Chapter 5: Elasticity, Taxation, and Consumer Choice (Micro)

1/42

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

43 Terms

What does elasticity show?

It shows how responsive consumers and producers are to changes in price.

Deadweight loss

When a market FAILS to produce an optimal output.

Elasticity of DEMAND

Measures how CONSUMERS respond to changes in price.

→ When demand is inelastic, consumers are insensitive to changes in price, meaning the change in quantity demanded is small.

→ With elastic demand, a price change leads to a LARGE change in quantity demanded relative to the price change.

Calculating price elasticity of demand.

→ ignore negatives, use absolute values FOR ANSWER!

Price Elasticity of Demand (ED) = %Change in quantity demanded(QD) / % Change in price (P)

—> % change in (QD) or P = Change in P or QD/ Initial P or QD

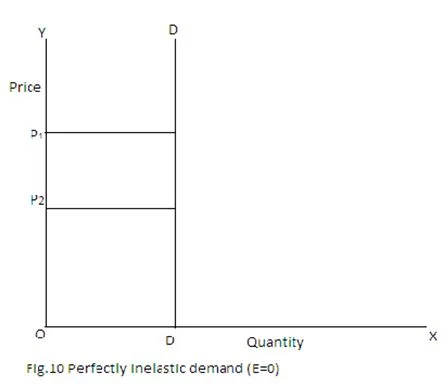

Perfectly inelastic

=0

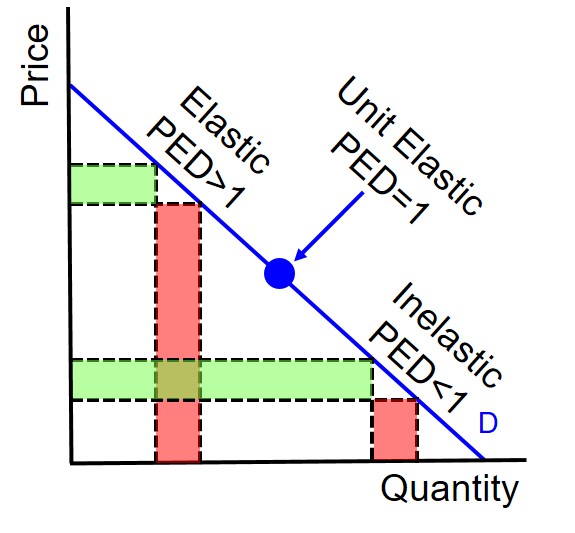

Relatively Inelastic

<1

Unit elastic

=1

Relatively elastic

>1

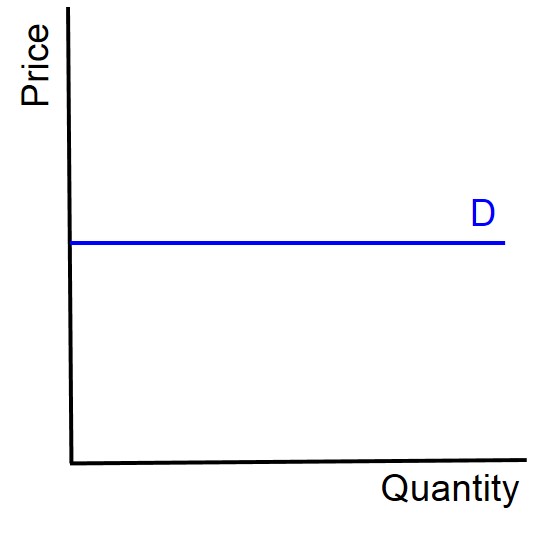

Perfectly elastic

∞

Total Revenue

Amount of money received from sales of a product.

