elasticity of demand

the idea that the price of one good is affecting the quantity demanded of a different good

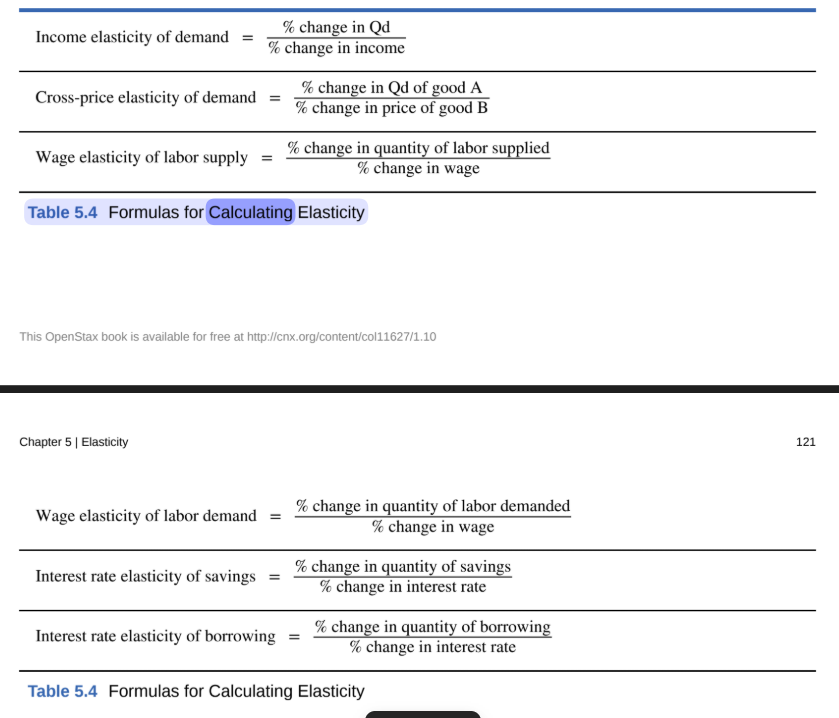

Elasticity of labor supply

% change in quantity of labor supplied / % change in wage

elasticity of savings

the percentage change in the quantity of savings divided by the percentage change in interest rates

Formulas for calculating elasticity

increasing the price of inelastic goods

increases total revenue

increasing the price of elastic goods

decreases total revenue

Marginal Utility formula

change in total utility / change in quantity

total utility

satisfaction derived from consumer choices

marginal utility per dollar formula

marginal utility / price

maximizing utility formula

MU1 / P1 = PU2 / P2

consumer equilibrium

hen the price of good 1 is divided by the price of good 2, at the utility-maximizing point this will equal the marginal utility of good 1 divided by the marginal utility of good 2 (P1 / P2 = MU1 / MU2)

substitution effect

occurs when a price changes and consumers have an incentive to consume less of the good with a relatively higher price and more of the good with a relatively lower price

income effect

is that a higher price means, in effect, the buying power of income has been reduced, which leads to buying less of the good (when the good is normal).

backward-bending supply curve for labor

the situation of high-wage people who can earn so much that they respond to a still-higher wage by working fewer hours

behavioral economics

seeks to enrich the understanding of decision-making by integrating the insights of psychology into economics

fungible

units of good eg.dollars have equal value to the individual, regardless of the situation

firm (or business)

combines inputs of labor, capital, land, and raw or finished component materials to produce outputs.

production

goes beyond manufacturing (i.e., making things). It includes any process or service that creates value, including transportation, distribution, wholesale and retail sales

Explicit costs

out-of-pocket costs, that is, payments that are actually made

Implicit costs

represent the opportunity cost of using resources already owned by the firm

Accounting profit

a cash concept. It means total revenue minus explicit costs—the difference between dollars brought in and dollars paid out

Economic profit

total revenue minus total cost, including both explicit and implicit costs.

total cost

the sum of fixed and variable costs of production

Fixed costs

expenditures that do not change regardless of the level of production, at least not in the short term.

Variable costs

incurred in the act of producing—the more you produce, the greater the variable cost.

Average total cost

total cost divided by the quantity of output.

Average variable cost

obtained when variable cost is divided by quantity of output

Marginal cost

the additional cost of producing one more unit of output

average profit

divide profit by the quantity of output produced we get

long-run average cost curve

shows the lowest possible average cost of production, allowing all the inputs to production to vary so that the firm is choosing its production technology

short-run average cost curves

the average total cost curve in the short term; shows the total of the average fixed costs and the average variable costs

constant returns to scale

allowing all inputs to expand does not much change the average cost of production

economies of scale

refers to the situation where, as the quantity of output goes up, the cost per unit goes down

diseconomies of scale

the long-run average cost of producing each individual unit increases as total output increases

Marginal Cost Formula

TC2-TC1 / Q2-Q1

Point where profits are maximized with amount of goods produced

when marginal revenue = marginal cost

market structure

the conditions in an industry, such as number of sellers, how easy or difficult it is for a new firm to enter, and the type of products that are sold

entry

the long-run process of firms entering an industry in response to industry profits

marginal revenue

the additional revenue gained from selling one more unit

perfect competition

each firm faces many competitors that sell identical products

price taker

a firm in a perfectly competitive market that must take the prevailing market price as given

shutdown point

level of output where the marginal cost curve intersects the average variable cost curve at the minimum point of AVC; if the price is below this point, the firm should shut down immediately

allocative efficency

producing the optimal quantity of some output; the quantity where the marginal benefit to society of one more unit just equals the marginal cost (P=MC)

barriers to entry

the legal, technological, or market forces that may discourage or prevent potential competitors from entering a market

deregulation

removing government controls over setting prices and quantities in certain industries

legal monopoly

legal prohibitions against competition, such as regulated monopolies and intellectual property protection

marginal profit

profit of one more unit of output, computed as marginal revenue minus marginal cost

monopoly

a situation in which one firm produces all of the output in a market

natural monopoly

economic conditions in the industry, for example, economies of scale or control of a critical resource, that limit effective competition

predatory pricing

when an existing firm uses sharp but temporary price cuts to discourage new competition

trade secrets

methods of production kept secret by the producing firm

cartel

a group of firms that collude to produce the monopoly output and sell at the monopoly price

collusion

when firms act together to reduce output and keep prices high

differentiated product

a product that is perceived by consumers as distinctive in some way