A100 Final IU

1/63

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

64 Terms

Financial Accounting Report

Periodic financial statements and related disclosures

Managerial Accounting Report

Detailed plans and continuous performance reports

External Decision Makers

Evaluate the Company (creditors, investors)

Internal Decision Makers

Run the company (managers)

Accounting

The recording of business transactions, the preparation of reports summarizing these transactions, and the analysis of financial information

Capital Markets

All investors and creditors that provide funds to the business to operate and grow

Accounting Equation

Assets= Liabilities(outsider claim to assets) + Stockholders' Equity(insider claim to assets)

Business Activities Categories

Operating, Investing, Financing

Operating Activities

Everyday business transactions (including interest expense, dividend revenue)

Investing Activities

Transactions involving long term assets and investments

Financing Activities

Transactions involving long-term liabilities, stock, and dividend payments

Equity Investors

Contributions from Owners (for a corporation = stockholders) Earnings retained from profitable business operations (Retained Earnings).

Debt Investors

Creditors of the business, such as a bank, bondholders, leasing companies

Reported as current "liabilities" or "long-term liabilities" on the financial statements

Financial Leverage

Using borrowed money (debt) to increase the potential return on an investment.

By borrowing money, you can invest more than you could with just your own funds. If the investment does well, you earn more profit than you would have without borrowing

Legal Rights of Stockholders

Those contributing funds to the company are awarded share of ownership (shareholders).

Shareholders have voting rights on significant corporate matters.

Shareholders share in the company's profits and losses.

Risks to Stockholders

Stockholders face the risk of not receiving a satisfactory return on their investment.

Sometimes investors can lose some or all of the investment if the business fails.

Stockholders may expect dividend payments that are taxable income.

Benefits to Stockholders

Stockholders may enjoy increases in market value of their shares.

Stockholders may enjoy dividends if awarded by the Board of Directors

Benefits to the Company of Equity Financing

No obligation to repay.

The company doesn't have to pay dividends unless the BOD declares them.

More investors share in the risk of the project

Risks to Company of Equity Financing

Owners give up portions of their company to shareholders (who probably have opinions)

Company's may feel pressure to share profits through dividend payments instead of reinvesting in the company

Dividends are NOT tax deductible and are NOT expenses on the Income Statement

Legal Rights of Debt Investors

Both interest (tax deductible) and principal must be paid to the investor.

If the company does not make payments, the debt investor has legal recourse to "call" the loan and demand payment.

Creditors have a higher claim on the company's assets in bankruptcy over stockholder's.

Risks to Debt Investors

Payments will not be made on time.

Sometimes companies have to liquidate assets to make payments.

Liquidating assets may cause the company to file for bankruptcy.

Interest rate risk (if interest rates rise the value of existing fixed rate loans decrease on the creditor's Balance Sheet.)

Benefits to Debt Investors

Creditors receive regular interest payments (taxable revenue).

Creditors often secure loans with collateral in the even of non-payment.

Creditors can enforce loan covenants (restrictions to limit the company's financial activities and manage risk).

Benefits to the Company of Debt Financing

The owners retain full ownership.

Once the loan in paid in full, the relationship is over.

The company can budget exactly how much payments (principal and interest) will be.

Potential for higher rate of return (goal is to earn a higher return than that of the borrowed funds- net is retained by the company

Risks to the Company of Debt Financing

A company has to bay it back....plus interest! Even if the investment fails.

These payments could put a company in a cash flow crunch..

A company may need to sell their assets to make loan payments.

Financial Reporting Objectives

Provide specific information about economic resources, claims to those resources, and changes to resources and claims

Provide information useful in understanding a company's cash flows. This includes assessing the amount, timing of cash flows, and uncertainty of future cash flows.

Provide general information to help make investment and credit decisions

Securities & Exchange Commission (SEC)

Established in 1934

Only applies to public companies

Requires public companies to file reports of company activity

SEC required reports

Form 10-K (annually)

Form 10-Q (quarterly)

Annual financial statements audited by an "independent auditor"

Generally Accepted Accounting Principles (GAAP)

The accounting standards that companies based in the United States are required to use.

Standards give the statements credibility and allow reports of different companies to be compared

Financial Accounting Standards Board (FASB)

The organization that determines the GAAP

Independent Auditor

Also called an "external auditor", is an accounting firm that specializes in "public accounting"

Public Accounting

The company is in business to provide accounting services to

other companies. The external auditors performing the audit must be independent of the company they are auditing