Total revenue formula

Price x Quantity = Total Revenue

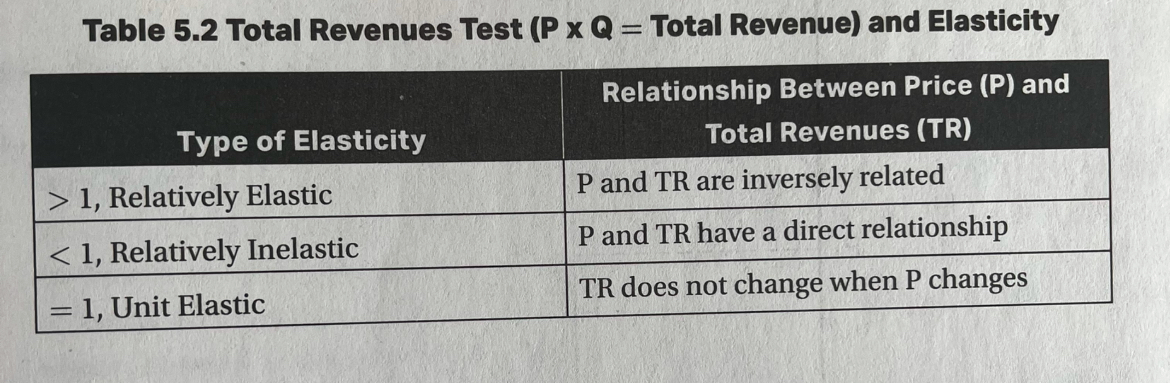

Total revenues test to determine elasticity

If price increases and total revenue decreases, elasticity of demand is relatively elastic. If price increases and total revenue also increases, elasticity of demand is relatively inelastic, and if price changes and total revenue remains the same, elasticity of demand is unit elastic.

Perfect Elasticity

If demand is perfectly elastic, the price elasticity of demand is infinity. As price changes, the change in quantity demanded is infinite. AT ANY PRICE ABOVE D, QUANTITY DEMANDED IS 0, AT ANY PRICE BELOW, QUANTITY DEMANDED IS INFINITE.

Perfectly Inelastic

A "perfectly inelastic demand curve" represents a situation in economics where the quantity demanded of a good remains completely unchanged regardless of any price fluctuation, meaning consumers will buy the same amount of a product no matter how high or low the price is, and is visually depicted as a vertical line on a graph; essentially, price has no impact on the quantity demanded. QUANTITY DEMANDED REMAINS UNCHANGED.

Elasticity along a demand curve.

On a downsloping linear demand curve, price elasticity of demand VARIES along the curve. Midpoint of the curve is unit elastic.

Price and elastcitiy

As price decreases in the elastic range, total revenue increases, as price decreases in inelastic range, total revenue FALLS.

Three questions to DETERMINE demand elasticity

Are there adequate substitutes available, or is the good a necessity? → If a good is a NECESITY with no good substitutes, the consumer is likely to purchase the same quantity even if there are price changes (inelastic). Example: Insulin/medicine/gasoline

Can the purchase be DELAYED? → If consumers have a longer time to make a buying decision, the demand for a certain product may be more elastic. IF the purchase cant be delayed, its more inelastic. Emergency medical care is inelastic demand.

Does the purchase require a large percentage of INCOME? → If a good is a large part of one’s budget, the good tends to be more price elastic. If s luxury boat price increases by 10%, it can be SEVERAL thousands of dollars. Leading to less in quantity demanded. However, if price of salt goes up 10%, its a smaller percentage from income so its more INELASTIC.

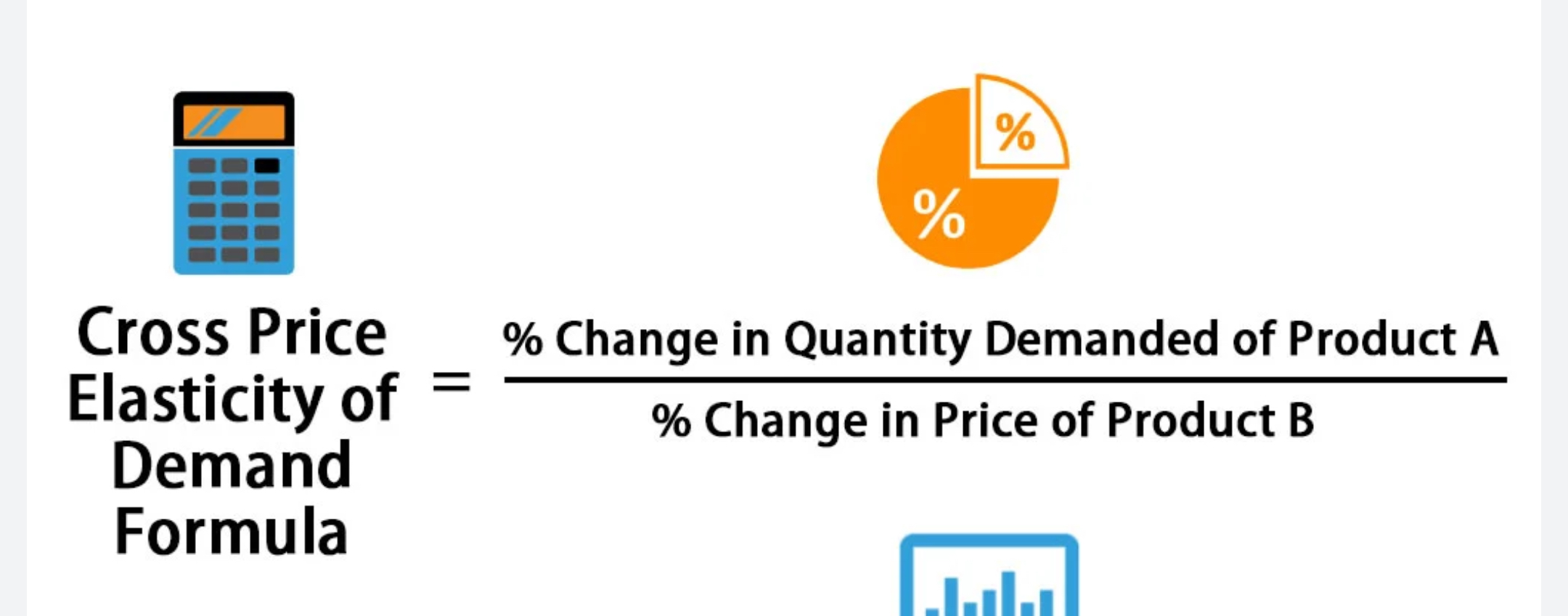

Cross Price Elasticity of Demand (CPED)

Measures how a price change in one product affects the quantity demanded of another product. If it’s a positive value, the two goods are substitutes, if it’s a negative value, they are complements .

Cross price elasticity of demand equation

Substitute vs complement

A "substitute good" can be used in place of another good to fulfill the same need, while a "complementary good" is a good that is used alongside another good to enhance its value, meaning they are typically consumed together; essentially, substitutes can replace each other, while complements are used together to create a more complete experience.