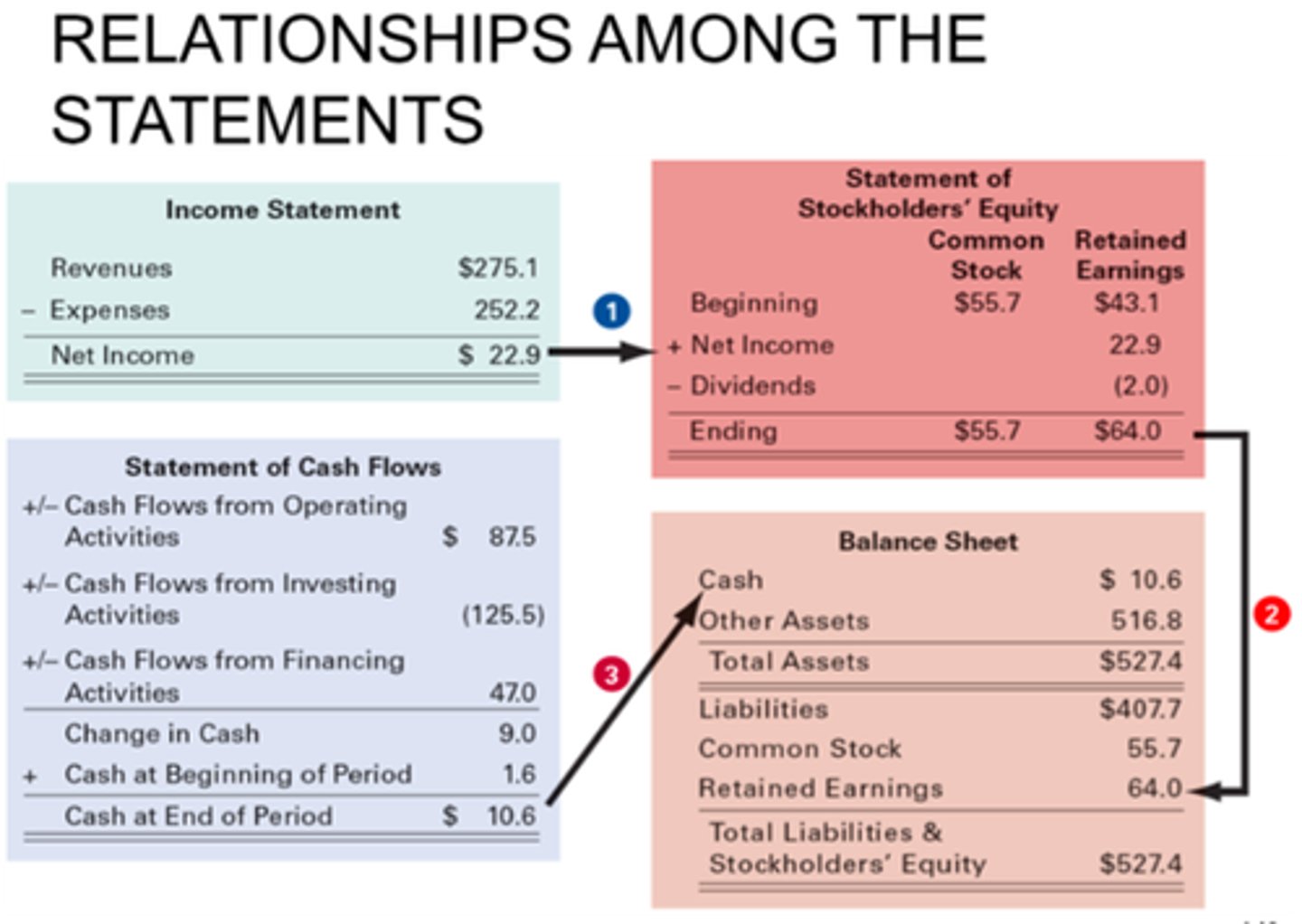

Financial Statements

Balance Sheet

Income Statement

Statement of Retained Earnings/Stockholder's Equity

Statement of Cash Flows

Notes to the Financial Statements

Can be prepared anytime.

Are the responsibility of the company's management

Income Statement

Revenue

- Cost of goods sold

= Gross profit

- Operating expenses

= Net income from operations

+/- Gain or loss on sale of other assets

= Net income (Net Loss)

Statement of Retained Earnings

Beginning retained earnings

+ Net income (or - Net Loss)

- Dividends paid

Ending retained earnings

Balance Sheet

Assets = Liabilities + Stockholder's Equity

Statement of Cash Flows

Beginning cash

+/- Cash flows from operations

+/- Cash flows from investing

+/- Cash flows from financing

= Ending cash

Relationship between the financial statements

Accrual Basis (GAAP)

Records transactions in the period in which the events occurred, not when cash changes hands.

Cash Basis (Not GAAP)

Records transactions in the period in which cash changes hands, not when they occurred.

Matching Principle

Expenses are matched in the same period in which they contribute to the revenue earned

Accounts Payable (Liability)

If goods or services are provided before cash changes hands, then the company has expenses (on income statement) increase

Accounts Receivable (Asset)

If goods are services are provided before cash changes hands, then the company has an increase in revenue (on income statement)

Unearned Revenue (Liability on balance sheet)

When cash is received and before goods are services are provided, cash increases, but there is no revenue until the transaction occurs

Prepaid Expenses (Asset on balance sheet)

When cash is paid before goods are services are provided. Cash decreases, but the expense is not recorded until the transaction occurs.