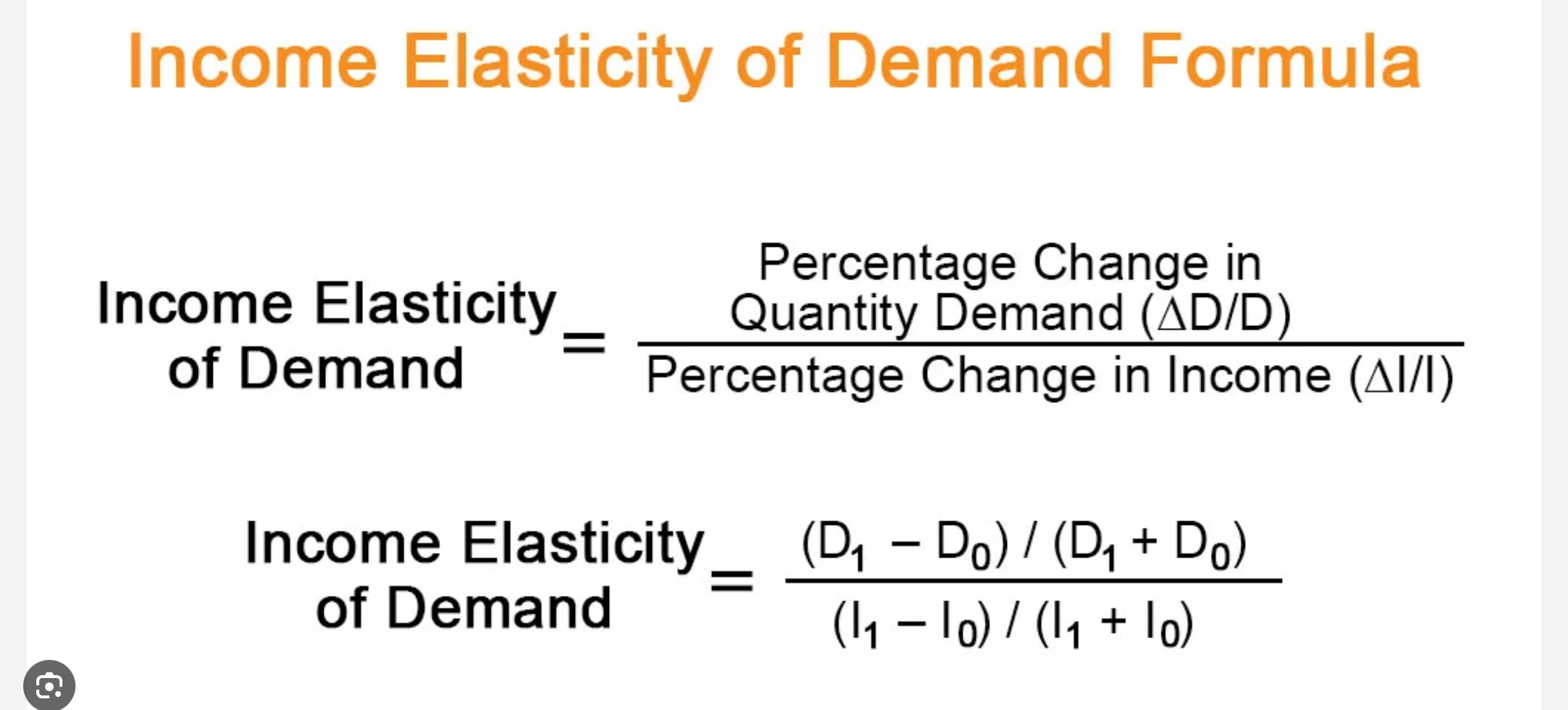

Income Elasticity of Demand

Since purchasing decisions are constrained by budgets, consumers sensitivity in terms of their responses to changes in both prices and incomes.

Income Elasticity of Demand Formula

This formula shows wether the good is inferior or normal. Ratio for normal goods is positive, inferior is negative.

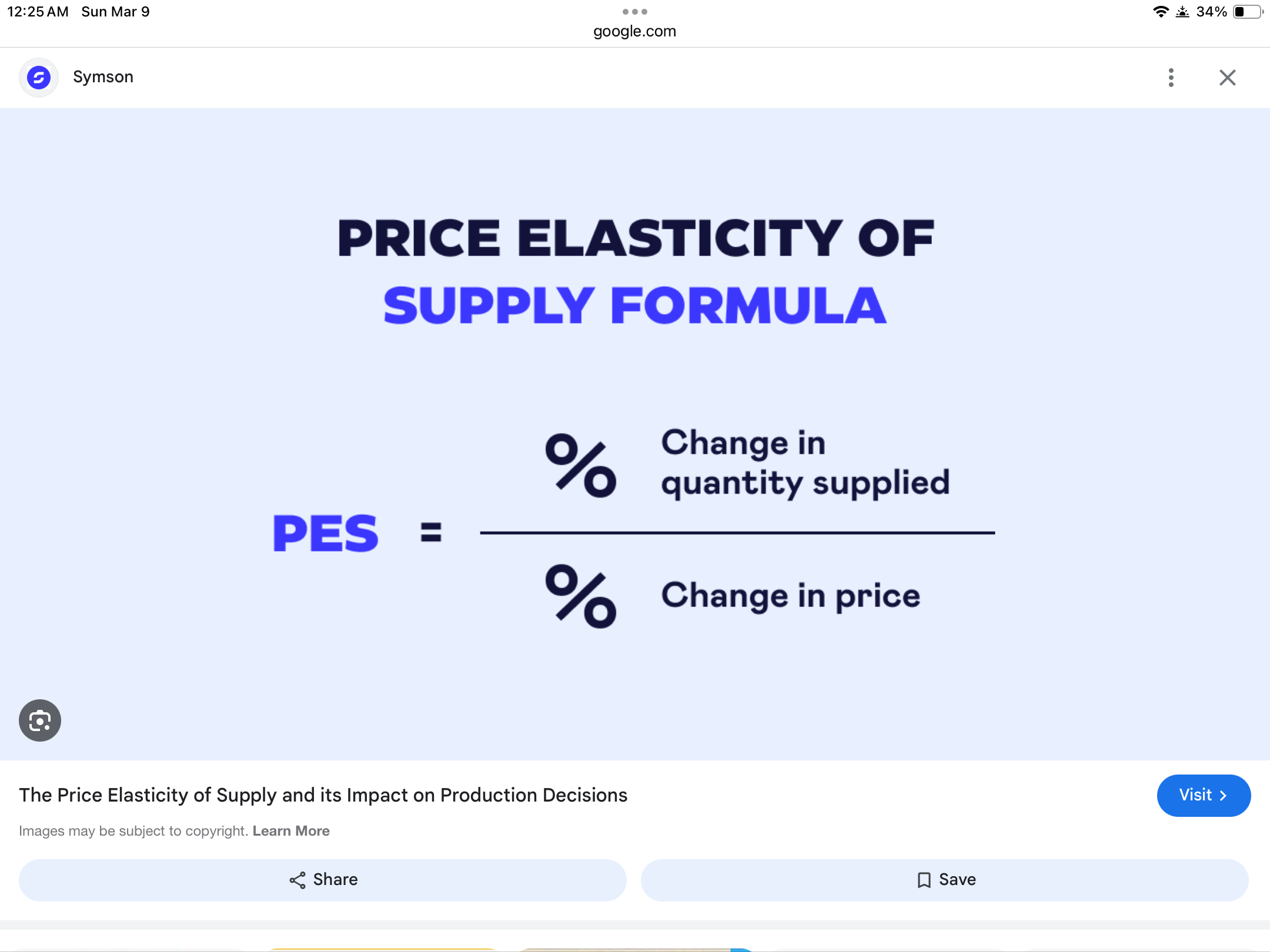

Price elasticity of supply

Price elasticity of supply considers how a change in price affects the quantity supplied.

Price Elasticity of Supply

Consumer surplus

Difference between the highest price a customer would pay and the actual price paid.

Producer surplus

Difference between the lowest price a producer would sell the product for vs the actual price received

Consumer surplus formula

Consumer Surplus = 1/2(Maximum price willing to pay - Actual price) × Quantity purchased

Producer surplus formula

Producer Surplus = 1/2(Market Price - Minimum Price Willing to Accept)* quantity sold

Price Ceiling

Maximum Legal Price that can be charged for a product or service. a binding price ceiling is placed BELOW the equilibrium price.

Price Floor

Minimum legal price that can be charged for a product or service. A binding price floor is set above equilibrium price.

Deadweight loss

Loss of total surplus when a market fails to reach a competitive equilibrium.

Deadweight loss with a price floor

A "deadweight loss" with a price floor refers to the economic inefficiency that occurs when a government-imposed minimum price (price floor) is set above the market equilibrium price, leading to a surplus of goods and a reduction in the total quantity traded, resulting in a loss of potential economic welfare for both consumers and producers; essentially, some potential transactions that would have happened at a lower price are lost due to the price floor being too high.