Revenue Recognition

Record revenue when EARNED (when service is performed, when product is delivered), not when cash is received

Expense Recognition

Record expense when INCURRED (USED), not when cash is paid

Audit

An independent professional service that improves the quality of information for decision makers

Auditors

They objectively collect and evaluate evidence.

They have to be independent (unbiased/objective).

Make sure the F.S. are prepared in accordance with GAAP = with no material misstatements

Provide their opinion in an audit report to users (investors)

Principal-Agent Relationship

There is a conflict in priorities between the owner of an asset and the person to whom control of the asset has been delegated

Audit Opinion

Provides reasonable assurance about whether the financial statements are fairly stated in accordance with GAAP in all material respects

Audit Risk

The risk the auditor gives a clean opinion on financial statements that are materially misstated

Clean Audit Opinion

Indicates that all matters have been satisfactorily addressed

Tax Reporting

Cash-based with more advisory / consulting / planning

Major Sources of Tax Revenue

Local Tax, State Tax, Federal Tax

Local Tax

County, city, real estate (property) Ex: Education

Property Tax

Real Estate - Based on assessed (by the government) value of Real Estate

State Tax

Sales tax, income tax, C Corp. Business Income Tax. Ex: State parks

C Corp. business income tax

Only a small amount of tax collected; not a major source of taxes

Federal Tax

Individual Income Tax, C Corp. Business income tax, Federal Payroll Tax, Self-employment tax. Ex: Social Security and Medicare

Individual Income Tax

Income - Deductions = Taxable Income

Passthrough Entities

Does NOT file its own Federal Income Tax Return. Ex: Limited Liability Company (LLC), Partnership,

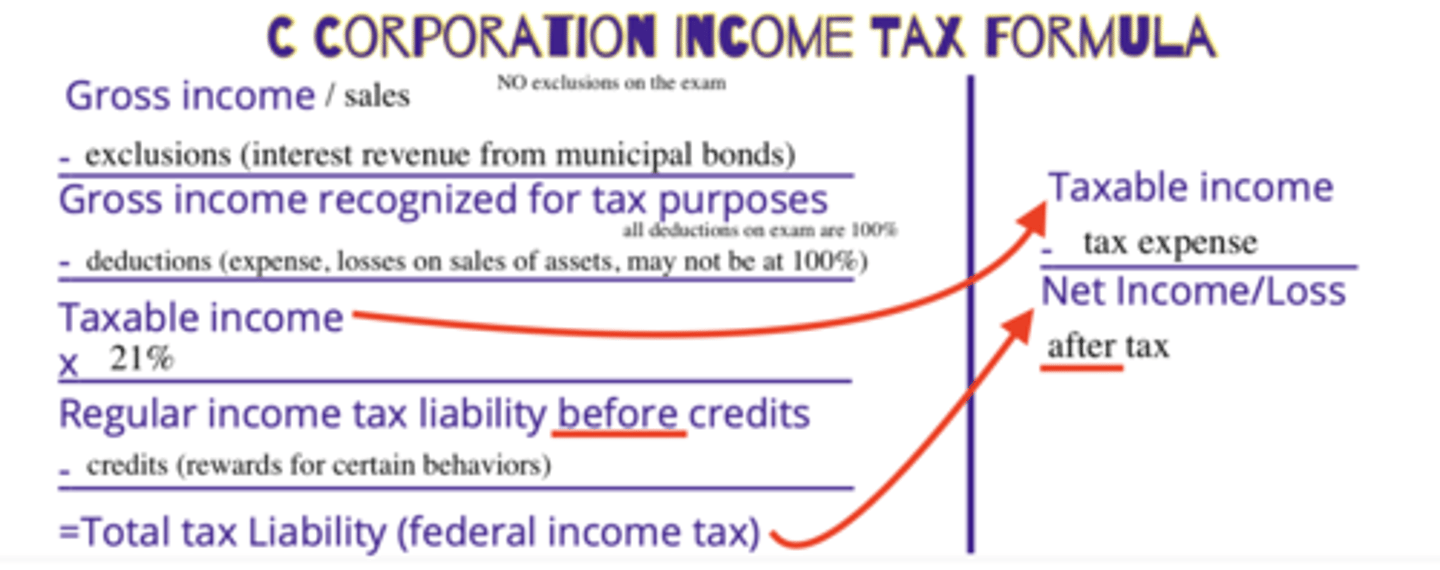

C Corporation Income Tax Formula

Limited Liability Company (LLC)

Earnings "passthrough" to each "members" individaul 1040 Federal Income Tax Return (Schedule C)

Partnership

Earnings "passthrough" to each "partners" individaul 1040 Federal Income Tax Return (Schedule K-1)