Impact of taxes on consumer and producer surpluses

Taxation results in a reduction of total surplus, which is a dead weight loss.

Excise Tax

A per unit tax on the production or sale of a good.

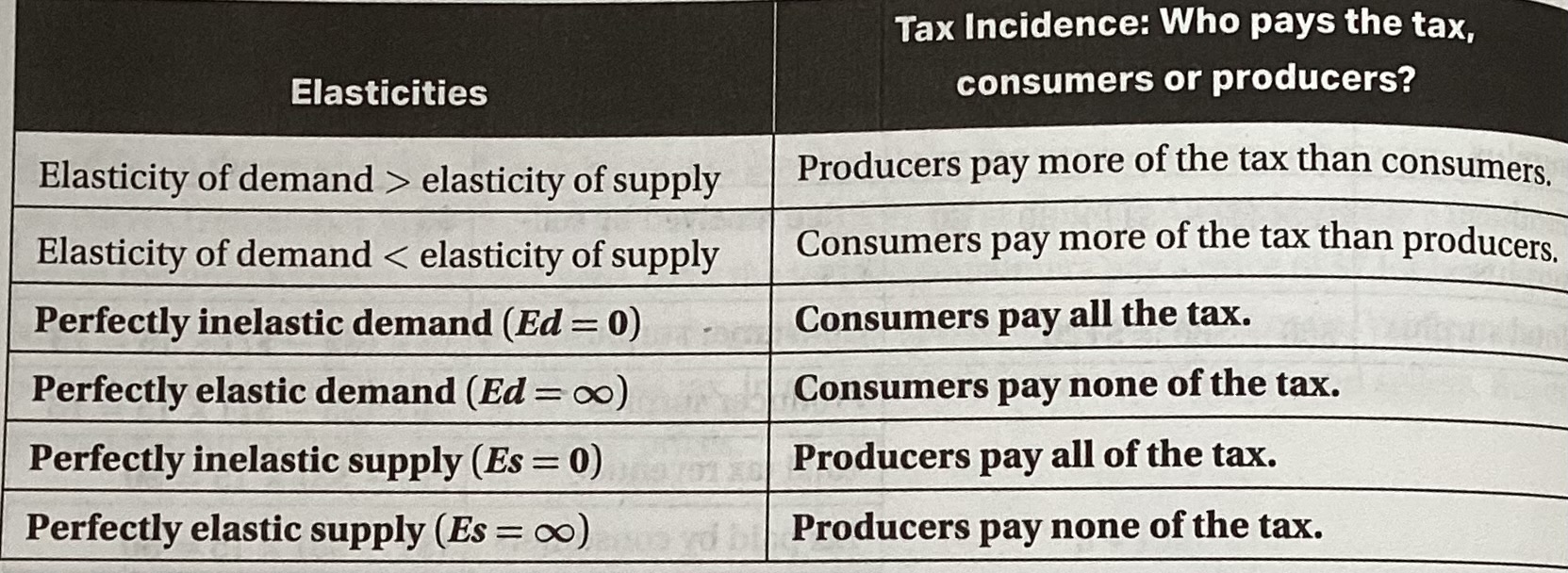

Tax incidence

All taxes create..

A deadweight loss

Consumer Choice Theory

How a consumer allocates a limited income among a wide variety of choices.

Utility

Making rational decisions to expect that the benefits of the purchase outweigh the costs.

Diminishing Marginal Utility

As you consume a good or service , each additional unit consumed yeilds a decreasing additional amount of satisfaction or utility.

Total utility

total utility amount of satisfaction or utility a person receives from the consumption of a good or service .

Marginal utility

Extra amount of satisfaction or utility from consuming one more unit of a good or service.

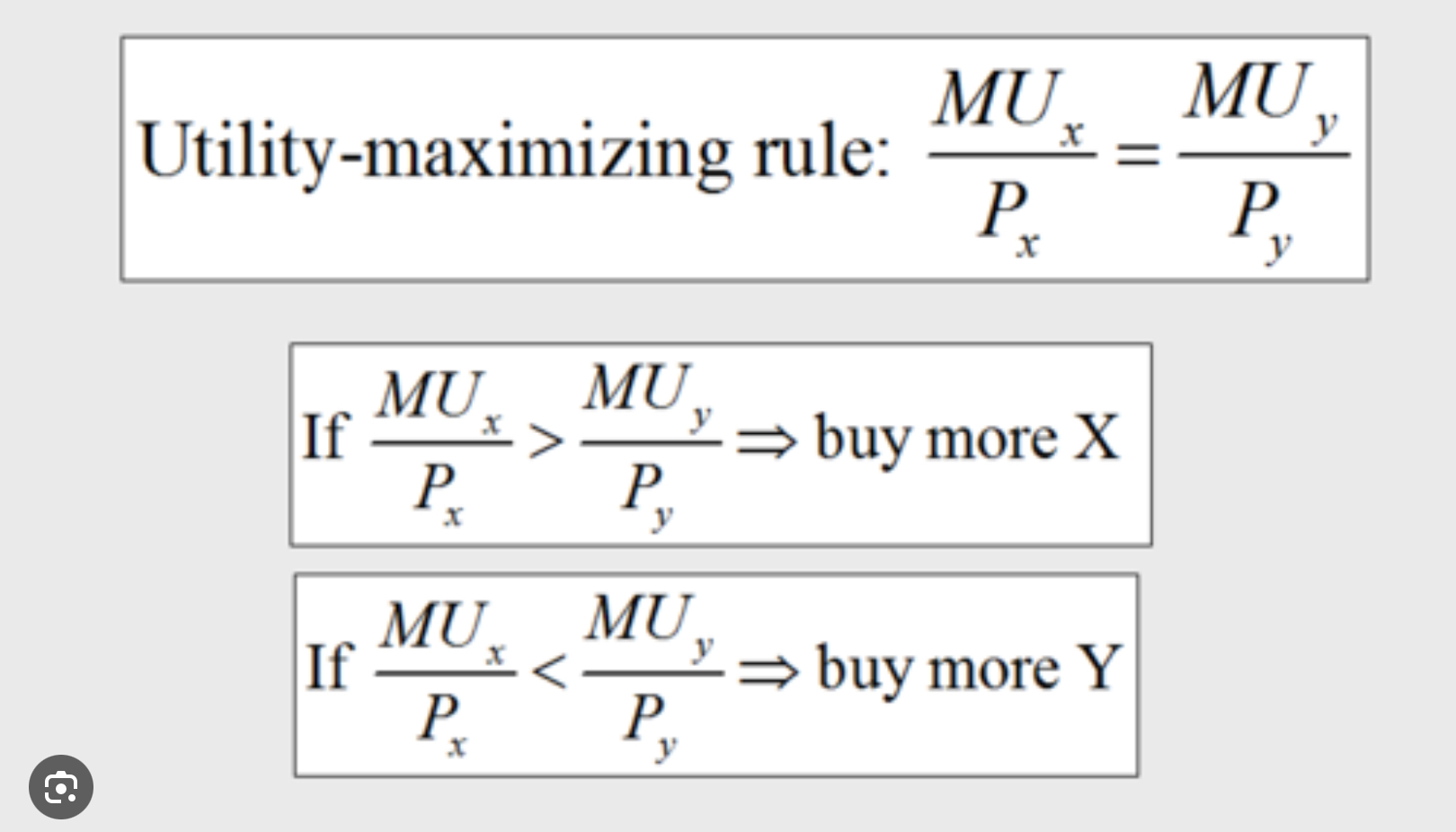

The utility maximization rule

A consumer maximize utility when the marginal utility per dollar spent for all items is equal given budget constraints. If the marginal utility per dollar is not equal consumers will want to begin by buying the product with the highest marginal utility per dollar and spending less on the product with a lower marginal utility per dollar.

Negative income elasticity means a product is

Inferior